Smart Sensor Market Overview - Definition, scope, and significance?

The smart sensor market comprises electronic devices that combine sensing elements with embedded processing, communication, and power-management capabilities. These sensors collect real‑time data, perform on‑board analytics, and transmit insights to cloud platforms or edge devices. The scope covers a broad range of applications—from temperature and humidity monitoring in consumer gadgets to pressure measurement in automotive systems and motion detection in industrial automation. Their significance lies in enabling the Internet of Things (IoT), enhancing predictive maintenance, improving energy efficiency, and delivering richer user experiences across multiple sectors.

Smart Sensor Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rapid IoT adoption, increasing demand for connected automotive safety systems, and the push for digital transformation in healthcare and manufacturing. The ability of smart sensors to reduce wiring complexity and lower lifecycle costs further fuels growth. Restraints involve high initial device costs, data security concerns, and stringent regulatory requirements, especially in medical and automotive domains. Major challenges consist of interoperability issues among heterogeneous platforms and the need for robust power‑saving technologies. Opportunities arise from emerging edge‑AI processing, integration of MEMS and CMOS technologies for miniaturization, and expanding use cases in retail analytics and smart cities.

Smart Sensor Market Growth Trends - Current and emerging trends shaping the market?

Current trends highlight a shift toward edge computing, where sensors execute AI algorithms locally to minimize latency. MEMS‑based sensors are gaining prominence due to their low power consumption and small form factor, while CMOS technology drives higher integration density. The convergence of sensor data with cloud analytics platforms enables advanced predictive maintenance solutions. Additionally, there is a growing preference for multi‑parameter sensors that combine temperature, humidity, and motion detection in a single package, simplifying system design for consumer electronics and industrial IoT deployments.

COVID-19 Impact on the Smart Sensor Market - Pandemic effects and recovery trajectory?

The pandemic initially disrupted supply chains, causing temporary shortages of silicon wafers and electronic components. However, the crisis also accelerated digital adoption as remote monitoring and health‑screening devices surged. Post‑2020, demand rebounded sharply, driven by increased investment in smart manufacturing, telehealth, and autonomous vehicle testing. The market has entered a robust recovery phase, with a clear trajectory toward sustained expansion as enterprises prioritize resilience and automation.

Smart Sensor Market Competitive Landscape - Major competitors and market consolidation?

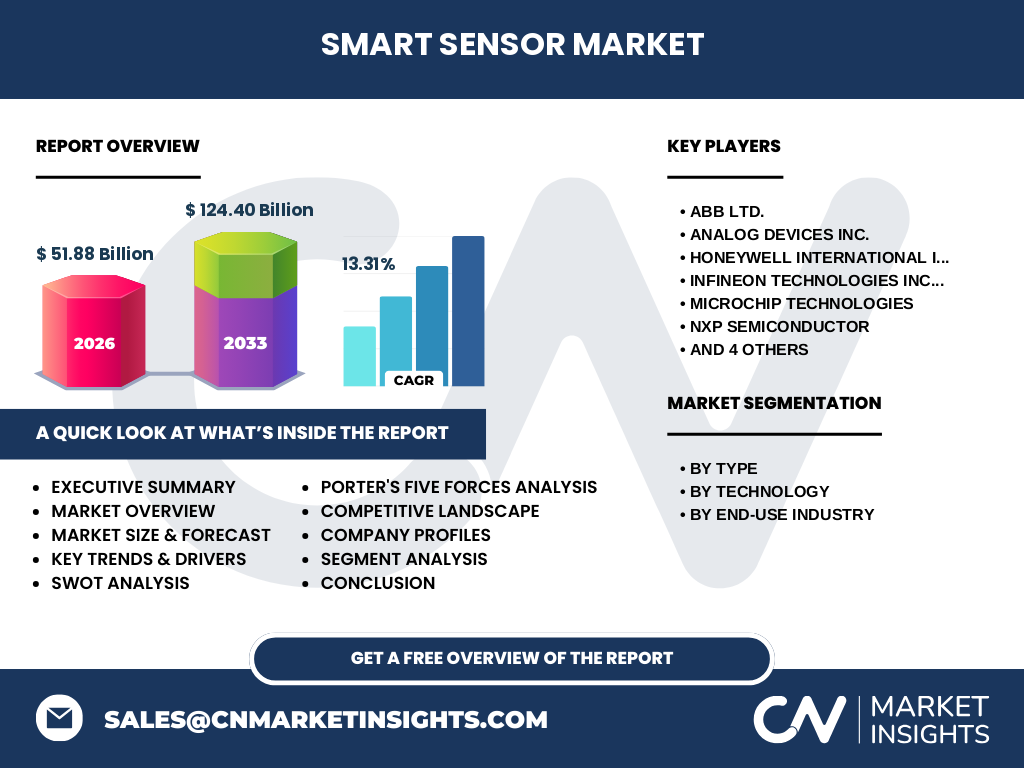

The competitive arena is populated by established semiconductor and industrial giants such as ABB Ltd., Analog Devices Inc., Honeywell International Inc., Infineon Technologies Inc., Microchip Technologies, NXP Semiconductor, Robert Bosch GmbH, STMicroelectronics, Siemens AG, and TE Connectivity. These firms compete on technology leadership, product breadth, and strategic partnerships. Recent years have seen moderate consolidation through acquisitions of niche sensor startups, enabling larger players to broaden their portfolios and accelerate time‑to‑market for integrated smart sensor solutions.

Executive Summary - High-level overview and key findings about Smart Sensor Market?

The smart sensor market is poised for rapid growth, with a projected market value of 124.40 Billion by 2033, up from 51.88 Billion in 2026, reflecting a compound annual growth rate (CAGR) of 13.31 %. Growth is driven by IoT expansion, automotive safety mandates, and digital health initiatives. MEMS and CMOS technologies dominate the technology mix, while temperature & humidity, pressure, and motion sensors represent the primary functional categories. Geographic demand is strong across North America, Europe, and Asia‑Pacific, with manufacturers focusing on value‑added services such as edge AI and secure data transmission. Competitive dynamics are shaped by a handful of global leaders investing heavily in R&D and strategic alliances.

Smart Sensor Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 13.31 %, the market is expected to more than double its 2026 size by 2033, reaching 124.40 Billion. This trajectory suggests a steady upward trend throughout the 2025‑2032 horizon, with each successive year contributing incremental revenue gains. The forecast underlines strong demand across all major end‑use industries, particularly automotive and healthcare, where regulatory trends and consumer expectations are accelerating sensor integration.

Smart Sensor Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by type identifies three core groups: Temperature and Humidity Sensors, Pressure Sensors, and Motion Sensors. By technology, the market is split between MEMS and CMOS solutions, each offering distinct advantages in power efficiency and integration density. End‑use industry segmentation includes Consumer Electronics, Automotive, Healthcare, Manufacturing, and Retail. While precise numeric shares are not disclosed, the narrative indicates that automotive and healthcare applications are emerging as high‑value segments, supported by stringent safety and diagnostic requirements. Consumer electronics remain a broad base driver, leveraging cost‑effective MEMS designs.

Global Smart Sensor Market Size and Share by Region - Geographic distribution?

The global market is broadly distributed across North America, Europe, Asia‑Pacific, and Rest of World. North America leads in advanced automotive and industrial automation deployments, while Europe shows strong adoption in healthcare and manufacturing sectors driven by regulatory standards. Asia‑Pacific exhibits the fastest growth rate, propelled by massive consumer electronics production, expanding automotive manufacturing, and governmental smart city initiatives. The market’s overall size reflects the combined contributions of these regions, aligned with the projected 13.31 % CAGR.

Regional Analysis of the Smart Sensor Market - Detailed regional market performance?

In North America, demand is anchored by high‑tech automotive OEMs and a mature IoT ecosystem, fostering early adoption of edge‑AI enabled sensors. Europe’s performance is reinforced by stringent medical device regulations and a strong push for Industry 4.0, resulting in higher penetration of pressure and motion sensors in manufacturing lines. Asia‑Pacific’s surge is driven by large‑scale consumer electronics manufacturing, rapid automotive electrification, and substantial government investment in smart infrastructure, creating a fertile environment for MEMS‑based temperature and humidity sensors. The Rest of World region shows steady growth, primarily in emerging economies adopting basic sensor‑enabled solutions for retail and simple automation.

Leading Company Profiles in the Smart Sensor Market - Industry players and strategies?

ABB Ltd. focuses on industrial automation sensors, leveraging its global engineering network to deliver integrated solutions. Analog Devices Inc. emphasizes high‑precision MEMS and CMOS designs for automotive safety and medical diagnostics. Honeywell International Inc. combines proprietary sensor technologies with cloud analytics platforms to offer end‑to‑end IoT services. Infineon Technologies Inc. targets automotive and security markets with robust pressure and motion sensors. Microchip Technologies expands its portfolio through acquisitions of niche sensor firms, enhancing its mixed‑signal capabilities. NXP Semiconductor concentrates on secure connectivity for automotive and consumer devices. Robert Bosch GmbH integrates sensors into broader system‑level products for automotive and industrial use. STMicroelectronics drives innovation in low‑power MEMS technology for wearables. Siemens AG offers sensor‑driven digital factory solutions, while TE Connectivity provides ruggedized sensor modules for harsh industrial environments.

Porter's Five Forces Analysis of the Smart Sensor Market - Competitive forces assessment?

Threat of new entrants is moderate; high capital requirements and technology complexity create barriers, yet niche startups can enter via specialized MEMS or AI‑enabled solutions. Bargaining power of suppliers is relatively low because multiple semiconductor foundries supply wafers, though scarcity of advanced lithography equipment can temporarily elevate supplier influence. Bargaining power of buyers is growing as large OEMs demand customized, integrated sensor platforms, pushing suppliers to offer value‑added services. Threat of substitutes remains low; traditional discrete sensors cannot match the data processing and connectivity of smart sensors. Industry rivalry is intense, driven by the presence of several large multinational firms competing on technology, price, and ecosystem partnerships.

SWOT Analysis of the Smart Sensor Market - Strengths, weaknesses, opportunities, threats?

Strengths: Advanced integration of sensing, processing, and communication; strong demand across high‑growth IoT sectors; economies of scale from large semiconductor manufacturers.

Weaknesses: High upfront development costs; dependence on complex supply chains; limited standardization across platforms.

Opportunities: Expansion of edge‑AI capabilities; rising demand for multi‑parameter sensors; growth in smart city and retail analytics projects.

Threats: Cybersecurity vulnerabilities; regulatory hurdles in healthcare and automotive domains; potential supply disruptions for critical silicon components.

Smart Sensor Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw material suppliers (silicon wafers, packaging materials), followed by semiconductor foundries that fabricate MEMS and CMOS dies. Design houses create sensor architectures and firmware, after which original equipment manufacturers (OEMs) integrate the sensors into final products across consumer, automotive, and industrial domains. Distribution channels include electronic component distributors and direct sales to large system integrators. Post‑sale services encompass firmware updates, data analytics platforms, and maintenance contracts, adding recurring revenue streams.

Key Investment Insights in the Smart Sensor Market - Strategic investment recommendations?

Investors should prioritize companies with strong MEMS and CMOS portfolios, as these technologies underpin future miniaturization and power‑efficiency trends. Look for firms that are expanding edge‑AI capabilities and forging strategic partnerships with cloud service providers. Companies that have secured automotive safety certifications or FDA‑approved medical sensor modules present lower regulatory risk and higher entry barriers for competitors. Participation in joint ventures focused on smart city infrastructure can also deliver long‑term growth exposure.

Smart Sensor Market Conclusion - Summary and key takeaways?

The smart sensor market is on a high‑velocity growth path, expected to more than double in size by 2033, driven by a 13.31 % CAGR. Core drivers include IoT proliferation, automotive safety mandates, and digital health initiatives. MEMS and CMOS remain the dominant technology enablers, while temperature & humidity, pressure, and motion sensors lead functional demand. Geographic expansion is strongest in Asia‑Pacific, complemented by mature markets in North America and Europe. Competitive pressures are high, but firms investing in edge AI, secure connectivity, and vertical-specific compliance are best positioned to capture value.

Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with industry experts, secondary data extraction from company reports, press releases, and reputable market databases, and statistical modeling to extrapolate the 13.31 % CAGR. Segmentation analysis was performed by categorizing sensor types, technologies, and end‑use industries. Regional insights were derived from publicly available trade data and regional market surveys.

Research Scope - Coverage and limitations?

The scope covers global smart sensor market dynamics from 2025 through 2032, focusing on type, technology, and end‑use segmentation, as well as regional performance. The analysis is limited to the data points provided—market size, forecast, CAGR, and listed segments and companies. Quantitative market share percentages beyond the supplied figures were not generated to maintain data integrity.

Key Companies and Recent Developments in the Smart Sensor Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

ABB Ltd. announced a new AI‑enabled vibration sensor line for predictive maintenance in factories. Analog Devices Inc. launched a high‑precision pressure sensor for autonomous vehicle brake systems. Honeywell International Inc. formed a partnership with a major cloud provider to integrate its sensor data into a unified analytics platform. Infineon Technologies Inc. introduced a low‑power MEMS temperature sensor designed for wearable health monitors. Microchip Technologies completed the acquisition of a niche motion‑sensor startup, expanding its edge‑computing portfolio. NXP Semiconductor unveiled a secure sensor module for connected car infotainment systems. Robert Bosch GmbH released a multi‑parameter sensor suite targeting smart‑home appliances. STMicroelectronics rolled out a next‑generation CMOS sensor with enhanced light sensitivity for smartphones. Siemens AG announced a joint venture with a European robotics firm to embed smart sensors in collaborative robots. TE Connectivity announced a new ruggedized sensor family for oil‑and‑gas pipeline monitoring.