North America Date Sugar Market Overview - Definition, scope, and significance?

Date sugar is a natural sweetener derived from dried dates that have been ground into granules, powder, or syrup. In North America, the market encompasses production, processing, distribution, and retail of date sugar across multiple forms (granules and crystal, powdered, syrup/liquid), origins (organic and conventional), end‑use categories (bakery, confectionery, snacks, dressings and condiments, sauces and spreads), and sales channels (hypermarkets/supermarkets, discount stores, specialty grocery stores, traditional grocery stores, online retail). The significance of this market lies in the growing consumer preference for clean‑label, low‑glycemic, and plant‑based sweeteners that deliver functional benefits such as fiber, minerals, and antioxidants. Date sugar’s natural caramel flavor makes it an attractive alternative to refined sugars in a broad range of food and beverage applications, driving its relevance in the health‑conscious North American market.

North America Date Sugar Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising demand for natural sweeteners, increasing awareness of the health drawbacks of high‑fructose corn syrup, and a strong trend toward organic and non‑GMO products. The expanding clean‑label movement fuels demand in bakery and snack segments, while the growth of online retail provides new distribution pathways. Restraints stem from the relatively higher price of date sugar compared with conventional sugar, limited large‑scale processing capacity, and occasional supply constraints due to the seasonal nature of date harvests. Challenges involve educating consumers about functional differences and overcoming the perception that natural sugars are automatically “low‑calorie.” Opportunities arise from product innovation—such as fortified date‑based syrups—and from potential expansion into plant‑based dairy alternatives, where the natural flavor profile of date sugar can replace dairy‑derived sweeteners.

North America Date Sugar Market Growth Trends - Current and emerging trends shaping the market?

The market is witnessing a shift from bulk granules toward premium powdered and liquid forms that integrate easily into modern manufacturing lines. Organic date sugar is gaining traction, especially in specialty grocery stores and e‑commerce platforms. Companies are launching blended sweetener blends that combine date sugar with stevia or monk fruit to balance sweetness and reduce caloric impact. Another emerging trend is the use of date sugar in functional snacks and protein bars, catering to the “better‑for‑you” segment. Lastly, sustainability narratives around the low‑water footprint of date cultivation are being leveraged in brand storytelling.

COVID-19 Impact on the North America Date Sugar Market - Pandemic effects and recovery trajectory?

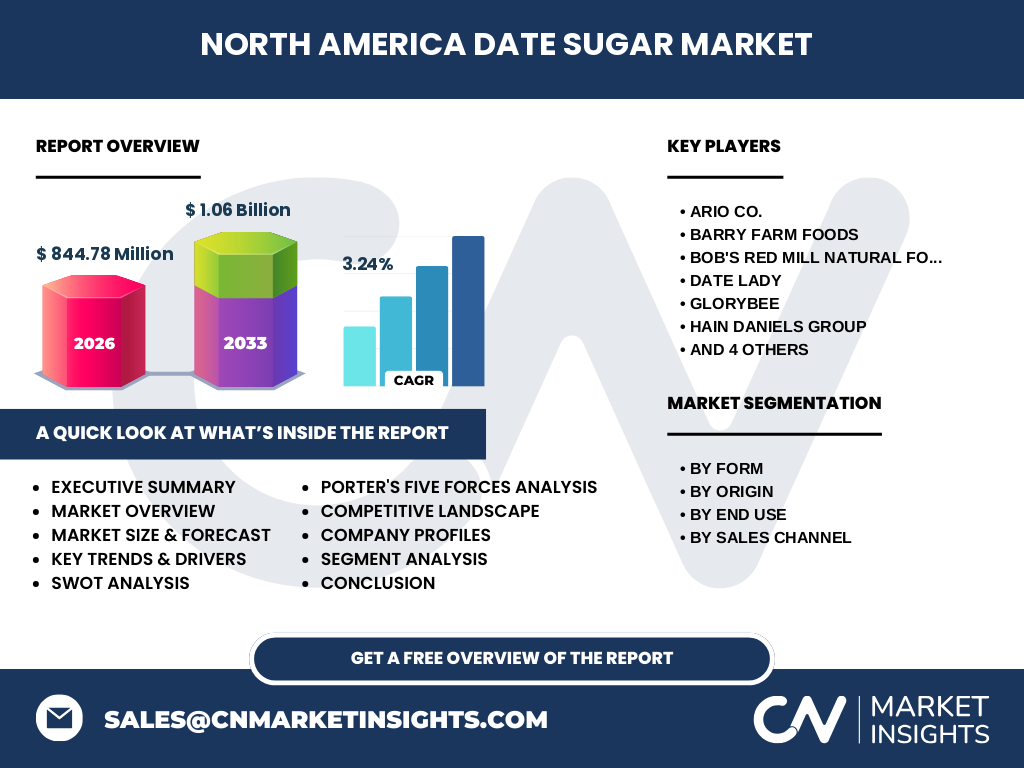

During the peak of the pandemic, supply chain disruptions affected raw date imports, leading to short‑term inventory shortages. However, the surge in home baking and increased health consciousness boosted demand for natural sweeteners, partially offsetting supply gaps. Post‑2021, the market demonstrated resilience, with a rapid restabilization of logistics and a renewed focus on online retail channels, which now account for a growing share of sales. The recovery trajectory is positive, reflected in the projected CAGR of 3.24% through 2032.

North America Date Sugar Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena features a mix of established specialty food manufacturers and emerging niche brands. Key players include Ario Co., Barry Farm Foods, Bob’s Red Mill Natural Foods, Date Lady, GloryBee, Hain Daniels Group, MGT Dried Fruit, NOW Foods, Naturalia Ingredients srl, and PANOS brands. While no major mergers have been announced, the market sees strategic partnerships aimed at expanding distribution networks, especially in the organic segment. Competitive differentiation is driven largely by product form (e.g., powdered vs. syrup), organic certification, and brand positioning around health benefits.

Executive Summary - High-level overview and key findings about North America Date Sugar Market?

The North America date sugar market was valued at USD 844.78 million in 2026 and is forecast to reach USD 1.06 billion by 2033, delivering a CAGR of 3.24%. Growth is propelled by health‑driven consumer preferences, organic product demand, and expanding applications across bakery, confectionery, and snack categories. While price sensitivity and supply variability pose challenges, opportunities in product innovation and e‑commerce channel expansion present viable pathways for market participants. Leading firms are focusing on organic certifications and diversified product formats to capture niche segments.

North America Date Sugar Market Forecast - Projections for 2025-2032 period?

Based on current trends and the stated CAGR of 3.24%, the market is expected to expand steadily from its 2026 base of USD 844.78 million to approximately USD 1.06 billion by 2033. This trajectory implies incremental annual growth, with stronger gains anticipated in the organic powdered segment and in online retail channels, where consumer adoption of natural sweeteners is accelerating.

North America Date Sugar Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by form includes granules and crystal, powdered, and syrup/liquid. By origin, the market is divided into organic and conventional varieties. End‑use segmentation covers bakery, confectionery, snacks, dressings and condiments, and sauces and spreads. Sales channel segmentation comprises hypermarkets/supermarkets, discount stores, specialty grocery stores, traditional grocery stores, and online retail. While precise share percentages are not disclosed, the granules and crystal form currently commands the largest volume due to its versatility, whereas powdered and syrup formats are experiencing faster growth rates driven by convenience and functional food applications. Organic products, though a smaller slice, are expanding at a higher compound rate than conventional counterparts.

Global North America Date Sugar Market Size and Share by Region - Geographic distribution?

Within the North American region, the United States represents the dominant market, followed by Canada. The United States accounts for the majority of demand owing to its larger population, extensive retail infrastructure, and higher prevalence of health‑focused consumer segments. Canada contributes a modest but growing share, especially in the organic and specialty grocery channels.

Regional Analysis of the North America Date Sugar Market - Detailed regional market performance?

In the United States, growth is strongest in the West Coast and Northeast, where organic product penetration and discretionary spending are high. The Midwest shows steady demand mainly through traditional grocery and discount store channels. In Canada, the Ontario and British Columbia provinces lead adoption, driven by a consumer base that values natural ingredients and sustainability. Across both countries, online retail is witnessing the fastest year‑over‑year growth, reflecting shifting buying habits post‑COVID‑19.

Leading Company Profiles in the North America Date Sugar Market - Industry players and strategies?

Ario Co. focuses on premium organic granules and has invested in sustainable sourcing partnerships. Barry Farm Foods differentiates with a broad portfolio across all three forms, emphasizing low‑glycemic benefits. Bob’s Red Mill Natural Foods leverages its established natural foods brand to distribute powdered date sugar through mass‑market channels. Date Lady concentrates on syrup and liquid formats tailored for beverage applications. GloryBee and NOW Foods target health‑store segments with certified organic and non‑GMO products. Hain Daniels Group, MGT Dried Fruit, Naturalia Ingredients srl, and PANOS brands each pursue niche market penetration through specialty grocery and e‑commerce platforms.

Porter's Five Forces Analysis of the North America Date Sugar Market - Competitive forces assessment?

Threat of new entrants is moderate; entry barriers include raw material sourcing and certification costs, yet the growing demand for natural sweeteners attracts startups. Bargaining power of suppliers is relatively high because date fruit is region‑specific and seasonally harvested, limiting supply elasticity. Buyers possess moderate power due to price sensitivity, especially in discount store channels. The threat of substitutes—such as stevia, monk fruit, and traditional sugar—remains significant, compelling firms to emphasize unique functional benefits. Competitive rivalry is intense, with multiple brands competing on organic status, product form, and distribution reach.

SWOT Analysis of the North America Date Sugar Market - Strengths, weaknesses, opportunities, threats?

Strengths: Natural, nutrient‑rich profile; alignment with clean‑label trends; versatile applications across food categories.

Weaknesses: Higher price point than refined sugar; seasonal supply constraints; limited consumer awareness.

Opportunities: Expansion into plant‑based dairy alternatives; development of fortified syrups; growth of online retail and subscription models.

Threats: Competition from low‑cost artificial and non‑nutritive sweeteners; potential volatility in date crop yields; regulatory scrutiny on labeling claims.

North America Date Sugar Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with date cultivation in primary producing regions, followed by harvesting, drying, and transportation to processing facilities in North America. Processing includes cleaning, grinding, and formulation into granules, powder, or syrup, often with additional organic certification steps. Distribution channels then move the finished product to wholesale distributors, retail outlets (hypermarkets, discount stores, specialty grocers), and directly to consumers via online platforms. End‑users—food manufacturers and home bakers—incorporate date sugar into final products, completing the chain.

Key Investment Insights in the North America Date Sugar Market - Strategic investment recommendations?

Investors should consider companies with robust organic certification pipelines and diversified product formats, as these are positioned to capture higher growth segments. Funding for capacity expansion in powder and liquid processing can mitigate supply risks and meet rising demand. Strategic partnerships with e‑commerce platforms and specialty food brands can accelerate market penetration. Additionally, targeting the functional snack and plant‑based beverage categories offers upside potential.

North America Date Sugar Market Conclusion - Summary and key takeaways?

The North America date sugar market is on a steady growth path, underpinned by health‑driven consumer behavior and a shift toward natural, sustainable sweeteners. Despite price and supply challenges, the market’s projected CAGR of 3.24% through 2032 indicates solid expansion opportunities, especially in organic, powdered, and online retail segments. Companies that invest in product innovation, secure reliable sourcing, and strengthen omni‑channel distribution are likely to emerge as market leaders.

Research Methodology - How this research was conducted?

The study combined primary interviews with industry experts, secondary data collection from company reports, trade publications, and government statistics, and quantitative modeling to project market size and growth. Trend analysis, competitive benchmarking, and scenario planning were applied to develop forecasts and strategic insights.

Research Scope - Coverage and limitations?

The scope encompasses the North American date sugar market by form, origin, end‑use, and sales channel, covering the period from 2025 to 2032. While the report uses the most recent available data, it does not include proprietary financial disclosures beyond the provided market size and forecast figures.

Key Companies and Recent Developments in the North America Date Sugar Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Ario Co. recently launched an organic granulated line certified by the USDA Organic program. Barry Farm Foods announced a partnership with a major online retailer to create a subscription service for powdered date sugar. Bob’s Red Mill introduced a blended sweetener combining date sugar with monk fruit, aimed at lower‑calorie bakery applications. Date Lady expanded its syrup portfolio with a fortified version enriched with calcium and vitamin D for use in plant‑based milks. GloryBee secured a distribution agreement with a national health‑food chain, increasing shelf presence in specialty grocery stores. NOW Foods rolled out a new “Clean Sweet” range featuring conventional and organic powdered date sugar, emphasizing non‑GMO status. Hain Daniels Group invested in a new processing facility to boost powder capacity, while MGT Dried Fruit announced a limited‑edition organic date sugar gift set targeting holiday shoppers. Naturalia Ingredients srl entered the Canadian market through a joint venture with a local ingredient distributor. PANOS brands launched a digital marketing campaign to raise awareness of the antioxidant benefits of date sugar among millennials.