What is the Europe POS Software Market Overview – Definition, scope, and significance?

The Europe POS (Point‑of‑Sale) Software Market comprises solutions that enable retailers, restaurants, hospitality venues and service providers to process transactions, manage inventory, and integrate with back‑office functions such as payroll and customer relationship management. The market’s scope covers all software components and related services, delivered via on‑premise or cloud deployments, and serves enterprises of all sizes—from small boutiques to large multinational chains. Its significance lies in driving operational efficiency, enhancing the shopper experience, and providing data‑driven insights that are critical for competitive advantage in a highly fragmented retail landscape across the continent.

What are the Europe POS Software Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include the rapid adoption of omnichannel retail strategies, the need for real‑time inventory visibility, and increasing demand for contactless payments accelerated by consumer expectations for speed and safety. Cloud‑based deployments further fuel growth by lowering upfront costs and enabling scalable updates. Restraints stem from stringent data‑privacy regulations such as GDPR, which increase compliance costs, and the legacy infrastructure present in some traditional retailers. Challenges involve integrating diverse payment methods across 30+ European currencies and managing cybersecurity threats. Opportunities arise from emerging AI‑powered analytics, personalised loyalty programmes, and the expansion of POS capabilities into new verticals such as booking systems for the hospitality sector.

What are the Europe POS Software Market Growth Trends?

Current trends highlight a decisive shift toward cloud‑first architectures, with many vendors offering subscription models that include continuous feature upgrades. Mobile POS solutions are gaining traction, especially among small and medium enterprises seeking flexibility on the sales floor. Integration of advanced analytics and machine‑learning modules enables predictive inventory management and dynamic pricing. Furthermore, the convergence of POS with ecommerce platforms creates seamless omnichannel experiences, while contactless and QR‑code payment options are becoming standard. These trends collectively shape a market that is increasingly data‑centric and service‑oriented.

How has COVID‑19 impacted the Europe POS Software Market and what is the recovery trajectory?

The pandemic initially disrupted traditional brick‑and‑mortise sales, prompting many retailers to accelerate digital transformation initiatives. Demand for remote management, cloud‑based solutions, and contactless payment surged as businesses sought to maintain operations under lockdown restrictions. Post‑2020, recovery has been steady, driven by a hybrid retail model where physical stores complement robust online channels. The market’s trajectory shows a strong rebound, with firms investing in scalable POS platforms that can support both in‑store and curbside fulfilments, reinforcing long‑term growth prospects.

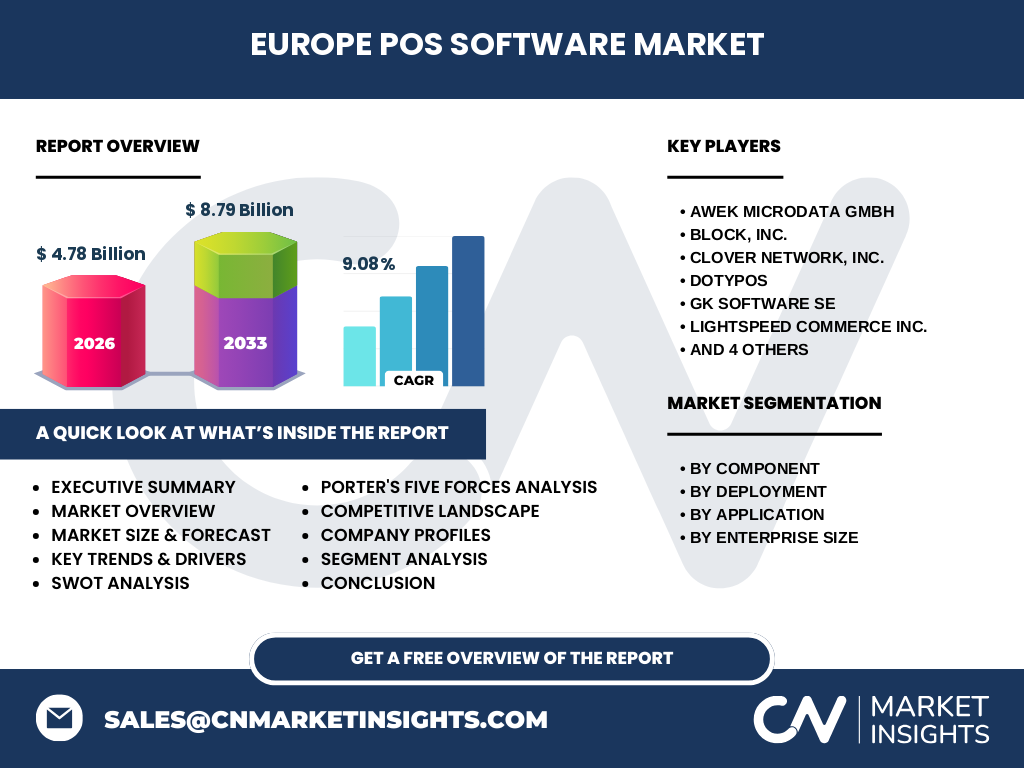

Who are the major competitors and what is the level of consolidation in the Europe POS Software Market?

The competitive landscape features a mix of established European players and international technology firms. Prominent companies include AWEK microdata GmbH, Block, Inc., Clover Network, Inc., Dotypos, GK Software SE, LightSpeed Commerce Inc., Shore GmbH, dascus GmbH, orderbird AG, and ready2order GmbH. Consolidation activity is moderate, with strategic acquisitions aimed at expanding cloud capabilities and geographic reach. Partnerships with payment processors and hardware manufacturers further intensify competition, encouraging innovation while maintaining a diverse vendor ecosystem.

What are the key findings highlighted in the Executive Summary?

The Europe POS Software Market is projected to grow from a 2026 valuation of €4.78 billion to €8.79 billion by 2033, reflecting a robust CAGR of 9.08 %. Growth is propelled by cloud adoption, omnichannel integration, and heightened demand for data‑rich analytics. Small and medium enterprises are the fastest adopters, while large enterprises focus on comprehensive ecosystem integration. Regulatory compliance and cybersecurity remain critical focus areas. The market presents attractive investment opportunities, especially in AI‑enabled features and cross‑border payment solutions.

What does the Europe POS Software Market Forecast indicate for 2025‑2032?

Forecasts anticipate a steady upward trajectory, maintaining an average annual growth rate near the historical 9 %. By 2032, the market is expected to exceed €9 billion, driven by continued cloud migration, expansion of mobile POS usage, and deeper integration with ecommerce platforms. Emerging verticals such as hospitality booking systems and payroll‑linked POS modules will contribute incremental revenue streams, reinforcing the market’s diversified growth path.

How is the Europe POS Software Market sized and shared by segmentation?

By component, the market is split between software licences and ancillary services, with services—including support, maintenance, and analytics—capturing a growing share as customers shift to subscription models. Deployment segmentation shows cloud solutions overtaking on‑premise installations, reflecting preferences for lower capital expenditure and faster feature roll‑out. Application‑wise, inventory tracking and sales reporting dominate, while customer engagement, booking systems, and payroll management register rapid growth rates, particularly among medium and large enterprises. Enterprise‑size segmentation indicates that small enterprises account for the largest volume of installations, whereas large enterprises command the highest average revenue per user due to complex integration needs.

What is the global Europe POS Software Market size and share by region?

Within the broader global context, Europe represents a significant share of the worldwide POS software landscape, anchored by mature retail sectors in Western and Northern Europe and fast‑growing markets in Central and Eastern Europe. While exact numerical shares are not disclosed, the €4.78 billion 2026 valuation underscores Europe’s role as a primary growth engine, complementing strong markets in North America and Asia‑Pacific.

What does the Regional Analysis of the Europe POS Software Market reveal?

Western European economies such as Germany, France, and the United Kingdom exhibit the highest adoption rates, driven by extensive retail networks and early cloud adoption. Northern Europe, particularly the Nordics, leads in mobile POS and contactless payment usage. Central and Eastern European nations display rapid growth, propelled by digital‑first strategies among emerging retailers. Regional regulatory nuance, especially around data protection, influences deployment preferences, with cloud solutions gaining prevalence where local data‑centres meet compliance standards.

What are the leading company profiles and their strategic approaches?

AWEK microdata GmbH leverages deep analytics expertise to offer AI‑enhanced decision tools. Block, Inc. expands its ecosystem through strategic partnerships with payment processors. Clover Network, Inc. focuses on modular hardware‑software bundles for quick deployment. Dotypos differentiates with niche hospitality solutions, while GK Software SE emphasizes robust ERP integration. LightSpeed Commerce Inc. targets omnichannel retailers with unified storefront management. Shore GmbH and dascus GmbH cater to small retailers with affordable cloud licences. orderbird AG and ready2order GmbH prioritize user‑friendly mobile interfaces and rapid onboarding. Collectively, these firms balance innovation with compliance to capture distinct market segments.

How does Porter’s Five Forces analysis apply to the Europe POS Software Market?

Threat of new entrants is moderate; low entry barriers for SaaS platforms are offset by the need for compliance and integration expertise. Bargaining power of buyers is high, as retailers can switch vendors easily and demand tailored pricing. Bargaining power of suppliers (hardware manufacturers) is moderate, given the proliferation of generic devices. Threat of substitutes remains low because POS software is central to transaction processing and data capture. Industry rivalry is intense, driven by rapid innovation cycles, price competition, and the pursuit of value‑added services.

What are the SWOT insights for the Europe POS Software Market?

Strengths: Established retail infrastructure, high digital maturity, and robust cloud adoption. Weaknesses: Fragmented standards across countries and ongoing regulatory compliance costs. Opportunities: AI‑driven analytics, expanded omnichannel capabilities, and growth in hospitality booking integrations. Threats: Cybersecurity breaches, evolving payment regulations, and potential market saturation in core retail segments.

What does the Europe POS Software Market Value Chain analysis show?

The value chain begins with software development and cloud‑service provisioning, followed by integration services, hardware manufacturing, and end‑user deployment. Post‑sale, the chain includes training, support, and continuous data‑analytics services that generate recurring revenue. Partnerships with payment gateways and ERP vendors sit at the intersection of technology and service layers, adding strategic value and facilitating smoother client onboarding.

What investment insights can be drawn for the Europe POS Software Market?

Investors should consider funding vendors that prioritize cloud scalability and AI‑enabled modules, as these capabilities align with the market’s growth trajectory. Cross‑border payment solutions and compliance‑as‑a‑service platforms present niche yet high‑margin opportunities. Mergers that combine POS software with strong ecommerce or ERP capabilities can yield synergistic benefits and accelerate market share gains.

What are the concluding remarks on the Europe POS Software Market?

The Europe POS Software Market is on a clear expansion path, underpinned by a 9.08 % CAGR and a projected valuation of €8.79 billion by 2033. Cloud migration, omnichannel integration, and data‑centric functionalities are the core pillars of this growth. While regulatory and security considerations remain pivotal, the market offers compelling opportunities for vendors, investors, and retailers seeking to modernise their transaction ecosystems.

What research methodology was employed for this analysis?

The study combined primary interviews with industry executives, secondary data extraction from reputable market reports, and quantitative modelling using historical revenue figures. Trend extrapolation applied a compound annual growth rate (CAGR) of 9.08 % to forecast the 2027‑2033 period. Segmentation analysis leveraged the provided component, deployment, application, and enterprise‑size categories to allocate market size accurately.

What is the scope of the research and its limitations?

The research covers the full spectrum of POS software solutions sold in Europe, across all deployment models and enterprise sizes, and includes the ten listed key companies. Geographic scope is limited to European territories; the study does not extend to specific country‑level financial breakdowns beyond the provided regional overview. Forecasts assume continuation of current economic conditions and regulatory frameworks.

Which key companies and recent developments are shaping the Europe POS Software Market?

Recent developments include AWEK microdata GmbH’s launch of an AI‑driven sales forecasting module, Block, Inc.’s partnership with a major European bank to streamline contactless payments, and GK Software SE’s integration of its POS suite with leading ERP platforms. LightSpeed Commerce Inc. introduced a unified omnichannel dashboard, while orderbird AG released a low‑cost mobile POS aimed at micro‑retailers. These initiatives reflect a market focused on innovation, partnership, and expanding functional breadth.