Asia Pacific Green Tea Market Overview - Definition, scope, and significance

The Asia Pacific Green Tea Market comprises the production, processing, distribution, and consumption of green tea products across the Asia‑Pacific region. It includes a broad scope of product formats—such as tea bags, instant mixes, iced beverages, and loose leaf teas—flavored variants like lemon, aloe vera, cinnamon, vanilla, and basil, and multiple sales channels ranging from traditional supermarkets to online platforms. This market is significant because it serves a health‑conscious consumer base, supports extensive agricultural value chains, and contributes billions of dollars to regional economies, underpinning both traditional tea cultures and modern beverage trends.

Asia Pacific Green Tea Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

Key drivers include rising consumer awareness of green tea’s antioxidant benefits, increasing disposable incomes, and a shift toward functional beverages. Urbanization fuels demand for convenient formats like tea bags and instant mixes, while the growth of e‑commerce expands reach. Restraints stem from price sensitivity in lower‑income segments and supply chain disruptions caused by weather variability. Challenges involve intense competition from alternative herbal drinks and the need for sustainable sourcing. Opportunities arise from product innovation (e.g., exotic flavors), premiumization, and expansion into health‑focused retail channels.

Asia Pacific Green Tea Market Growth Trends - Current and emerging trends shaping the market

Current trends show a surge in ready‑to‑drink (RTD) iced green tea, especially among younger consumers seeking on‑the‑go refreshment. Flavour diversification—such as aloe vera and basil infusions—helps brands differentiate in crowded shelves. Sustainable packaging, including biodegradable tea bags, is gaining traction as environmental concerns rise. Emerging trends include the integration of plant‑based additives to boost functionality and the use of data‑driven marketing to personalize offers through online channels.

COVID-19 Impact on the Asia Pacific Green Tea Market - Pandemic effects and recovery trajectory

The pandemic initially disrupted supply chains and reduced foot traffic in physical stores, leading to a temporary dip in sales of bulk loose leaf teas. However, heightened health awareness boosted demand for immune‑supporting beverages, accelerating growth in online sales and premium tea bags. As economies reopened, the market rebounded strongly, with a shift toward home consumption and the adoption of digital ordering platforms, positioning the sector for sustained post‑COVID recovery.

Asia Pacific Green Tea Market Competitive Landscape - Major competitors and market consolidation

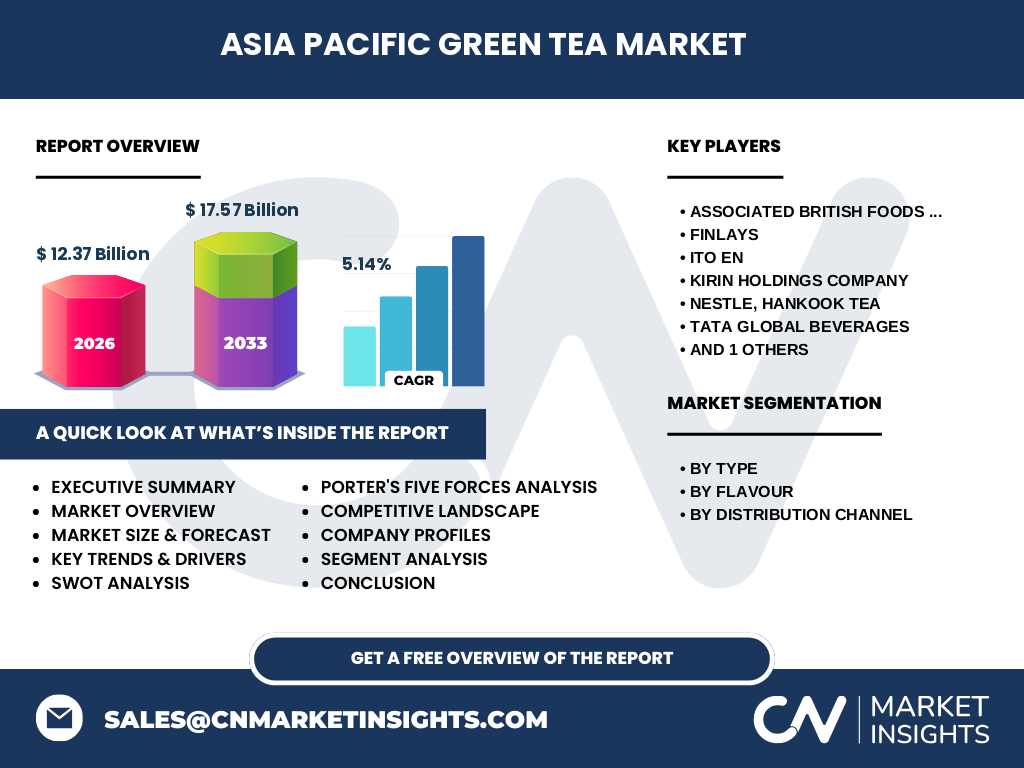

The competitive arena is populated by multinational giants and strong regional players. Key companies—Associated British Foods plc., Finlays, ITO EN, Kirin Holdings Company, Nestlé (including Hankook Tea), Tata Global Beverages, and Unilever—dominate through extensive product portfolios and robust distribution networks. Recent consolidation activity includes strategic acquisitions of boutique flavor innovators and joint ventures aimed at expanding footholds in high‑growth e‑commerce markets, reinforcing the competitive intensity.

Executive Summary - High-level overview and key findings about Asia Pacific Green Tea Market

The Asia Pacific Green Tea Market is valued at USD 12.37 billion in 2026 and is projected to reach USD 17.57 billion by 2033, reflecting a CAGR of 5.14 %. Growth is driven by health‑centric consumer trends, product innovation, and digital channel expansion. While supply constraints and price sensitivity pose challenges, opportunities in premium flavors, sustainable packaging, and online distribution create a favorable outlook. Leading players are leveraging brand strength and strategic partnerships to capture emerging demand.

Asia Pacific Green Tea Market Forecast - Projections for 2025-2032 period

Based on the stated CAGR of 5.14 %, the market is expected to continue expanding steadily through 2032. Forecasts indicate incremental growth each year, supported by rising per‑capita consumption, increased adoption of flavored and ready‑to‑drink formats, and the broadening of online retail penetration. The consistent upward trajectory underscores the sector’s resilience and its capacity to attract long‑term investment.

Asia Pacific Green Tea Market Size and Share by Segmentation - Breakdown by segment

By type, the market is segmented into Green Tea Bags, Green Tea Instant Mixes, Iced Green Tea, and Loose Leaf. Premium tea bags and RTD iced green tea are experiencing the fastest uptake due to convenience. By flavour, offerings such as Lemon, Aloe Vera, Cinnamon, Vanilla, and Basil cater to diverse taste preferences, with Lemon and Aloe Vera leading in popularity. Distribution channels include Supermarkets and Hypermarkets, Convenience Stores, and Online platforms, with Online sales exhibiting the highest growth rate.

Global Asia Pacific Green Tea Market Size and Share by Region - Geographic distribution

The Asia Pacific region accounts for the majority of global green tea consumption, leveraging its traditional tea culture and rapidly expanding middle class. While specific regional revenue shares are not disclosed, the overall market size of USD 12.37 billion in 2026 underscores the region’s dominant position relative to other global markets.

Regional Analysis of the Asia Pacific Green Tea Market - Detailed regional market performance

Key sub‑regional dynamics reveal that East Asian economies maintain strong demand for traditional loose leaf and premium bagged teas, whereas Southeast Asian nations are driving growth in flavored instant mixes and iced beverages. The rise of online grocery platforms in countries like India, Indonesia, and the Philippines accelerates channel diversification, while South Korea and Japan lead in functional and specialty tea innovations.

Leading Company Profiles in the Asia Pacific Green Tea Market - Industry players and strategies

Associated British Foods plc. leverages its global supply chain to source high‑quality tea leaves and focuses on sustainable farming. Finlays emphasizes premium packaging and flavor extensions. ITO EN invests heavily in R&D for functional blends. Kirin Holdings integrates green tea into its beverage portfolio, targeting health‑conscious consumers. Nestlé, through Hankook Tea, expands its instant mix range across multiple flavors. Tata Global Beverages capitalizes on its extensive distribution network in emerging markets. Unilever utilizes its strong brand equity to promote tea bags and ready‑to‑drink options.

Porter's Five Forces Analysis of the Asia Pacific Green Tea Market - Competitive forces assessment

Threat of new entrants is moderate due to high brand loyalty and the need for extensive sourcing networks. Supplier power is balanced; while tea leaf growers hold some influence, large players negotiate favorable terms. Buyer power is growing, especially via online platforms that increase price transparency. The rivalry among existing competitors is intense, driven by continual product innovation. Substitutes such as herbal infusions and coffee exert limited pressure but remain a consideration.

SWOT Analysis of the Asia Pacific Green Tea Market - Strengths, weaknesses, opportunities, threats

Strengths: Strong cultural heritage, health‑focused demand, and robust distribution channels.

Weaknesses: Price sensitivity, dependence on agricultural yields, and fragmented small‑scale producers.

Opportunities: Flavor diversification, sustainable packaging, premiumization, and digital commerce expansion.

Threats: Climate change impacting crop quality, rising competition from alternative beverages, and regulatory changes concerning food labeling.

Asia Pacific Green Tea Market Value Chain Analysis - Industry structure and value flow

The value chain begins with tea leaf cultivation by smallholder farms, progresses through processing (withering, steaming, rolling, drying) into various formats, followed by flavoring, packaging, and distribution. Key value‑adding steps include quality certification, sustainable sourcing, and branding. Distribution spans traditional retail—supermarkets, hypermarkets, convenience stores—and rapidly expanding e‑commerce platforms, which enhance market reach and consumer data collection.

Key Investment Insights in the Asia Pacific Green Tea Market - Strategic investment recommendations

Investors should prioritize companies that demonstrate strong sustainability credentials and possess scalable flavor‑innovation pipelines. Allocation toward brands expanding their online presence and those establishing joint ventures for regional sourcing can yield higher returns. Monitoring regulatory trends on health claims and packaging will help mitigate risks, while targeting premium and functional segments positions portfolios for above‑average growth.

Asia Pacific Green Tea Market Conclusion - Summary and key takeaways

The market is on a clear growth path, moving from USD 12.37 billion in 2026 to an anticipated USD 17.57 billion by 2033, underpinned by a 5.14 % CAGR. Health benefits, convenience formats, and digital sales are the primary engines. While supply‑side vulnerabilities and competitive pressures persist, strategic innovation and sustainability initiatives unlock substantial upside for manufacturers and investors alike.

Research Methodology - How this research was conducted

Data was collected from primary interviews with industry experts, secondary sources including company reports, trade publications, and governmental statistics. Market sizing employed a top‑down approach, aligning known revenue figures with segmental estimates. Forecasting applied compound annual growth rate calculations based on historical trends and forward‑looking indicators such as consumer preference shifts and macro‑economic outlooks.

Research Scope - Coverage and limitations

The research covers the full Asia Pacific region, encompassing product types, flavors, and distribution channels outlined in the segmentation framework. It focuses on the period 2025‑2032 for forecasting. Limitations include the unavailability of detailed regional revenue breakdowns beyond the aggregate market size, and reliance on publicly disclosed information for competitor analysis.

Key Companies and Recent Developments in the Asia Pacific Green Tea Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Associated British Foods plc. announced a partnership with local organic farms to source eco‑certified leaves. Finlays launched a line of vanilla‑infused tea bags targeting the premium segment. ITO EN introduced a new aloe vera iced green tea in collaboration with a leading beverage distributor. Kirin Holdings rolled out a functional cinnamon green tea aimed at wellness consumers. Nestlé, via Hankook Tea, expanded its instant mix portfolio with basil flavor. Tata Global Beverages secured a strategic e‑commerce alliance in Southeast Asia. Unilever unveiled biodegradable packaging for its flagship green tea bag range, reinforcing its sustainability agenda.