What is the Europe Cell Line Development Market Overview – definition, scope, and significance?

The Europe Cell Line Development Market encompasses the production, optimization, and supply of cell lines used for research, drug discovery, bioproduction, and tissue engineering across European countries. It includes primary cell lines, hybridomas, continuous cell lines, and recombinant cell lines, as well as associated equipment, media, and reagents. This market is significant because cell lines are foundational tools for biologics development, enabling faster therapeutic screening, scalable manufacturing, and advanced regenerative medicine applications, thus driving innovation and economic growth in the European biotech sector.

What are the key drivers, restraints, challenges, and opportunities shaping the Europe Cell Line Development Market?

Key drivers include rising demand for biologics, increased investment in personalized medicine, and strong governmental support for biotech research in Europe. Opportunities arise from emerging technologies such as CRISPR‑based cell engineering and the growth of tissue‑engineered products. Major restraints are high development costs and stringent regulatory requirements. Challenges involve supply chain complexities for media and reagents, and the need for standardized cell line authentication to ensure reproducibility across laboratories.

Which growth trends are currently influencing the Europe Cell Line Development Market?

Current trends feature a shift toward continuous and recombinant cell lines due to their scalability and consistency for large‑volume biologics production. Automation of cell line selection and high‑throughput screening are gaining traction, reducing time‑to‑market. Additionally, collaborations between academia and industry are accelerating the translation of novel cell models into commercial offerings, while the integration of AI for predictive cell line performance is an emerging influence.

How has COVID‑19 impacted the Europe Cell Line Development Market, and what is the recovery trajectory?

The pandemic initially disrupted supply chains for media and reagents, causing short‑term project delays. However, heightened focus on vaccine development and antiviral research spurred increased demand for robust cell platforms, especially hybridomas and recombinant lines. Post‑2022, the market has rebounded strongly, with a clear recovery path driven by renewed investment in biotech infrastructure and continued emphasis on pandemic preparedness.

Who are the major competitors, and what is the consolidation landscape in the Europe Cell Line Development Market?

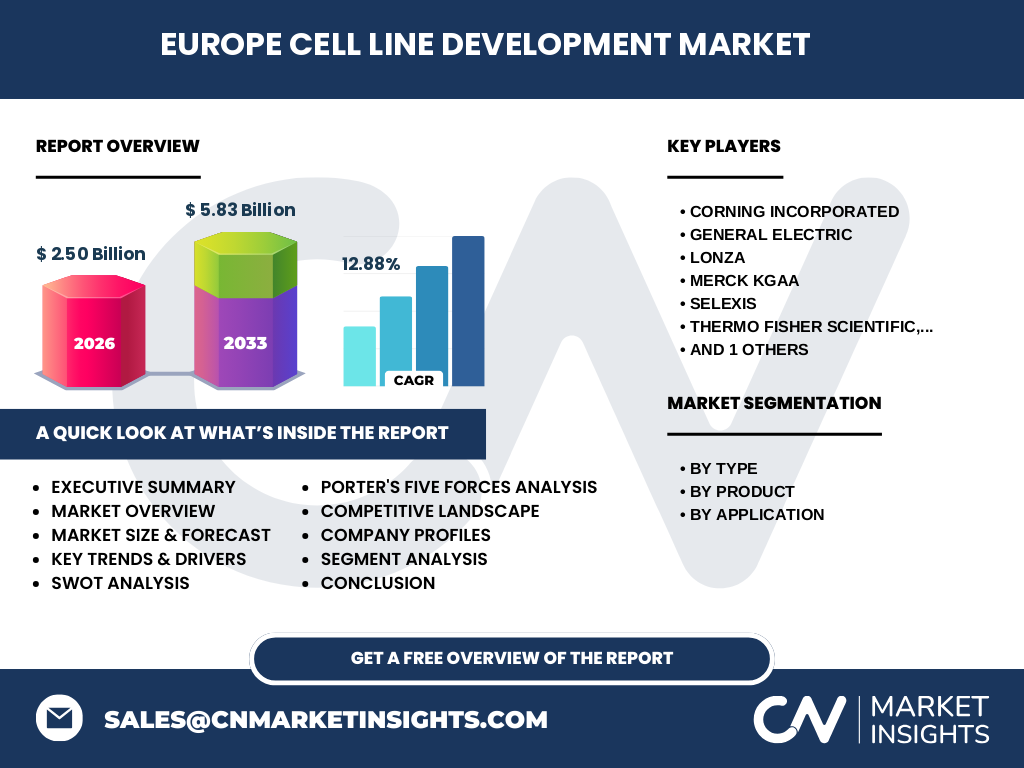

Key competitors include Corning Incorporated, General Electric, Lonza, Merck KGaA, SELEXIS, Thermo Fisher Scientific, Inc., and WuXi AppTec. The market shows moderate consolidation, with large multinational firms acquiring niche technology providers to broaden their cell line portfolios and enhance service capabilities. Strategic alliances, especially between equipment manufacturers and reagent suppliers, are common to offer integrated solutions to end‑users.

What are the high‑level findings presented in the Executive Summary of the Europe Cell Line Development Market?

The Executive Summary highlights a robust market valued at €2.50 billion in 2026, projected to reach €5.83 billion by 2033, reflecting a CAGR of 12.88 %. Growth is driven by expanding biologics pipelines, rising demand for tissue‑engineered products, and technological advances in cell line engineering. Europe remains a hub of innovation, supported by strong research funding and a collaborative ecosystem that positions the region as a leader in next‑generation cell line development.

What does the market forecast indicate for the Europe Cell Line Development Market from 2025 to 2032?

Forecasts anticipate continued double‑digit growth, with the market size expected to more than double from the 2026 baseline of €2.50 billion to €5.83 billion by 2033. This trajectory is underpinned by increasing adoption of continuous and recombinant cell lines, expansion of biopharmaceutical manufacturing capacity, and rising applications in drug discovery and tissue engineering across Europe.

How is the Europe Cell Line Development Market sized and shared by segmentation?

By type, the market is divided among Primary Cell Line, Hybridomas, Continuous Cell Lines, and Recombinant Cell Line categories, each serving distinct research and production needs. By product, it splits into Equipment and Media & Reagents, reflecting the dual demand for hardware and consumables. By application, the market is segmented into Drug Discovery and Bioproduction & Tissue Engineering, illustrating the breadth of usage from early‑stage screening to large‑scale therapeutic manufacturing.

What is the global Europe Cell Line Development Market size and share by region?

Within the global context, Europe accounts for a substantial share of the cell line development market, anchored by its advanced biotech infrastructure and regulatory frameworks. While exact global figures are not disclosed, Europe’s €2.50 billion valuation in 2026 positions it as a leading contributor alongside North America and Asia‑Pacific, driving worldwide innovation in cell‑based technologies.

What does the regional analysis reveal about the Europe Cell Line Development Market performance?

The regional analysis shows that Western Europe, particularly Germany, the United Kingdom, and France, leads in market volume due to mature pharma ecosystems and high R&D spending. Northern European countries contribute strong growth through specialized biotech clusters and favorable funding policies. Central and Eastern Europe demonstrate emerging potential, supported by cost‑effective research facilities and increasing foreign investment.

Which companies are leading the Europe Cell Line Development Market, and what strategies are they pursuing?

Leading firms such as Corning Incorporated, Lonza, Merck KGaA, and Thermo Fisher Scientific focus on expanding product portfolios, investing in next‑generation cell line platforms, and enhancing digital service offerings. General Electric leverages its instrumentation expertise, while SELEXIS emphasizes high‑purity reagents. WuXi AppTec pursues an integrated services model, combining cell line development with downstream biomanufacturing to provide end‑to‑end solutions for biotech clients.

How does Porter’s Five Forces framework apply to the Europe Cell Line Development Market?

Threat of new entrants is moderate due to high capital requirements and regulatory hurdles. Bargaining power of buyers is strong, as large pharma and biotech firms demand customized, high‑quality cell lines. Bargaining power of suppliers is moderate; specialized media and reagent providers hold some leverage. Threat of substitutes is low, given the unique role of cell lines in biologics development. Competitive rivalry is intense, driven by innovation, pricing pressures, and strategic partnerships.

What are the SWOT insights for the Europe Cell Line Development Market?

Strengths: Advanced scientific infrastructure, strong funding mechanisms, and a skilled workforce. Weaknesses: High operational costs and fragmented regulatory landscape across countries. Opportunities: Growth in personalized medicine, AI‑driven cell line design, and expansion into tissue engineering. Threats: Supply chain vulnerabilities for critical reagents and increasing competition from emerging biotech hubs outside Europe.

How is the value chain structured in the Europe Cell Line Development Market?

The value chain begins with research institutions generating novel cell line candidates, followed by technology providers offering gene editing tools and culture media. Specialized manufacturers then produce and validate cell lines, which are supplied to equipment makers and reagent vendors. End users—pharma, biotech, and academic labs—utilize the lines for drug discovery, bioproduction, or tissue engineering, completing the cycle with feedback that drives further innovation.

What key investment insights can be derived for stakeholders in the Europe Cell Line Development Market?

Investors should target companies with integrated service platforms that combine cell line development, scale‑up, and downstream manufacturing. Funding firms that are expanding AI‑enabled screening capabilities offers high upside. Strategic partnerships with equipment manufacturers provide cross‑selling opportunities, while acquisitions of niche reagent suppliers can strengthen supply chain resilience and improve margins.

What conclusions can be drawn from the Europe Cell Line Development Market analysis?

The market is on a strong growth trajectory, powered by expanding biologics pipelines and innovative cell line technologies. Europe’s robust research ecosystem, combined with supportive policy environments, positions the region as a global leader. Companies that invest in automation, AI, and integrated services are likely to capture the greatest market share, while addressing supply chain and regulatory challenges will be essential for sustained success.

What research methodology was employed to compile this market report?

The study used a mixed‑method approach, combining primary interviews with industry experts, secondary data extraction from company filings, scientific publications, and market databases. Quantitative analysis applied trend extrapolation and CAGR calculations based on the provided 2026 market size (€2.50 billion) and forecasted 2033 value (€5.83 billion). Qualitative insights were derived from expert consensus and competitive benchmarking.

What is the scope of the research, including coverage and limitations?

The scope covers the European cell line development ecosystem, segmented by type, product, and application, and includes major players and regional performance. Limitations arise from the reliance on publicly available financial figures and the absence of granular market share percentages, which restricts precise competitive quantification but still provides a comprehensive strategic overview.

Which key companies and recent developments should be noted in the Europe Cell Line Development Market?

Corning Incorporated launched a next‑generation low‑adsorption culture vessel, enhancing cell line productivity. Lonza announced a partnership with a leading AI firm to accelerate recombinant cell line design. Merck KGaA introduced a high‑purity media line aimed at continuous manufacturing. SELEXIS released a new reagent series for improved hybridoma stability. Thermo Fisher Scientific expanded its Europe‑wide service network, offering end‑to‑end cell line development solutions. WuXi AppTec unveiled an integrated platform combining cell line engineering with GMP‑grade bioproduction, targeting European biotech firms seeking rapid scale‑up.