What is the Gas Turbine Market Overview – Definition, scope, and significance?

The gas turbine market encompasses the design, manufacturing, distribution, and servicing of gas‑driven turbine engines used across power generation, oil and gas, and various industrial applications. These turbines convert the energy of high‑temperature combustion gases into mechanical power, which can directly drive generators (open‑cycle) or feed a combined‑cycle system for higher efficiency. The scope of the market includes a broad range of capacity classes—from small units below 40 MW suitable for distributed generation to large installations above 300 MW that form the backbone of utility‑scale power plants. Significance stems from the technology’s ability to provide rapid start‑up, high power density, and relatively low emissions compared with conventional coal‑fired plants, making it a cornerstone of the global transition toward cleaner and more flexible energy systems.

What are the Gas Turbine Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising demand for reliable baseload and peaking power, especially as renewable sources introduce variability; the need for efficient cogeneration in oil‑and‑gas operations; and stringent emission regulations that favor low‑carbon turbine solutions. Restraints arise from high upfront capital costs and the competitive pressure from alternative technologies such as battery storage and advanced nuclear. Challenges involve maintaining supply chain resilience for critical components like high‑temperature alloys and managing the skills gap for turbine maintenance. Opportunities are found in the growing adoption of combined‑cycle configurations, digital monitoring and predictive maintenance platforms, and the expansion of gas‑turbine use in emerging markets seeking to replace aging diesel generators.

What are the current Gas Turbine Market Growth Trends?

Recent trends highlight a shift toward higher efficiency combined‑cycle plants, driven by utility‑scale projects that aim to exceed 60 % thermal efficiency. Modular and fast‑install turbine packages are gaining traction for rapid deployment in remote or disaster‑recovery scenarios. Additionally, there is an increasing integration of turbines with renewable assets to provide grid‑balancing services, while hybrid configurations that pair turbines with battery storage are emerging in the power‑generation segment. Digitalization, including IoT‑enabled condition monitoring, is becoming a standard offering, enhancing turbine availability and lifecycle cost management.

How did COVID‑19 impact the Gas Turbine Market and what is the recovery trajectory?

The pandemic caused temporary project delays, supply‑chain disruptions, and a short‑term dip in capital spending, particularly in the industrial and oil‑and‑gas segments. However, the market showed resilience as governments and utilities accelerated clean‑energy initiatives to stimulate economies, leading to a swift resumption of turbine orders in 2021. Recovery is now robust, supported by renewed investment in grid reliability and a surge in demand for flexible generation to complement the growing share of intermittent renewables. The trajectory points toward sustained growth, aligning with the overall market CAGR of 5.35 %.

Who are the major competitors and what is the current competitive landscape?

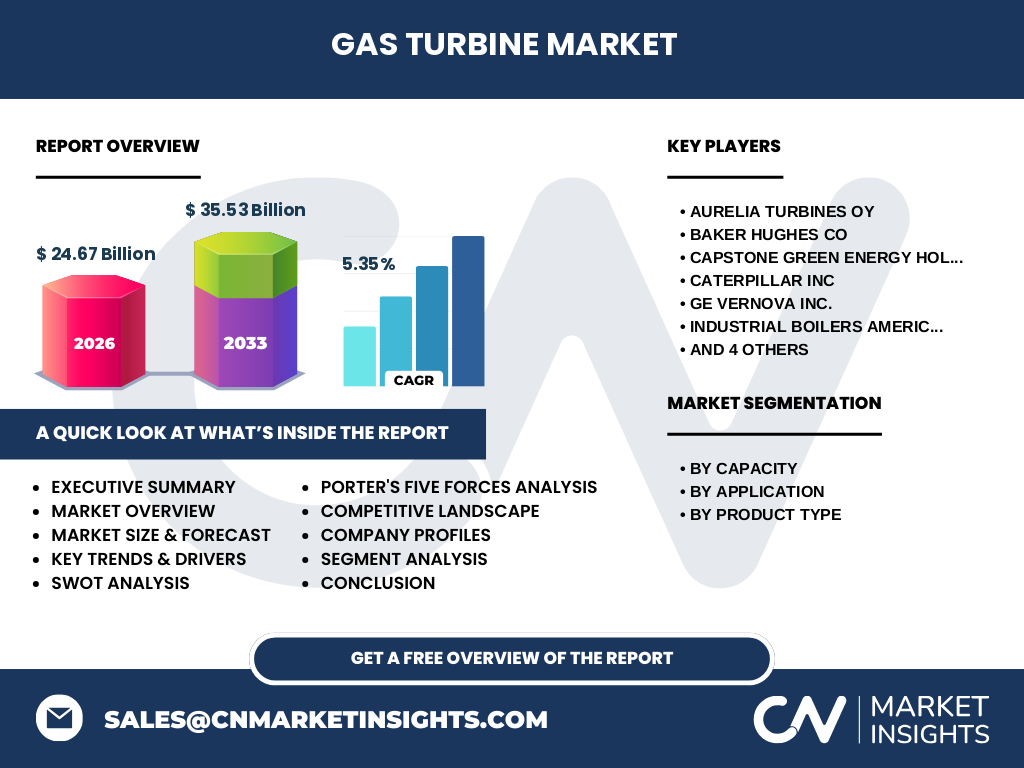

The competitive landscape is characterized by a handful of global OEMs that dominate through extensive product portfolios, after‑sales service networks, and R&D capabilities. Leading players include GE Vernova Inc., Siemens AG, Mitsubishi Heavy Industries Ltd, Kawasaki Heavy Industries Ltd, and Caterpillar Inc. These firms compete on turbine efficiency, reliability, and digital service solutions. Smaller yet innovative firms such as Capstone Green Energy Holdings, Inc., and Aurelia Turbines Oy focus on niche markets like small‑scale distributed generation. The market has seen moderate consolidation through strategic acquisitions aimed at expanding service capabilities and geographic reach.

What are the key findings in the Executive Summary?

The gas turbine market is valued at $24.67 billion in 2026 and is projected to reach $35.53 billion by 2033, reflecting a robust CAGR of 5.35 %. Growth is propelled by the need for flexible, low‑emission power and the expanding use of combined‑cycle technology. While capital intensity and competition from alternative energy storage pose challenges, digitalization and hybrid solutions create substantial upside. The market remains highly concentrated among a few large OEMs, with emerging opportunities in developing regions and in the integration of turbines with renewable and storage assets.

What are the Gas Turbine Market Forecasts for 2025‑2032?

Forecasts indicate a steady upward trajectory, with the market expanding from the 2026 base of $24.67 billion to exceed $35 billion by the early 2030s. The 5.35 % CAGR suggests consistent demand across all capacity segments, with the combined‑cycle segment expected to capture the largest share due to efficiency gains. Growth will be supported by ongoing renewable integration, industrial decarbonisation initiatives, and continued investments in grid‑stability solutions.

How is the Gas Turbine Market sized and shared by segmentation?

Segmentation by capacity reveals four distinct groups: Below 40 MW, 40‑120 MW, 120‑300 MW, and Above 300 MW. The below 40 MW segment caters to distributed and backup power, while the 40‑120 MW range dominates mid‑size utility projects. The 120‑300 MW bracket is favored for large combined‑cycle plants, and the above 300 MW category represents the most capital‑intensive, high‑output installations. By application, the market splits among Power Generation, Oil and Gas, and Industrial users, each demanding specific turbine configurations. Product‑type segmentation differentiates Open Cycle turbines—valued for quick start‑up—and Combined Cycle turbines—chosen for superior efficiency.

What is the Global Gas Turbine Market Size and Share by Region?

The global market is distributed across North America, Europe, Asia‑Pacific, the Middle East & Africa, and Latin America. While precise regional monetary values are not disclosed, the overall market size of $24.67 billion in 2026 reflects contributions from mature markets such as the United States and Europe, alongside rapid growth in Asia‑Pacific driven by industrialization and power‑generation needs.

What does the Regional Analysis of the Gas Turbine Market reveal?

North America remains a stronghold due to extensive power‑grid modernization programs and a mature oil‑and‑gas sector. Europe focuses on decarbonisation, fostering demand for high‑efficiency combined‑cycle turbines. Asia‑Pacific shows the highest growth potential, propelled by expanding industrial bases, rising electricity demand, and government incentives for cleaner generation. The Middle East and Africa exhibit steady demand linked to natural‑gas projects and power‑capacity expansion, while Latin America’s growth is constrained by economic volatility but benefits from emerging renewable‑integration projects.

Which companies lead the Gas Turbine Market and what are their strategies?

GE Vernova Inc. emphasizes advanced digital twins and service contracts to extend turbine life. Siemens AG leverages its strong wind‑energy portfolio to offer hybrid turbine solutions. Mitsubishi Heavy Industries Ltd focuses on high‑efficiency combined‑cycle units for Asian markets. Kawasaki Heavy Industries Ltd pursues modular designs for rapid deployment. Caterpillar Inc. targets the low‑capacity segment with compact, cost‑effective turbines. Capstone Green Energy Holdings, Inc. specializes in micro‑turbine technology for distributed generation, while Aurelia Turbines Oy invests in next‑generation materials to improve high‑temperature performance.

How does Porter’s Five Forces apply to the Gas Turbine Market?

Threat of new entrants is moderate due to high capital requirements and technology barriers. Bargaining power of suppliers is relatively strong because key components like turbine blades rely on specialized alloys. Bargaining power of buyers is moderate; large utilities negotiate long‑term contracts, but smaller industrial customers have limited leverage. Threat of substitutes is growing, especially from battery storage and renewable‑only solutions, yet turbines retain advantages in dispatchability. Competitive rivalry is intense among the few dominant OEMs, each seeking differentiation through efficiency, digital services, and after‑sales support.

What are the SWOT insights for the Gas Turbine Market?

Strengths: High power density, quick start‑up, and proven reliability. Weaknesses: High upfront costs and dependence on fossil‑fuel supply chains. Opportunities: Integration with renewable and storage assets, digital maintenance platforms, and expansion in emerging economies. Threats: Accelerating adoption of renewable‑only generation, regulatory shifts, and supply‑chain vulnerabilities for advanced materials.

What does the Gas Turbine Market Value Chain look like?

The value chain starts with raw‑material suppliers (nickel‑based superalloys, coatings), followed by component manufacturers (blades, combustors), turbine assembly plants, and system integrators that configure turbines for open‑ or combined‑cycle applications. Aftermarket services—including spare‑parts logistics, predictive maintenance, and retrofit upgrades—represent a high‑margin segment, increasingly supported by data analytics and remote monitoring platforms.

What are the key investment insights for the Gas Turbine Market?

Investors should prioritize companies with strong digital service ecosystems, as aftermarket revenue is less cyclical than new‑turbine sales. Exposure to firms expanding combined‑cycle portfolios aligns with efficiency‑driven demand. Emerging‑market projects offer higher growth rates but require careful assessment of political and currency risks. Partnerships that bring together turbine OEMs with renewable or storage providers create differentiated, future‑proof offerings and are attractive for long‑term capital allocation.

What are the main conclusions of the Gas Turbine Market report?

The market is on a clear growth path, underpinned by the need for flexible, low‑emission power generation. While capital intensity and competition from non‑turbine technologies pose challenges, the sector’s adaptability—through combined‑cycle efficiency, digital services, and hybridization—ensures strong upside. The forecasted increase to $35.53 billion by 2033 validates the sector’s resilience and relevance in the evolving energy landscape.

How was the research methodology conducted?

The study combined primary interviews with industry experts, OEM technical teams, and key end‑users, alongside secondary data from company reports, regulatory filings, and reputable market databases. Trend analysis employed historical growth rates and forward‑looking scenario modeling to derive the 5.35 % CAGR. Segmentation and regional breakdowns were validated through cross‑reference with publicly available project pipelines and capacity announcements.

What is the research scope and its limitations?

The scope covers global gas‑turbine manufacturing, sales, and service activities across the defined capacity, application, and product‑type segments, with a focus on the period 2025‑2032. Limitations include reliance on publicly disclosed financials and project data; private‑company specifics and confidential contracts are not reflected. Geographic granularity is limited to broad regions rather than country‑level detail.

Which key companies have recent developments in the Gas Turbine Market?

GE Vernova Inc. announced a partnership with a leading cloud provider to enhance its digital twin capabilities for turbine predictive maintenance. Siemens AG launched a next‑generation 400‑MW combined‑cycle turbine featuring a 62 % efficiency rating. Mitsubishi Heavy Industries Ltd. secured a multi‑year supply agreement for gas turbines in a Southeast Asian power‑plant consortium. Capstone Green Energy Holdings, Inc. unveiled a new micro‑turbine model targeting data‑center backup power. Kawasaki Heavy Industries Ltd. introduced a modular turbine container system designed for rapid deployment in remote locations.