North America Automation-as-a-service Market Overview - Definition, scope, and significance?

The North America Automation‑as‑a‑Service (AaaS) market comprises cloud‑based platforms that deliver end‑to‑end automation solutions—ranging from robotic process automation to intelligent workflow orchestration—via subscription models. It spans multiple deployment models (on‑premise and cloud) and serves diverse business functions such as sales & marketing, finance & operations, human resources, and IT. The market is significant because it enables organizations to accelerate digital transformation, reduce operational costs, and improve compliance without large upfront capital expenditures.

North America Automation-as-a-service Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include the rapid adoption of digital workflows, the need for cost‑effective scalability, and increasing regulatory pressure for audit‑ready processes. Restraints arise from legacy system integration complexity and concerns about data security in multi‑tenant environments. Major challenges involve talent shortages in AI‑enhanced automation and the high initial learning curve for enterprise users. Opportunities are found in expanding into underserved verticals such as government agencies and in leveraging AI to create hyper‑personalized automation services.

North America Automation-as-a-service Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift toward hyper‑automation, where AI, machine learning, and RPA converge on a single cloud platform. Another emerging trend is the proliferation of low‑code/no‑code development tools that democratize automation creation across non‑technical users. Additionally, the rise of edge‑enabled automation allows real‑time process execution in manufacturing and logistics, while subscription‑based pricing models continue to gain traction as firms seek predictable OPEX.

COVID-19 Impact on the North America Automation-as-a-service Market - Pandemic effects and recovery trajectory?

COVID‑19 accelerated demand for remote‑ready automation solutions as businesses scrambled to maintain continuity while employees worked from home. Adoption rates jumped, particularly for cloud‑based deployment models, which proved resilient to lockdowns. Post‑pandemic, the market has entered a recovery phase marked by sustained investment in automation to address labor shortages and to build more resilient supply chains, maintaining the momentum generated during the crisis.

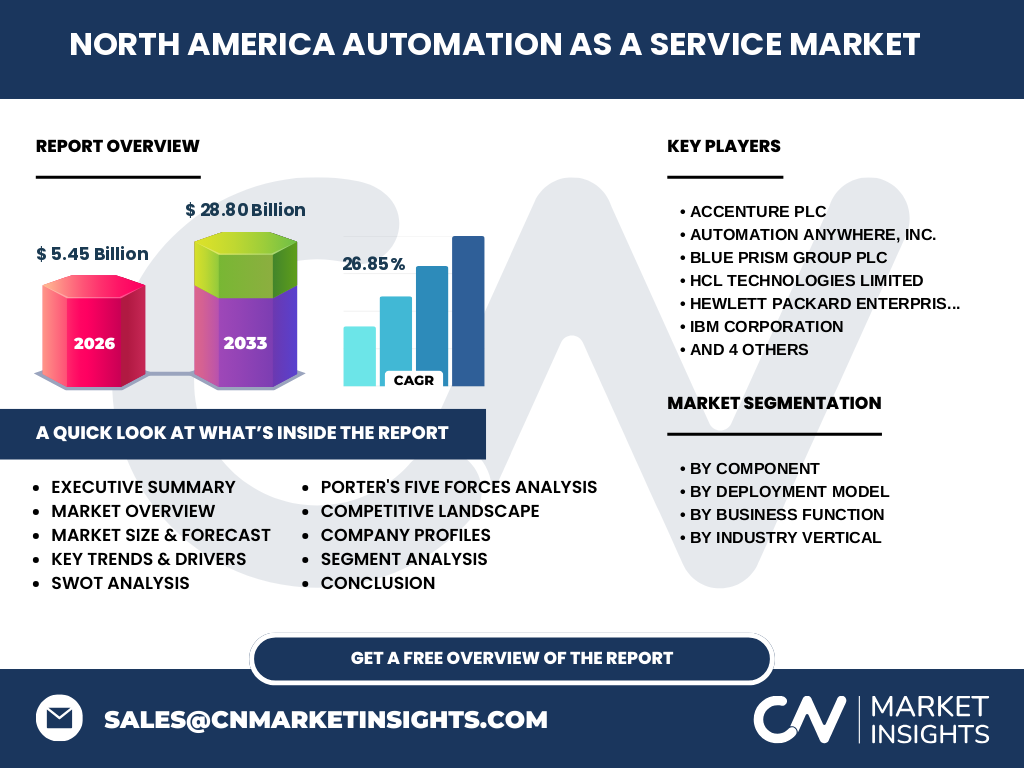

North America Automation-as-a-service Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena is dominated by technology giants and specialized automation firms. Leading players such as Accenture PLC, Automation Anywhere, Inc., Blue Prism Group plc, HCL Technologies Limited, Hewlett Packard Enterprise, IBM Corporation, Microsoft Corporation, NICE Ltd., Pegasystems Inc., and UiPath command the market through robust solution portfolios and extensive channel networks. Recent years have witnessed strategic acquisitions—e.g., large cloud providers acquiring niche RPA startups—indicating ongoing consolidation aimed at delivering integrated AaaS suites.

Executive Summary - High-level overview and key findings about North America Automation-as-a-service Market?

The North America AaaS market is poised for explosive growth, with a 2026 valuation of $5.45 billion and an expected rise to $28.80 billion by 2033, reflecting a robust CAGR of 26.85 %. Growth is fueled by broader digital adoption, cloud migration, and the pursuit of operational efficiency across all business functions. Leading vendors are expanding through M&A and AI‑driven service enhancements, while emerging trends such as low‑code automation and edge computing promise new avenues for value creation.

North America Automation-as-a-service Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 26.85 %, the market is projected to expand from its 2026 base of $5.45 billion to approximately $28.80 billion by 2033. This trajectory suggests consistent double‑digit growth throughout the 2025‑2032 horizon, driven by continued cloud adoption, expanding use cases in finance, HR, and IT, and the increasing prevalence of AI‑augmented automation across all industry verticals.

North America Automation-as-a-service Market Size and Share by Segmentation - Breakdown by segment?

Segmentation reveals four primary dimensions. By component, the market splits between comprehensive solutions and services that support implementation and maintenance. Deployment models divide into on‑premise and cloud, with cloud rapidly outpacing on‑premise due to flexibility. Business functions are served across sales & marketing, finance & operations, human resource, and information technology, each showing distinct adoption curves. Industry verticals include BFSI, IT & Telecom, Retail, Healthcare & Life Sciences, Transportation & Logistics, Government Agencies & Defense, and Manufacturing, reflecting broad applicability of AaaS.

Global North America Automation-as-a-service Market Size and Share by Region - Geographic distribution?

Within the global context, North America remains the largest regional contributor to the AaaS market, accounting for the full reported market size of $5.45 billion in 2026. The region’s mature cloud infrastructure, high concentration of enterprise headquarters, and strong innovation ecosystems underpin this dominance. While detailed percentages for other regions are not disclosed, the forecasted growth to $28.80 billion by 2033 underscores North America’s continued leadership.

Regional Analysis of the North America Automation-as-a-service Market - Detailed regional market performance?

In North America, the United States drives the majority of revenue, leveraging its extensive enterprise base and early cloud adoption. Canada follows with steady growth, buoyed by government digitization initiatives and a thriving tech sector. Both countries exhibit strong demand for cloud‑based deployment, particularly in finance, healthcare, and manufacturing, where regulatory compliance and operational efficiency are paramount.

Leading Company Profiles in the North America Automation-as-a-service Market - Industry players and strategies?

Key vendors such as Microsoft Corporation and IBM Corporation focus on integrating AaaS with their broader cloud ecosystems, offering AI‑enhanced automation modules. UiPath and Automation Anywhere specialize in RPA‑centric platforms, expanding through partner networks and vertical‑specific solutions. Accenture PLC leverages consulting expertise to deliver end‑to‑end managed services, while Hewlett Packard Enterprise differentiates with on‑premise‑ready automation stacks for regulated industries. Each player pursues a mix of organic product development and strategic acquisitions to broaden functionality.

Porter's Five Forces Analysis of the North America Automation-as-a-service Market - Competitive forces assessment?

Threat of new entrants is moderate; high capital requirements for AI research and cloud infrastructure create barriers, yet low‑code platforms lower entry costs. Bargaining power of buyers is strong, as enterprises demand flexibility and price transparency. Bargaining power of suppliers—primarily cloud infrastructure providers—is moderate, with few dominant players influencing cost. Threat of substitutes remains low, given the unique value of integrated automation‑as‑a‑service. Industry rivalry is intense, driven by rapid innovation and aggressive M&A activity among the listed leaders.

SWOT Analysis of the North America Automation-as-a-service Market - Strengths, weaknesses, opportunities, threats?

Strengths: High growth CAGR, strong cloud infrastructure, and diverse vertical applicability.

Weaknesses: Integration complexity with legacy systems and talent gaps in AI‑driven automation.

Opportunities: Expansion into government and defense sectors, development of edge‑enabled automation, and growth of low‑code creation tools.

Threats: Data security concerns, evolving regulatory landscapes, and potential market saturation as vendors converge on similar AI capabilities.

North America Automation-as-a-service Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with technology providers delivering AI, RPA, and cloud infrastructure. Next, system integrators and consulting firms customize solutions for specific business functions. Software vendors supply the AaaS platform—often on a subscription basis—while deployment partners manage cloud or on‑premise installations. Finally, end‑users across functional areas consume the service, generating feedback that drives continuous product enhancements.

Key Investment Insights in the North America Automation-as-a-service Market - Strategic investment recommendations?

Investors should target companies with strong AI roadmaps and proven cloud scalability, as these attributes align with the market’s 26.85 % CAGR. Strategic M&A opportunities exist in niche low‑code platforms that can be integrated into larger AaaS suites. Additionally, funding initiatives that address talent development in automation engineering will likely yield higher returns by mitigating one of the sector’s primary constraints.

North America Automation-as-a-service Market Conclusion - Summary and key takeaways?

The North America AaaS market is on an accelerated growth path, moving from a $5.45 billion base in 2026 to an estimated $28.80 billion by 2033. Cloud adoption, AI integration, and cross‑functional automation are the principal catalysts. While integration challenges and security concerns persist, the market presents ample opportunities for vendors, investors, and enterprises seeking to modernize operations and achieve sustainable cost efficiencies.

Research Methodology - How this research was conducted?

Primary data were collected through interviews with industry executives, technology providers, and end‑user decision makers. Secondary sources included vendor financial reports, market intelligence databases, and reputable industry publications. Quantitative analysis applied CAGR calculations to extrapolate the forecast range, while qualitative assessments examined trends, competitive dynamics, and regulatory influences.

Research Scope - Coverage and limitations?

The study covers the North America Automation‑as‑a‑Service market from 2025 through 2032, encompassing all major components, deployment models, business functions, and industry verticals listed. It focuses on publicly disclosed financial figures and does not incorporate speculative market share percentages beyond the provided data. Geographic scope is limited to North America, with global context provided for comparative insight.

Key Companies and Recent Developments in the North America Automation-as-a-service Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent developments include Microsoft Corporation expanding its Power Automate suite with AI Builder, IBM Corporation launching a hybrid cloud automation platform for finance, and UiPath announcing a partnership with a major banking consortium to streamline loan processing. Accenture PLC completed the acquisition of a low‑code automation startup, enhancing its managed services offering. Hewlett Packard Enterprise introduced an on‑premise edge automation kit for manufacturing, while Automation Anywhere released a new AI‑driven bot marketplace. These moves reflect a clear industry focus on AI integration, partnership ecosystems, and broadened deployment flexibility.