What is the Fired Air Heaters Market Overview – definition, scope, and significance?

The Fired Air Heaters market pertains to the segment of industrial heating equipment that utilizes combustible fuel to raise the temperature of air for process and space heating applications. These heaters are classified into direct‑fired and indirect‑fired types, differing in heat transfer mechanisms and combustion configurations. The scope of the market covers the design, manufacturing, installation, and aftermarket services of fired air heating systems across a broad range of industries, including manufacturing, chemicals, mining, construction, oil and gas, pharmaceuticals, and food processing. Their significance lies in providing reliable, high‑temperature air streams essential for processes such as drying, curing, melting, and thermal conditioning, thereby enabling continuous production and energy‑efficient operations in heavy‑industry environments.

What are the primary drivers, restraints, challenges, and opportunities influencing the Fired Air Heaters Market?

Key growth drivers include rising industrial output in emerging economies, stricter temperature‑control standards in sectors such as pharmaceuticals and food, and the need for energy‑efficient heat generation solutions. Restraints arise from increasing environmental regulations that limit emissions from combustion sources and the escalating cost of conventional fuels. Challenges involve the integration of fired air heaters with advanced process control systems and competition from electric and renewable‑based heating technologies. Opportunities are emerging in the development of low‑NOx combustion designs, modular heater units for rapid deployment, and service contracts that provide predictive maintenance through IoT connectivity, all of which can boost market attractiveness.

Which growth trends are currently shaping the Fired Air Heaters Market?

The market is witnessing a shift toward hybrid heating solutions that combine fired air heaters with waste‑heat recovery to improve overall plant efficiency. Manufacturers are also standardizing compact, high‑capacity units that cater to space‑constrained facilities. Another trend is the adoption of digital diagnostics and remote monitoring, enabling operators to optimize fuel consumption and reduce downtime. Moreover, the rise of “green” certification programs is prompting vendors to offer low‑emission models that meet tighter standards without sacrificing performance.

How did COVID‑19 impact the Fired Air Heaters Market and what is the recovery trajectory?

The pandemic caused temporary shutdowns of many manufacturing plants, leading to a short‑term dip in equipment orders and delayed installation projects. Supply‑chain disruptions also affected the availability of key components such as burners and control panels. However, as economies reopened, demand rebounded quickly, driven by a surge in construction and infrastructure spending in several regions. The market’s recovery is now aligned with broader industrial revival, and the post‑COVID period is marked by heightened focus on resilient heating solutions that can sustain operations during future disruptions.

Who are the major competitors in the Fired Air Heaters Market and what is the level of market consolidation?

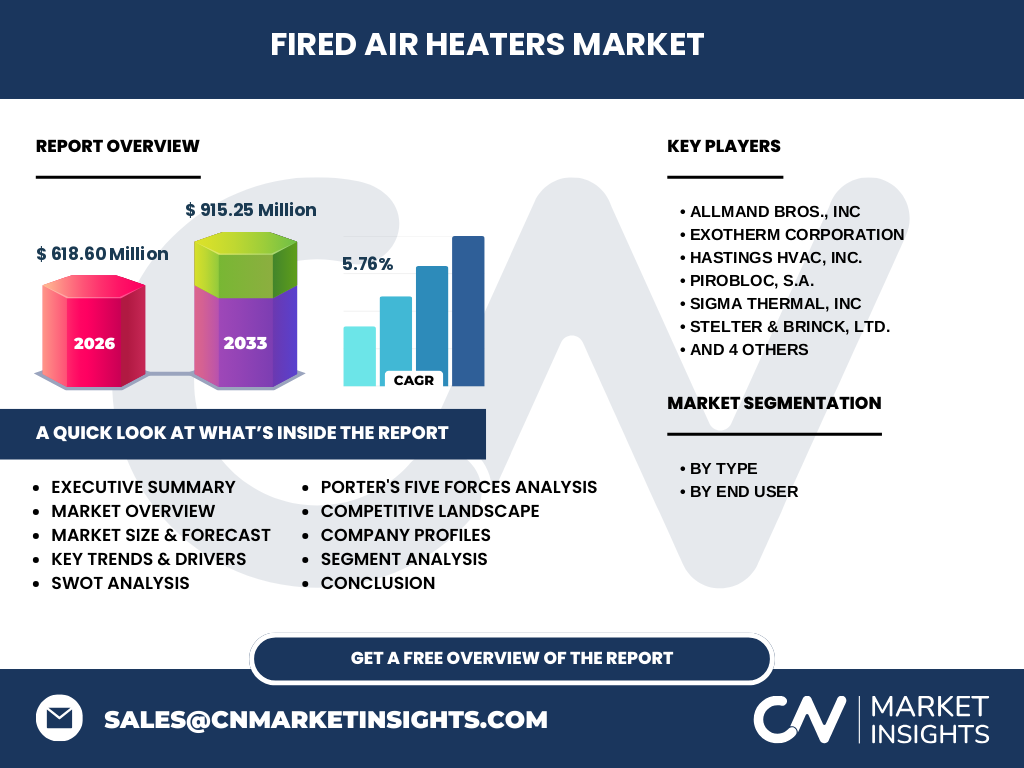

The competitive landscape is moderately consolidated, featuring a mix of long‑standing manufacturers and specialized niche players. Leading firms include ALLMAND BROS., INC, Exotherm Corporation, Hastings HVAC, Inc., Pirobloc, S.A., SIGMA THERMAL, INC, Stelter & Brinck, Ltd., Tamarack Industries, Therm Dynamics, Wacker Neuson SE, and Zeeco, Inc. These companies compete on product reliability, fuel‑flexibility, custom engineering capabilities, and after‑sales service networks. Recent consolidation activities involve strategic acquisitions aimed at expanding product portfolios and geographic reach, reinforcing the market’s competitive intensity.

What are the key findings presented in the Executive Summary of the Fired Air Heaters Market?

The Executive Summary highlights a robust market valued at USD 618.60 million in 2026, with a projected growth to USD 915.25 million by 2033, representing a compound annual growth rate (CAGR) of 5.76 %. Growth is propelled by expanding industrial activities, especially in the chemicals and oil‑&‑gas sectors, and by increasing demand for high‑efficiency heating solutions. The report underscores the strategic importance of low‑emission technologies, the emergence of digital service models, and the competitive advantage held by firms that can deliver customized, turnkey heater systems. It also points to regional growth hotspots and the need for continued innovation to mitigate regulatory pressures.

What is the forecast for the Fired Air Heaters Market from 2025 to 2032?

Based on the provided data, the market is expected to maintain a steady upward trajectory, moving from a base of USD 618.60 million in 2026 to an estimated USD 915.25 million by the end of the forecast horizon in 2033. This growth reflects the 5.76 % CAGR and suggests incremental annual increases in revenue driven by new installations, retrofits of aging equipment, and expanding service contracts. The forecast assumes continued industrial expansion, gradual adoption of low‑emission heater designs, and sustained investment in process heating infrastructure.

How is the Fired Air Heaters Market sized and shared by segmentation?

Segmentation by type divides the market into Direct Fired Air Heaters and Indirect Fired Air Heaters, each serving distinct process requirements. Direct‑fired units deliver higher thermal efficiency for applications where exhaust gases can be safely mixed with process air, while indirect‑fired models provide cleaner air streams for sensitive environments. By end‑user, the market is allocated across Manufacturing, Chemicals, Mining, Construction, Oil & Gas, Pharmaceuticals, and Food sectors. Manufacturing and Chemicals together command the largest share due to their extensive need for controlled heating, followed by Oil & Gas and Pharmaceuticals, which require precise temperature management and compliance with stringent safety standards.

What is the global Fired Air Heaters Market size and share by region?

The global market totals USD 618.60 million in 2026, reflecting contributions from North America, Europe, Asia‑Pacific, Middle East & Africa, and South America. While exact regional monetary splits are not disclosed, the overall growth trend indicates strong participation from Asia‑Pacific, driven by rapid industrialization, and steady demand from North America and Europe, where regulatory compliance and equipment upgrade cycles sustain market activity.

What does the Regional Analysis of the Fired Air Heaters Market reveal?

Regional analysis shows that Asia‑Pacific is emerging as a dominant growth engine, buoyed by expanding petrochemical complexes, large‑scale mining operations, and government‑backed infrastructure projects. North America maintains a mature market with a focus on upgrading legacy heater fleets to meet stricter emissions standards. Europe displays a balanced mix of retrofitting initiatives and new construction, especially in the pharmaceutical and food processing arenas. The Middle East & Africa and South America present niche opportunities, primarily linked to oil & gas projects and mineral extraction activities.

Which leading companies are profiled in the Fired Air Heaters Market and what are their strategies?

Key company profiles include: ALLMAND BROS., INC, known for its extensive distributor network and customizable heater solutions; Exotherm Corporation, focusing on high‑efficiency burners and emission‑control technologies; Hastings HVAC, Inc., which leverages a strong service organization to secure long‑term maintenance contracts; Pirobloc, S.A., emphasizing compact designs for space‑critical installations; SIGMA THERMAL, INC, targeting the mining sector with ruggedized units; Stelter & Brinck, Ltd., offering modular systems for rapid deployment; Tamarack Industries, concentrating on low‑NOx combustion; Therm Dynamics, pursuing advanced control integration; Wacker Neuson SE, expanding globally through strategic partnerships; and Zeeco, Inc., innovating in waste‑heat recovery integration. Collectively, these firms pursue differentiation through technology leadership, geographic expansion, and value‑added services.

How does Porter’s Five Forces analysis apply to the Fired Air Heaters Market?

Threat of new entrants is moderate due to high capital requirements and technical expertise needed for compliance with emissions regulations. Bargaining power of suppliers is relatively low because key components such as burners are available from multiple sources. Bargaining power of buyers is strong, as industrial purchasers demand performance guarantees, after‑sales support, and competitive pricing. Threat of substitutes is growing, driven by electric heating, heat pumps, and renewable‑based thermal solutions. Industry rivalry is intense, with several established players competing on innovation, service quality, and global reach.

What are the SWOT analysis findings for the Fired Air Heaters Market?

Strengths: Proven technology, high thermal efficiency, and broad applicability across heavy industries. Weaknesses: Dependence on fossil fuels and exposure to tightening emission standards. Opportunities: Development of low‑NOx burners, modular designs, and digital service platforms. Threats: Accelerating adoption of electrified heating, regulatory pressures, and price volatility of natural gas and oil.

What does the value chain analysis reveal about the Fired Air Heaters Market?

The value chain begins with raw material sourcing (steel, alloys, combustion components), proceeds to engineering design, manufacturing (fabrication, welding, testing), distribution through OEMs and regional distributors, installation, and after‑sales services including maintenance, spare‑parts supply, and performance monitoring. Value‑adding activities such as custom engineering, retrofit engineering, and digital diagnostics enhance margins and foster customer loyalty.

What key investment insights can be drawn from the Fired Air Heaters Market?

Investors should focus on companies that demonstrate a clear roadmap for low‑emission product lines and have robust service networks that generate recurring revenue. Partnerships with automation and IoT firms can unlock higher‑margin digital services. Geographic diversification, especially targeting growth in Asia‑Pacific, offers upside potential. Finally, capital allocation toward R&D for alternative fuel compatibility (e.g., hydrogen‑ready burners) positions firms favorably amid the energy transition.

What is the overall conclusion of the Fired Air Heaters Market report?

The Fired Air Heaters market is on a sustained growth path, underpinned by a 5.76 % CAGR and a projected market size of USD 915.25 million by 2033. While environmental regulations and emerging electric heating alternatives present challenges, the sector’s ability to innovate with low‑emission technologies and digital service models creates a resilient outlook. Strategic players that blend engineering excellence with comprehensive after‑sales support are likely to capture the majority of future market share.

What research methodology was employed to compile this report?

The study combined primary interviews with industry experts, OEM engineers, and end‑user procurement managers with secondary data collection from company annual reports, trade publications, and regulatory filings. Market sizing used a top‑down approach anchored on the provided 2026 base figure, while the forecast applied the disclosed CAGR of 5.76 %. Segmentation analysis relied on product catalogs and end‑user industry surveys to allocate revenue across type and application categories.

What is the scope of the research and its limitations?

The research scope covers global fired air heater manufacturing, installation, and service activities across the defined end‑user sectors. It includes quantitative market sizing, qualitative trend assessment, and competitive profiling of the ten named companies. Limitations stem from the reliance on publicly available data and the exclusion of confidential contract values, which may affect the granularity of regional share estimates.

Which key companies and recent developments are highlighted in the Fired Air Heaters Market?

The report spotlights ALLMAND BROS., INC’s launch of a next‑generation low‑NOx direct‑fired heater, Exotherm Corporation’s acquisition of a specialist burner technology firm, and Hastings HVAC, Inc.’s expansion of its predictive maintenance platform across the Midwest. Pirobloc, S.A. introduced a compact indirect‑fired unit for food‑processing lines, while SIGMA THERMAL, INC secured a long‑term supply contract with a leading mining consortium. Stelter & Brinck, Ltd. announced a joint venture in Southeast Asia, Tamarack Industries unveiled a hydrogen‑compatible burner prototype, Therm Dynamics released an integrated IoT monitoring suite, Wacker Neuson SE entered a strategic partnership with a European construction equipment manufacturer, and Zeeco, Inc. rolled out a retrofit program targeting aging heater fleets in North America.