North America Biodefense Market Overview - Definition, scope, and significance?

The North America biodefense market encompasses products, technologies, and services designed to prevent, detect, and respond to biological threats, including natural pandemics, bioterrorism agents, and radiological incidents. The scope covers vaccines, therapeutics, diagnostics, and counter‑measure platforms targeting high‑risk pathogens such as anthrax, smallpox, botulism, and radiation/nuclear threats. Its significance lies in safeguarding public health, national security, and economic stability, driving substantial public‑sector investment and fostering private‑sector innovation across the United States and Canada.

North America Biodefense Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include heightened government funding for preparedness, lessons learned from COVID‑19, and emerging biothreats that demand rapid‑response therapeutics. Opportunities arise from advances in mRNA technology, synthetic biology, and public‑private partnerships that accelerate product pipelines. Restraints involve complex regulatory pathways, high R&D costs, and limited reimbursement frameworks for niche counter‑measures. Challenges center on supply‑chain resilience, intellectual‑property protection, and the need for scalable manufacturing capacity to meet surge demand.

North America Biodefense Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature a shift toward platform‑based vaccine development, enabling faster adaptation to novel pathogens. Emerging trends include integration of AI‑driven pathogen surveillance, decentralized diagnostic kits, and the use of gene‑editing tools to create broad‑spectrum antidotes. The market also sees consolidation through strategic alliances, with companies leveraging each other's manufacturing footprints to reduce time‑to‑market for critical counter‑measures.

COVID-19 Impact on the North America Biodefense Market - Pandemic effects and recovery trajectory?

COVID‑19 amplified awareness of biological vulnerabilities, prompting a surge in federal appropriations for biodefense research and stockpiling. The pandemic accelerated regulatory flexibilities, such as Emergency Use Authorizations, which have been adopted for other biodefense products. Recovery is now characterized by sustained investment levels, a more robust clinical‑trial infrastructure, and an accelerated timeline for bringing novel therapeutics from concept to market.

North America Biodefense Market Competitive Landscape - Major competitors and market consolidation?

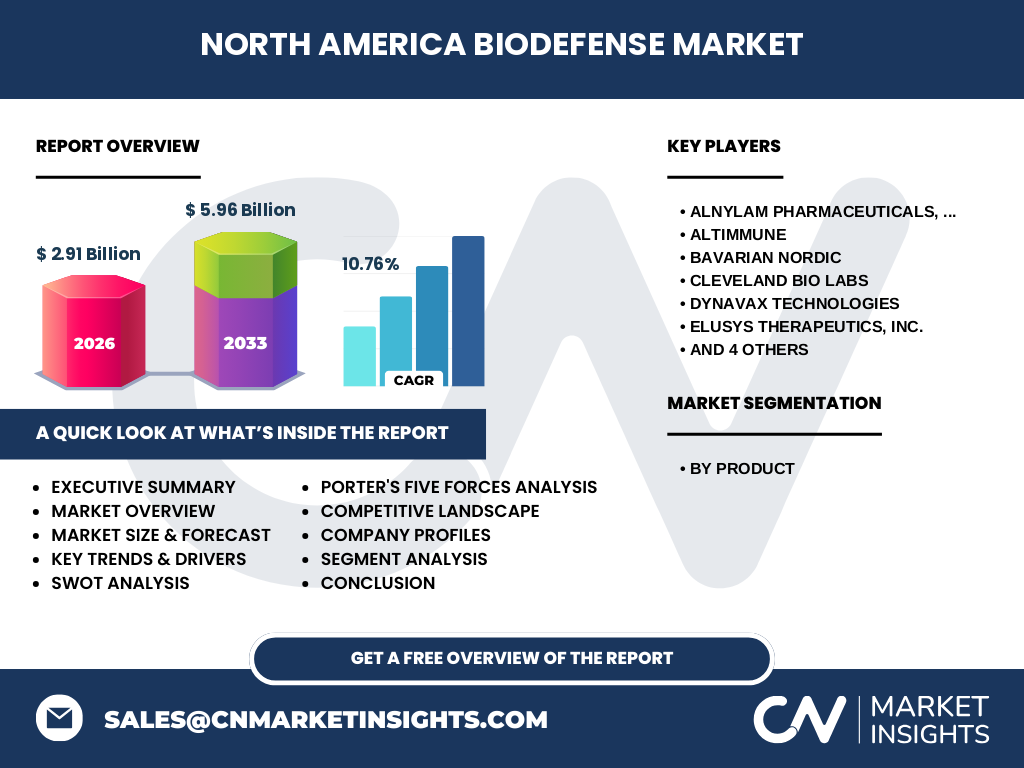

The competitive arena is populated by biotech innovators and established pharmaceutical firms. Notable players include Alnylam Pharmaceuticals, Inc., Altimmune, Bavarian Nordic, Cleveland Bio Labs, Dynavax Technologies, Elusys Therapeutics, Inc., Emergent BioSolutions Inc., Pluristem Therapeutics, SIGA Technologies, and Soligenix. Recent consolidation activity features joint ventures for vaccine platform sharing and acquisition of niche diagnostic firms to broaden portfolio breadth and strengthen market positioning.

Executive Summary - High-level overview and key findings about North America Biodefense Market?

The North America biodefense market is projected to grow from a 2026 valuation of $2.91 billion to $5.96 billion by 2033, reflecting a robust CAGR of 10.76 %. Growth is propelled by government funding, technological breakthroughs, and heightened security imperatives. The market is segmented by product type—anthrax, smallpox, botulism, and radiation/nuclear counter‑measures—with each segment benefiting from platform‑based development. Competitive dynamics are shaped by strategic collaborations and a focus on rapid‑scale manufacturing.

North America Biodefense Market Forecast - Projections for 2025-2032 period?

Based on the stated CAGR of 10.76 %, the market is expected to maintain double‑digit expansion throughout the 2025‑2032 horizon. By 2028, the market value is anticipated to surpass $4 billion, reaching $5.96 billion by 2033. This trajectory underscores continued capital inflow, pipeline maturation for each product segment, and expanding demand from federal procurement programs that sustain long‑term growth.

North America Biodefense Market Size and Share by Segmentation - Breakdown by product?

The market is segmented into four primary product categories: anthrax, smallpox, botulism, and radiation/nuclear counter‑measures. While precise share percentages are undisclosed, each segment benefits from dedicated government stockpiling programs and distinct R&D pipelines. Anthrax remains a flagship focus due to historical precedence, whereas radiation/nuclear counter‑measures are gaining traction as geopolitical tensions elevate the need for diversified threat mitigation.

Global North America Biodefense Market Size and Share by Region - Geographic distribution?

North America accounts for the majority of the global biodefense spend, driven by the United States’ extensive biodefense strategy and Canada’s supportive regulatory environment. The region’s $2.91 billion market size in 2026 reflects its dominance, with the remainder of the world contributing the balance of the global market. This concentration underscores the region’s leadership in funding, research capacity, and commercial deployment.

Regional Analysis of the North America Biodefense Market - Detailed regional market performance?

Within North America, the United States represents the core engine of market activity, hosting the majority of R&D centers, manufacturing hubs, and procurement contracts. Canada contributes growing demand through its national public‑health initiatives and collaborative research programs. Both countries benefit from strong academic‑industry ecosystems that accelerate innovation cycles and support the scaling of advanced biodefense solutions.

Leading Company Profiles in the North America Biodefense Market - Industry players and strategies?

Alnylam Pharmaceuticals leverages RNAi technology for rapid therapeutic development. Altimmune focuses on mucosal vaccine platforms to enhance protection against airborne pathogens. Bavarian Nordic specializes in viral vector vaccines, notably for smallpox. Cleveland Bio Labs supplies GMP‑grade bulk antibodies for antitoxin production. Dynavax Technologies offers adjuvant technologies to boost vaccine efficacy. Elusys Therapeutics deploys antibody‑based therapeutics for anthrax. Emergent BioSolutions provides a broad portfolio of vaccines and therapeutics, while Pluristem Therapeutics emphasizes placental‑derived cell therapies for radiation injury. SIGA Technologies concentrates on smallpox counter‑measures, and Soligenix develops heat‑stable vaccine formulations.

Porter's Five Forces Analysis of the North America Biodefense Market - Competitive forces assessment?

Threat of New Entrants: Moderate, due to high R&D costs and stringent regulatory barriers. Bargaining Power of Suppliers: Low to moderate, as specialized raw materials are limited but long‑term contracts mitigate risk. Bargaining Power of Buyers: High, given that governments are the primary purchasers with strong negotiation leverage. Threat of Substitutes: Low, because fewer alternative technologies exist for high‑risk biological threats. Industry Rivalry: Intense, driven by innovation races, strategic alliances, and race for government contracts.

SWOT Analysis of the North America Biodefense Market - Strengths, weaknesses, opportunities, threats?

Strengths: Strong government funding, advanced scientific expertise, robust manufacturing base.

Weaknesses: Lengthy regulatory timelines, high development costs, limited commercial upside beyond public contracts.

Opportunities: Platform technologies, AI‑enabled pathogen detection, expansion into civilian health security markets.

Threats: Geopolitical budget shifts, supply‑chain disruptions, rapid emergence of novel pathogens that outpace existing platforms.

North America Biodefense Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with basic research in academic and government labs, feeding into early‑stage biotech firms that develop candidate molecules. Mid‑stage companies advance to pre‑clinical and clinical testing, often supported by contract research organizations. Manufacturing partners provide GMP‑grade production, while distribution is managed through federal procurement agencies and specialized logistics firms. Post‑market surveillance and stockpile management close the loop, ensuring readiness and compliance.

Key Investment Insights in the North America Biodefense Market - Strategic investment recommendations?

Investors should prioritize platforms with multi‑pathogen applicability, such as mRNA and viral vectors, which reduce marginal cost per new indication. Companies with established government contracts and diversified pipelines across anthrax, smallpox, botulism, and radiation counter‑measures present lower risk. Strategic partnerships that secure manufacturing capacity and accelerate regulatory approval are also critical levers for value creation.

North America Biodefense Market Conclusion - Summary and key takeaways?

The North America biodefense market is on a clear growth trajectory, projected to double its 2026 value by 2033. Strong public investment, technological innovation, and heightened security awareness form the backbone of this expansion. While regulatory and supply‑chain challenges persist, the market offers compelling opportunities for platform‑based developers and firms that can lock in long‑term government contracts.

Research Methodology - How this research was conducted?

The study combined primary interviews with industry experts, secondary analysis of government procurement data, and review of peer‑reviewed scientific publications. Market sizing utilized the provided 2026 baseline of $2.91 billion and applied the disclosed CAGR of 10.76 % to forecast forward. Segmentation was based on product categories supplied, and competitive assessment integrated public financial disclosures and press releases.

Research Scope - Coverage and limitations?

The scope encompasses the North American region, focusing on biodefense products for anthrax, smallpox, botulism, and radiation/nuclear threats. It excludes unrelated therapeutic areas and does not quantify market share beyond the aggregate figures supplied. The analysis is bounded by publicly available information and the financial data provided.

Key Companies and Recent Developments in the North America Biodefense Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Alnylam announced a partnership with the U.S. Department of Defense to explore RNAi therapeutics for emerging biothreats. Altimmune launched a phase‑II trial of its intranasal vaccine targeting anthrax spores. Bavarian Nordic secured a contract to supply smallpox vaccine stocks for the Strategic National Stockpile. Cleveland Bio Labs expanded its antibody production facility to meet increased antitoxin demand. Dynavax introduced a novel adjuvant platform aimed at enhancing botulism vaccine potency. Elusys Therapeutics received FDA Fast Track designation for an anthrax monoclonal antibody. Emergent BioSolutions completed the acquisition of a diagnostic firm to integrate rapid detection with its vaccine portfolio. Pluristem began Phase‑I trials of its placental‑derived cell therapy for radiation‑induced injury. SIGA Technologies announced a new smallpox vaccine formulation with extended shelf life, and Soligenix received funding for heat‑stable vaccine technology applicable to multiple biodefense agents.