Europe Artificial Intelligence (AI) Chip Market Overview - Definition, scope, and significance

The Europe Artificial Intelligence (AI) Chip Market encompasses the design, development, and deployment of specialized semiconductor processors optimized for AI workloads across the European continent. These chips are engineered to accelerate machine learning algorithms, neural network computations, and deep learning processes, offering significantly improved performance compared to traditional general-purpose processors. The market includes various chip architectures such as CPUs, GPUs, ASICs, and FPGAs, each serving distinct AI applications ranging from data center operations to edge computing scenarios. The significance of this market lies in its foundational role in enabling Europe's digital transformation, supporting critical industries including automotive, healthcare, finance, and telecommunications while positioning the region as a competitive player in the global AI technology landscape.

Europe Artificial Intelligence (AI) Chip Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the Europe AI Chip Market include the accelerating adoption of AI technologies across industries, increasing demand for high-performance computing capabilities, and substantial investments in data center infrastructure. The automotive sector's push toward autonomous vehicles and the healthcare industry's adoption of AI-powered diagnostics represent significant growth catalysts. However, the market faces restraints such as high development costs, complex supply chain dependencies, and the shortage of skilled semiconductor engineers. Challenges include intense global competition, particularly from established players in Asia and North America, and the need for continuous innovation to maintain technological leadership. Opportunities exist in the growing edge computing segment, the development of energy-efficient AI chips, and the potential for European companies to establish specialized niches in vertical-specific AI applications.

Europe Artificial Intelligence (AI) Chip Market Growth Trends - Current and emerging trends shaping the market

The Europe AI Chip Market is experiencing several transformative trends that are reshaping its trajectory. There is a clear shift toward heterogeneous computing architectures that combine multiple processing units to optimize AI workloads. Edge AI processing is gaining momentum, driven by the need for real-time inference capabilities in applications such as autonomous vehicles and industrial automation. The market is also witnessing increased focus on energy-efficient chip designs to address sustainability concerns and operational costs. Another notable trend is the rise of open-source hardware initiatives and collaborative research projects between academic institutions and industry players. Additionally, the integration of AI capabilities directly into system-on-chip (SoC) designs is becoming more prevalent, enabling more compact and cost-effective solutions for various applications.

COVID-19 Impact on the Europe Artificial Intelligence (AI) Chip Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the Europe AI Chip Market through supply chain interruptions, delayed product launches, and reduced manufacturing capacity. However, the crisis also accelerated certain market dynamics, particularly the demand for AI-powered healthcare solutions, remote monitoring systems, and automation technologies. The pandemic highlighted the strategic importance of semiconductor sovereignty, prompting European governments to increase investments in domestic chip manufacturing capabilities. The recovery trajectory has been characterized by renewed focus on supply chain resilience, increased government support for semiconductor initiatives, and accelerated digital transformation across industries. The market has shown remarkable adaptability, with companies pivoting toward remote collaboration tools and cloud-based AI solutions to maintain business continuity.

Europe Artificial Intelligence (AI) Chip Market Competitive Landscape - Major competitors and market consolidation

The competitive landscape of the Europe AI Chip Market is characterized by a mix of established semiconductor giants and innovative startups. Major players include Advanced Micro Devices, Intel Corporation, NVIDIA Corporation, and Samsung Electronics, which compete alongside European companies like Graphcore and Axelera AI. The market is witnessing increasing consolidation through strategic partnerships, acquisitions, and joint ventures aimed at strengthening technological capabilities and market presence. Competition is particularly intense in the data center segment, where performance, energy efficiency, and total cost of ownership are critical differentiators. The landscape is further complicated by the entry of non-traditional players from the technology sector, including Google and Huawei, who are developing proprietary AI chip solutions for their specific needs.

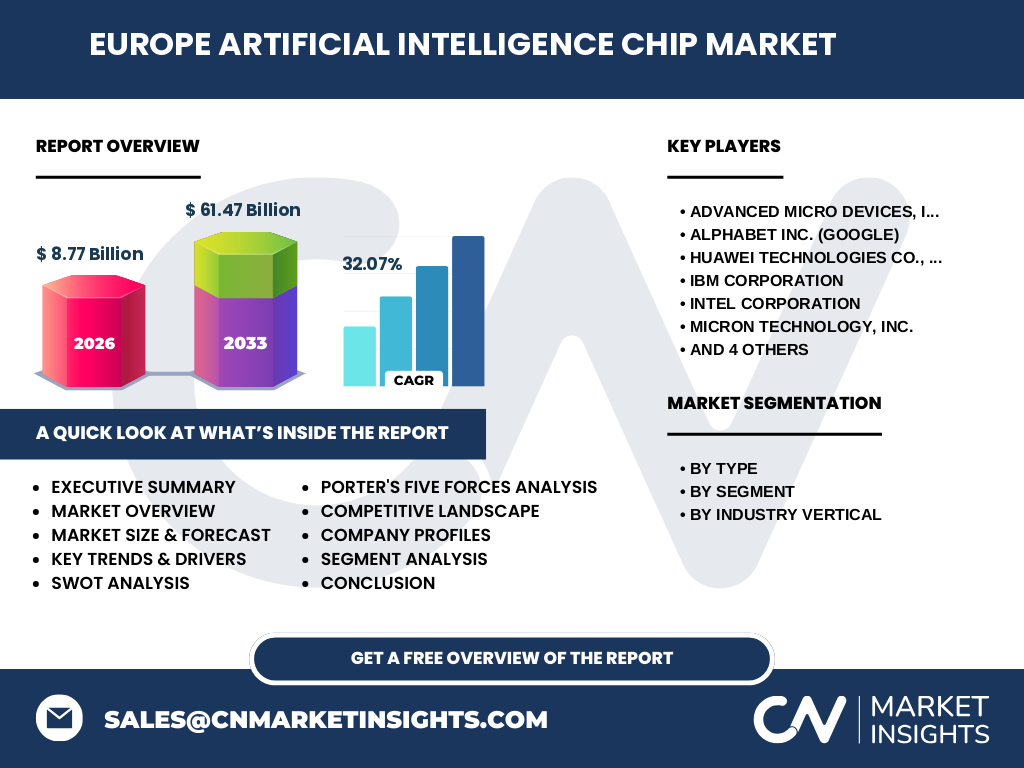

Executive Summary - High-level overview and key findings about Europe Artificial Intelligence (AI) Chip Market

The Europe AI Chip Market is positioned for substantial growth, with market size projected to reach 8.77 Billion by 2026 and expand to 61.47 Billion by 2033, representing a robust CAGR of 32.07%. The market is characterized by diverse segmentation across chip types (CPU, GPU, ASIC, FPGA), deployment segments (Data Center, Edge), and industry verticals (BFSI, Retail, IT & Telecom, Automotive & Transportation, Healthcare, Media & Entertainment). Key findings indicate strong growth potential in edge computing applications, significant opportunities in automotive and healthcare sectors, and increasing demand for specialized AI accelerators. The market faces challenges from global competition and supply chain complexities but benefits from strong government support and increasing investments in semiconductor research and development.

Europe Artificial Intelligence (AI) Chip Market Forecast - Projections for 2025-2032 period

Looking ahead to the 2025-2032 period, the Europe AI Chip Market is expected to maintain its strong growth trajectory, building upon the foundation of 8.77 Billion market size in 2026 and expanding to 61.47 Billion by 2033. This growth will be driven by several factors, including the continued expansion of AI applications across industries, increasing demand for edge computing capabilities, and the evolution of more sophisticated AI algorithms requiring specialized hardware acceleration. The forecast period will likely see accelerated adoption of AI chips in automotive applications, particularly for autonomous driving systems, and increased deployment in healthcare for medical imaging and diagnostic applications. The market will also benefit from ongoing technological advancements that improve performance while reducing power consumption and manufacturing costs.

Europe Artificial Intelligence (AI) Chip Market Size and Share by Segmentation - Breakdown by {segmentData}

The Europe AI Chip Market demonstrates distinct characteristics across its various segments. By chip type, GPUs currently dominate the market due to their versatility in handling diverse AI workloads, followed by ASICs which offer optimized performance for specific applications. In terms of deployment, the data center segment holds the largest share, driven by cloud computing and enterprise AI applications, while the edge segment is experiencing the fastest growth rate. Among industry verticals, the IT & Telecom sector represents the largest market share, followed closely by Automotive & Transportation, which is expected to show the highest growth rate due to the increasing adoption of AI in autonomous vehicles and connected car technologies. The BFSI sector also represents a significant portion of the market, utilizing AI chips for fraud detection and risk assessment applications.

Global Europe Artificial Intelligence (AI) Chip Market Size and Share by Region - Geographic distribution

The Europe AI Chip Market exhibits varied performance across different European regions, with Western European countries including Germany, France, and the United Kingdom leading in terms of market size and technological adoption. These countries benefit from strong industrial bases, significant R&D investments, and established semiconductor ecosystems. Northern European countries are notable for their focus on sustainable and energy-efficient AI chip designs, while Southern European nations are emerging as cost-competitive manufacturing hubs. Eastern European countries are gaining prominence in chip design and testing services, supported by growing technical talent pools. The regional distribution reflects varying levels of technological maturity, industrial focus, and government support across different European markets.

Regional Analysis of the Europe Artificial Intelligence (AI) Chip Market - Detailed regional market performance

A detailed regional analysis reveals distinct market dynamics across European territories. Germany leads the market with its strong automotive industry driving demand for AI chips in autonomous driving applications, supported by robust manufacturing capabilities and engineering expertise. The United Kingdom excels in AI chip design and innovation, particularly in the financial technology and healthcare sectors. France has established itself as a leader in AI research and development, with significant government support for semiconductor initiatives. Nordic countries are focusing on energy-efficient AI chip designs, leveraging their expertise in sustainable technologies. Southern European regions are developing specialized manufacturing capabilities, while Eastern European countries are emerging as important contributors in chip design services and technical support.

Leading Company Profiles in the Europe Artificial Intelligence (AI) Chip Market - Industry players and strategies

The Europe AI Chip Market features several prominent players with distinct strategic approaches. Advanced Micro Devices focuses on high-performance computing solutions and has strengthened its position through strategic acquisitions and partnerships. Intel Corporation maintains a strong presence through its comprehensive portfolio of AI accelerators and investments in European R&D facilities. NVIDIA Corporation dominates the GPU segment and continues to expand its data center solutions. European companies like Graphcore are gaining recognition for their specialized AI processors designed specifically for machine learning workloads. These companies employ various strategies including vertical integration, strategic partnerships, and focus on specific market segments to maintain competitive advantage. Their approaches range from developing proprietary architectures to collaborating with ecosystem partners for comprehensive solutions.

Porter's Five Forces Analysis of the Europe Artificial Intelligence (AI) Chip Market - Competitive forces assessment

Porter's Five Forces analysis reveals a complex competitive environment in the Europe AI Chip Market. The threat of new entrants remains moderate due to high capital requirements and technical expertise needed for chip design and manufacturing. Bargaining power of buyers is increasing as they demand more specialized solutions and better pricing, particularly in the enterprise segment. Suppliers of raw materials and manufacturing equipment hold significant power, influencing production costs and timelines. The threat of substitutes is relatively low as AI chips offer unique performance advantages for machine learning workloads. Competitive rivalry is intense, with both established players and innovative startups competing on performance, energy efficiency, and total cost of ownership. The analysis suggests that companies must focus on differentiation and value creation to maintain market position.

SWOT Analysis of the Europe Artificial Intelligence (AI) Chip Market - Strengths, weaknesses, opportunities, threats

The Europe AI Chip Market demonstrates several key strengths, including strong research and development capabilities, government support for semiconductor initiatives, and a skilled workforce in chip design and engineering. However, weaknesses exist in the form of fragmented market structure and dependence on external manufacturing capabilities. Opportunities abound in emerging applications such as autonomous vehicles, edge computing, and specialized industry solutions. Threats include intense global competition, particularly from Asia-based manufacturers, and potential supply chain disruptions. The market's strengths position it well to capitalize on opportunities, particularly in developing innovative solutions for specific European market needs and establishing leadership in certain AI chip segments.

Europe Artificial Intelligence (AI) Chip Market Value Chain Analysis - Industry structure and value flow

The value chain in the Europe AI Chip Market encompasses several key stages, from semiconductor design and manufacturing to distribution and end-user applications. The design phase involves significant R&D investments and collaboration between chip designers, software developers, and industry partners. Manufacturing relies on complex supply chains and specialized fabrication facilities, with increasing focus on European production capabilities. Distribution channels include direct sales to large enterprises, partnerships with system integrators, and relationships with cloud service providers. Value is created through continuous innovation in chip architecture, optimization for specific AI workloads, and the development of comprehensive software ecosystems. The value chain is becoming increasingly integrated, with companies seeking to control more stages of the process to ensure quality and performance.

Key Investment Insights in the Europe Artificial Intelligence (AI) Chip Market - Strategic investment recommendations

Investment opportunities in the Europe AI Chip Market are particularly promising in several areas. Edge computing applications represent a significant growth area, with increasing demand for AI chips that can process data locally while maintaining energy efficiency. The automotive sector offers substantial investment potential, particularly in chips designed for autonomous driving and advanced driver assistance systems. Healthcare applications, including medical imaging and diagnostic AI, present another attractive investment opportunity. Strategic investments in research and development, particularly in energy-efficient designs and specialized AI accelerators, are likely to yield strong returns. Additionally, investments in manufacturing capabilities and supply chain resilience are becoming increasingly important as the market matures.

Europe Artificial Intelligence (AI) Chip Market Conclusion - Summary and key takeaways

The Europe AI Chip Market presents a compelling growth story, with market size expanding from 8.77 Billion in 2026 to 61.47 Billion by 2033, representing a robust CAGR of 32.07%. The market is characterized by diverse segmentation across chip types, deployment segments, and industry verticals, with significant opportunities in edge computing, automotive applications, and healthcare. While facing challenges from global competition and supply chain complexities, the market benefits from strong government support, technological innovation, and increasing investments in semiconductor capabilities. Success in this market requires a focus on differentiation, strategic partnerships, and continuous innovation to address evolving customer needs and maintain competitive advantage.

Research Methodology - How this research was conducted

This market research was conducted through a comprehensive methodology combining primary and secondary research sources. Primary research involved interviews with industry experts, semiconductor manufacturers, and end-users across various European countries. Secondary research included analysis of financial reports, industry publications, patent filings, and government statistics. The research methodology employed both top-down and bottom-up approaches to validate market size and growth projections. Data triangulation was used to ensure accuracy and reliability of findings. The research also incorporated analysis of market trends, competitive landscape, and regulatory environment to provide a holistic view of the Europe AI Chip Market.

Research Scope - Coverage and limitations

The research scope encompasses the Europe AI Chip Market across all major European countries, covering various chip types (CPU, GPU, ASIC, FPGA), deployment segments (Data Center, Edge), and industry verticals (BFSI, Retail, IT & Telecom, Automotive & Transportation, Healthcare, Media & Entertainment). The study period extends from historical data through 2026 and includes forecasts until 2033. Limitations include the rapidly evolving nature of AI technology, which may impact long-term projections, and the challenge of obtaining precise market share data for certain segments due to the competitive and fragmented nature of the market. The research focuses on commercial AI chip applications and does not extensively cover military or classified applications.

Key Companies and Recent Developments in the Europe Artificial Intelligence (AI) Chip Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Key companies in the Europe AI Chip Market have been actively pursuing various strategic initiatives. Advanced Micro Devices has announced expanded partnerships with European cloud service providers and launched new AI-optimized GPU solutions. Intel Corporation has increased its investment in European R&D facilities and introduced specialized AI accelerators for edge computing applications. NVIDIA Corporation continues to strengthen its position through acquisitions and partnerships, particularly in the automotive and healthcare sectors. European companies like Graphcore have secured significant funding rounds and announced collaborations with major technology partners. Recent developments also include increased government support for semiconductor initiatives, new product launches focused on energy efficiency, and strategic partnerships aimed at strengthening the European AI chip ecosystem.