What is the Cocoa Derivatives Market Overview – definition, scope, and significance?

The Cocoa Derivatives Market encompasses all traded products derived from cocoa beans, including cocoa butter, cocoa powder, and processed cocoa beans used in various downstream applications. Its scope covers both organic and conventional categories and serves key industries such as food & beverages and personal care. The market is significant because cocoa derivatives provide essential functional properties—flavor, texture, and health benefits—making them indispensable in confectionery, bakery, dairy, cosmetics, and nutraceutical formulations worldwide.

What are the main drivers, restraints, challenges, and opportunities shaping the Cocoa Derivatives Market?

Key drivers include rising consumer demand for premium chocolate products, growing interest in organic ingredients, and expanding personal‑care formulations that leverage cocoa’s antioxidant properties. Restraints stem from volatile cocoa bean prices, stringent sustainability regulations, and supply chain disruptions caused by climate‑related risks. Challenges involve ensuring traceability, meeting increasingly complex food‑safety standards, and competing with alternative plant‑based fats. Opportunities arise from product innovation—such as functional snacks and clean‑label cosmetics—and from emerging markets that are adopting Western consumption patterns.

What growth trends are currently influencing the Cocoa Derivatives Market?

Current trends feature a shift toward clean‑label and organic cocoa derivatives, driven by health‑conscious consumers. Manufacturers are also integrating cocoa butter alternatives to reduce saturated fat content while retaining melt‑in‑mouth sensations. Hybrid products that combine cocoa with super‑foods (e.g., beetroot, matcha) are gaining traction in the snack sector. Digital traceability platforms are being adopted to enhance supply‑chain transparency, appealing to sustainability‑focused buyers.

How did COVID‑19 impact the Cocoa Derivatives Market and what is the recovery trajectory?

The pandemic temporarily disrupted cocoa bean harvesting and logistics, leading to short‑term price spikes and inventory imbalances. Demand in the food‑service channel contracted, while retail sales of confectionery and home‑baking ingredients surged. Post‑2021, the market has rebounded steadily as supply chains normalized and consumer confidence returned. The recovery trajectory is positive, supported by pent‑up demand for indulgent products and continued growth in home‑cooking trends.

Who are the major competitors and what is the level of consolidation in the Cocoa Derivatives Market?

The competitive landscape is characterized by a mix of multinational agribusinesses and specialized cocoa processors. Leading players include Barry Callebaut AG, Cargill Inc, Olam Group Ltd, and Natra SA, alongside regional firms such as Alt?nmarka G?da San ve Tic AS and United Cocoa Processor Inc. The market exhibits moderate consolidation, with large firms acquiring niche processors to broaden organic portfolios and expand geographic reach.

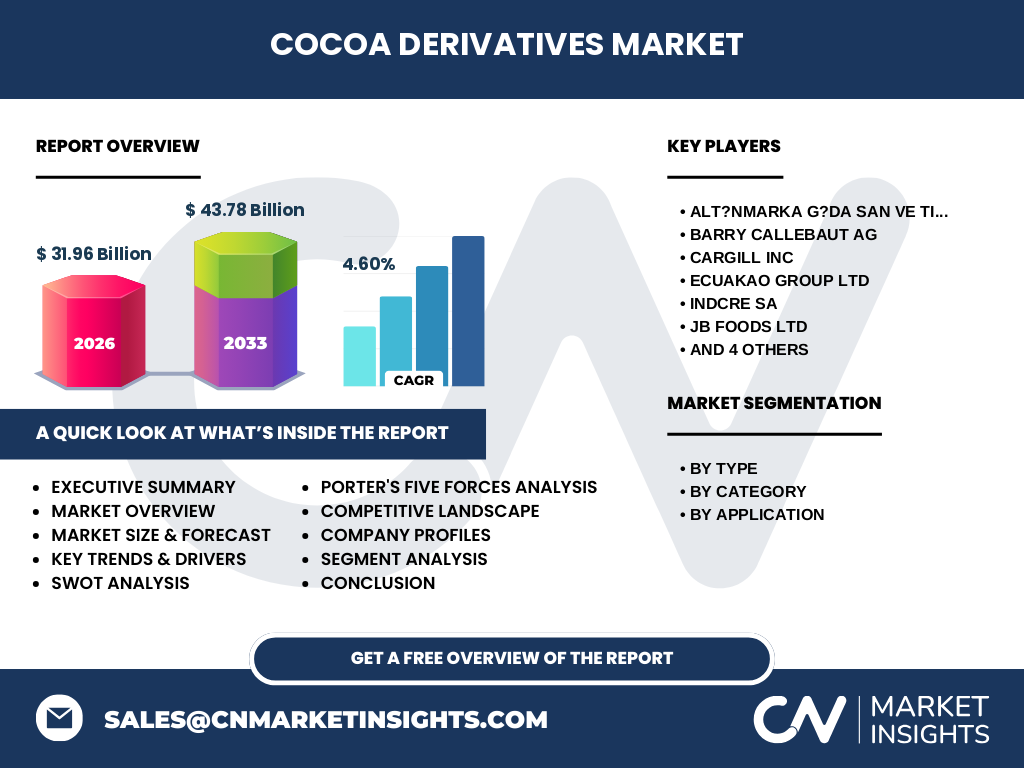

What are the high‑level insights and key findings in the Executive Summary of the Cocoa Derivatives Market?

The market is valued at US 31.96 billion in 2026 and is projected to reach US 43.78 billion by 2033, reflecting a CAGR of 4.60 % over the forecast horizon. Organic derivatives are accelerating faster than conventional segments, driven by clean‑label demand. Food & beverages remain the dominant application, yet personal‑care is emerging as a high‑growth niche. Geographic expansion in Asia‑Pacific and Africa presents the most untapped potential.

What is the forecast for the Cocoa Derivatives Market from 2025 to 2032?

Based on the stated CAGR of 4.60 %, the market is expected to continue expanding steadily through 2032. Growth will be propelled by rising disposable incomes in emerging economies, increasing adoption of organic cocoa products, and diversification of applications beyond traditional confectionery. The forecast underscores a robust trajectory that outpaces many adjacent commodity markets.

How is the Cocoa Derivatives Market sized and shared by segmentation?

By type, the market is divided into cocoa butter, cocoa beans, and cocoa powder, each serving distinct functional roles. By category, products are classified as organic or conventional, with organic commanding higher price premiums. By application, the split is between food & beverages—accounting for the majority share—and personal‑care, which is gaining relevance as manufacturers capitalize on cocoa’s skin‑benefiting properties.

What is the global distribution of Cocoa Derivatives Market size and share by region?

The market’s global footprint spans North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. While Europe and North America historically dominate due to mature chocolate consumption, Asia‑Pacific is witnessing the fastest growth rate as urbanization fuels demand for premium confectionery and functional foods.

What detailed insights can be drawn from the regional analysis of the Cocoa Derivatives Market?

In Europe, sustainability initiatives drive a surge in organic cocoa butter and powder. North America’s personal‑care segment benefits from innovative cosmetic formulations. Asia‑Pacific’s rapid middle‑class expansion translates into higher per‑capita consumption of cocoa‑based snacks. Latin America, a key cocoa‑bean producing zone, is adding value locally through processing facilities, while Africa’s market is poised for growth as infrastructure investments improve export capabilities.

Which companies lead the Cocoa Derivatives Market and what are their core strategies?

Barry Callebaut AG focuses on premium cocoa solutions and vertical integration from bean to bar. Cargill Inc leverages its extensive grain‑handling network to ensure supply stability. Olam Group Ltd emphasizes sustainable sourcing and farmer‑support programs. Natra SA invests in R&D for functional cocoa ingredients. Smaller players such as Alt?nmarka G?da San ve Tic AS differentiate through niche organic product lines and regional market focus.

How does Porter’s Five Forces analysis apply to the Cocoa Derivatives Market?

Threat of new entrants is moderate due to high capital requirements and stringent quality standards. Bargaining power of suppliers is relatively strong because cocoa beans are sourced from limited geographic regions susceptible to climate shocks. Bargaining power of buyers is growing as large food manufacturers demand traceability and sustainability. Threat of substitutes remains low; few alternatives replicate cocoa’s unique flavor and functional profile. Competitive rivalry is intense, driven by price competition, product innovation, and brand reputation.

What are the SWOT attributes of the Cocoa Derivatives Market?

Strengths: Strong global demand, versatile applications, and established supply chains. Weaknesses: Price volatility of raw cocoa beans and reliance on weather‑sensitive agriculture. Opportunities: Expansion into organic and functional segments, and growth in personal‑care applications. Threats: Regulatory pressure on sustainability, and potential supply disruptions from climate change.

What does the value chain of the Cocoa Derivatives Market look like?

The value chain begins with cocoa‑bean farming, followed by fermentation, drying, and shipping to processing hubs. At processing facilities, beans are transformed into cocoa liquor, from which cocoa butter, cocoa powder, and cocoa nibs are extracted. These derivatives are then packaged and distributed to food manufacturers, personal‑care formulators, and specialty ingredient distributors. Value‑add services such as certification, traceability, and custom blending occur throughout the chain.

What key investment insights can be derived for stakeholders in the Cocoa Derivatives Market?

Investors should prioritize companies with robust sustainability credentials and diversified product portfolios, as these are better positioned to capture premium pricing. Funding opportunities exist in downstream processing capacities—especially for organic cocoa butter—and in digital traceability platforms that enhance supply‑chain transparency. Partnerships with agritech firms can mitigate supply risks, while joint ventures in high‑growth regions like Asia‑Pacific can accelerate market entry.

What are the main conclusions drawn from the Cocoa Derivatives Market analysis?

The market demonstrates solid growth prospects, underpinned by a 4.60 % CAGR and a projected increase to US 43.78 billion by 2033. Organic differentiation, expanding personal‑care uses, and geographic diversification are the principal engines of growth. While supply‑side vulnerabilities persist, strategic investments in sustainability and value‑added processing can deliver competitive advantage.

How was the research for this report conducted?

The methodology combined primary interviews with industry experts, secondary data collection from reputable trade publications, company annual reports, and government statistics. Trend analysis, market sizing, and forecasting employed a combination of top‑down and bottom‑up approaches, calibrated to the provided market size and CAGR figures.

What is the scope of this research and its limitations?

The scope covers global market size, segmentation by type, category, and application, and regional performance up to 2033. It excludes granular market‑share percentages beyond the provided figures and does not delve into price forecasting or detailed macro‑economic modeling, focusing instead on strategic insights and growth directions.

Which key companies are highlighted and what recent developments have they announced?

Key players include Barry Callebaut AG (launch of a new organic cocoa butter line), Cargill Inc (strategic partnership with a West African farmer cooperative), Olam Group Ltd (investment in a sustainable cocoa processing plant in Vietnam), and Natra SA (introduction of a cocoa‑based functional ingredient for skin‑care). Smaller innovators such as Alt?nmarka G?da San ve Tic AS have announced expansion into the EU organic market, while United Cocoa Processor Inc reported a joint venture to enhance traceability across its supply chain.