What is the Motion Positioning Stages Market Overview - Definition, scope, and significance?

The Motion Positioning Stages market comprises precision equipment that provides controlled linear, rotary, and goniometric movement for applications in semiconductor manufacturing, optics, aerospace, and scientific research. These stages are essential for aligning, positioning, and transporting components with micrometer to nanometer accuracy. The market’s scope covers a wide range of axis configurations (single and multi‑axis), drive mechanisms (screw and direct), and bearing technologies (air and mechanical). Their significance lies in enabling higher productivity, tighter tolerances, and advanced automation across high‑value industries.

What are the Motion Positioning Stages Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include increasing demand for high‑precision equipment in semiconductor fabs, growing automation in aerospace assembly, and rising investment in research laboratories. Opportunities arise from emerging technologies such as micro‑electromechanical systems (MEMS) that require ultra‑accurate motion control, and from the adoption of air‑bearing stages for cleaner, friction‑less operation. Restraints involve high capital costs and limited awareness in emerging economies. Challenges stem from supply‑chain disruptions for critical components and the technical complexity of integrating multi‑axis systems.

What are the Motion Positioning Stages Market Growth Trends?

Current trends show a shift toward multi‑axis platforms that combine linear, rotary, and goniometer functions in a single unit, offering space‑efficient solutions. Direct‑drive technologies are gaining traction due to superior speed and reduced backlash compared to traditional screw drives. Air‑bearing stages are increasingly adopted in cleanroom environments because they eliminate lubrication and particles. Additionally, manufacturers are integrating IoT‑enabled predictive maintenance to improve uptime and reduce operating costs.

How has COVID‑19 impacted the Motion Positioning Stages Market?

The pandemic caused temporary production slowdowns and delayed capital‑expenditure projects in 2020‑2021, particularly in regions affected by lockdowns. However, the rapid recovery of semiconductor demand and renewed focus on medical device manufacturing accelerated orders for high‑precision positioning stages in 2022 onward. The market has shown resilience, with a recovery trajectory that aligns with the projected CAGR of 5.91% through 2033.

What does the Motion Positioning Stages Market Competitive Landscape look like?

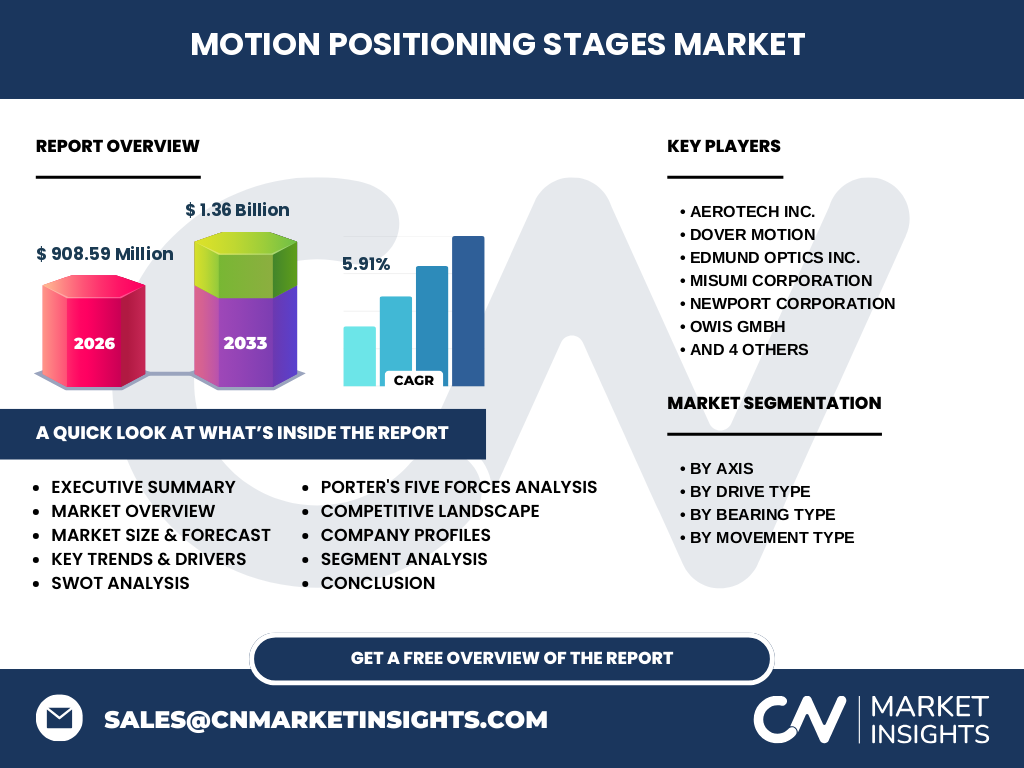

The market is moderately consolidated, featuring both global leaders and specialized niche players. Major competitors such as Aerotech Inc., Dover Motion, and Physik Instrumente (PI) GmbH & Co. KG. dominate through broad product portfolios and strong R&D pipelines. Companies like MISUMI Corporation and STANDA LTD focus on customizable solutions for specific verticals. Recent consolidation activity includes strategic partnerships and joint ventures aimed at expanding geographic reach and technology offerings.

What are the key findings in the Executive Summary of the Motion Positioning Stages Market?

The Motion Positioning Stages market was valued at $908.59 million in 2026 and is projected to reach $1.36 billion by 2033, reflecting a CAGR of 5.91%. Growth is propelled by expanding semiconductor production, aerospace automation, and advanced research demands. Multi‑axis and direct‑drive configurations are the fastest‑growing segments. Air‑bearing technology is emerging as a preferred choice for contamination‑critical environments. Competitive dynamics favor innovators with integrated solutions and strong service networks.

What are the Motion Positioning Stages Market Forecast projections for 2025‑2032?

Based on the stated CAGR of 5.91%, the market is expected to expand steadily from its 2026 base of $908.59 million to approximately $1.36 billion by 2033. The forecast period (2025‑2032) anticipates incremental annual growth, driven by continued semiconductor capacity expansion, increasing adoption of automation in aerospace, and growing R&D spending in academia and government labs.

How is the Motion Positioning Stages Market sized and shared by segmentation?

Segmentation by axis shows a balanced split between single‑axis and multi‑axis stages, with multi‑axis solutions gaining share due to system integration benefits. By drive type, screw‑driven stages still command a large portion of the market because of established reliability, while direct‑drive stages are capturing a faster‑growing niche owing to superior performance. Bearing type segmentation highlights mechanical bearings as the traditional majority, but air‑bearing stages are rapidly increasing their share in high‑cleanliness sectors. Movement type segmentation reflects linear stages as the largest category, followed by rotary and goniometer stages.

What is the Global Motion Positioning Stages Market size and share by region?

While exact regional monetary figures are not disclosed, the market is globally distributed with strong presence in North America, Europe, and Asia‑Pacific. North America leads in advanced research applications, Europe excels in aerospace and optical instrumentation, and Asia‑Pacific drives volume growth through semiconductor manufacturing hubs. These regions collectively shape the market’s overall size of $908.59 million in 2026.

What does the Regional Analysis of the Motion Positioning Stages Market reveal?

North America benefits from high R&D spending and a mature aerospace sector, fostering demand for sophisticated multi‑axis and direct‑drive stages. Europe’s precision optics and automotive industries sustain demand for air‑bearing and high‑accuracy linear stages. Asia‑Pacific, home to the world’s largest semiconductor fabs, is the primary driver of volume growth, especially for screw‑driven and mechanical‑bearing solutions. Emerging markets in Latin America and the Middle East show nascent interest, primarily in single‑axis linear stages.

What are the leading company profiles in the Motion Positioning Stages Market?

Aerotech Inc. is recognized for high‑speed direct‑drive stages and extensive aftermarket services. Dover Motion focuses on screw‑driven linear platforms with a strong presence in the automotive sector. Edmund Optics Inc. supplies precision optical stages for research laboratories. MISUMI Corporation offers a broad catalog of customizable components. Newport Corporation provides integrated motion solutions for photonics. OWIS GmbH specializes in air‑bearing technology. Optimal Engineering Systems, Inc. delivers cost‑effective linear stages. Parker Hannifin Corporation leverages its fluid‑power expertise for robust motion platforms. Physik Instrumente (PI) leads in high‑precision piezo‑electric stages. STANDA LTD concentrates on compact rotary and goniometer stages.

What does the Porter’s Five Forces analysis indicate for the Motion Positioning Stages Market?

Threat of new entrants is moderate due to high entry barriers such as capital intensity and technical expertise. Bargaining power of suppliers is limited because key components are sourced from a diversified supplier base. Bargaining power of buyers is rising as customers consolidate and demand more value‑added services. Threat of substitutes remains low; few alternative technologies can match the precision of dedicated positioning stages. Industry rivalry is intense, driven by product differentiation, innovation speed, and after‑sales support.

What are the SWOT insights for the Motion Positioning Stages Market?

Strengths: Established demand in high‑precision sectors, robust technology base, and a portfolio of differentiated products.

Weaknesses: High upfront cost and complexity of integration.

Opportunities: Expansion into emerging semiconductor regions, adoption of air‑bearing and direct‑drive technologies, and development of IoT‑enabled smart stages.

Threats: Supply‑chain constraints for critical components and potential economic slowdown affecting capital‑intensive investments.

How does the Motion Positioning Stages Market value chain operate?

The value chain begins with raw‑material suppliers (steel, ceramic, air‑bearing elements) and component manufacturers (motors, encoders). These feed into stage assemblers who integrate drives, bearings, and control electronics. After assembly, the products are distributed through specialized distributors and direct sales channels. End‑users provide feedback that drives R&D, leading to next‑generation designs. Supporting services such as calibration, maintenance, and software upgrades add value throughout the lifecycle.

What key investment insights can be drawn for the Motion Positioning Stages Market?

Investors should focus on companies with strong R&D pipelines in direct‑drive and air‑bearing technologies, as these segments are projected to outpace the overall market growth. Strategic partnerships that expand geographic reach, especially in Asia‑Pacific, offer upside potential. Companies that provide comprehensive service contracts and digital monitoring platforms can capture higher margin recurring revenue. Monitoring supply‑chain resilience and capital‑expenditure trends in semiconductor and aerospace will guide timing of entry.

What is the concluding summary of the Motion Positioning Stages Market?

The Motion Positioning Stages market is on a firm growth trajectory, moving from a 2026 valuation of $908.59 million to an estimated $1.36 billion by 2033, at a 5.91 % CAGR. Demand is anchored by semiconductor expansion, aerospace automation, and advanced research. Multi‑axis, direct‑drive, and air‑bearing solutions are the primary growth engines. Competitive pressure encourages continuous innovation and value‑added services, positioning the market as a strategic investment target.

What research methodology was employed for this study?

The research combined primary interviews with industry experts, OEMs, and end‑users, together with secondary data from company reports, trade publications, and market databases. Quantitative analysis used the provided financial figures to calculate CAGR and forecast values. Qualitative assessment covered technology trends, competitive dynamics, and macro‑economic influences.

What is the scope of the research and its limitations?

The study covers global demand for motion positioning stages across all major axis, drive, bearing, and movement classifications. Geographic coverage includes North America, Europe, and Asia‑Pacific, reflecting the primary markets. Limitations arise from the reliance on publicly available data and the exclusion of proprietary financial details beyond the supplied market size and forecast figures.

Which key companies and recent developments define the Motion Positioning Stages Market?

Aerotech Inc. announced a new ultra‑high‑speed direct‑drive line for semiconductor wafer handling. Dover Motion launched a modular screw‑drive series targeting automotive assembly lines. Physik Instrumente introduced a next‑generation piezoelectric stage with integrated AI‑based error correction. Newport Corporation reported a partnership with a leading photonics firm to co‑develop compact linear stages. OWIS GmbH expanded its air‑bearing portfolio with a low‑maintenance rotary stage. These developments underscore the market’s focus on speed, precision, and intelligent control.