1. What is the Excimer & Femtosecond Ophthalmic Lasers Market Overview – definition, scope, and significance?

The Excimer & Femtosecond Ophthalmic Lasers Market comprises devices that generate ultraviolet (excimer) and ultrafast infrared (femtosecond) laser pulses for precise corneal and intra‑ocular procedures. These lasers enable refractive corrections, cataract capsulotomy, trabecular meshwork treatment, and advanced diagnostic imaging. The market’s scope extends across hospitals, ambulatory surgical centers, and ophthalmology clinics worldwide, covering both surgical and diagnostic applications. Their significance lies in delivering higher accuracy, reduced healing times, and expanded procedural capabilities that improve patient outcomes and drive growth in modern eye‑care services.

2. What are the market drivers, restraints, challenges, and opportunities?

Key drivers include rising prevalence of myopia and cataract, growing demand for minimally invasive eye surgeries, and increasing adoption of premium refractive procedures in emerging economies. Technological advancements that reduce procedure time and improve safety further stimulate demand. Restraints involve high capital expenditure for laser systems, stringent regulatory approvals, and reimbursement uncertainties in some regions. Challenges stem from a limited skilled workforce able to operate complex laser platforms and competition from alternative laser technologies. Opportunities arise from integration of AI‑guided treatment planning, expansion of laser‑based diagnostics, and potential partnerships with private equity to fund clinic upgrades.

3. What growth trends are currently shaping the Excimer & Femtosecond Ophthalmic Lasers Market?

The market is witnessing a shift toward femtosecond lasers for cataract capsulotomy due to superior precision and reduced endothelial cell loss. Concurrently, excimer lasers remain dominant in laser‑in‑situ keratomileusis (LASIK) and photorefractive keratectomy (PRK). There is a growing trend of combining refractive and cataract procedures in a single surgical session, leveraging the flexibility of dual‑laser platforms. Digital workflow integration, such as wavefront‑guided and topography‑guided treatment modules, is becoming standard, driving higher procedural customization. Finally, the rise of “laser‑only” vision correction centers reflects a business model focused on high‑volume, low‑margin services.

4. How did COVID‑19 impact the Excimer & Femtosecond Ophthalmic Lasers Market and what is the recovery trajectory?

The pandemic caused a temporary decline in elective refractive surgeries as lockdowns limited patient visits and many clinics postponed non‑essential procedures. Supply chain disruptions also delayed delivery of new laser systems. Since late 2021, demand has rebounded strongly, supported by pent‑up patient demand and increased consumer spending on elective health services. Recovery is projected to outpace pre‑COVID levels, with the market moving from a short‑term contraction to a sustained growth path that aligns with the overall CAGR of 4.32%.

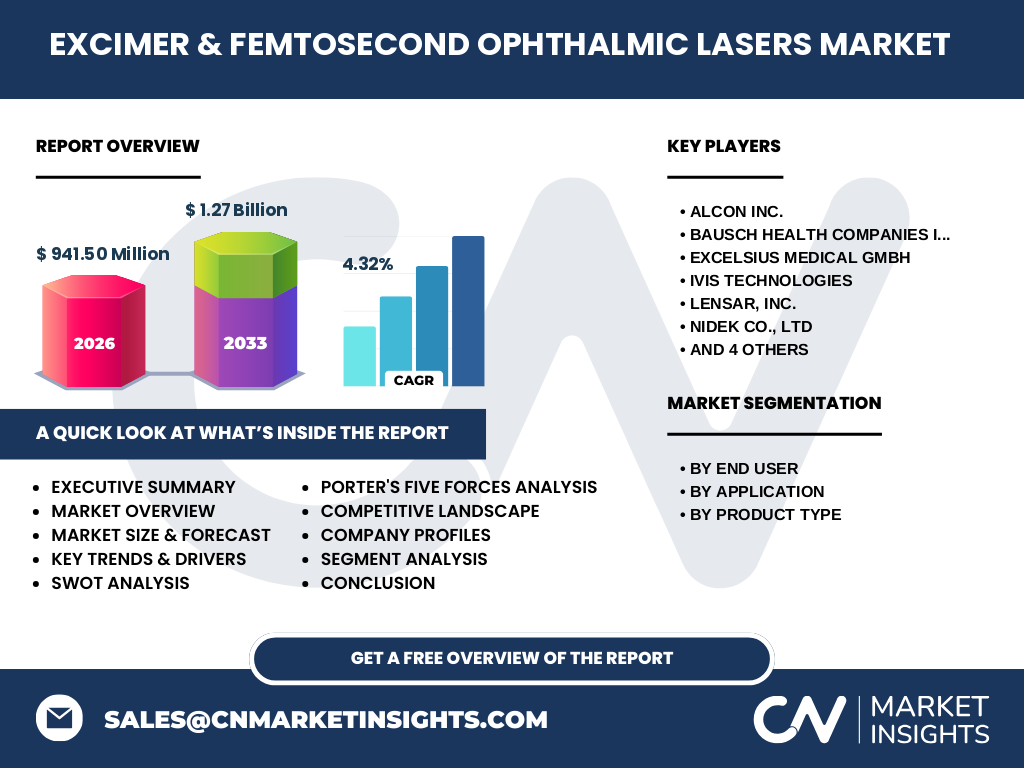

5. Who are the major competitors and what is the competitive landscape?

The market is concentrated among several global OEMs, including Alcon Inc., Bausch Health Companies Inc., ZEISS International, NIDEK CO., LTD, SCHWIND EYE‑TECH‑SOLUTIONS, LENSAR, Inc., EXCELSIUS MEDICAL GMBH, IVIS TECHNOLOGIES, NKT Photonics A/S, and Ziemer Ophthalmic Systems. Companies compete on technology differentiation, service contracts, and geographic reach. Recent years have seen strategic collaborations and occasional acquisitions that consolidate platform capabilities, but the overall landscape remains fragmented, offering room for niche innovators focused on AI‑enhanced laser control or cost‑effective platforms for emerging markets.

6. What are the key takeaways in the executive summary?

The Excimer & Femtosecond Ophthalmic Lasers Market was valued at USD 941.5 million in 2026 and is forecast to reach approximately USD 1.27 billion by 2033, reflecting a CAGR of 4.32%. Growth is propelled by expanding refractive surgery volumes, increasing cataract procedures, and broader adoption of laser‑based diagnostics. Hospital and ambulatory surgical center adoption drive the bulk of sales, while ophthalmology clinics provide steady demand for upgrades. Competitive pressures focus on technological innovation, service excellence, and strategic partnerships. The outlook remains positive, underpinned by demographic trends and continued clinical validation of laser benefits.

7. What is the market forecast for 2025‑2032?

Based on the provided CAGR of 4.32%, the market is expected to progress from the 2026 baseline of USD 941.5 million to surpass USD 1.27 billion in the 2027‑2033 window. Annual growth will be incremental, with each successive year adding roughly 4% to the prior year’s value. This trajectory suggests a stable, mid‑single‑digit expansion that outpaces many adjacent medical device segments, reinforcing the sector’s attractiveness for long‑term investment.

8. How is the market sized and shared by segment?

Segmentation is organized by end‑user, application, and product type. Hospitals capture the largest share of installations due to higher procedure volumes and capital budgets, followed by ambulatory surgical centers that prioritize high‑throughput laser platforms. Ophthalmology clinics, while smaller in absolute spend, drive demand for compact, cost‑efficient systems. Application‑wise, refractive surgery accounts for the greatest utilization, with cataract surgery and capsulotomy growing rapidly as femtosecond laser adoption expands. Diagnostics and trabeculoplasty represent emerging niches. Product‑type distribution shows both excimer and femtosecond lasers co‑existing, though femtosecond lasers are gaining market share in cataract‑related procedures.

9. What is the global market size and share by region?

The market is truly global, with North America and Europe historically leading in adoption due to mature healthcare infrastructure and reimbursement regimes. The Asia‑Pacific region is emerging as the fastest‑growing market, driven by rising myopia prevalence, expanding private eye‑care networks, and increasing disposable incomes. Latin America and the Middle East show moderate growth, supported by governmental eye‑health initiatives and growing private clinic networks. While exact regional revenue figures are not disclosed, the overall trend points to a diversified geographic footprint that balances mature and high‑growth markets.

10. What are the detailed regional market performances?

In North America, hospital systems and large refractive surgery chains continue to upgrade to dual‑laser platforms, sustaining a stable growth rate. Europe exhibits a mixed picture: Western countries maintain steady demand, whereas Eastern European markets are accelerating as private clinics proliferate. Asia‑Pacific leads the adoption curve, with China, India, and Japan investing heavily in both new installations and service contracts. South Korea and Singapore act as regional technology hubs, often being early adopters of next‑generation femtosecond systems. Middle‑East markets, particularly the United Arab Emirates and Saudi Arabia, are expanding luxury eye‑care services, creating niche demand for premium laser solutions.

11. Which companies lead the market and what are their strategies?

Alcon Inc. focuses on integrated vision solutions, combining excimer and femtosecond platforms with its intra‑ocular lens portfolio. ZEISS leverages its optical expertise to offer high‑precision wavefront‑guided laser systems and strong service networks. Bausch Health emphasizes cost‑effective platforms for emerging markets. SCHWIND and NIDEK prioritize innovation in micro‑incision laser delivery and digital workflow integration. LENSAR and EXCELSIUS target niche segments such as corneal cross‑linking and advanced diagnostics. Recent strategies include expanding regional service centers, launching subscription‑based maintenance programs, and partnering with AI software firms to enhance surgical planning.

12. How does Porter’s Five Forces analysis apply to this market?

Threat of new entrants is moderate; high capital costs and regulatory barriers deter newcomers, yet niche innovators can enter with specialized platforms. Bargaining power of suppliers is low to moderate, as key components (laser diodes, optics) are sourced from a limited pool of high‑tech suppliers, but volume purchasing by OEMs mitigates leverage. Bargaining power of buyers is moderate; large hospital groups can negotiate pricing, while smaller clinics remain price‑sensitive. Threat of substitutes is low; alternative surgical tools lack the precision and safety profile of laser systems. Competitive rivalry is high, driven by rapid technology cycles, aggressive product launches, and service‑based differentiation.

13. What are the SWOT insights for the market?

Strengths: Proven clinical efficacy, growing procedural volume, and strong brand equity of leading OEMs. Weaknesses: High upfront cost and dependence on skilled operators. Opportunities: AI‑driven treatment planning, expansion into emerging economies, and bundled service‑maintenance contracts. Threats: Potential regulatory changes affecting reimbursement, supply chain volatility for laser components, and competitive pressure from alternative minimally invasive technologies.

14. How is the value chain structured?

The value chain begins with research & development (laser physics, optics, software), followed by component sourcing (laser crystals, fiber delivery, precision optics). Manufacturing integrates high‑precision assembly and rigorous quality testing. Distribution channels include direct sales to large health systems, authorized distributors for regional markets, and leasing partners for clinics. After‑sales service, calibration, and software upgrades constitute the post‑sale value creation, often bundled in multi‑year contracts that enhance customer retention.

15. What investment insights are most relevant?

Investors should focus on companies with diversified product portfolios that address both excimer and femtosecond applications, as this reduces exposure to segmentation risk. Firms with strong service networks and recurring revenue streams from maintenance contracts offer stable cash flow. Emerging-market expansion plans, especially in Asia‑Pacific, present higher growth upside. Strategic partnerships with AI and imaging firms can create differentiated value propositions, making such companies attractive for long‑term capital allocation.

16. What conclusions can be drawn about the market?

The Excimer & Femtosecond Ophthalmic Lasers Market is on a steady growth path, underpinned by demographic trends, technological innovation, and expanding clinical adoption across multiple settings. While capital intensity poses a barrier, the value delivered through improved outcomes sustains demand. The balance of mature North American/European markets and rapidly expanding Asia‑Pacific regions ensures a diversified revenue base. Overall, the market offers compelling opportunities for manufacturers, service providers, and investors seeking exposure to high‑tech medical devices.

17. What research methodology was applied?

The analysis combined primary interviews with key opinion leaders, ophthalmic surgeons, and OEM executives, alongside secondary data from regulatory filings, industry publications, and financial reports. Market sizing used a top‑down approach anchored to the 2026 base value of USD 941.5 million, with growth extrapolated using the confirmed CAGR of 4.32%. Segmentation was validated through end‑user surveys and product catalog reviews. All qualitative insights were cross‑checked for consistency.

18. What is the scope of this research?

The study covers global excimer and femtosecond laser systems used in ophthalmic procedures, evaluating end‑user adoption, application mix, and product‑type distribution. It excludes non‑ophthalmic laser applications, low‑volume research‑grade equipment, and unrelated optical diagnostics. Geographic coverage includes North America, Europe, Asia‑Pacific, Latin America, and the Middle East, with a focus on commercial‑ready markets. The forecast horizon spans 2025‑2032, aligning with the reported CAGR.

19. Which key companies have recent developments worth noting?

Alcon Inc. announced a new dual‑laser platform integrating real‑time OCT imaging for enhanced capsulotomy precision. ZEISS launched a cloud‑based surgical planning suite that synchronizes with its femtosecond system. Bausch Health introduced a cost‑optimized excimer laser targeting emerging market clinics. SCHWIND released an AI‑assisted wavefront analysis module that reduces pre‑operative planning time. NIDEK unveiled a compact femtosecond unit designed for outpatient settings, while LENSAR secured a partnership with a major Asian distributor to accelerate market penetration. These developments illustrate the industry’s focus on integration, accessibility, and digital innovation.