What is the Wheat Flour Market Overview – definition, scope, and significance?

The Wheat Flour Market encompasses the production, distribution, and consumption of flour derived from wheat grains for food and industrial use. It covers all product types—including all‑purpose, bread, semolina, durum, and whole‑wheat flour—across residential and commercial end‑users, as well as varied applications such as bread, bakery products, noodles, pasta, and other specialty foods. The market’s significance lies in its role as a staple ingredient for global food security, supporting bakery, confectionery, and fast‑food sectors while driving agricultural demand and employment worldwide.

What are the Wheat Flour Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising consumer demand for convenient baked goods, population growth in emerging economies, and increasing per‑capita wheat consumption. Restraints stem from volatile wheat commodity prices, strict food‑safety regulations, and competition from alternative grains. Challenges involve supply‑chain disruptions, climate‑induced yield fluctuations, and evolving dietary preferences toward gluten‑free options. Opportunities arise from product innovation (e.g., fortified and organic flours), expansion of online distribution channels, and growth in ready‑to‑eat bakery segments.

What are the current Wheat Flour Market Growth Trends?

Growth trends feature a shift toward premium and specialty flours, such as high‑protein bread flour and whole‑wheat blends, driven by health‑conscious consumers. E‑commerce is gaining traction, with online sales channels accounting for an increasing share of total distribution. Additionally, manufacturers are adopting clean‑label formulations and sustainable sourcing practices, while automation in milling processes improves efficiency and reduces waste, collectively sustaining market expansion.

How has COVID‑19 impacted the Wheat Flour Market and what is the recovery trajectory?

The pandemic triggered a surge in residential flour purchases as lockdowns boosted home baking, while commercial demand contracted due to restaurant closures. Supply chains experienced temporary bottlenecks, but rapid adaptation—such as reallocating production to retail channels—mitigated longer‑term effects. As economies reopen, commercial usage is rebounding, and the market is transitioning to a balanced growth path, supported by continued strong residential demand and recovery in food‑service segments.

What does the Wheat Flour Market Competitive Landscape look like?

The market is moderately consolidated, led by global players such as Archer Daniels Midland, General Mills, and ITC Limited, alongside regional powerhouses like Acarsan Holding and Manildra Group. Competitive strategies focus on capacity expansion, product diversification, and strategic partnerships. Mergers and acquisitions have modestly increased consolidation, while smaller niche firms pursue specialty flour segments to differentiate themselves.

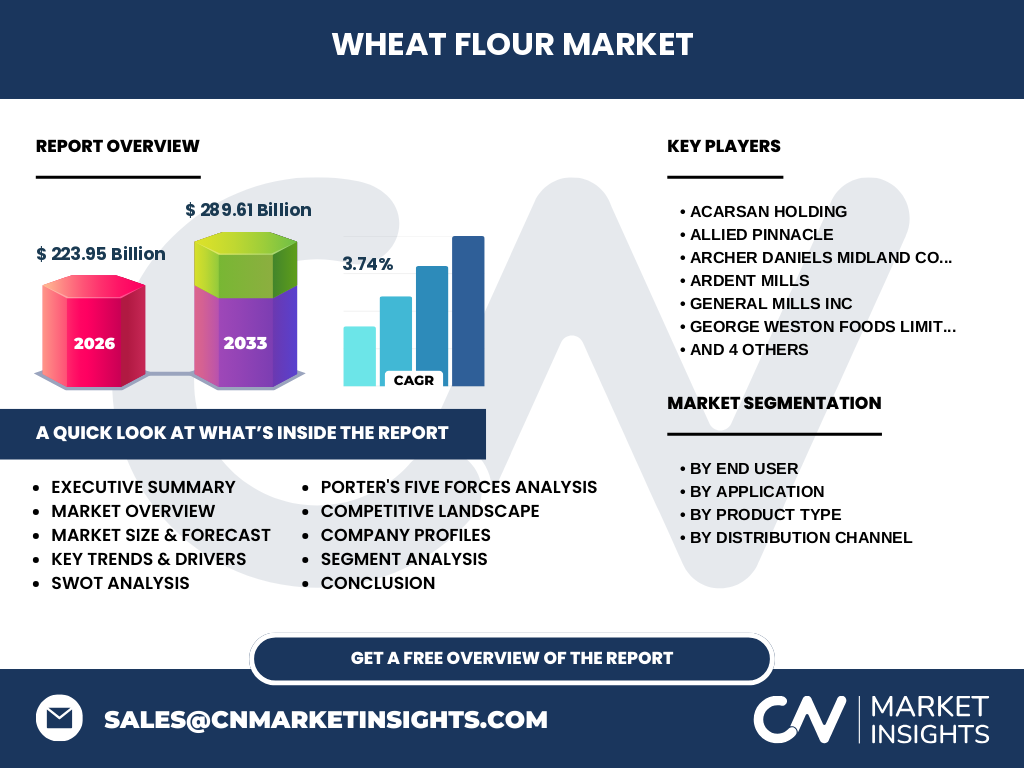

What are the key findings in the Executive Summary of the Wheat Flour Market?

The Wheat Flour Market is valued at 223.95 billion USD in 2026 and is projected to reach 289.61 billion USD by 2033, reflecting a CAGR of 3.74 % over the forecast period. Growth is propelled by expanding residential consumption, rising demand for bakery and noodle products, and the acceleration of online distribution. Competitive dynamics are shaped by a mix of large multinational mills and agile regional firms, while innovation in product types and sustainability offers significant upside.

What are the Wheat Flour Market Forecasts for 2025‑2032?

Based on the provided CAGR of 3.74 %, the market is expected to maintain steady expansion through 2032, moving from the 2026 baseline of 223.95 billion USD toward the 2033 forecast of 289.61 billion USD. This trajectory suggests consistent year‑over‑year growth, underpinned by increasing per‑capita wheat consumption, continued investment in milling technology, and broader adoption of digital sales platforms across all end‑user segments.

How is the Wheat Flour Market Size and Share broken down by segmentation?

Segmentation reveals diverse demand drivers. By end‑user, residential consumption accounts for the larger share due to home baking trends, while commercial use—restaurants, bakeries, and institutional kitchens—contributes significant volume. Application‑wise, bread and bakery products dominate, followed by noodles and pasta, with “others” covering specialty and fortified flours. Product‑type distribution highlights all‑purpose flour as the base‑line offering, complemented by strong growth in bread flour, semolina/durum, and whole‑wheat variants. Distribution channels are led by supermarkets and hypermarkets, with convenience stores and online channels gaining momentum.

What is the Global Wheat Flour Market Size and Share by Region?

The market’s global footprint spans North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. While specific regional monetary values are not disclosed, the overall size of 223.95 billion USD (2026) and projected 289.61 billion USD (2033) reflects contributions from all regions, with Asia‑Pacific expected to show the fastest growth due to expanding middle‑class populations and rising wheat‑based product consumption.

What does the Regional Analysis of the Wheat Flour Market reveal?

North America remains a mature market with high per‑capita flour usage and strong retail infrastructure. Europe exhibits steady demand, driven by artisanal bakeries and health‑focused whole‑grain products. Asia‑Pacific leads in volume growth, fueled by urbanization, increased bakery chain penetration, and noodle consumption. Latin America shows moderate expansion, while the Middle East & Africa present emerging opportunities linked to rising disposable incomes and shifting dietary patterns toward wheat‑based staples.

Who are the leading companies in the Wheat Flour Market and what are their strategies?

Key players include Archer Daniels Midland, General Mills, ITC Limited, Acarsan Holding, Allied Pinnacle, Ardent Mills, George Weston Foods, KORFEZ Flour Group, Manildra Group, and The King Arthur Baking Company. Their strategies encompass capacity upgrades, acquisition of niche flour brands, development of fortified and organic product lines, expansion of e‑commerce capabilities, and sustainability initiatives such as using renewable energy in milling operations.

How does Porter’s Five Forces analysis apply to the Wheat Flour Market?

Threat of new entrants is moderate due to high capital requirements for milling plants and stringent food‑safety standards. Supplier power is moderate; wheat growers are abundant, yet price volatility can affect margins. Buyer power is strong, especially among large retailers and food‑service chains demanding consistent quality and price. The threat of substitutes remains low, as wheat flour is a primary bakery ingredient, though gluten‑free alternatives pose niche competition. Competitive rivalry is intense, driven by product differentiation, brand loyalty, and cost efficiencies.

What are the SWOT insights for the Wheat Flour Market?

Strengths: essential staple commodity, diversified end‑uses, and established global supply chains. Weaknesses: sensitivity to wheat price fluctuations and dependence on agricultural yields. Opportunities: growth in premium and fortified flours, expansion of online sales, and sustainability‑focused production. Threats: climate change impacts on wheat harvests, rising health trends favoring gluten‑free diets, and regulatory pressures on fortification and labeling.

What does the Wheat Flour Market Value Chain look like?

The value chain begins with wheat farming, followed by grain cleaning, milling, and flour refinement. Subsequent steps include blending, fortification, packaging, and distribution through wholesale, retail, and direct‑to‑consumer channels. Key value‑adding activities involve quality testing, brand development, and logistics optimization. Each stage presents cost‑control and efficiency opportunities, particularly in automated milling and digital supply‑chain management.

What are the key investment insights for the Wheat Flour Market?

Investors should focus on companies expanding capacity in high‑growth regions, especially Asia‑Pacific, and those innovating with specialty flours (e.g., high‑protein, organic, fortified). Platforms enhancing online distribution present scalable revenue streams. Sustainable milling practices and renewable‑energy integration can improve margins and meet ESG criteria, making such firms attractive for long‑term capital allocation.

What conclusions can be drawn from the Wheat Flour Market analysis?

The wheat flour sector demonstrates resilient growth, anchored by its status as a dietary cornerstone and supported by evolving consumer preferences for healthier and convenient baked goods. Even after pandemic disruptions, the market is on a steady recovery path, with a projected CAGR of 3.74 % through 2033. Strategic focus on product innovation, digital channels, and sustainable operations will be decisive for market leaders.

How was the research methodology designed for this Wheat Flour Market report?

The study employed a mixed‑method approach, combining primary interviews with industry experts, secondary data extraction from company filings, trade publications, and governmental statistics. Market sizing used a bottom‑up technique, aggregating segment revenues and applying the provided CAGR for forward projections. Competitive analysis incorporated SWOT and Porter’s Five Forces frameworks, while regional assessments leveraged macro‑economic indicators and consumption trends.

What is the scope of this Wheat Flour Market research?

The scope covers global wheat flour production, consumption, and distribution across residential and commercial end‑users, segmented by application, product type, and distribution channel. Geographic coverage includes all major regions. The report excludes granular market‑share percentages and proprietary financial data beyond the supplied figures, focusing instead on trend analysis, strategic insights, and forward‑looking forecasts.

Which key companies and recent developments are highlighted in the Wheat Flour Market?

Leading firms such as Archer Daniels Midland, General Mills, ITC Limited, Acarsan Holding, and The King Arthur Baking Company are featured. Recent developments include Archer Daniels Midland’s investment in high‑efficiency milling technology, General Mills’ launch of a fortified whole‑wheat line, ITC’s expansion of its organic flour portfolio in South Asia, and Manildra Group’s partnership with an e‑commerce platform to streamline online sales. These initiatives illustrate the market’s focus on innovation, sustainability, and digital transformation.