What is the Saudi Arabia Liquid Filtration Market Overview – definition, scope, and significance?

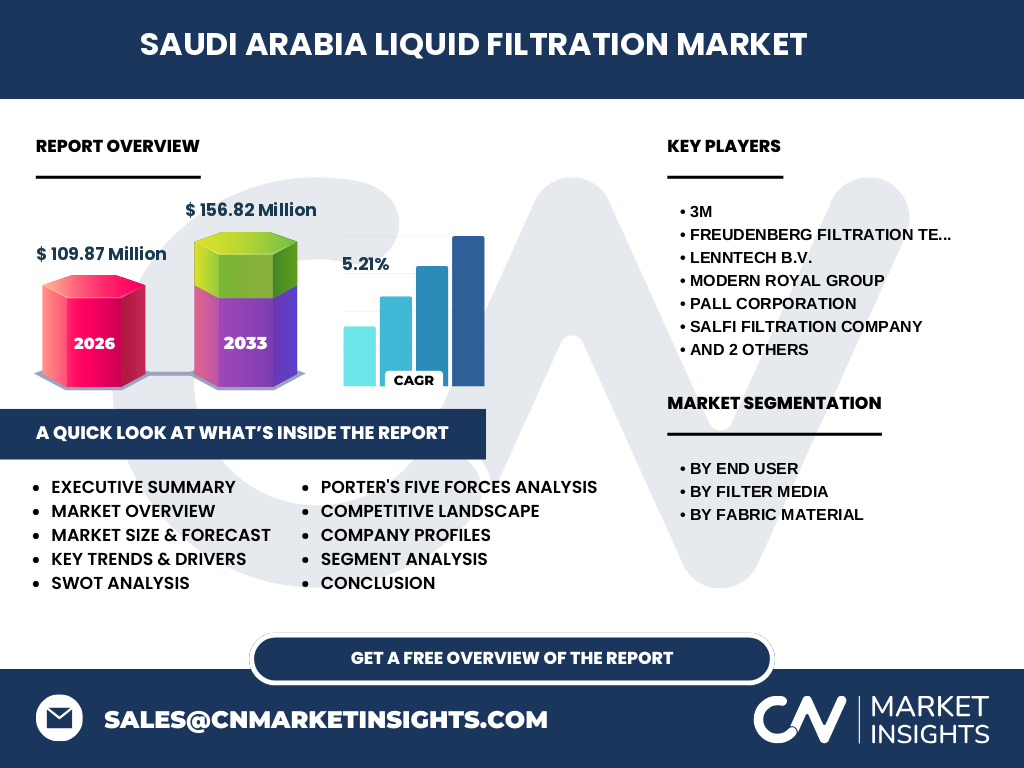

The Saudi Arabia Liquid Filtration Market encompasses all technologies, products, and services used to remove contaminants from liquids across municipal and industrial applications. It includes filtration media such as woven, non‑woven, and mesh fabrics, fabricated from polymer, cotton, or metal materials. The market’s significance stems from Saudi Arabia’s rapidly expanding water‑treatment infrastructure, aggressive industrial diversification under Vision 2030, and growing demand for high‑purity process water in sectors such as petrochemicals, power generation, and desalination. With a 2026 market size of USD 109.87 million, the sector plays a critical role in safeguarding public health, supporting economic growth, and ensuring compliance with increasingly stringent environmental regulations.

What are the key drivers, restraints, challenges, and opportunities shaping the Saudi Arabia Liquid Filtration Market?

Key drivers include massive government investment in water‑treatment plants, the need for reliable wastewater recycling in oil‑and‑gas operations, and the rise of industrial zones that demand advanced filtration solutions. Restraints involve high capital expenditure for large‑scale filtration installations and a limited number of locally manufactured filter media, which can increase dependence on imports. Challenges arise from fluctuating raw material costs for polymer‑based filters and the technical complexity of integrating filtration systems with existing plant infrastructure. Opportunities are emerging in the development of sustainable, low‑energy filter media, digital monitoring of filter performance, and niche applications such as pharmaceutical‑grade water purification, where Saudi Arabia’s expanding healthcare sector creates additional demand.

What are the current growth trends in the Saudi Arabia Liquid Filtration Market?

Current trends highlight a shift toward high‑efficiency, low‑maintenance filtration technologies, especially non‑woven polymer membranes that offer superior contaminant capture with reduced pressure drop. There is increasing adoption of modular filtration units that allow rapid scaling in response to demand spikes. Digitalization is another emerging trend, with sensors and IoT platforms being integrated to provide real‑time monitoring of filter integrity and lifespan, thus optimizing maintenance schedules. Finally, the market is seeing growing collaboration between local distributors and international manufacturers to localize production of filter components, aligning with the Kingdom’s “Made in Saudi” industrial policy.

How did COVID‑19 impact the Saudi Arabia Liquid Filtration Market, and what is the recovery trajectory?

The pandemic initially slowed new project approvals due to delayed financing and supply‑chain disruptions, reducing short‑term demand for large‑scale filtration equipment. However, heightened awareness of hygiene and water safety spurred increased procurement of municipal treatment filters to assure safe drinking water. By late 2021, government stimulus packages and renewed focus on infrastructure revitalized the market. Recovery is now well underway, with demand accelerating as the Kingdom pursues ambitious water‑security projects and the forecasted CAGR of 5.21% reflects confidence in sustained growth through 2032.

Who are the major competitors, and how is the market consolidating in Saudi Arabia?

The competitive landscape is dominated by a mix of global leaders and regional specialists. Key players include 3M, Freudenberg Filtration Technologies SE and Co. KG, Lenntech B.V., Modern Royal Group, Pall Corporation, Salfi Filtration Company, Sandler AG, and Wetico. These firms compete on technology innovation, product reliability, and service networks. Recent consolidation activities involve strategic partnerships and joint ventures aimed at expanding local manufacturing capabilities, reducing lead times, and enhancing after‑sales support. The market is moving toward fewer, larger players with broader product portfolios, which intensifies competition on value‑added services rather than price alone.

What are the high‑level findings highlighted in the executive summary?

The Saudi Arabia Liquid Filtration Market is poised for steady expansion, reaching an estimated USD 156.82 million by 2033, driven by Vision 2030 infrastructure initiatives and robust industrial growth. A 5.21 % CAGR underscores resilient demand across municipal and industrial end‑users. Non‑woven polymer media and digital filtration monitoring are identified as the fastest‑growing segments. While capital intensity and import reliance pose challenges, opportunities abound in localized production, sustainable filter materials, and advanced analytics. The competitive environment is shaping toward strategic alliances, positioning the market for continued innovation and value creation.

What are the forecast expectations for the Saudi Arabia Liquid Filtration Market from 2025 to 2032?

Based on the provided CAGR of 5.21 %, the market is projected to grow from the 2026 baseline of USD 109.87 million to approximately USD 156.82 million by 2033. This trajectory suggests a consistent upward trend throughout the 2025‑2032 horizon, with annual growth driven by expanding municipal water‑treatment projects, increased industrial water recycling initiatives, and the adoption of higher‑efficiency filter media. The forecast reflects a balanced mix of organic growth and incremental market share gains among leading manufacturers.

How is the market size and share distributed across the defined segments?

The market is segmented by end‑user, filter media, and fabric material. End‑user segmentation divides demand between municipal treatment and industrial treatment, with both segments showing robust growth, although industrial applications often require higher‑specification filters for process water. By filter media, woven, non‑woven, and mesh fabrics compete, with non‑woven polymer media gaining the largest share due to its superior performance and lower maintenance. Fabric material segmentation includes polymer, cotton, and metal, where polymer dominates because of its durability, chemical resistance, and adaptability to various filtration designs. While exact percentages are not disclosed, the segment hierarchy follows: Industrial > Municipal, Non‑woven > Woven > Mesh, and Polymer > Cotton > Metal.

What is the geographic distribution of the Saudi Arabia Liquid Filtration Market on a global scale?

Within the global context, Saudi Arabia represents a significant Middle‑East hub for liquid filtration, driven primarily by its domestic water‑security agenda and petrochemical complex concentration. The Kingdom’s market contributes a notable portion of regional demand, complemented by neighboring GCC countries that import similar filtration technologies. Though specific regional market shares are unavailable, Saudi Arabia’s strategic initiatives place it among the leading Middle‑East markets for filtration solutions.

How does the regional analysis of the Saudi Arabia Liquid Filtration Market break down performance?

Regionally, the Kingdom’s western province (Makkah and Madinah) shows strong municipal filtration activity due to urban population growth and tourism‑related water usage. The Eastern Province, home to the oil and gas corridor, dominates industrial treatment demand, requiring high‑purity water for refining and petrochemical processes. Central Saudi Arabia, including Riyadh, reflects a balanced mix of municipal upgrades and emerging industrial parks, driving diversified filter media adoption. These regional dynamics influence supplier logistics, with distributors establishing localized inventories to meet distinct regional requirements efficiently.

Who are the leading companies operating in the Saudi Arabia Liquid Filtration Market and what are their strategies?

The leading companies—3M, Freudenberg Filtration Technologies, Lenntech, Modern Royal Group, Pall Corporation, Salfi Filtration Company, Sandler AG, and Wetico—focus on technology leadership, localized service, and portfolio breadth. 3M leverages its extensive R&D to introduce high‑performance membrane filters. Freudenberg emphasizes sustainable polymer media. Lenntech provides turnkey water‑treatment solutions with integrated filtration. Modern Royal Group and Salfi focus on regional distribution networks and after‑sales support. Pall Corporation expands its presence through advanced bio‑filtration systems for pharmaceutical applications. Sandler AG and Wetico pursue niche market segments such as high‑temperature metal filters and modular filtration units. Collaborative ventures and local manufacturing are common strategic themes.

What does Porter’s Five Forces analysis reveal about the Saudi Arabia Liquid Filtration Market?

• Bargaining Power of Buyers: Moderate to high, as large municipal utilities and industrial conglomerates can negotiate favorable terms and demand customized solutions.

• Bargaining Power of Suppliers: Moderate, given the reliance on specialized polymer resin and precision‑engineered fabrics, which are sourced from a limited global supplier base.

• Threat of New Entrants: Low to moderate, due to high capital requirements, stringent regulatory standards, and the technical expertise needed for filter media development.

• Threat of Substitutes: Low, because liquid filtration remains the most effective method for contaminant removal in both municipal and industrial contexts.

• Industry Rivalry: High, driven by a concentrated set of global and regional players competing on technology, service reliability, and price optimization.

What are the SWOT findings for the Saudi Arabia Liquid Filtration Market?

Strengths: Strong government backing, increasing water‑security investments, and presence of world‑class technology providers.

Weaknesses: Dependence on imported filter media, high upfront capital costs, and limited local R&D capacity.

Opportunities: Development of locally produced sustainable polymer filters, digital monitoring solutions, and expansion into high‑purity sectors like pharma and food‑beverage.

Threats: Volatile raw‑material prices, potential regulatory changes tightening environmental standards, and geopolitical risks affecting import logistics.

How is the value chain structured for the Saudi Arabia Liquid Filtration Market?

The value chain begins with raw‑material suppliers (polymer resin, metal fibers, cotton), progresses to filter‑media manufacturers (woven, non‑woven, mesh fabric producers), then to system integrators who design and assemble filtration units for specific end‑users. Distributors and local service partners provide logistics, installation, and maintenance. End‑users—municipal water authorities and industrial plants—consume the final product and generate feedback that drives R&D for next‑generation filters. Value‑added services such as performance monitoring, filter‑change scheduling, and training constitute the higher‑margin segment of the chain.

What investment insights are most relevant for stakeholders in the Saudi Arabia Liquid Filtration Market?

Investors should prioritize assets that enable local production of polymer‑based non‑woven media, aligning with the Kingdom’s “localization” agenda and reducing supply‑chain exposure. Funding digital platform providers that offer real‑time filter performance analytics presents a high‑growth opportunity. Joint ventures with established global manufacturers can accelerate technology transfer while leveraging existing distribution networks. Lastly, targeting niche high‑purity markets—pharmaceutical water systems, food‑processing plants—offers premium pricing and lower price‑elasticity.

What are the concluding takeaways from this market research?

The Saudi Arabia Liquid Filtration Market is on a clear growth path, underpinned by Vision 2030 water‑security priorities and industrial diversification. A 5.21 % CAGR leads to a projected market size of USD 156.82 million by 2033. Non‑woven polymer filters and digital monitoring are the primary growth engines. While capital intensity and import reliance pose challenges, strategic localization, sustainable material development, and advanced analytics provide compelling avenues for value creation. Competitive dynamics favor firms that combine technology leadership with strong local service capabilities.

What research methodology was employed to compile this market report?

The study used a mixed‑method approach, combining secondary data collection from industry publications, government reports, and company disclosures with primary interviews of key stakeholders, including municipal water authorities, industrial plant engineers, and senior executives from leading filtration firms. Quantitative data were validated through cross‑checking with market databases, and qualitative insights were synthesized to develop the trend analysis, forecasting model, and strategic assessments presented herein.

What is the scope of this research, and what limitations should readers be aware of?

The research scope covers the Saudi Arabian liquid filtration market from 2025 through 2032, focusing on municipal and industrial end‑users, filter‑media types (woven, non‑woven, mesh), and fabric materials (polymer, cotton, metal). It excludes downstream applications such as solid‑waste filtration and air filtration. Geographic analysis is limited to Saudi Arabia within the broader Middle‑East context; detailed country‑by‑country breakdowns for neighboring markets are not provided. Financial figures are based on publicly available data and the supplied market size and forecast values.

Which key companies are highlighted, and what recent developments have they announced?

Leading companies include 3M, Freudenberg Filtration Technologies SE and Co. KG, Lenntech B.V., Modern Royal Group, Pall Corporation, Salfi Filtration Company, Sandler AG, and Wetico. Recent developments comprise 3M’s launch of a next‑generation polymer membrane series optimized for high‑temperature desalination, Freudenberg’s partnership with a Saudi university to develop biodegradable filter media, Lenntech’s rollout of modular water‑treatment plants incorporating IoT‑enabled filtration modules, and Pall Corporation’s acquisition of a local specialty filter distributor to strengthen its industrial foothold. Salfi Filtration announced a joint venture with a domestic polymer producer to localize non‑woven filter fabrication, while Sandler AG introduced a metal‑mesh filter line designed for high‑pressure petrochemical applications. Wetico expanded its service network across the Eastern Province, offering on‑site maintenance contracts for large‑scale industrial filters.