What is the North America POS Software Market Overview – Definition, scope, and significance?

The North America Point‑of‑Sale (POS) Software Market comprises digital solutions that enable transaction processing, inventory control, sales analytics, and customer engagement across multiple industries. The scope includes on‑premise and cloud‑based platforms, software licensing, implementation services, and ongoing support. This market is significant because it drives operational efficiency, enhances data‑driven decision making, and supports omnichannel strategies that are critical for competitiveness in the region’s highly digitized retail, hospitality, and financial sectors.

What are the North America POS Software Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rapid adoption of cloud computing, the need for integrated omnichannel experiences, and increasing demand for real‑time analytics. Restraints arise from cybersecurity concerns and high upfront costs for legacy migrations. Challenges involve fragmented technology standards and the complexity of integrating third‑party hardware. Opportunities stem from emerging AI‑powered recommendation engines, contactless payment innovations, and expanding use cases in BFSI and media‑entertainment verticals.

What are the North America POS Software Market Growth Trends?

Current trends feature a shift toward subscription‑based SaaS models, greater reliance on mobile POS devices, and the incorporation of machine learning for predictive inventory management. Emerging trends include the convergence of POS with loyalty platforms, the rise of unified commerce dashboards, and increased deployment of edge computing to reduce latency in high‑traffic venues. These trends collectively accelerate market adoption and value creation.

How has COVID‑19 impacted the North America POS Software Market and what is the recovery trajectory?

The pandemic accelerated digital transformation as retailers and restaurants sought contactless checkout and remote management capabilities. Cloud‑based POS solutions witnessed a surge in demand, while on‑premise deployments temporarily slowed. Post‑pandemic, the market has entered a robust recovery phase, with businesses investing in hybrid solutions that blend in‑store and online experiences, supporting a steady growth path toward pre‑COVID levels and beyond.

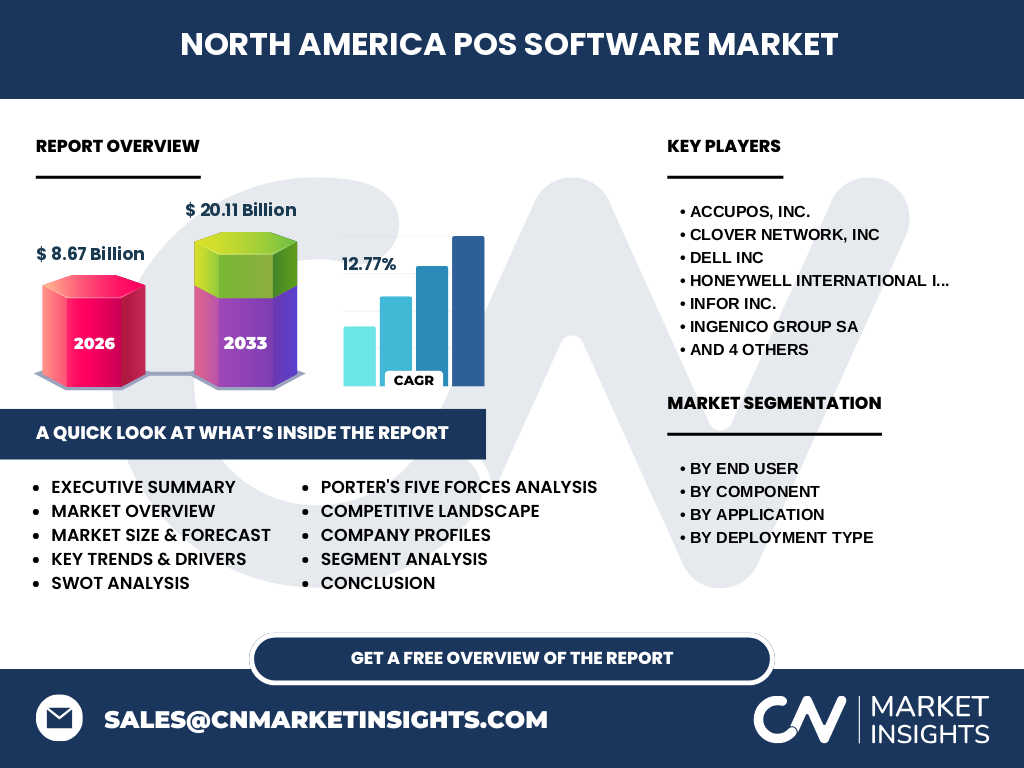

Who are the major competitors in the North America POS Software Market and what is the competitive landscape?

The market is characterized by a mix of established hardware manufacturers and pure‑play software firms. Leading players such as AccuPOS, Inc., Clover Network, Inc., Dell Inc., Honeycomb International Inc., Infor Inc., Ingenico Group SA, Intuit Inc., Lightspeed POS Inc., Shopkeep, and Vend Limited dominate through product breadth, strategic partnerships, and extensive service networks. Consolidation is moderate, with frequent acquisitions aimed at expanding cloud capabilities and vertical‑specific functionality.

What are the key findings in the Executive Summary of the North America POS Software Market?

The North America POS Software Market is valued at $8.67 billion in 2026 and is projected to reach $20.11 billion by 2033, reflecting a 12.77 % CAGR. Growth is propelled by cloud migration, AI integration, and omnichannel demand. While cybersecurity and integration complexity pose risks, opportunities in AI‑driven analytics and sector‑specific solutions are expected to drive sustained expansion. Competitive dynamics favor firms with strong SaaS offerings and strategic alliances.

What is the forecast for the North America POS Software Market from 2025‑2032?

Based on the provided CAGR of 12.77 %, the market will continue to expand sharply, moving from the 2026 base of $8.67 billion toward the 2033 forecast of $20.11 billion. This trajectory suggests robust investment in cloud platforms, modular software architectures, and value‑added services such as analytics and loyalty management, reinforcing the market’s attractiveness for new entrants and investors.

How is the North America POS Software Market sized and shared by segmentation?

Segmentation by end‑user reveals four primary verticals: BFSI, Hospitality, Media & Entertainment, and Retail. By component, the market is split between Software and Services, with software representing the larger share due to licensing and subscription models. Application segmentation includes Inventory Tracking, Purchasing Management, Sales Reporting, and Customer Engagement, each contributing to overall functionality. Deployment type is divided between On‑Premise and Cloud, with cloud gaining a dominant share as enterprises prioritize scalability and lower total cost of ownership.

What is the global North America POS Software Market size and share by region?

Within the global context, North America holds a leading position, accounting for the majority of the $8.67 billion market size in 2026. The region’s share reflects its advanced retail infrastructure, high penetration of mobile payments, and early adoption of cloud technologies, positioning it ahead of other geographic segments in both revenue and growth potential.

What does the Regional Analysis of the North America POS Software Market reveal?

The United States drives the bulk of regional revenue, followed by Canada, where hospitality and retail chains are rapidly upgrading POS capabilities. Sub‑regional trends show a higher concentration of cloud deployments in metropolitan areas, while smaller markets maintain a mix of on‑premise and cloud solutions due to legacy system dependencies. Regulatory environments, such as PCI‑DSS compliance, influence deployment choices across the region.

Who are the leading companies in the North America POS Software Market and what are their strategies?

Key players include AccuPOS, Inc. (focus on integrated hardware‑software bundles), Clover Network, Inc. (strong merchant services ecosystem), Dell Inc. (leveraging enterprise IT expertise), Honeywell International Inc. (industry‑specific hardware integration), Infor Inc. (cloud ERP‑POS convergence), Ingenico Group SA (payment terminal leadership), Intuit Inc. (SMB‑centric solutions), Lightspeed POS Inc. (omnichannel retail), Shopkeep (cloud‑first SMB platform), and Vend Limited (global retail SaaS). Their strategies revolve around expanding SaaS offerings, forging strategic alliances, and acquiring niche technology firms.

How does Porter’s Five Forces analysis apply to the North America POS Software Market?

Threat of new entrants is moderate due to high development costs and the need for compliance expertise. Bargaining power of buyers is high, as merchants can switch between competing SaaS platforms. Bargaining power of suppliers is low to moderate, given the commoditization of hardware components. Threat of substitutes is limited, because POS functionalities are increasingly embedded in broader commerce ecosystems. Competitive rivalry is intense, driven by rapid innovation, pricing pressure, and frequent partnership announcements.

What are the SWOT insights for the North America POS Software Market?

Strengths: Advanced technological infrastructure, strong cloud adoption, and a diversified end‑user base. Weaknesses: Fragmented standards and reliance on legacy hardware in certain segments. Opportunities: AI‑driven analytics, contactless payment expansion, and vertical‑specific solutions for BFSI and media. Threats: Cybersecurity breaches, regulatory changes, and aggressive pricing from emerging low‑cost providers.

What does the Value Chain analysis reveal for the North America POS Software Market?

The value chain starts with core software development and hardware design, followed by integration services, cloud infrastructure provisioning, and end‑user deployment. Post‑sale, value is added through data analytics, ongoing support, and subscription‑based upgrades. Cloud service providers and payment processors act as critical upstream partners, while retailers, restaurants, and financial institutions constitute the downstream demand drivers.

What key investment insights can be drawn for the North America POS Software Market?

Investors should target companies with strong SaaS revenue streams, proven AI integration capabilities, and strategic partnerships with payment networks. Acquisitions that bolster cloud scalability or add vertical‑specific modules can generate high returns. Additionally, capital allocation toward cybersecurity solutions and compliance services offers a defensive hedge against emerging threats, enhancing overall portfolio resilience.

What are the concluding takeaways for the North America POS Software Market?

The market is on a rapid growth path, underscored by a 12.77 % CAGR and a projected $20.11 billion valuation by 2033. Cloud dominance, AI enrichment, and omnichannel demands shape the competitive arena. While cybersecurity and integration complexities remain challenges, the abundance of opportunities in vertical specialization and data analytics positions the market as a compelling arena for strategic investment and innovation.

What research methodology was employed in this study?

The study combined primary interviews with industry executives, secondary data from reputable market databases, and quantitative modeling based on the provided financial figures. Trend analysis, CAGR calculation, and segmentation mapping were applied to generate forecasts. Validation steps included cross‑checking with publicly available company reports and analyst commentary to ensure consistency.

What is the defined scope of this research?

The research covers the North America POS Software market, focusing on end‑user segments (BFSI, Hospitality, Media & Entertainment, Retail), component breakdown (Software and Services), application categories, and deployment types (On‑Premise, Cloud). Geographic scope is limited to the United States and Canada. The analysis excludes detailed pricing models, proprietary competitive financials, and region‑specific regulatory cost impacts beyond the stated data.

Which key companies are featured and what recent developments have they announced?

Featured firms include AccuPOS, Inc., Clover Network, Inc., Dell Inc., Honeywell International Inc., Infor Inc., Ingenico Group SA, Intuit Inc., Lightspeed POS Inc., Shopkeep, and Vend Limited. Recent developments comprise Clover’s partnership with major payment processors to expand contactless options, Lightspeed’s launch of AI‑powered inventory forecasting, Honeywell’s rollout of integrated IoT‑enabled POS terminals, and Vend’s acquisition of a European SaaS provider to broaden its omnichannel suite. These moves highlight ongoing consolidation and innovation within the market.