What is the Carbon Black Market Overview – Definition, scope, and significance?

Carbon black is a fine black powder produced by the incomplete combustion of heavy petroleum products. It is primarily used as a reinforcing filler in rubber products and as a pigment in plastics, inks, and coatings. The market encompasses the production, distribution, and application of carbon black across multiple industries, including automotive (tires and non‑tire rubber), construction, packaging, and printing. Its significance lies in its ability to enhance mechanical strength, durability, and conductivity of materials, making it an essential component for modern manufacturing and a key driver of product performance and cost efficiency.

What are the Carbon Black Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include the steady growth of the global automotive sector, especially the demand for high‑performance tires, and the expanding use of carbon black in lightweight polymer composites for electric vehicles. Environmental regulations encouraging lower‑emission tires and the need for improved fuel efficiency also boost demand for specialty grades. Restraints arise from stringent emissions standards at production facilities, which increase operational costs. Challenges involve raw material price volatility and the emergence of alternative reinforcing agents such as silica. Opportunities are found in the development of nano‑structured carbon blacks for advanced electronics, the rising demand for specialty grades in high‑temperature applications, and strategic partnerships that enable access to emerging markets in Asia and Africa.

What are the Carbon Black Market Growth Trends?

Current trends include a shift toward specialty and high‑performance grades, driven by the automotive industry's focus on fuel efficiency and durability. Manufacturers are investing in research to produce carbon blacks with tailored conductivity for emerging applications in flexible electronics and energy storage. Another trend is geographic diversification, with increasing production capacity in emerging economies to meet local demand and reduce logistics costs. Sustainable production practices, such as the adoption of low‑emission furnace technologies, are also gaining traction as companies respond to environmental scrutiny.

How has COVID‑19 impacted the Carbon Black Market and what is the recovery trajectory?

The pandemic caused a temporary slowdown in tire production and automotive assembly lines, leading to a short‑term dip in carbon black demand. However, the market demonstrated resilience as lockdowns lifted and vehicle production rebounded. Recovery was accelerated by pent‑up consumer demand for personal mobility and a rapid resurgence in non‑tire rubber applications such as medical devices and consumer goods. The market is now on a clear upward trajectory, supported by strong fiscal stimulus in key regions and the continued rollout of electric vehicles, which are expected to sustain demand growth beyond the pandemic period.

Who are the major competitors in the Carbon Black Market and what does the competitive landscape look like?

The market is highly consolidated, featuring several global players with integrated production facilities and extensive distribution networks. Leading competitors include Cabot Corp, Continental Carbon Company, Tokai Carbon Co Ltd, and Orion Engineered Carbons SA. These firms compete on product quality, portfolio breadth, and technological innovation. Recent consolidation activities, such as strategic acquisitions and joint ventures, have intensified competition, encouraging firms to focus on specialty grades and value‑added services to differentiate themselves in a mature market.

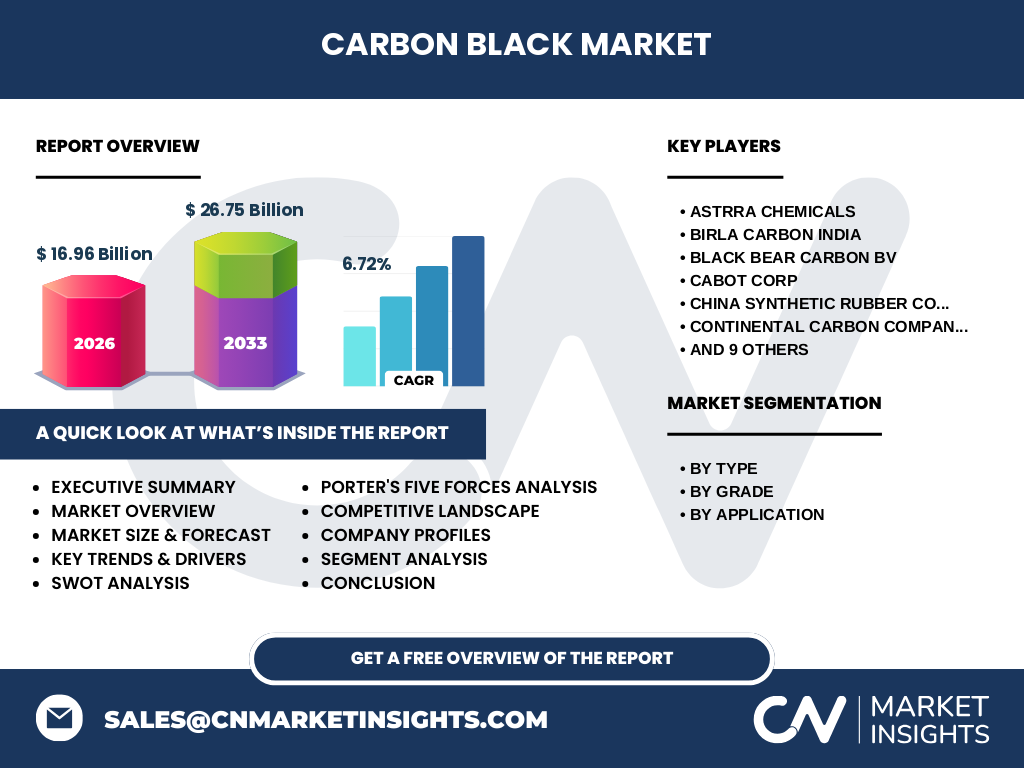

What are the key findings in the Executive Summary of the Carbon Black Market?

The carbon black market is projected to grow from a 2026 valuation of USD 16.96 billion to USD 26.75 billion by 2033, reflecting a compound annual growth rate (CAGR) of 6.72 %. Growth is fueled by expanding tire demand, rising use of specialty grades, and increased adoption in non‑tire rubber and polymer applications. Regional analysis shows strong performance in Asia‑Pacific, while Europe remains a hub for high‑specification specialty products. Competitive dynamics highlight a shift toward innovation, with leading firms investing in low‑emission production and advanced carbon black formulations. The market presents attractive opportunities for investors seeking exposure to both volume‑driven and high‑margin specialty segments.

What are the Carbon Black Market Forecasts for the 2025‑2032 period?

Based on the provided CAGR of 6.72 %, the market is expected to maintain steady growth throughout the forecast horizon. By 2032, the market size is anticipated to exceed USD 25 billion, driven by continuous demand in the tire sector and expanding applications in plastics, inks, and coatings. Specialty grades are projected to outpace standard grades, reflecting the industry's move toward performance‑oriented solutions. The forecast underscores the importance of innovation and geographic expansion as key levers for sustaining growth.

How is the Carbon Black Market sized and shared by segmentation?

The market is segmented by type, grade, and application. By type, furnace black remains the dominant segment due to its versatility and cost‑effectiveness, while acetylene, channel, and thermal blacks serve niche high‑performance applications. Grade segmentation distinguishes between standard grade, which dominates volume‑driven markets such as tire manufacturing, and specialty grade, which captures higher margins in electronics, high‑temperature rubber, and premium coatings. Application segmentation shows tire as the largest end‑use, followed by non‑tire rubber, plastics, and inks & coatings. Each segment contributes uniquely to the overall market structure, with specialty grades and non‑tire applications offering the fastest growth potential.

What is the Global Carbon Black Market size and share by region?

The global market is anchored by strong demand in Asia‑Pacific, reflecting the region’s extensive automotive production and rubber manufacturing base. North America and Europe together hold substantial shares, driven by mature tire markets and a focus on specialty carbon blacks for high‑performance applications. While exact regional monetary values are not disclosed, the distribution pattern indicates Asia‑Pacific as the primary growth engine, with Europe maintaining a leadership role in specialty‑grade innovation.

What does the Regional Analysis of the Carbon Black Market reveal?

Asia‑Pacific exhibits the highest growth rate, supported by expanding automotive output in China, India, and Southeast Asia, as well as increasing consumption of non‑tire rubber in construction and consumer goods. Europe’s market is characterized by stringent environmental regulations, prompting manufacturers to adopt low‑emission production technologies and develop higher‑value specialty grades. North America shows steady demand, largely tied to the performance‑oriented tire segment and a growing market for sustainable packaging plastics. Emerging markets in Latin America and the Middle East present nascent opportunities as infrastructure projects stimulate rubber and polymer consumption.

Which companies lead the Carbon Black Market and what are their strategic approaches?

Key players include Cabot Corp, known for its extensive specialty carbon black portfolio and strong R&D capabilities; Tokai Carbon Co Ltd, which leverages integrated production facilities across Asia and Europe to serve both volume and specialty segments; Orion Engineered Carbons SA, focusing on high‑performance powders for electronics and advanced composites; and Continental Carbon Company, emphasizing sustainable production and strategic partnerships. These companies pursue growth through capacity expansion, product innovation, and acquisitions that broaden geographic reach and technology depth.

How does Porter’s Five Forces assess the Carbon Black Market?

• Threat of new entrants: Low to moderate due to high capital intensity, stringent environmental compliance, and established economies of scale among incumbents.

• Bargaining power of suppliers: Moderate, as raw material (oil, natural gas) prices can affect margins, but large producers often secure long‑term contracts.

• Bargaining power of buyers: High in the tire segment because of large, consolidated tire manufacturers who demand consistent quality and price stability.

• Threat of substitutes: Growing, with silica and other reinforcing agents gaining market share in low‑rolling‑resistance tires.

• Industry rivalry: Intense, driven by product differentiation, capacity utilization, and innovation in specialty grades.

What is the SWOT analysis of the Carbon Black Market?

Strengths: Proven demand in automotive and rubber industries; wide range of applications; established supply chains.

Weaknesses: High energy consumption and emissions in production; dependence on fossil‑based feedstocks.

Opportunities: Development of nano‑carbon blacks for electronics; expansion into sustainable packaging; growth in emerging economies.

Threats: Regulatory pressure on emissions; competition from silica and bio‑based fillers; volatility in oil and gas prices.

How is the Carbon Black Market value chain structured?

The value chain begins with upstream raw material sourcing (heavy petroleum oils, natural gas), followed by manufacturing processes (furnace, channel, acetylene, thermal methods). Midstream activities involve product grading, quality control, and packaging. Downstream, carbon black is distributed to tire manufacturers, rubber compounders, plastics processors, and ink/coating producers. Value creation is enhanced through R&D for specialty grades, logistics optimization, and after‑sales technical support to tailor formulations for end‑users.

What are the key investment insights in the Carbon Black Market?

Investors should focus on companies with diversified product portfolios that balance high‑volume furnace blacks and high‑margin specialty grades. Capital allocation toward low‑emission production technologies can mitigate regulatory risk and improve ESG credentials. Geographic diversification, particularly increasing exposure to fast‑growing Asian markets, offers upside potential. Strategic investments in R&D for nano‑structured and conductive carbon blacks align with the surge in electronics and energy storage, presenting a compelling growth narrative.

What conclusions can be drawn from the Carbon Black Market analysis?

The carbon black market is on a robust growth trajectory, underpinned by a 6.72 % CAGR and expanding applications beyond traditional tire reinforcement. While environmental constraints pose challenges, they also stimulate innovation in cleaner production and specialty products. Companies that invest in advanced grades, sustainable processes, and emerging geographies are positioned to capture the greatest share of future market value. The overall outlook remains positive, with strong fundamentals supporting continued expansion through 2032.

What research methodology was employed for this market study?

The research combined primary interviews with industry experts, senior executives, and supply‑chain participants, alongside secondary data collection from company reports, industry publications, and governmental databases. Market sizing utilized a top‑down approach anchored on the provided 2026 market value, calibrated with historic growth rates and corroborated through triangulation of multiple data sources. Forecasting applied compound annual growth rate (CAGR) calculations and scenario analysis to reflect potential macro‑economic influences.

What is the scope of the Carbon Black Market research?

The study covers global production, consumption, and trade of carbon black, segmented by type, grade, and end‑use application. Geographic coverage includes major regions—Asia‑Pacific, Europe, North America, and emerging markets in Latin America and the Middle East. The scope extends to competitive dynamics, value‑chain analysis, and forward‑looking forecasts up to 2033, providing insight into both volume‑driven and specialty segments.

Which key companies have recent developments in the Carbon Black Market?

Recent announcements include Cabot Corp’s launch of a new high‑performance conductive carbon black for flexible printed electronics, Tokai Carbon’s partnership with a leading electric‑vehicle battery manufacturer to supply specialty blacks for electrode coatings, and Orion Engineered Carbons’ acquisition of a niche European plant to boost specialty grade capacity. Additionally, Black Bear Carbon BV has expanded its furnace capacity in Europe, while Imerys SA introduced a low‑emission furnace technology aimed at reducing carbon footprints across its production sites.