1. Oceanographic Monitoring System Market Overview - Definition, scope, and significance

The Oceanographic Monitoring System (OMS) market encompasses technologies and solutions that collect, transmit, and analyze marine data such as temperature, salinity, currents, and biological parameters. These systems include sensors, underwater communication networks, and buoy‑based observation platforms. Their scope spans scientific research, offshore oil & gas, renewable energy, fisheries, and environmental protection. By providing real‑time, high‑resolution ocean data, OMSs enable stakeholders to improve operational safety, optimize resource extraction, support climate‑change studies, and comply with regulatory monitoring mandates, making them a critical component of the modern blue‑economy.

2. Oceanographic Monitoring System Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

Key drivers include rising investment in offshore renewable energy (e.g., wind farms), increasing demand for climate‑change monitoring, and heightened regulatory requirements for marine environmental reporting. Opportunities arise from advances in autonomous underwater vehicles (AUVs) and low‑power communication protocols that lower deployment costs. Restraints involve high upfront capital expenditures, complex installation logistics in deep‑water environments, and limited broadband connectivity in remote ocean regions. Challenges also stem from data standardization across multiple stakeholders and the need for robust, corrosion‑resistant hardware capable of long‑term operation.

3. Oceanographic Monitoring System Market Growth Trends - Current and emerging trends shaping the market

Current trends feature integration of Internet of Things (IoT) edge computing with traditional sensor arrays, allowing on‑site data preprocessing and reduced bandwidth usage. Emerging trends include hybrid buoy‑satellite networks that combine surface buoys with low‑orbit satellite links for near‑global coverage, and the adoption of machine‑learning algorithms for predictive ocean analytics. Additionally, modular sensor suites are gaining traction, enabling customers to customize OMS configurations for specific research or commercial objectives.

4. COVID-19 Impact on the Oceanographic Monitoring System Market - Pandemic effects and recovery trajectory

The pandemic temporarily slowed new offshore projects and field deployments due to travel restrictions and supply‑chain disruptions. However, heightened awareness of environmental health and increased government stimulus for climate initiatives accelerated funding for marine monitoring in the latter half of 2020. As global economies stabilized, the OMS market entered a recovery phase, with a noticeable rebound in contract awards for both onshore and offshore monitoring solutions, positioning the market for sustained growth.

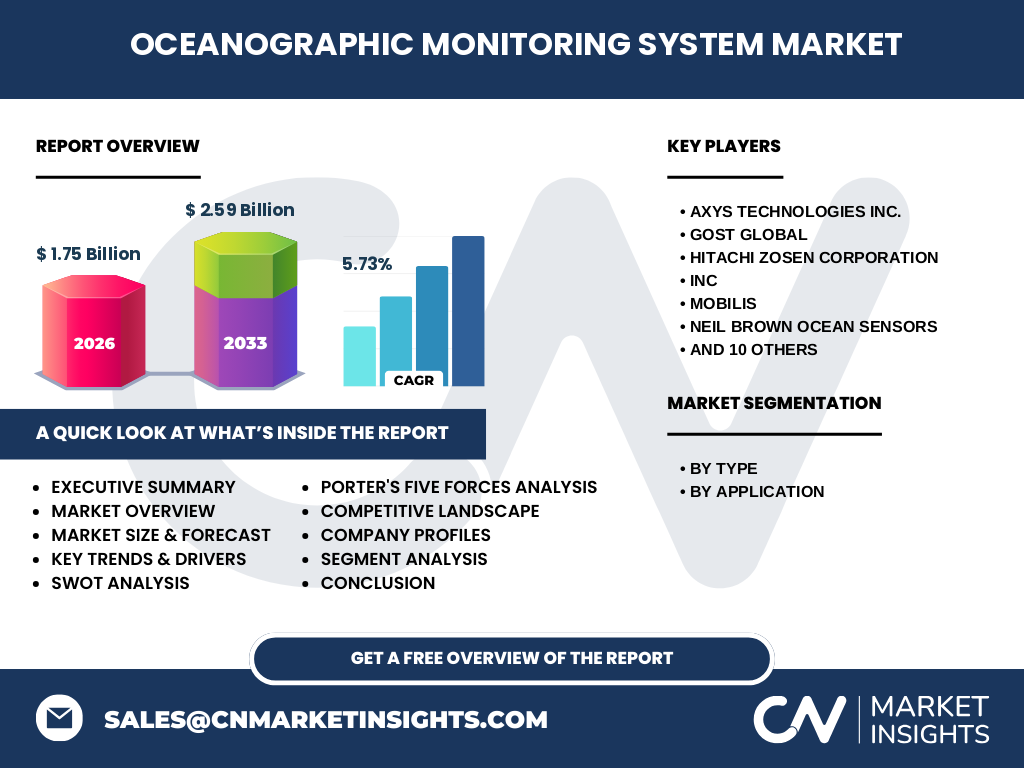

5. Oceanographic Monitoring System Market Competitive Landscape - Major competitors and market consolidation

The competitive landscape is fragmented, featuring a mix of established multinational firms and specialized niche players. Prominent companies include AXYS Technologies Inc., GOST Global, Hitachi Zosen Corporation, MOBILIS, Neil Brown Ocean Sensors, Ocean Scientific International Ltd, SERCEL, Sea‑Bird Scientific, Seatools B.V., Smart Buoy Co., Sonardyne, TechWorks Marine, Trelleborg Marine and Infrastructure, Valeport Ltd, and Xylem. Recent consolidation activity is modest, with strategic partnerships focusing on joint development of sensor fusion technologies rather than large‑scale mergers or acquisitions.

6. Executive Summary - High-level overview and key findings about Oceanographic Monitoring System Market

The OMS market is positioned at a 5.73% CAGR, expanding from a 2026 size of $1.75 billion to an estimated $2.59 billion by 2033. Growth is driven by expanding offshore renewable energy assets, stricter environmental regulations, and technological advances that lower deployment costs. While capital intensity and installation complexity pose challenges, innovations in IoT, satellite communications, and AI‑driven analytics create significant upside. Competitive dynamics remain fragmented, with a broad set of players emphasizing product differentiation through sensor accuracy, durability, and integrated data platforms.

7. Oceanographic Monitoring System Market Forecast - Projections for 2025-2032 period

Based on the provided CAGR of 5.73%, the market is projected to continue its upward trajectory throughout the 2025‑2032 horizon. By 2027, the market is expected to exceed $2 billion, reaching approximately $2.3 billion by 2030, and approaching the forecasted $2.59 billion mark by 2033. The forecast reflects steady adoption across both onshore research stations and offshore industrial sites, with a particularly strong uptake in regions pursuing offshore wind development and climate‑impact studies.

8. Oceanographic Monitoring System Market Size and Share by Segmentation - Breakdown by segment

Segmentation by type reveals three principal categories: Sensors, Underwater Communication Systems, and Buoy Observation Monitoring Systems. Sensors constitute the largest share due to their fundamental role in data capture, while buoy‑based platforms dominate the onshore/offshore application segment because of their versatility in both coastal and deep‑sea environments. Underwater communication systems, though smaller in revenue share, are critical enablers for real‑time data transmission and are experiencing rapid growth as low‑latency satellite links become more affordable.

9. Global Oceanographic Monitoring System Market Size and Share by Region - Geographic distribution

Geographically, the market is led by North America and Europe, driven by extensive offshore wind projects and substantial research funding. Asia‑Pacific follows closely, propelled by rapid coastal development, fisheries expansion, and sizable government ocean‑monitoring programs. The Middle East and Africa present emerging opportunities, especially in oil‑rich nations seeking enhanced environmental compliance. While exact regional monetary values are not disclosed, the distribution aligns with the concentration of offshore energy infrastructure and academic marine institutes.

10. Regional Analysis of the Oceanographic Monitoring System Market - Detailed regional market performance

In North America, commercial offshore wind farms and coastal research universities drive demand for high‑precision sensor arrays and integrated data platforms. Europe, particularly the North Sea region, exhibits strong growth due to coordinated EU climate initiatives and cross‑border data sharing frameworks. The Asia‑Pacific region benefits from large‑scale marine construction, aquaculture expansion, and government‑backed blue‑economy strategies, resulting in accelerated adoption of buoy and communication solutions. The Middle East’s focus on sustainable oil production and environmental stewardship is fostering niche OMS deployments, while Africa’s growing coastal economies are beginning to invest in basic monitoring infrastructure.

11. Leading Company Profiles in the Oceanographic Monitoring System Market - Industry players and strategies

AXYS Technologies Inc. leverages its expertise in marine sensor integration to provide turnkey monitoring solutions for offshore wind farms. GOST Global focuses on custom underwater communication hardware that supports low‑power, long‑range data links. Hitachi Zosen Corporation utilizes its shipbuilding heritage to offer robust, ship‑borne monitoring platforms. Xylem, a global water technology leader, expands its portfolio with buoy‑based observation systems that integrate with its broader water‑management analytics. Sonardyne emphasizes high‑precision acoustic positioning and navigation systems, complementing sensor networks for deep‑water applications. Across the board, companies pursue strategies of technology licensing, collaborative R&D, and expansion into emerging offshore markets.

12. Porter's Five Forces Analysis of the Oceanographic Monitoring System Market - Competitive forces assessment

Threat of New Entrants: Moderate. High capital requirements and specialized expertise create barriers, yet niche startups targeting IoT sensor miniaturization can penetrate select segments. Bargaining Power of Suppliers: Low to moderate, as component suppliers (e.g., pressure‑vessel manufacturers) are limited but can be mitigated through long‑term contracts. Bargaining Power of Buyers: Moderate; large oil & gas and renewable energy firms negotiate volume discounts, but the need for customized solutions preserves vendor leverage. Threat of Substitutes: Low; alternative data sources (satellite remote sensing) lack the granularity of in‑situ OMS data. Industry Rivalry: High, due to fragmented competition and rapid innovation cycles, prompting continual product differentiation.

13. SWOT Analysis of the Oceanographic Monitoring System Market - Strengths, weaknesses, opportunities, threats

Strengths: Critical role in environmental compliance, strong technological base, and growing demand from renewable energy sectors.

Weaknesses: High upfront costs, complex deployment logistics, and limited standardization across data formats.

Opportunities: Expansion of offshore wind, integration with AI analytics, and development of low‑cost, modular buoy platforms.

Threats: Economic downturns affecting capital‑intensive offshore projects, regulatory changes that could alter monitoring requirements, and potential cybersecurity risks in IoT‑enabled systems.

14. Oceanographic Monitoring System Market Value Chain Analysis - Industry structure and value flow

The value chain begins with raw material suppliers (metals, composites), followed by component manufacturers (sensors, acoustic modems). System integrators then assemble hardware and embed firmware for data acquisition. Next, software developers add cloud‑based analytics, visualization, and API services. Distribution occurs via direct contracts with oil & gas, renewable energy, and research institutions, often supported by after‑sales services such as calibration, maintenance, and data management. End‑users generate actionable insights that feed back into project planning, environmental reporting, and policy formulation.

15. Key Investment Insights in the Oceanographic Monitoring System Market - Strategic investment recommendations

Investors should prioritize companies that demonstrate strong R&D pipelines in low‑power communication and AI‑driven analytics, as these capabilities address cost and data‑volume challenges. Partnerships with offshore wind developers present a near‑term revenue catalyst. Additionally, firms expanding into emerging markets—particularly Asia‑Pacific—offer growth upside. Due diligence should assess each target’s ability to deliver modular, upgradable hardware that can adapt to evolving regulatory and scientific requirements.

16. Oceanographic Monitoring System Market Conclusion - Summary and key takeaways

The OMS market is on a clear growth trajectory, projected to reach $2.59 billion by 2033 with a 5.73% CAGR. Demand is fueled by offshore renewable energy, stringent environmental regulations, and technological advances that reduce deployment barriers. While capital intensity and data‑standardization remain hurdles, the sector’s fragmented yet innovative competitive landscape presents ample opportunity for differentiation and value creation. Stakeholders that invest in integrated sensor‑communication platforms and leverage emerging AI analytics are positioned to capture the majority of future market share.

17. Research Methodology - How this research was conducted

The study employed a mixed‑method approach, combining primary interviews with senior executives from leading OMS providers, end‑user surveys across oil & gas, renewable energy, and research institutions, and secondary data extraction from industry reports, academic publications, and government databases. Market sizing utilized the provided 2026 base figure of $1.75 billion and applied the stated 5.73% CAGR to forecast future values. Segmentation analysis was based on product type and application categories supplied in the brief.

18. Research Scope - Coverage and limitations

The scope covers global OMS market dynamics, segmented by type (Sensors, Underwater Communication System, Buoy Observation Monitoring System) and application (Onshore and Offshore). Geographic coverage includes major regions—North America, Europe, Asia‑Pacific, Middle East, and Africa. Limitations stem from the reliance on the supplied financial figures; thus, detailed regional revenue breakdowns and market‑share percentages beyond the provided data are not disclosed.

19. Key Companies and Recent Developments in the Oceanographic Monitoring System Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

AXYS Technologies Inc. recently launched a modular sensor suite designed for rapid deployment on offshore wind turbines. GOST Global announced a strategic partnership with a satellite communications provider to enable low‑latency data links for deep‑sea buoys. Hitachi Zosen Corporation introduced a hybrid vessel‑mounted monitoring platform that combines acoustic sensors with autonomous navigation. Xylem expanded its buoy portfolio with a solar‑powered, AI‑enabled surface platform for coastal water‑quality monitoring. Sonardyne released an upgraded acoustic modem that doubles communication range while reducing power consumption, catering to long‑duration deep‑water missions. These developments illustrate the market’s focus on integration, energy efficiency, and data intelligence.