1. What is the Retinal Imaging Devices Market Overview – definition, scope, and significance?

The Retinal Imaging Devices Market comprises medical equipment and systems used to capture high‑resolution images of the retina for diagnostic, therapeutic, and monitoring purposes. Products include fluorescein angiography systems, fundus cameras, and optical coherence tomography (OCT) devices. The market’s scope extends across hospitals, clinics, ambulatory surgical centers, and specialized eye‑care facilities, serving ophthalmologists, optometrists, and retinal specialists worldwide. Its significance lies in enabling early detection of vision‑threatening diseases such as diabetic retinopathy, age‑related macular degeneration, and glaucoma, thereby improving clinical outcomes and reducing long‑term healthcare costs.

2. What are the main drivers, restraints, challenges, and opportunities for the Retinal Imaging Devices Market?

Key drivers include rising prevalence of chronic eye disorders, aging populations, and growing demand for minimally invasive diagnostics. Technological advances—particularly in OCT resolution and AI‑enhanced image analysis—fuel adoption. Restraints involve high upfront capital costs, reimbursement uncertainties, and stringent regulatory pathways. Challenges encompass a shortage of trained personnel in emerging economies and interoperability issues with electronic health records. Opportunities arise from tele‑ophthalmology expansion, integration of cloud‑based analytics, and emerging markets investing in eye‑care infrastructure.

3. Which growth trends are currently shaping the Retinal Imaging Devices Market?

Current trends feature a shift toward portable and handheld retinal imaging solutions that support point‑of‑care screening. Artificial intelligence is increasingly embedded in devices to automate disease detection and risk stratification. The market also sees convergence with digital health platforms, enabling remote monitoring and data sharing. Another notable trend is the development of multimodal systems that combine fluorescein angiography, fundus photography, and OCT into a single platform, enhancing workflow efficiency for clinicians.

4. How has COVID‑19 impacted the Retinal Imaging Devices Market, and what is the recovery trajectory?

The pandemic caused temporary clinic closures and deferred elective eye examinations, leading to a short‑term dip in device installations. Supply‑chain disruptions affected component availability, particularly for high‑precision optics. However, the crisis accelerated tele‑ophthalmology adoption, prompting manufacturers to enhance remote imaging capabilities. As health systems normalize, demand rebounds strongly, supported by pent‑up screening needs and heightened awareness of chronic disease management, positioning the market on a clear upward recovery path.

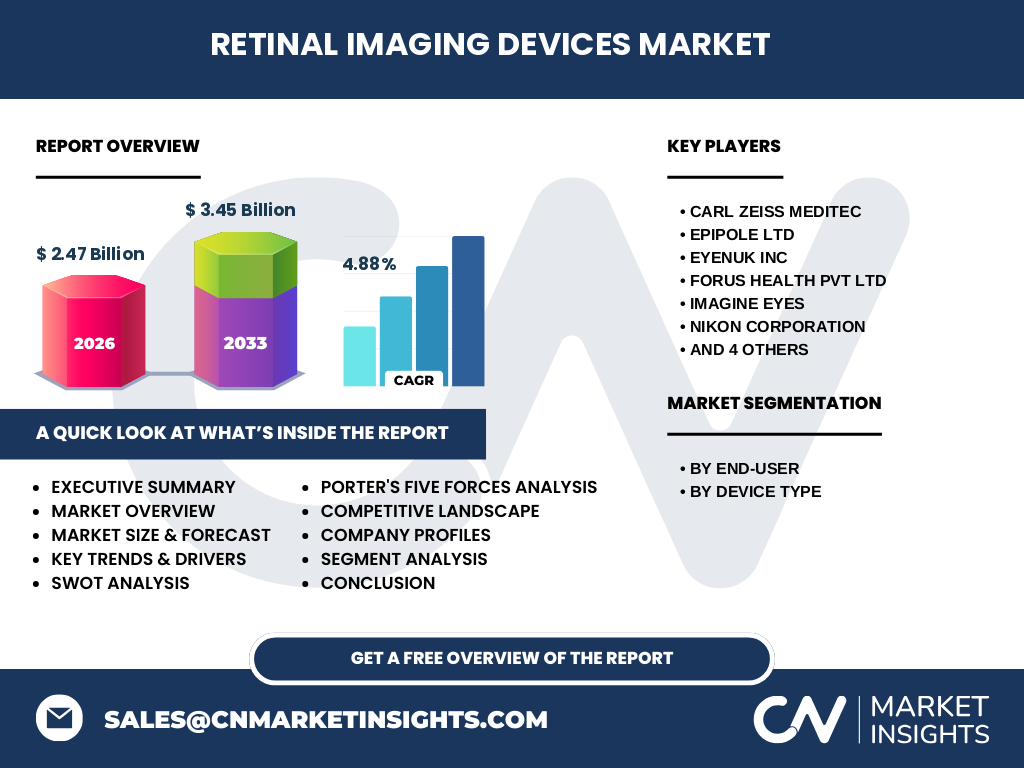

5. What does the competitive landscape of the Retinal Imaging Devices Market look like?

The market is moderately consolidated, with a mix of established optical manufacturers and innovative start‑ups. Leading players such as Carl Zeiss Meditec, Nikon Corporation, and Topcon Corporation dominate the OCT and fundus camera segments, leveraging strong brand equity and global distribution networks. Emerging competitors like Epipole Ltd and Imagine Eyes focus on AI‑driven analytics and portable devices, creating competitive pressure. Recent years have seen strategic partnerships and acquisition activity aimed at expanding product portfolios and geographic reach.

6. What are the high‑level findings in the Executive Summary of the Retinal Imaging Devices Market?

The market is valued at USD 2.47 billion in 2026 and is projected to reach USD 3.45 billion by 2033, reflecting a compound annual growth rate of 4.88 %. Growth is propelled by increasing disease burden, technological innovation, and expanding end‑user segments. OCT remains the fastest‑growing device type, while hospitals and clinics continue to be the principal purchasers. Geographic expansion is strongest in North America and Europe, with emerging opportunities in Asia‑Pacific. Competitive dynamics are shifting toward digital integration and AI, suggesting that companies investing in smart platforms will capture superior market share.

7. What are the market forecasts for the Retinal Imaging Devices Market for 2025‑2032?

Based on the provided CAGR of 4.88 %, the market is expected to maintain steady expansion through 2032. By 2032, the market size is anticipated to exceed USD 4 billion, with each segment—hospitals & clinics, ambulatory surgical centers, specialized eye‑care centers, and other end‑users—experiencing incremental growth aligned with overall demand drivers. Device‑type forecasts show OCT leading the segmental increase, followed by fundus cameras, while fluorescein angiography maintains a stable niche role for complex retinal vascular assessments.

8. How is the Retinal Imaging Devices Market sized and shared by segmentation?

Segmentation by end‑user reveals that hospitals & clinics command the largest share, reflecting their role as primary diagnostic hubs. Ambulatory surgical centers and specialized eye‑care centers follow, driven by procedural volumes and focused retinal services. The “Other End Users” category includes research institutions and mobile screening units, showing modest but growing participation. By device type, optical coherence tomography holds the leading position due to its high diagnostic value, while fundus cameras occupy a substantial secondary share owing to their versatility and lower cost. Fluorescein angiography represents a specialized niche, primarily utilized in tertiary care settings.

9. What is the global geographic distribution of the Retinal Imaging Devices Market?

North America remains the largest regional market, supported by high healthcare expenditure, advanced reimbursement frameworks, and early technology adoption. Europe follows closely, benefiting from robust ophthalmology networks and regulatory harmonization. Asia‑Pacific is the fastest‑growing region, propelled by expanding middle‑class populations, increasing prevalence of diabetes, and government initiatives to improve eye‑care access. Latin America and the Middle East & Africa present emerging opportunities, though currently contributing a smaller share of overall revenue.

10. Can you provide a detailed regional analysis of the Retinal Imaging Devices Market?

In the United States, market growth is driven by widespread OCT deployment in retinal disease management and strong insurance coverage. Canada’s market is characterized by centralized procurement and adoption in academic ophthalmology centers. European countries such as Germany, France, and the United Kingdom demonstrate steady uptake, with national health services investing in high‑resolution imaging platforms. In China and India, rapid urbanization and rising diabetes rates stimulate demand, while government‑backed vision‑screening programs accelerate device penetration. Japan’s market is mature, focusing on upgrade cycles for existing OCT fleets. Emerging economies in Southeast Asia are beginning to import mid‑range devices, creating a pipeline for future expansion.

11. Which companies lead the Retinal Imaging Devices Market and what are their strategic approaches?

Carl Zeiss Meditec focuses on high‑performance OCT systems, coupling them with proprietary software for quantitative analysis. Nikon Corporation leverages its optics expertise to deliver advanced fundus cameras with integrated AI diagnostics. Topcon Corporation offers a broad portfolio across all device types, emphasizing modularity and service contracts. Smaller innovators such as Epipole Ltd and Imagine Eyes prioritize AI‑enabled image interpretation and cloud connectivity, aiming to differentiate through software value. Companies like Forus Health and Phoenix Technology Group pursue cost‑effective portable solutions for screening in low‑resource settings.

12. How does Porter’s Five Forces model apply to the Retinal Imaging Devices Market?

Threat of new entrants is moderate; high capital requirements and regulatory compliance deter many newcomers, yet digital‑health start‑ups can enter via software‑first models. Bargaining power of suppliers is low to moderate, as key optical components are sourced from multiple vendors, though specialized lasers can be a concentration point. Bargaining power of buyers is increasing, especially large hospital groups that negotiate volume discounts and demand service bundles. Threat of substitutes is limited; while smartphone‑based retinal imaging exists, it lacks clinical accuracy compared with dedicated devices. Competitive rivalry is intense, driven by continual innovation, price competition, and aftermarket service differentiation.

13. What are the SWOT insights for the Retinal Imaging Devices Market?

Strengths: Proven clinical efficacy, growing disease prevalence, and strong reimbursement pathways in major economies. Weaknesses: High acquisition cost and dependence on specialist training. Opportunities: Integration of AI, tele‑ophthalmology expansion, and penetration into emerging markets. Threats: Regulatory delays for next‑generation devices, potential pricing pressure from public‑sector procurement, and rapid technological obsolescence.

14. How is the value chain structured for the Retinal Imaging Devices Market?

The value chain begins with component suppliers (optics, sensors, lasers), proceeds to device manufacturers who assemble and calibrate the systems, followed by software developers providing image‑processing algorithms. Distribution channels include direct sales to large health systems, regional distributors for smaller clinics, and online platforms for portable units. Post‑sale services encompass installation, training, maintenance contracts, and cloud‑based data management. End‑users—clinicians and allied health professionals— generate diagnostic data that feeds back into R&D for iterative product improvement.

15. What key investment insights emerge for stakeholders in the Retinal Imaging Devices Market?

Investors should prioritize companies that combine hardware excellence with scalable AI analytics, as this synergy creates recurring revenue streams through software licensing. Partnerships with tele‑medicine platforms can accelerate market entry in underserved regions. Acquisitions of niche firms specializing in portable imaging or data analytics can augment existing portfolios and enhance competitive positioning. Finally, focusing on regions with strong public‑health eye‑screening initiatives offers a path to volume‑driven growth.

16. What conclusions can be drawn from the Retinal Imaging Devices Market analysis?

The market is on a sustained growth trajectory, underpinned by demographic shifts, disease burden, and technological maturation. While capital intensity and regulatory demands present barriers, the convergence of AI, portability, and tele‑health creates a fertile environment for innovation. Companies that invest in integrated hardware‑software ecosystems and expand into emerging geographies are likely to capture the bulk of the projected USD 3.45 billion market by 2033.

17. How was the research for this report conducted?

The study employed a mixed‑method approach, combining primary interviews with ophthalmology clinicians, device manufacturers, and regulatory experts, alongside secondary data extraction from industry reports, peer‑reviewed journals, and company filings. Market sizing utilized the provided baseline (USD 2.47 billion in 2026) and applied the stated CAGR of 4.88 % to generate forward‑looking estimates. Trend analysis incorporated technology roadmaps and patent activity, while competitive assessment drew from publicly available financials and product launch announcements.

18. What is the scope of this research and its limitations?

The scope covers global demand for retinal imaging devices across four end‑user categories and three primary device types, with geographic segmentation into major regions. It excludes detailed pricing analytics, country‑level market shares, and confidential proprietary data. Forecasts are based on the supplied market size and growth rate, assuming stable macro‑economic conditions and no major disruptive regulatory changes.

19. Which key companies have made recent developments in the Retinal Imaging Devices Market?

Carl Zeiss Meditec launched a next‑generation OCT platform featuring real‑time eye‑tracking and cloud‑based analytics. Nikon introduced a compact fundus camera with embedded AI that flags diabetic retinopathy signs during acquisition. Topcon released a multimodal system that integrates fluorescein angiography, fundus photography, and OCT in a single user interface. Epipole Ltd announced a partnership with a major tele‑health provider to deploy portable retinal scanners in rural clinics. Imagine Eyes secured funding to accelerate its AI‑driven retinal disease detection software, targeting integration with existing hardware platforms. These developments illustrate the market’s focus on combining diagnostic precision with digital connectivity.