1. What is the Dairy Ingredients Market and why is it significant?

The Dairy Ingredients Market comprises all value‑added products derived from milk, such as proteins, milk powder, milk‑fat concentrates, lactose and its derivatives. These ingredients are processed and supplied to diverse end‑use sectors including food & beverages, animal feed, pharmaceuticals & nutraceuticals, and personal care. The market’s significance stems from its role in enhancing nutritional profiles, functional properties, and sensory attributes of a wide range of consumer goods. Additionally, dairy ingredients support health‑focused trends—such as high‑protein diets and clean‑label formulations—while providing essential nutrients in animal nutrition and therapeutic applications.

2. What are the main drivers, restraints, challenges, and opportunities in the Dairy Ingredients Market?

Key drivers include rising consumer demand for protein‑rich foods, growing awareness of calcium and vitamin D benefits, and increasing adoption of dairy‑based functional ingredients in nutraceuticals. Urbanization and expanding middle‑class income in emerging economies further boost demand for value‑added dairy products. Restraints arise from volatility in raw milk prices, strict regulatory requirements for food safety, and competition from plant‑based alternatives. Challenges involve supply chain disruptions, especially in regions with limited dairy farming infrastructure, and the need for sustainable processing to address environmental concerns. Opportunities are present in developing novel low‑lactose or lactose‑free ingredients, expanding into high‑growth personal‑care applications, and leveraging biotechnology to create whey‑protein isolates with enhanced functional properties.

3. Which growth trends are currently shaping the Dairy Ingredients Market?

Current trends include a shift toward clean‑label dairy ingredients, where manufacturers seek minimally processed proteins and powders with clear provenance. There is also a surge in fortified dairy powders enriched with vitamins, minerals, and probiotics. The rise of high‑protein snack bars, dairy‑based sports nutrition, and functional beverages drives demand for whey and casein isolates. In animal feed, the incorporation of dairy by‑products improves protein efficiency and reduces reliance on soy. Personal‑care trends favor milk‑fat concentrates for their emollient and skin‑conditioning properties, especially in natural‑beauty formulations.

4. How did COVID‑19 affect the Dairy Ingredients Market and what is the recovery outlook?

The pandemic caused short‑term disruptions in milk collection and processing due to lockdowns, leading to temporary supply gaps. Simultaneously, heightened health consciousness boosted demand for immune‑supporting dairy ingredients, such as vitamin‑D‑fortified powders and probiotic‑enriched whey. Recovery has been steady, as supply chains normalized and consumer confidence returned. The market is now on a growth trajectory supported by post‑pandemic emphasis on nutrition and functional foods, aligning with the projected CAGR of 2.40%.

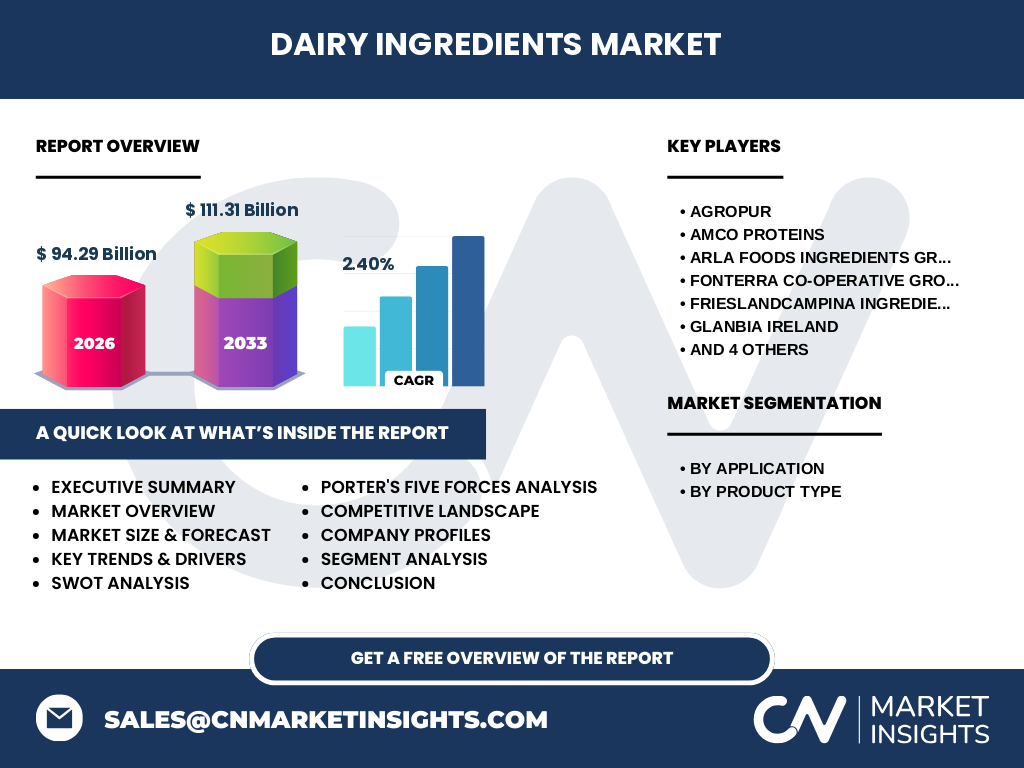

5. Who are the major competitors and what is the level of consolidation in the Dairy Ingredients Market?

Key competitors include AGROPUR, AMCO Proteins, Arla Foods Ingredients Group, Fonterra Co‑operative Group, FrieslandCampina Ingredient, Glanbia Ireland, Kerry Group, Lactalis Ingredients, PROLACTAL, and Saputo Inc. The market exhibits moderate consolidation, with a handful of large multinational dairy cooperatives and specialty ingredient firms commanding significant share, while numerous regional players serve niche segments. Strategic alliances, joint ventures, and acquisitions are common as companies aim to expand product portfolios and geographic reach.

6. What are the high‑level findings of the Dairy Ingredients Market Executive Summary?

The Dairy Ingredients Market was valued at USD 94.29 billion in 2026 and is projected to reach USD 111.31 billion by 2033, reflecting a CAGR of 2.40% over the forecast horizon. Growth is driven by protein demand, functional food trends, and expanding applications in animal feed and personal care. Regional analysis shows robust performance in North America and Europe, with emerging growth in Asia‑Pacific. Competitive dynamics are shaped by a few global leaders and ongoing innovation in low‑lactose and fortified ingredients. The outlook remains positive, supported by health‑centric consumer behavior and sustained investment in processing technologies.

7. What are the forecast expectations for the Dairy Ingredients Market from 2025 to 2032?

Based on the provided CAGR of 2.40%, the market is expected to continue a moderate expansion, moving from the 2026 baseline of USD 94.29 billion toward the 2033 forecast of USD 111.31 billion. This trajectory suggests annual incremental growth driven by increasing adoption of dairy proteins, higher‑value milk powders, and lactose derivatives across the identified end‑use sectors. The forecast underscores steady demand rather than rapid spikes, indicating a mature market with consistent, long‑term opportunities.

8. How is the Dairy Ingredients Market sized and shared by product type and application?

By product type, the market is segmented into protein, milk powder, milk‑fat concentrates, and lactose & lactose derivatives. By application, the segments are food & beverages, animal feed, pharmaceuticals & nutraceuticals, and personal care. While exact numeric shares are not disclosed, protein‑based ingredients dominate the food & beverage segment due to their functional and nutritional benefits. Milk powder holds significant share in animal feed and pharmaceutical formulations, whereas lactose derivatives are increasingly used in nutraceuticals for prebiotic effects. Milk‑fat concentrates are gaining traction in personal‑care products for their skin‑conditioning qualities.

9. What is the geographic distribution of the Global Dairy Ingredients Market?

The market is globally distributed, with major concentration in North America and Europe, reflecting well‑established dairy farming and processing infrastructure. Asia‑Pacific shows rapid growth potential driven by rising disposable incomes and expanding dairy consumption. While specific regional revenue figures are not provided, the overall global size of USD 94.29 billion (2026) and the anticipated increase to USD 111.31 billion (2033) indicate broad geographic participation.

10. How does each major region perform within the Dairy Ingredients Market?

North America leads in high‑protein ingredient demand, fueled by the sports‑nutrition and functional‑beverage sectors. Europe maintains strong sales of fortified milk powders and lactose derivatives, propelled by stringent food‑safety standards and consumer preference for natural ingredients. Asia‑Pacific is the fastest‑growing region, with increasing dairy consumption, expanding food‑service outlets, and growing pet‑food markets driving ingredient uptake. Latin America and the Middle East display moderate growth, primarily in animal‑feed applications and emerging personal‑care formulations.

11. Which companies are leading the Dairy Ingredients Market and what strategies are they pursuing?

Leading players include AGROPUR, AMCO Proteins, Arla Foods Ingredients Group, Fonterra, FrieslandCampina Ingredient, Glanbia Ireland, Kerry Group, Lactalis Ingredients, PROLACTAL, and Saputo Inc. Their strategies focus on product innovation (e.g., high‑purity whey isolates), geographic expansion through acquisitions, and sustainability initiatives such as carbon‑footprint reduction in processing. Partnerships with food‑tech startups and investment in R&D for lactose‑free and fortified ingredients are common themes aimed at capturing emerging consumer trends.

12. What does Porter’s Five Forces analysis reveal about the Dairy Ingredients Market?

• Threat of new entrants: Moderate – high capital requirements and strict regulations limit newcomers, though niche specialty firms may enter.

• Bargaining power of suppliers: Moderate – raw milk supply can be volatile, giving farmers some leverage, but large cooperatives mitigate risk through contracts.

• Bargaining power of buyers: High – large food manufacturers demand consistent quality, volume discounts, and can switch between suppliers, pressuring margins.

• Threat of substitutes: Growing – plant‑based proteins and alternative fats present competitive pressure, especially in health‑focused markets.

• Industry rivalry: Intense – established global players compete on price, innovation, and sustainability credentials.

13. What are the SWOT insights for the Dairy Ingredients Market?

Strengths: Established supply chains, strong nutritional profile, versatile applications.

Weaknesses: Sensitivity to raw‑milk price swings, lactose intolerance concerns limiting certain segments.

Opportunities: Development of low‑lactose and lactose‑free ingredients, expansion into personal‑care, adoption of green processing technologies.

Threats: Escalating competition from plant‑based alternatives, regulatory changes regarding allergen labeling, and sustainability pressures on dairy farming.

14. How is the value chain structured in the Dairy Ingredients Market?

The value chain starts with dairy farming (milk production), followed by collection, transport, and primary processing (pasteurization, separation). Next are secondary processing steps such as protein extraction, spray‑drying for powders, and fractionation for lactose derivatives. Subsequent stages involve formulation, packaging, and distribution to downstream users in food & beverage manufacturers, animal‑feed processors, pharmaceutical firms, and personal‑care producers. Value‑adding services—like custom blending and fortification—enhance margins for ingredient specialists.

15. What investment insights are recommended for stakeholders in the Dairy Ingredients Market?

Investors should prioritize companies with strong R&D pipelines for lactose‑free and fortified products, as these align with consumer health trends. Acquisitions of niche technology firms can accelerate innovation. Sustainable processing capabilities and transparent supply‑chain traceability are becoming differentiators; capital allocation toward low‑carbon manufacturing can yield long‑term competitive advantage. Finally, expanding presence in fast‑growing Asia‑Pacific markets through joint ventures offers upside potential.

16. What are the key takeaways from the Dairy Ingredients Market analysis?

The market is steady, valued at USD 94.29 billion in 2026 and projected to grow to USD 111.31 billion by 2033 (CAGR 2.40%). Protein and milk‑powder segments dominate, driven by health‑centric consumer demand. Geographic growth is strongest in Asia‑Pacific, while North America and Europe remain mature hubs. Competitive dynamics revolve around innovation, sustainability, and strategic consolidation. The outlook is positive, supported by functional‑food trends and expanding applications.

17. How was the research for this report conducted?

The study employed a combination of primary interviews with industry experts, secondary data extraction from company reports, trade publications, and reputable market databases. Quantitative analysis utilized historical sales figures, pricing trends, and macro‑economic indicators to model the forecast. Qualitative insights were derived from expert opinions on regulatory impacts, consumer behavior, and technology adoption.

18. What is the scope of this research and its limitations?

The scope covers global market size, segmentation by product type and application, regional performance, competitive landscape, and forward‑looking forecasts up to 2033. Limitations include reliance on publicly available financial disclosures, which may omit proprietary data, and the exclusion of granular market‑share percentages due to data confidentiality. Nevertheless, the analysis provides a comprehensive view of the Dairy Ingredients Market.

19. Which companies are highlighted and what recent developments have they announced?

Highlighted firms include AGROPUR, AMCO Proteins, Arla Foods Ingredients Group, Fonterra, FrieslandCampina Ingredient, Glanbia Ireland, Kerry Group, Lactalis Ingredients, PROLACTAL, and Saputo Inc. Recent developments feature AGROPUR’s launch of a high‑purity whey protein isolate targeting sports nutrition; Kerry Group’s partnership with a biotech start‑up to develop lactose‑free powders; Fonterra’s investment in renewable‑energy‑driven processing plants; and Glanbia’s acquisition of a specialty lactose‑derivative manufacturer to broaden its nutraceutical portfolio. These initiatives reflect the industry’s focus on innovation, sustainability, and market expansion.