What is the Basic Aromatics Market Overview – Definition, scope, and significance?

The Basic Aromatics Market encompasses the production, distribution, and consumption of aromatic hydrocarbons such as styrene monomer, divinylbenzene, benzene, toluene, xylene, cresol, and pyridine. These compounds serve as foundational building blocks for a wide range of downstream applications, including pharmaceuticals, pesticides, agriculture, food and beverages, cosmetics, paints, coatings, and solvents. Their significance lies in enabling the synthesis of polymers, intermediates, and specialty chemicals that drive growth across multiple industrial sectors worldwide.

What are the Basic Aromatics Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising demand for high‑performance polymers, expanding pharmaceutical pipelines, and growing consumer preference for durable coatings and personal‑care products. Restraints stem from stringent environmental regulations on volatile organic compounds and volatile pricing of crude oil feedstocks. Challenges involve supply chain volatility and the need for greener production technologies. Opportunities arise from investments in bio‑based aromatic routes, emerging markets’ infrastructure development, and increased use of aromatics in renewable energy storage solutions.

What are the Basic Aromatics Market Growth Trends?

Current trends show a shift toward integrated petrochemical complexes that co‑locate aromatic production with downstream processing, improving logistics and cost efficiency. There is also a notable rise in specialty aromatics tailored for high‑value applications such as advanced coatings and medical‑grade solvents. Digitalization of plant operations and adoption of AI‑driven process optimization are emerging, enhancing yield and reducing emissions across the value chain.

How has COVID‑19 impacted the Basic Aromatics Market?

The pandemic temporarily suppressed demand in automotive and construction sectors, leading to a short‑term dip in aromatic consumption. However, accelerated demand for medical‑grade solvents and disinfectants boosted specific segments like benzene and toluene. Recovery has been steady, supported by the resurgence of manufacturing activities and increased investment in health‑care supply chains, positioning the market on a clear upward trajectory.

What does the Basic Aromatics Market Competitive Landscape look like?

The market is characterized by a handful of large integrated players that dominate global capacity. Companies such as BASF SE, Exxon Mobil Corp, Ineos Group Holdings SA, and The Dow Chemical Co hold significant production footprints. Recent consolidation activities include strategic joint ventures and asset swaps aimed at optimizing geographic coverage and technology portfolios, intensifying competition while fostering collaborative innovation.

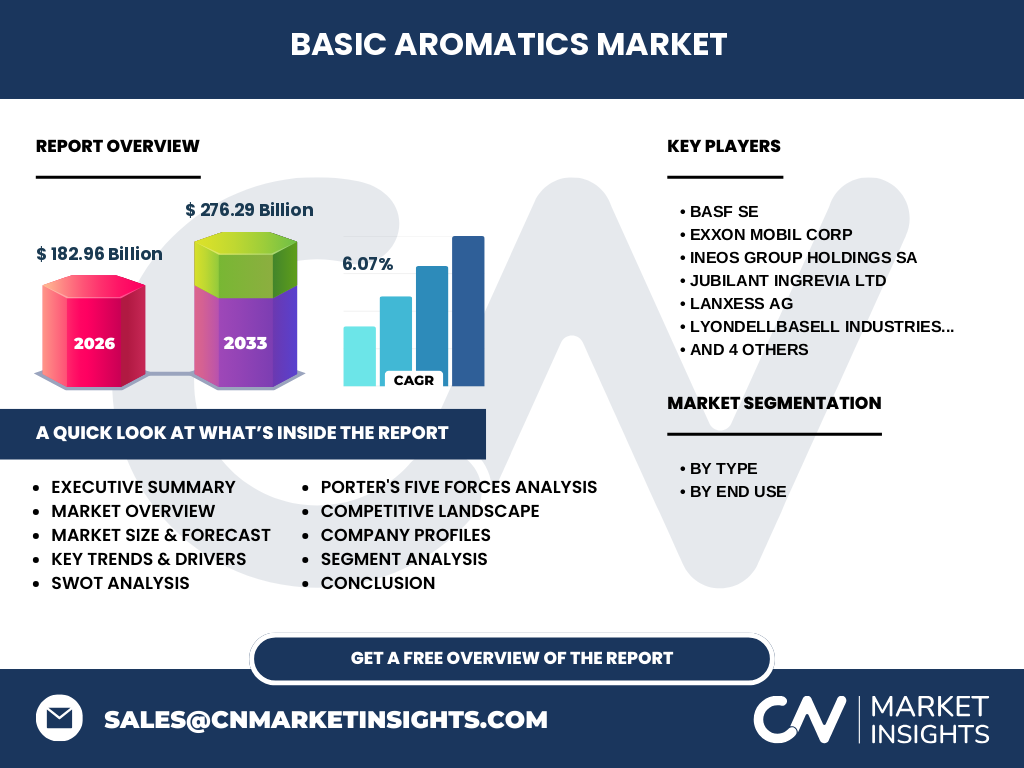

What are the key findings in the Executive Summary of the Basic Aromatics Market?

The Basic Aromatics Market is projected to reach a size of $276.29 billion by 2033, growing at a CAGR of 6.07% from 2027 onward. Strong demand from pharmaceuticals, paints, and solvents drives growth, while regulatory pressures push firms toward greener processes. The competitive arena is consolidated among ten major players, with regional expansion in Asia‑Pacific presenting the highest upside. Investment in bio‑based aromatics and digital plant technologies are highlighted as strategic imperatives.

What are the Basic Aromatics Market Forecasts for 2025‑2032?

Based on the provided CAGR of 6.07%, the market is expected to expand from its 2026 baseline of $182.96 billion to $276.29 billion by 2033. This growth trajectory suggests a steady increase each year between 2025 and 2032, underpinned by expanding end‑use applications and continued capacity additions by leading manufacturers. The forecast underscores a robust outlook, reinforcing confidence for stakeholders seeking long‑term commitments.

How is the Basic Aromatics Market Size and Share segmented by type and end use?

Segmentation by type includes styrene monomer, divinylbenzene, benzene, toluene, xylene, cresol, and pyridine. By end use, the market is divided among pharmaceuticals, pesticides, agriculture, food and beverages, cosmetics and personal care, paints and coatings, and solvents. While precise share percentages are not disclosed, each segment contributes to the overall market value, with polymers‑related aromatics (styrene, xylene) and solvent‑focused aromatics (benzene, toluene) historically representing the largest volume drivers.

What is the Global Basic Aromatics Market Size and Share by Region?

The market exhibits a worldwide footprint, with major consumption hubs in North America, Europe, and the Asia‑Pacific region. Though exact regional monetary shares are not provided, the growth momentum is strongest in Asia‑Pacific due to rapid industrialization and expanding chemical manufacturing capacity, while North America and Europe maintain stable demand driven by mature downstream industries.

What does the Regional Analysis of the Basic Aromatics Market reveal?

In Asia‑Pacific, countries such as China and India lead capacity expansions, leveraging lower production costs and strong domestic demand for construction materials and consumer goods. North America’s market is supported by advanced pharmaceutical and specialty chemical sectors, whereas Europe focuses on high‑value coatings and stringent environmental compliance, prompting investments in cleaner production technologies. Emerging economies in the Middle East and Africa show incremental growth potential as petrochemical complexes mature.

Who are the leading companies in the Basic Aromatics Market and what are their strategies?

The top ten players include BASF SE, Exxon Mobil Corp, Ineos Group Holdings SA, Jubilant Ingrevia Ltd, Lanxess AG, Lyondellbasell Industries NV, Nippon Steel Corp, Sasol Ltd, Shell Plc, and The Dow Chemical Co. Strategies span capacity expansion, diversification into bio‑derived aromatics, strategic acquisitions, and partnerships aimed at enhancing supply chain resilience. Many firms are also investing in digital twins and AI‑based process controls to improve efficiency and meet sustainability goals.

How does Porter’s Five Forces analysis apply to the Basic Aromatics Market?

Threat of new entrants is moderate due to high capital intensity and regulatory barriers. Bargaining power of suppliers is relatively low, as raw material (crude oil) markets are globally integrated. Bargaining power of buyers is moderate; large downstream users can negotiate pricing, yet product differentiation limits leverage. Threat of substitutes remains limited because few alternatives match the performance of traditional aromatics. Industry rivalry is intense, driven by a concentrated set of global players competing on scale, price, and technological innovation.

What are the SWOT insights for the Basic Aromatics Market?

Strengths: Established feedstock base, wide application spectrum, and mature production infrastructure.

Weaknesses: Environmental scrutiny, dependence on fossil‑based raw materials, and cyclical demand patterns.

Opportunities: Bio‑based aromatic development, expansion in high‑growth Asian markets, and adoption of smart manufacturing.

Threats: Stricter emissions regulations, volatility in oil prices, and potential disruptive technologies that could replace certain aromatic derivatives.

What does the Basic Aromatics Market Value Chain look like?

The value chain begins with upstream crude oil extraction and refining, followed by aromatic synthesis (e.g., catalytic reforming, alkylation). Midstream activities involve purification, blending, and logistics. Downstream, aromatics are sold to chemical processors, polymer manufacturers, and specialty formulators. Final users—pharma, coatings, and solvent manufacturers— integrate these intermediates into finished products. Value‑adding services such as custom blending and technical support are increasingly important for differentiation.

What key investment insights can be drawn for the Basic Aromatics Market?

Investors should focus on companies that are scaling capacity in high‑growth regions, particularly Asia‑Pacific, and those demonstrating commitment to sustainable production methods. Assets with integrated downstream capabilities offer higher margins. Funding ventures that develop bio‑based aromatic pathways or employ AI‑driven process optimization can yield long‑term upside as regulatory and cost pressures intensify.

What is the conclusion of the Basic Aromatics Market analysis?

The Basic Aromatics Market is positioned for robust growth through 2033, propelled by diversified end‑use demand and strategic initiatives by leading players. While environmental regulations pose challenges, they also create avenues for innovation and differentiation. Stakeholders who align with sustainability trends, expand in emerging geographies, and adopt advanced digital technologies will likely capture the greatest value.

How was the research methodology designed for this market report?

The study employed a mixed‑method approach, combining primary interviews with industry experts, supplier surveys, and secondary data extraction from company filings, trade publications, and reputable databases. Quantitative forecasts were derived using compound annual growth rate (CAGR) calculations based on the provided 2026 market size of $182.96 billion and the projected 2033 value of $276.29 billion. Qualitative insights were corroborated through cross‑validation with multiple sources.

What is the scope of the research and its limitations?

The research covers global production, consumption, and forecasting of basic aromatics across type and end‑use segments, with a regional breakdown for major markets. Limitations include reliance on publicly available data and the absence of granular market share percentages for individual regions or product lines, as these figures were not supplied. The analysis therefore emphasizes trends, drivers, and strategic insights rather than precise quantitative market share allocations.

Which key companies are highlighted and what recent developments have they announced?

Key players such as BASF SE, Exxon Mobil Corp, Ineos Group Holdings SA, and The Dow Chemical Co are featured. Recent developments include BASF’s launch of a low‑emission styrene plant in Europe, Exxon Mobil’s partnership with a bio‑technology firm to explore renewable benzene routes, Ineos’s acquisition of a mid‑scale xylene facility in Asia, and Dow’s rollout of AI‑enabled process control across its aromatic sites. These actions reflect a collective shift toward capacity expansion, sustainability, and digital transformation.