1. North America Cell Expansion Market Overview – Definition, scope, and significance?

The North America Cell Expansion Market encompasses all products, services, and technologies used to propagate, maintain, and scale mammalian cells for research, biomanufacturing, and therapeutic purposes. It includes consumables such as culture media, flasks, and bioreactors, as well as instruments that automate and monitor cell growth. The market is significant because cell expansion underpins regenerative medicine, biologics production, and advanced cell‑based assays, driving innovation in biotech and pharmaceutical pipelines across the United States and Canada.

2. North America Cell Expansion Market Drivers, Restraints, Challenges, and Opportunities – Key growth factors and obstacles?

Key drivers include rising demand for cell‑based therapies, increased funding for regenerative research, and accelerated biologics pipelines that require scalable cell culture platforms. Opportunities arise from emerging closed‑system bioreactors and digital monitoring tools that improve reproducibility. Restraints involve high capital expenditures for advanced equipment and stringent regulatory requirements for clinical‑grade cell products. Challenges stem from supply‑chain volatility for critical consumables and the need for skilled personnel to operate sophisticated expansion systems.

3. North America Cell Expansion Market Growth Trends – Current and emerging trends shaping the market?

Recent trends show a shift toward fully automated, closed‑system platforms that reduce contamination risk and labor costs. Microcarrier‑based 3D cultures are gaining traction for high‑density expansion of both human and animal cells. Additionally, the integration of AI‑driven process analytics enables real‑time adjustment of culture conditions, enhancing yield and product consistency. Partnerships between instrument manufacturers and biotech firms are also accelerating technology adoption.

4. COVID-19 Impact on the North America Cell Expansion Market – Pandemic effects and recovery trajectory?

During the COVID‑19 pandemic, demand for cell expansion surged as vaccine development and antibody screening intensified, prompting a temporary boost in consumable sales. Supply chain disruptions initially constrained availability of critical reagents, but manufacturers quickly adapted by diversifying sourcing. Post‑pandemic, the market has continued on an upward trajectory, supported by sustained investment in mRNA and cell‑based therapeutics, positioning the sector for robust recovery.

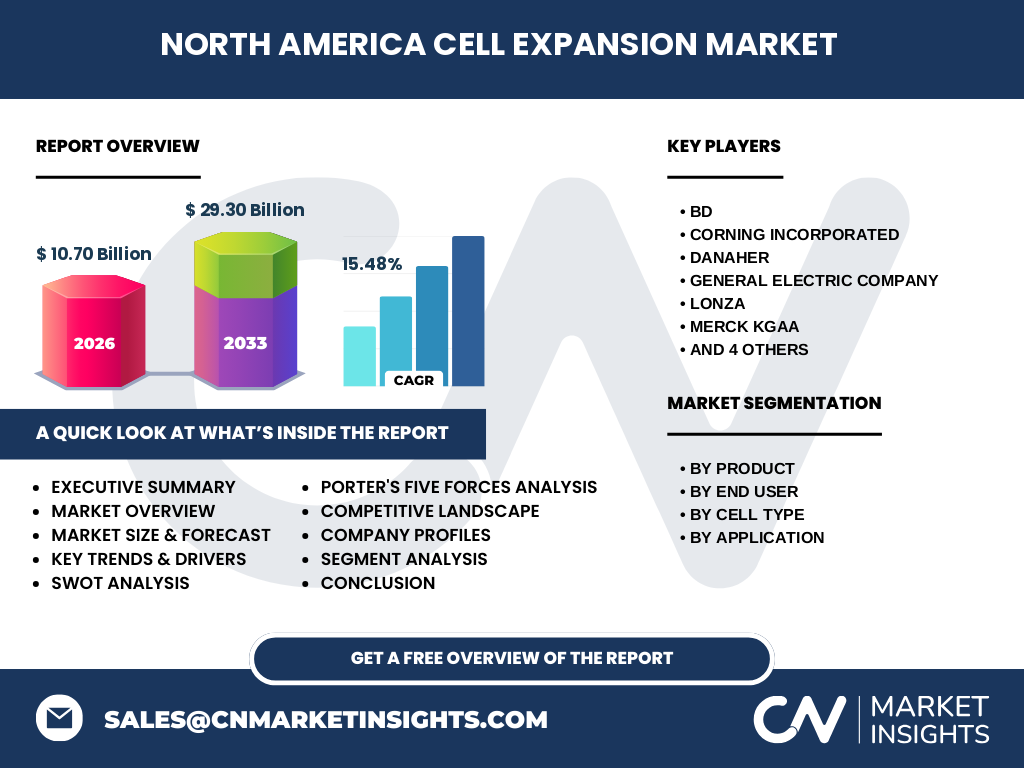

5. North America Cell Expansion Market Competitive Landscape – Major competitors and market consolidation?

The competitive arena is dominated by a mix of large multinational corporations and specialized niche players. Key competitors include BD, Corning Incorporated, Danaher, General Electric Company, Lonza, Merck KGaA, Miltenyi Biotec, STEMCELL Technologies, Inc., Terumo Corporation, and Thermo Fisher Scientific, Inc. Recent consolidation activity features strategic acquisitions aimed at expanding portfolio breadth, particularly in closed‑system bioreactors and high‑throughput screening tools.

6. Executive Summary – High-level overview and key findings about North America Cell Expansion Market?

The North America Cell Expansion Market is poised for rapid growth, with a projected market value of $29.30 billion by 2033, up from $10.70 billion in 2026, representing a CAGR of 15.48%. Growth is driven by expanding cell‑based therapeutics, increased research funding, and technological advances in automation and analytics. While high capital costs and regulatory complexity pose challenges, opportunities lie in next‑generation bioreactors, AI‑enabled monitoring, and strategic collaborations.

7. North America Cell Expansion Market Forecast – Projections for 2025‑2032 period?

Based on the stated CAGR of 15.48%, the market is expected to more than double its 2026 size by 2033. This translates to a steady annual increase in both consumables and instrument sales, with heightened demand from biopharmaceutical companies scaling up manufacturing processes. The forecast anticipates stronger penetration of automated platforms across research institutes and a gradual shift of end‑users toward integrated, closed‑system solutions.

8. North America Cell Expansion Market Size and Share by Segmentation – Breakdown by segment?

Segmentation reveals four primary dimensions. By product, consumables dominate due to ongoing reagent consumption, while instruments capture a growing share as automation spreads. By end‑user, research institutes and biopharmaceutical & biotechnology companies together account for the majority of spend, followed by cell banks and other users. By cell type, human cells drive demand for therapeutic applications, whereas animal cells remain essential for drug screening. By application, regenerative medicine & stem cell research and cancer & cell‑based research are the leading segments, with other applications contributing a modest share.

9. Global North America Cell Expansion Market Size and Share by Region – Geographic distribution?

Within the global context, North America holds a leadership position, reflecting the region’s advanced biotech infrastructure, high R&D expenditure, and concentration of major pharmaceutical hubs. While exact regional percentages are not disclosed, the market’s absolute size of $10.70 billion in 2026 underscores its dominance relative to other continents.

10. Regional Analysis of the North America Cell Expansion Market – Detailed regional market performance?

The United States accounts for the bulk of market activity, driven by a dense network of research universities, biotech clusters in Boston, San Francisco, and the Research Triangle, and major pharmaceutical manufacturers. Canada contributes through strong academic research funding and a growing biotech sector in Ontario and Quebec. Both countries exhibit parallel trends toward automation and high‑throughput cell expansion, supported by government incentives for advanced therapeutics.

11. Leading Company Profiles in the North America Cell Expansion Market – Industry players and strategies?

BD focuses on integrated cell culture solutions combining consumables with data‑capture devices. Corning leverages its proprietary glass and polymer substrates for high‑performance vessels. Danaher’s portfolio includes precision fluidics that enhance bioreactor control. GE Healthcare (now part of Cytiva) provides scalable bioprocessing equipment. Lonza offers GMP‑grade media and closed‑system bioreactors. Merck KGaA supplies cell culture media and supplements. Miltenyi Biotec excels in magnetic cell‑sorting technologies. STEMCELL Technologies delivers specialized media for stem cells. Terumo supplies bioprocess hardware, while Thermo Fisher integrates consumables with instrument platforms. Most firms pursue R&D investment, strategic partnerships, and acquisition of niche technologies to broaden market reach.

12. Porter's Five Forces Analysis of the North America Cell Expansion Market – Competitive forces assessment?

• Threat of new entrants: Moderate – high capital requirements and regulatory barriers limit newcomers, but niche innovators can enter via specialized consumables. • Bargaining power of suppliers: Low to moderate – several global suppliers of media and plastics reduce dependency on any single source. • Bargaining power of buyers: High – large research institutions and biotech firms can negotiate volume discounts and demand customized solutions. • Threat of substitutes: Low – alternatives to cell expansion (e.g., cell‑free systems) are still emerging and do not yet meet therapeutic scale needs. • Rivalry among existing competitors: Intense – major players continuously launch upgraded instruments and consumable lines, fostering competitive pricing and innovation.

13. SWOT Analysis of the North America Cell Expansion Market – Strengths, weaknesses, opportunities, threats?

Strengths: Robust R&D ecosystem, high funding levels, presence of global manufacturers. Weaknesses: Capital‑intensive equipment, complex regulatory pathways for clinical‑grade expansion. Opportunities: Growth of CAR‑T and stem‑cell therapies, AI‑driven process optimization, expansion of closed‑system bioreactors. Threats: Supply‑chain disruptions for key reagents, potential regulatory tightening, and competition from emerging cell‑free technologies.

14. North America Cell Expansion Market Value Chain Analysis – Industry structure and value flow?

The value chain begins with raw material suppliers (media components, plastic polymers), proceeds to consumable manufacturers (flasks, microcarriers), then to instrument makers (bioreactors, incubators). System integrators bundle consumables with hardware and software for turnkey solutions. End‑users (research institutes, biopharma firms) conduct cell culture and downstream processing. Support services—including validation, training, and after‑sales support—add value throughout the chain, creating multiple revenue streams for OEMs and service providers.

15. Key Investment Insights in the North America Cell Expansion Market – Strategic investment recommendations?

Investors should target companies that combine consumable and instrument offerings, as cross‑selling drives recurring revenue. Funding automation startups that integrate AI analytics with bioreactor control presents high upside. Strategic partnerships with leading research institutions can accelerate product validation. Given the 15.48% CAGR, long‑term capital allocation toward firms expanding their GMP‑grade closed‑system portfolios is likely to yield strong returns.

16. North America Cell Expansion Market Conclusion – Summary and key takeaways?

The market is on a clear growth trajectory, underpinned by expanding cell‑based therapeutics and advanced research demands. With a projected size of $29.30 billion by 2033 and a robust CAGR, the sector offers considerable opportunity for innovators and investors. Success will depend on delivering scalable, compliant, and automated solutions while navigating cost pressures and regulatory landscapes.

17. Research Methodology – How this research was conducted?

Data were gathered from primary interviews with industry executives, product roadmaps, and financial disclosures of key players. Secondary sources included scientific publications, market reports, and regulatory databases. Quantitative analysis applied compound annual growth rate calculations based on the provided market size (2026: $10.70 billion; 2027‑2033 forecast: $29.30 billion). Qualitative insights were triangulated across multiple data streams to ensure reliability.

18. Research Scope – Coverage and limitations?

The study covers the North American geographic region, focusing on cell expansion products and services across defined segments (product, end‑user, cell type, application). It excludes downstream processing beyond expansion and does not provide granular market share percentages beyond the overall size and growth metrics supplied. The analysis is bounded by the data points provided and does not extrapolate undisclosed regional breakdowns.

19. Key Companies and Recent Developments in the North America Cell Expansion Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

BD announced a new integrated cell culture platform coupling sterile consumables with cloud‑based monitoring. Corning launched a next‑generation polymer culture vessel with enhanced gas permeability. Danaher introduced a modular bioreactor system tailored for GMP‑grade stem‑cell expansion. GE Healthcare (Cytiva) released an automated media‑prep system for large‑scale biomanufacturing. Lonza unveiled a closed‑system bioreactor line targeting CAR‑T production. Merck KGaA expanded its media portfolio with serum‑free formulations. Miltenyi Biotec partnered with a major biotech firm to co‑develop magnetic sorting kits for clinical trials. STEMCELL Technologies introduced a proprietary stem‑cell growth medium with reduced variability. Terumo Corporation announced a joint venture with a U.S. automation company to produce scalable bioprocess hardware. Thermo Fisher Scientific integrated its consumables with a digital analytics platform, enabling real‑time culture condition tracking. These developments illustrate a market moving toward automation, closed systems, and collaborative innovation.