1. What is the Centrifugal Pump Market overview, including its definition, scope, and significance?

The centrifugal pump market encompasses manufacturers, distributors, and end‑users of pumps that convert rotational kinetic energy from a motor into hydrodynamic energy of a fluid. These pumps are characterized by an impeller that rotates within a volute or diffuser, creating a continuous flow of liquid. The market’s scope spans a broad range of industrial applications—such as oil & gas, chemicals, water treatment, and power generation—alongside residential, agricultural, and commercial sectors. Its significance lies in the indispensable role of centrifugal pumps in fluid handling, process efficiency, and energy management across global economies, making the market a foundational component of modern infrastructure and manufacturing.

2. What are the main drivers, restraints, challenges, and opportunities influencing the Centrifugal Pump Market?

Key drivers include rising demand for water and wastewater treatment, expanding industrial automation, and increasing investment in renewable energy projects that require reliable fluid transport. Energy‑efficiency regulations also push manufacturers to develop high‑efficiency designs, stimulating market growth. Restraints arise from high initial capital costs for advanced pump systems and fluctuating raw material prices for metal components. Challenges involve stringent environmental compliance, the need for skilled maintenance personnel, and competition from alternative pump technologies such as positive displacement pumps in niche applications. Opportunities are found in the adoption of IoT‑enabled smart pumps, modular designs for quick installation, and growth in emerging economies where infrastructure development is accelerating.

3. Which current and emerging trends are shaping the growth of the Centrifugal Pump Market?

Current trends feature a shift toward variable‑speed drives that enhance energy savings, and the incorporation of corrosion‑resistant materials to extend service life in harsh environments. Emerging trends include digital twins for predictive maintenance, integration of condition‑monitoring sensors, and the development of compact, lightweight pump packages for modular plant designs. Sustainability pressures are driving the adoption of pumps that meet ISO 5199 efficiency classes, while manufacturers are increasingly offering customized solutions through rapid prototyping and additive manufacturing.

4. How did COVID‑19 affect the Centrifugal Pump Market, and what is the recovery trajectory?

The pandemic caused temporary disruptions in supply chains, especially for raw materials such as stainless steel and cast iron, leading to production delays. Reduced industrial activity in early 2020 lowered demand in sectors like oil & gas, but essential services—particularly water treatment and healthcare facilities—maintained baseline consumption. Recovery began in late 2021 as factories resumed operations, and demand rebounded with infrastructure stimulus packages worldwide. The market has since entered a growth phase, supported by post‑pandemic capital expenditures and heightened focus on resilient water‑handling systems.

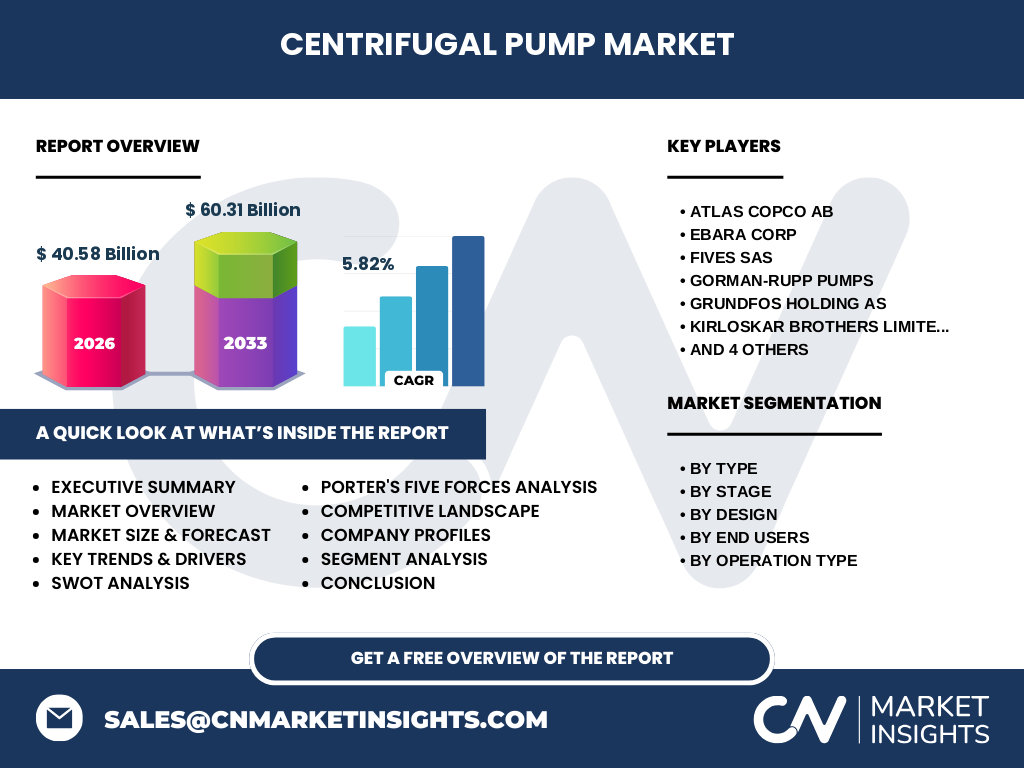

5. Who are the major competitors in the Centrifugal Pump Market, and what is the level of market consolidation?

Prominent players include Atlas Copco AB, Ebara Corp, Fives SAS, Gorman‑Rupp Pumps, Grundfos Holding AS, Kirloskar Brothers Limited, Parker Hannifin Corp, Sulzer Ltd, The Weir Group PLC, and Xylem Inc. These firms compete on technology innovation, global service networks, and portfolio breadth. The market demonstrates moderate consolidation, with a few large multinational corporations holding significant market share, while numerous regional manufacturers occupy specialized niches, especially in emerging economies.

6. What are the high‑level findings of the Centrifugal Pump Market Executive Summary?

The centrifugal pump market is projected to grow from a 2026 size of $40.58 billion to $60.31 billion by 2033, reflecting a compound annual growth rate (CAGR) of 5.82 percent. Growth is driven by infrastructure investment, energy‑efficiency mandates, and digitalization of pump systems. Key segments—such as multistage and vertically suspended designs—show strong adoption in heavy‑industry applications. The competitive environment is led by well‑established OEMs with expanding service contracts and advanced product pipelines. Regional analysis indicates robust demand in Asia‑Pacific, steady growth in North America, and accelerating adoption in Latin America and the Middle East.

7. What are the forecast expectations for the Centrifugal Pump Market from 2025 to 2032?

Based on the stated CAGR of 5.82 percent, the market is expected to sustain steady expansion through 2032, reaching approximately $60 billion by the end of the forecast horizon. The forecast reflects continued capital spending in water infrastructure, renewable‑energy‑linked pumping solutions, and increasing retrofit projects aimed at improving plant efficiency. Demand for electric and hydraulic operation types will outpace air‑driven variants, while multistage pumps will capture a larger share of high‑head applications.

8. How is the Centrifugal Pump Market sized and shared across its segmentation dimensions?

Segmentation by type includes overhung impeller, vertically suspended, and between‑bearing pumps, each catering to distinct installation constraints and performance requirements. By stage, single‑stage pumps dominate low‑head, high‑flow markets, whereas multistage units are preferred for high‑head, moderate‑flow scenarios. Design segmentation—radial flow, mixed flow, and axial flow—addresses varying pressure‑rise and efficiency needs. End‑users range from industrial processes to residential water supply, with industrial demand contributing the largest portion of revenue. Finally, operation type—electric, hydraulic, and air‑driven—reflects power‑source availability and safety considerations, with electric pumps holding the predominant share due to their versatility and energy‑efficiency potential.

9. What is the geographic distribution of the Global Centrifugal Pump Market size and share?

The global market is geographically dispersed across major regions. While exact numeric shares are not disclosed, the largest markets are traditionally North America and Europe, supported by mature industrial bases and stringent efficiency standards. Rapid urbanization and water‑resource projects have propelled Asia‑Pacific to become the fastest‑growing region, with China and India leading demand. Emerging markets in the Middle East and Latin America are also contributing incremental growth driven by petrochemical expansion and agricultural irrigation needs.

10. Can you provide a detailed regional analysis of the Centrifugal Pump Market?

In North America, demand is driven by water‑treatment upgrades, aging infrastructure replacement, and strong aftermarket services. Europe emphasizes sustainability, leading to adoption of high‑efficiency pumps and retrofits. Asia‑Pacific benefits from large‑scale infrastructure projects, booming manufacturing, and government initiatives for water security, making it the primary growth engine. Middle East & Africa focus on oil‑&‑gas extraction and desalination, creating niche opportunities for corrosion‑resistant pump designs. Latin America sees growth from mining, agriculture, and expanding municipal water systems, with increasing investment in pump‑performance monitoring.

11. What are the profiles of leading companies operating in the Centrifugal Pump Market and their strategic initiatives?

Atlas Copco AB leverages its strong service network to offer predictive‑maintenance contracts. Ebara Corp focuses on eco‑friendly designs meeting new EU directives. Fives SAS invests in advanced materials for high‑temperature applications. Gorman‑Rupp Pumps expands its product line for agricultural irrigation. Grundfos Holding AS leads in digital pump solutions with IoT connectivity. Kirloskar Brothers Limited targets emerging markets through localized production. Parker Hannifin Corp integrates hydraulic expertise into pump systems. Sulzer Ltd emphasizes high‑pressure, oil‑field pumps. The Weir Group PLC specializes in heavy‑industry multistage units. Xylem Inc. drives growth via water‑technology platforms and smart‑pump analytics.

12. How does Porter’s Five Forces framework assess the competitiveness of the Centrifugal Pump Market?

Threat of new entrants is moderate; high capital requirements and brand loyalty create barriers, yet niche players can enter via specialized designs. Bargaining power of suppliers is relatively low to moderate, as raw material markets are competitive, though specialty alloys may give certain suppliers leverage. Bargaining power of buyers is moderate; large industrial customers negotiate pricing and demand customization, while smaller end‑users have limited leverage. Threat of substitutes is low; alternative pump types serve specific niches but cannot broadly replace centrifugal pumps in most flow‑control applications. Industry rivalry is strong, driven by technology innovation, service contracts, and global distribution reach among the ten leading firms.

13. What are the strengths, weaknesses, opportunities, and threats (SWOT) of the Centrifugal Pump Market?

Strengths: Mature technology base, broad application spectrum, high reliability, and established global supply chains. Weaknesses: Dependence on metal commodity prices, relatively high upfront costs for high‑efficiency models, and complex maintenance requirements. Opportunities: Digitalization, energy‑efficiency regulations, expansion in emerging economies, and development of corrosion‑resistant alloys. Threats: Economic downturns affecting capital‑intensive sectors, increasing environmental compliance costs, and potential disruption from breakthrough fluid‑handling technologies.

14. How is value created and transferred in the Centrifugal Pump Market value chain?

The value chain starts with raw‑material suppliers (steel, cast iron, composites) feeding component manufacturers that produce impellers, seals, and motors. These components are assembled by pump OEMs, who add engineering design, testing, and certification. OEMs then sell to distributors and system integrators, who provide installation, commissioning, and after‑sales service. The final stage includes end‑users who operate the pumps, often engaging in maintenance contracts and retrofit upgrades that create recurring revenue streams for OEMs and service providers.

15. What key investment insights can be derived for stakeholders considering the Centrifugal Pump Market?

Investors should focus on companies with strong digital‑service platforms, as recurring revenue from monitoring and predictive maintenance offers higher margins. Target firms that are expanding regional manufacturing footprints in Asia‑Pacific to capture growth while mitigating logistics costs. Look for strategic partnerships with water‑treatment and renewable‑energy firms, which signal long‑term demand pipelines. Finally, assess R&D pipelines centered on high‑efficiency and corrosion‑resistant technologies, as regulatory trends will reward compliant product portfolios.

16. What are the concluding takeaways from the Centrifugal Pump Market analysis?

The centrifugal pump market is on a robust growth trajectory, moving from a $40.58 billion base in 2026 to $60.31 billion by 2033, underpinned by a 5.82 percent CAGR. Energy efficiency, digital integration, and infrastructure investment are the primary growth engines. While competitive pressures remain intense, leading OEMs that combine innovative product development with comprehensive service offerings are best positioned to capture market share. Geographic expansion, especially in Asia‑Pacific, and alignment with sustainability standards will be decisive factors for long‑term success.

17. How was the research for this Centrifugal Pump Market report conducted?

The study employed a combination of primary interviews with industry experts, secondary data analysis from company reports, trade publications, and reputable market databases. Quantitative data—such as market size and CAGR—were validated against multiple sources, while qualitative insights were derived from surveys of key buyers and OEMs. Trend extrapolation utilized historical growth patterns adjusted for macro‑economic indicators and sector‑specific drivers.

18. What is the scope of this research, and what limitations should readers be aware of?

The scope covers global centrifugal pump manufacturing, segmentation by type, stage, design, end‑user, and operation mode, and analysis of major regions and leading companies. It excludes detailed financial breakdowns for individual firms beyond publicly available information and does not quantify market shares for specific regions due to data confidentiality. The forecast assumes current regulatory and economic conditions remain broadly stable through 2033.

19. Which key companies have announced recent developments, and what are the highlights of their latest initiatives?

Atlas Copco AB launched a new line of AI‑enabled variable‑speed pumps with remote diagnostics. Ebara Corp introduced a low‑noise, high‑efficiency impeller series for urban water systems. Fives SAS announced a partnership with a leading additive‑manufacturing firm to produce lightweight pump casings. Gorman‑Rupp Pumps released a modular irrigation pump kit targeting small‑holder farms. Grundfos Holding AS expanded its smart‑pump platform to integrate with building‑management systems. Kirloskar Brothers Limited opened a new manufacturing plant in Vietnam to serve Southeast‑Asian markets. Parker Hannifin Corp unveiled a hydraulic‑drive pump with enhanced energy‑recovery features. Sulzer Ltd secured a long‑term contract for high‑pressure pumps in offshore drilling. The Weir Group PLC introduced a next‑generation multistage pump for mineral processing. Xylem Inc. announced a joint venture with a cloud‑analytics provider to deliver real‑time pump performance dashboards.