1. What is the Europe Green Tea Market Overview – definition, scope, and significance?

The Europe Green Tea Market comprises the production, distribution, and consumption of green tea products across European countries. It includes various formats such as tea bags, instant mixes, iced beverages, and loose leaf, as well as a range of flavours like lemon, aloe vera, and vanilla. The market is significant because it reflects growing consumer interest in health‑focused beverages, contributes billions of euros to the food‑and‑beverage sector, and drives innovation in packaging and distribution channels.

2. What are the key drivers, restraints, challenges, and opportunities shaping the Europe Green Tea Market?

Key drivers include rising health consciousness, demand for natural antioxidants, and expanding ready‑to‑drink (RTD) formats. Restraints stem from price sensitivity and competition from coffee and soft drinks. Challenges involve supply chain volatility for high‑quality tea leaves and stringent EU food‑safety regulations. Opportunities arise from product‑line extensions (e.g., functional blends), premiumisation, and growth of e‑commerce channels that reach younger, tech‑savvy consumers.

3. What growth trends are currently influencing the Europe Green Tea Market?

Current trends feature a surge in premium loose‑leaf offerings, increased adoption of flavoured iced green tea, and a shift toward sustainable packaging such as biodegradable tea bags. The market also sees a rise in “clean‑label” instant mixes that contain no artificial additives, and a growing preference for organic certifications driven by environmentally aware shoppers.

4. How has COVID‑19 impacted the Europe Green Tea Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and reduced foot‑traffic in supermarkets, prompting a temporary dip in sales. However, heightened focus on immunity boosted demand for health‑oriented drinks, accelerating online purchases. Recovery is strong, with a shift toward home‑brew formats and a sustained increase in digital sales, positioning the market on a steady upward path.

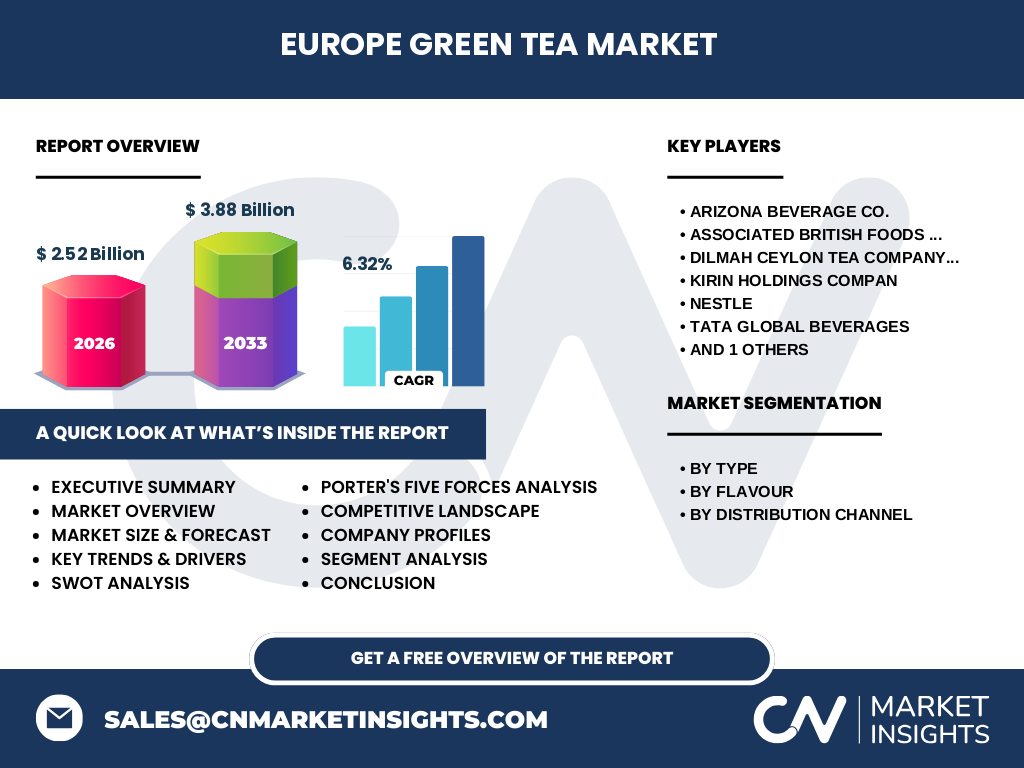

5. Who are the major competitors in the Europe Green Tea Market and how is consolidation occurring?

Leading players include AriZona Beverage Co., Associated British Foods plc, Dilmah Ceylon Tea Company PLC, Kirin Holdings Company, Nestlé, Tata Global Beverages, and Unilever. These firms are pursuing consolidation through strategic acquisitions, joint ventures, and portfolio diversification to capture emerging sub‑segments such as premium flavoured iced teas and organic instant mixes.

6. What are the key findings in the Executive Summary of the Europe Green Tea Market?

The market is valued at €2.52 billion in 2026 and is projected to reach €3.88 billion by 2033, reflecting a CAGR of 6.32 %. Growth is driven by health trends, premiumisation, and expanding e‑commerce. Competitive dynamics are shaped by multinational beverage giants expanding their green‑tea portfolios, while new entrants focus on niche, organic, and functional products.

7. What are the forecast expectations for the Europe Green Tea Market from 2025 to 2032?

According to the forecast, the market will expand from its 2026 base of €2.52 billion to €3.88 billion by 2033, maintaining an average annual growth rate of 6.32 %. This trajectory is underpinned by continued consumer preference for wellness beverages, increased distribution through online channels, and product innovation across flavour and format categories.

8. How is the Europe Green Tea Market sized and shared by segmentation?

By type, the market is divided into Green Tea Bags, Green Tea Instant Mixes, Iced Green Tea, and Loose Leaf. Flavour segmentation includes Lemon, Aloe Vera, Cinnamon, Vanilla, and Basil. Distribution channels comprise Supermarkets & Hypermarkets, Convenience Stores, and Online platforms. Each segment contributes to the overall market value, with premium loose leaf and iced formats showing the fastest growth.

9. What is the geographic distribution of the Europe Green Tea Market globally?

Europe represents a core region within the global green‑tea landscape, accounting for a substantial portion of the worldwide market. While specific regional percentages are not disclosed, the continent’s strong retail infrastructure and high consumer health awareness position it as a key driver of global demand.

10. How does the Europe Green Tea Market perform across different European regions?

Western European nations such as Germany, the United Kingdom, and France lead in volume due to mature retail networks and high purchasing power. Northern Europe shows strong growth in iced and flavoured variants, while Southern Europe favours traditional loose‑leaf and bagged formats. Emerging markets in Eastern Europe are expanding through online channels and convenience‑store penetration.

11. What are the profiles of leading companies in the Europe Green Tea Market?

AriZona Beverage Co. focuses on ready‑to‑drink iced teas with bold flavours. Associated British Foods plc leverages its extensive distribution to supply tea bags and premium loose leaf. Dilmah Ceylon emphasizes organic and single‑origin offerings. Kirin Holdings expands its Asian‑style iced teas. Nestlé integrates green tea into its health‑drink portfolio. Tata Global Beverages drives growth through sustainable sourcing, while Unilever combines brand heritage with modern packaging.

12. How does Porter’s Five Forces assess the Europe Green Tea Market?

• Bargaining power of buyers: High, due to abundant alternatives and price sensitivity. • Bargaining power of suppliers: Moderate, as high‑quality leaf suppliers are limited but can command premium prices. • Threat of new entrants: Medium, barriers exist in brand building and distribution but niche organic players can enter. • Threat of substitutes: High, from coffee, soft drinks, and herbal infusions. • Competitive rivalry: Intense, with multinational firms competing on innovation, branding, and channel reach.

13. What is the SWOT analysis of the Europe Green Tea Market?

Strengths: Strong health perception, diverse product formats, and robust retail networks. Weaknesses: Price premium for quality tea, fragmented supply chain. Opportunities: Expansion of functional blends, sustainability‑focused packaging, and growth of online sales. Threats: Volatile raw‑material costs, regulatory changes, and competition from other functional beverages.

14. How is the value chain of the Europe Green Tea Market structured?

The value chain begins with tea‑leaf cultivation (primarily in Asia), followed by processing (drying, cutting, blending), packaging (bags, sachets, bottles), distribution (wholesale to supermarkets, convenience stores, and online retailers), and finally consumption. Value‑addition occurs at each stage through certifications (organic, fair‑trade), flavour innovation, and eco‑friendly packaging.

15. What are the key investment insights for the Europe Green Tea Market?

Investors should target premium and functional segments, capitalize on the shift to online distribution, and seek partnerships with sustainable growers. Funding innovation in flavoured iced teas and biodegradable packaging can yield high returns. Acquisitions of niche organic brands provide entry points into growing consumer niches.

16. What conclusions can be drawn about the Europe Green Tea Market?

The market is on a solid growth path, driven by health trends, product diversification, and digital sales. While price competition and supply constraints pose challenges, strategic focus on premiumisation, sustainability, and e‑commerce will sustain the projected CAGR of 6.32 % through 2033.

17. What research methodology was employed for this market study?

The study combines primary interviews with industry executives, secondary data from company reports, trade publications, and EU statistical sources. Market sizing uses a top‑down approach anchored by the €2.52 billion 2026 figure, while forecasting applies CAGR extrapolation and scenario analysis to estimate the 2033 value.

18. What is the scope of the research and its limitations?

The scope covers product types, flavours, and distribution channels across all European countries, focusing on the period 2025‑2033. Limitations include the unavailability of granular country‑level revenue splits and reliance on publicly disclosed data for competitive insights.

19. Which key companies have recent developments in the Europe Green Tea Market?

Recent announcements include AriZona’s launch of a low‑sugar iced green tea line, Associated British Foods’ acquisition of a boutique organic tea brand, Dilmah’s introduction of a sustainable single‑origin loose leaf range, Kirin’s partnership with a European beverage distributor, Nestlé’s rollout of a fortified green‑tea snack, Tata Global Beverages’ investment in a fair‑trade tea plantation, and Unilever’s roll‑out of biodegradable tea‑bag packaging across its European portfolio.