1. What is the Precision Farming Market and why is it significant?

Precision farming, also known as site‑specific crop management, integrates advanced hardware, software, and services to collect real‑time agronomic data and enable data‑driven decisions on planting, fertilizing, irrigation, and harvesting. The market’s scope covers equipment such as GPS‑enabled tractors, drones, sensors, as well as analytics platforms and consultancy services. Its significance lies in delivering higher yields, reduced input costs, and sustainable resource use, positioning it as a critical enabler for food security and climate‑resilient agriculture.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Precision Farming Market?

Key drivers include rising global food demand, governmental incentives for sustainable agriculture, and rapid adoption of IoT and AI technologies. Restraints stem from high upfront capital costs and limited broadband connectivity in rural areas. Challenges involve data security concerns and the need for skilled personnel to interpret complex analytics. Opportunities arise from emerging services such as predictive maintenance, integration of satellite imagery, and growth in developing regions seeking to modernize traditional farms.

3. Which current and emerging trends are influencing the growth of the Precision Farming Market?

Current trends feature the convergence of cloud‑based analytics with edge computing, allowing faster on‑field decision making. Emerging trends include the use of autonomous machinery, blockchain for traceability, and machine‑learning models that predict pest outbreaks. Additionally, subscription‑based service models are gaining traction, offering farms access to premium data without large capital investments.

4. How did COVID‑19 affect the Precision Farming Market and what is the recovery outlook?

The pandemic disrupted supply chains for hardware components and delayed field trials, causing a short‑term slowdown in deployments. However, heightened awareness of supply‑chain resilience accelerated interest in digital agriculture solutions. Recovery began in late 2021, with accelerated adoption of remote monitoring tools, and the market is now on a robust growth trajectory supported by post‑pandemic investment in agri‑tech.

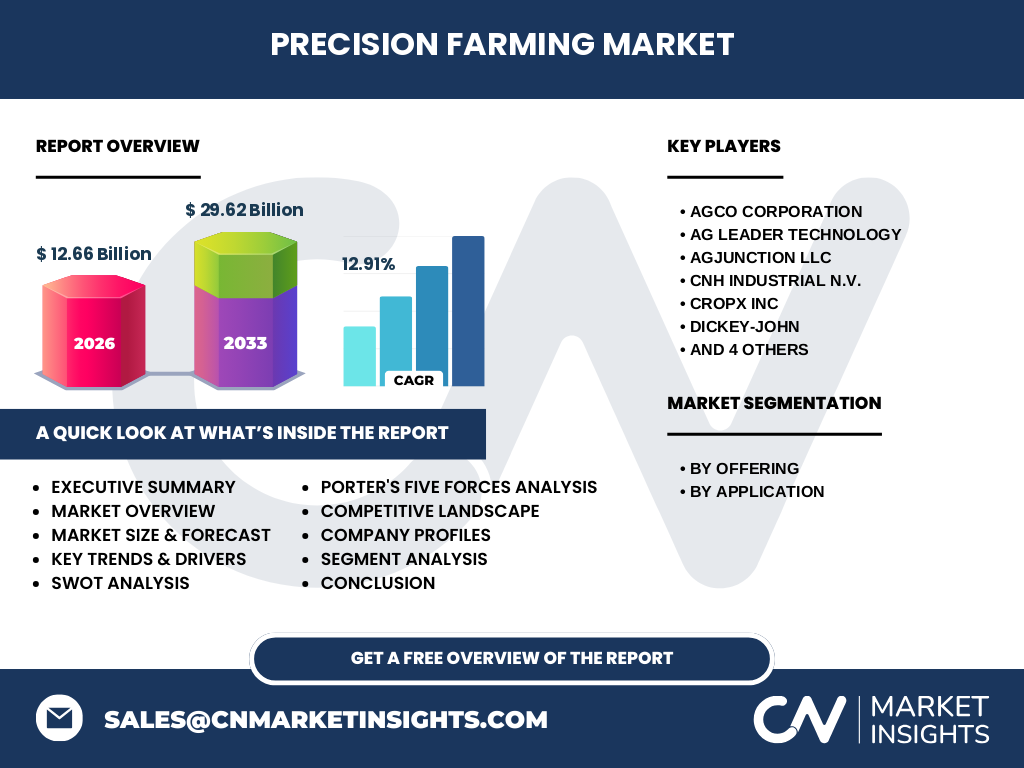

5. Who are the major competitors in the Precision Farming Market and what is the level of consolidation?

Leading competitors include AGCO Corporation, Deere & Company, Trimble Inc., CNH Industrial N.V., and Topcon. Others such as Ag Leader Technology, AgJunction LLC, CropX inc, DICKEY‑john, and TeeJet Technologies also hold notable positions. The market demonstrates moderate consolidation, with large agribusinesses acquiring niche sensor or software firms to broaden their end‑to‑end offerings.

6. What are the key findings from the executive summary of the Precision Farming Market?

The market is projected to expand from a 2026 valuation of $12.66 billion to $29.62 billion by 2033, reflecting a strong CAGR of 12.91 %. Growth is driven by technology integration, sustainability mandates, and increasing farm digitization. Hardware remains the largest offering segment, while yield monitoring and field mapping dominate application usage. Geographic expansion is especially strong in North America and Europe, with emerging opportunities in Asia‑Pacific.

7. What are the forecast expectations for the Precision Farming Market from 2025 to 2032?

Based on the stated CAGR of 12.91 %, the market is expected to maintain double‑digit growth through 2032. Continuous innovation in AI‑enabled decision support, widened broadband coverage, and rising adoption of subscription services are anticipated to sustain the upward trajectory, pushing total market value well above $30 billion by the early 2030s.

8. How is the Precision Farming Market sized and shared across its major segments?

By offering, the market is divided into hardware, software, and services. Hardware commands the largest share due to the necessity of sensors, GPS units, and autonomous equipment. Software follows, driven by analytics platforms that turn raw data into actionable insights. Services, including consulting and data‑management, represent a growing niche as farms outsource expertise. By application, yield monitoring, crop scouting, field mapping, inventory management, and weather tracking each capture distinct user needs, with yield monitoring and field mapping currently leading usage.

9. What is the global distribution of the Precision Farming Market size and share by region?

The market’s global footprint is anchored by North America and Europe, where early adoption of advanced agri‑tech and supportive policy frameworks generate the highest revenue concentration. Asia‑Pacific shows rapid expansion as agribusinesses invest in technology to meet population growth. While precise regional monetary values are not disclosed, the overall trend indicates a balanced yet accelerated shift toward emerging markets alongside established ones.

10. How does the Precision Farming Market perform in each major region?

In North America, strong farmer awareness and robust R&D ecosystems drive hardware sales and software subscriptions. Europe benefits from EU sustainability targets, fostering investment in field mapping and weather forecasting tools. Asia‑Pacific’s growth is fueled by large‑scale rice and wheat farms adopting yield monitoring to improve productivity. Latin America and the Middle East exhibit niche adoption, primarily in high‑value cash crops, creating pockets of opportunity for service providers.

11. Which companies lead the Precision Farming Market and what strategies are they employing?

Deere & Company and AGCO lead with integrated hardware‑software ecosystems, leveraging extensive dealer networks. Trimble and Topcon focus on high‑precision GNSS and mapping solutions, expanding through strategic partnerships with satellite providers. CNH Industrial emphasizes autonomous machinery, while CropX inc and AgJunction LLC drive innovation in soil‑sensor analytics and connectivity platforms. Across the board, firms are investing in mergers, joint ventures, and subscription‑based models to broaden market reach.

12. What does Porter’s Five Forces analysis reveal about the Precision Farming Market?

Threat of new entrants is moderate; high capital requirements and technology expertise create barriers. Bargaining power of suppliers is moderate, as specialized sensor components are limited but can be sourced from multiple vendors. Bargaining power of buyers is growing, with farms seeking cost‑effective, scalable solutions. Threat of substitutes remains low, given the unique benefits of data‑driven farming. Industry rivalry is intense, driven by rapid innovation and the race for integrated platforms.

13. What are the SWOT highlights for the Precision Farming Market?

Strengths: Proven yield improvements, strong sustainability credentials, and increasing digital infrastructure. Weaknesses: High initial investment and skill gaps in data interpretation. Opportunities: Expansion into emerging economies, development of AI‑based predictive tools, and service‑oriented revenue models. Threats: Cybersecurity risks, regulatory uncertainties, and potential price pressure from commoditized sensor markets.

14. How is the value chain structured in the Precision Farming Market?

The value chain begins with component manufacturers (sensors, GPS modules), proceeds to equipment assemblers (tractors, drones), then to software developers offering analytics platforms. Distribution occurs via dealer networks and direct online channels. End‑users (farmers) interact with service providers for installation, training, and data‑management support, creating feedback loops that drive product refinement and new feature development.

15. What investment insights are critical for stakeholders in the Precision Farming Market?

Investors should prioritize companies with strong R&D pipelines in AI and autonomous hardware, as these areas promise the highest margin expansion. Partnerships that combine satellite data with on‑field sensors are attractive for scaling solutions. Additionally, service‑oriented businesses delivering subscription analytics present recurring revenue streams and lower upfront cost barriers for end‑users, enhancing long‑term profitability.

16. What are the concluding takeaways from the Precision Farming Market analysis?

The market is on a decisive growth path, underpinned by a 12.91 % CAGR and a projected value of $29.62 billion by 2033. Technology integration, sustainability pressures, and evolving business models converge to create a fertile environment for both hardware innovators and software/service providers. Companies that can offer seamless, end‑to‑end solutions and address data‑security concerns will capture the dominant share of this expanding market.

17. Which research methodology was applied to develop this market report?

The study employed a mixed‑method approach, combining primary interviews with industry executives, secondary data collection from reputable agritech publications, and quantitative modeling using historical market figures. Trend extrapolation leveraged the provided CAGR of 12.91 % to forecast future values, while segment analysis derived from the listed offering and application categories.

18. What is the scope of this research and its limitations?

The scope covers global precision farming technologies, segmented by offering (hardware, software, services) and application (yield monitoring, crop scouting, field mapping, inventory management, weather tracking). Geographical coverage includes major regions such as North America, Europe, and Asia‑Pacific. Limitations stem from the reliance on publicly available data and the absence of granular regional revenue breakdowns, which may affect precise market‑share calculations.

19. Which key companies have recently announced developments in the Precision Farming Market?

Deere & Company launched an AI‑driven farm management suite integrating satellite imagery with machine‑learning yield forecasts. AGCO announced a strategic partnership with a leading cloud provider to deliver real‑time field data analytics. Trimble introduced a next‑generation GNSS module with enhanced accuracy for autonomous tractors. CropX inc released a low‑cost soil‑sensor network aimed at smallholder farms, while Topcon unveiled a cloud‑based field‑mapping platform that syncs with existing equipment fleets.