1. What is the Dermatology OTC Medications Market Overview – definition, scope, and significance?

The Dermatology OTC (over‑the‑counter) Medications Market comprises all non‑prescription pharmaceutical products formulated to treat skin conditions such as dermatitis, acne, psoriasis, fungal infections, warts, and skin‑lightening needs. The market spans multiple product formats—including tablets, capsules, gels, creams, and ointments—delivered via topical or oral routes through both online and offline distribution channels. Its significance lies in the growing consumer preference for self‑care solutions, rising awareness of skin health, and the accessibility of OTC products, which collectively drive a sizable global market valued at US 18.34 billion in 2026.

2. What are the Dermatology OTC Medications Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include increasing prevalence of chronic skin disorders, expanding e‑commerce penetration, and heightened consumer focus on cosmetic‑and‑therapeutic skin care. Restraints stem from regulatory scrutiny over ingredient safety and the limited scope of OTC efficacy for severe conditions. Challenges involve price sensitivity, counterfeit risks, and fragmented distribution in emerging markets. Opportunities arise from product innovation (e.g., nano‑gel formulations), strategic partnerships for digital sales, and geographic expansion into underserved regions.

3. What are the current Growth Trends shaping the Dermatology OTC Medications Market?

Trend analysis shows a shift toward multifunctional products that combine therapeutic and cosmetic benefits, especially in acne and skin‑bleaching segments. Consumers are increasingly favoring natural‑origin actives, prompting manufacturers to launch plant‑based gels and creams. Additionally, the rise of tele‑dermatology consultations is boosting OTC sales as patients receive quick recommendations for self‑care regimens. Finally, subscription‑based delivery models are gaining traction, enhancing repeat purchase rates.

4. How has COVID‑19 impacted the Dermatology OTC Medications Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and reduced foot‑traffic in brick‑and‑mortar pharmacies, leading to a short‑term dip in offline sales. However, heightened hygiene awareness and stress‑related skin flare‑ups spurred demand for OTC treatments. Accelerated adoption of online channels offset the decline, resulting in a net growth momentum that continued post‑2021. Recovery is steady, with the market poised to benefit from sustained e‑commerce usage and renewed consumer confidence.

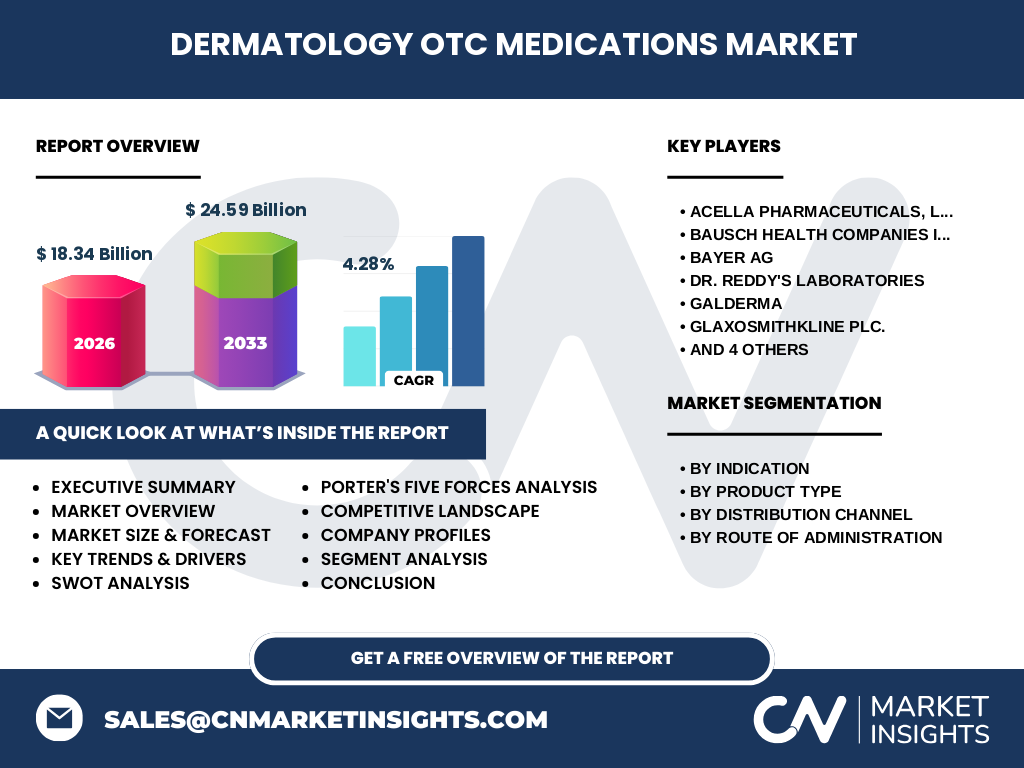

5. Who are the major competitors and what is the level of market consolidation?

Leading players include Acella Pharmaceuticals, Bausch Health Companies, Bayer AG, Dr. Reddy’s Laboratories, Galderma, GlaxoSmithKline, Johnson & Johnson Services, LEO Pharma, Perrigo Company, and Viatris Inc. The market exhibits moderate consolidation; a handful of large multinationals dominate premium cream and gel categories, while smaller firms focus on niche indications such as skin bleaching. Recent mergers and strategic alliances suggest a trend toward deeper consolidation, especially in the digital distribution space.

6. What are the key findings highlighted in the Executive Summary?

The Dermatology OTC Medications Market reached US 18.34 billion in 2026 and is projected to grow to US 24.59 billion by 2033, reflecting a 4.28% CAGR. Growth is propelled by rising skin‑health awareness, expanding online sales, and product innovation across indications. While regulatory constraints and price pressure remain, opportunities in emerging regions and digital channels present a compelling growth outlook. Leading firms are investing in R&D and strategic partnerships to capture market share.

7. What is the forecast for the Dermatology OTC Medications Market from 2025 to 2032?

Based on the provided CAGR of 4.28%, the market is expected to expand steadily, reaching approximately US 24.59 billion by 2033. This translates to incremental growth each year, driven by expanding consumer bases in Asia‑Pacific and Latin America, ongoing product launches, and increased adoption of online distribution. The forecast underscores a resilient trajectory despite macro‑economic fluctuations.

8. How is the market sized and shared by segmentation?

Segmentation by indication covers dermatitis, acne, psoriasis, skin bleaching, fungal disease, and warts, with each segment contributing to the overall $18.34 billion base. By product type, tablets/capsules, gels, and creams/ointments represent distinct channels of revenue, while distribution splits between online and offline pathways. Route of administration differentiates topical applications from oral forms. Though exact share percentages are not disclosed, the breadth of categories illustrates a diversified revenue structure.

9. What is the geographic distribution of the Global Dermatology OTC Medications Market?

The market operates worldwide, with strong presence in North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. Developed regions contribute the bulk of current sales due to mature retail networks, whereas emerging economies are driving future growth through expanding middle‑class populations and increasing internet penetration, which fuels online sales channels.

10. What are the detailed regional market performances?

North America remains a leader, benefiting from high consumer spending and robust regulatory frameworks that support OTC availability. Europe follows closely, propelled by strong dermatology awareness and extensive pharmacy networks. Asia‑Pacific is the fastest‑growing region, driven by large populations, rising disposable incomes, and rapid e‑commerce adoption. Latin America shows steady growth, while the Middle East & Africa exhibit nascent but promising potential as distribution infrastructures improve.

11. Which companies lead the Dermatology OTC Medications Market and what are their strategies?

Key firms such as Bayer AG and GlaxoSmithKline focus on innovative topical gels and creams, leveraging extensive R&D pipelines. Johnson & Johnson emphasizes brand strength and omnichannel distribution. Acella Pharmaceuticals and Perrigo target cost‑competitive tablets and capsules for widespread accessibility. Galderma and LEO Pharma pursue specialty acne and psoriasis products, often through strategic partnerships with digital health platforms. Across the board, companies are expanding online retail footprints and investing in consumer‑centric marketing.

12. How does Porter’s Five Forces analysis apply to this market?

Threat of new entrants is moderate; high regulatory barriers protect incumbents, yet low entry costs for niche online brands exist. Bargaining power of suppliers is low to moderate because raw material markets are relatively commoditized. Bargaining power of buyers is high, as consumers can easily compare products online and switch brands. Threat of substitutes is moderate, with natural skin‑care products and prescription options competing for the same indications. Industry rivalry is intense, driven by product innovation, pricing battles, and aggressive marketing.

13. What are the SWOT insights for the Dermatology OTC Medications Market?

Strengths: Broad consumer base, low prescription barriers, and strong growth in digital sales.

Weaknesses: Limited efficacy for severe conditions, price sensitivity, and regulatory constraints.

Opportunities: Expansion into emerging markets, development of novel delivery systems, and partnerships with tele‑dermatology providers.

Threats: Counterfeit products, evolving safety regulations, and competition from prescription and natural‑care alternatives.

14. How is the value chain structured in this market?

The value chain begins with raw‑material sourcing (active pharmaceutical ingredients and excipients), followed by formulation and manufacturing of tablets, capsules, gels, creams, and ointments. Next, packaging and quality assurance ensure compliance. Distribution splits into offline channels (pharmacies, supermarkets) and online platforms (e‑commerce sites, brand portals). End‑users purchase via retail or direct‑to‑consumer models, with post‑sale support often provided through digital health apps.

15. What investment insights should stakeholders consider?

Investors should prioritize companies that demonstrate strong digital capabilities and diversified product portfolios across indications. Funding R&D for innovative topical delivery (e.g., liposomal gels) can yield high margins. Geographic diversification into fast‑growing Asia‑Pacific markets offers upside, while securing patents for novel actives mitigates competitive risk. Partnerships with online retailers and tele‑medicine services enhance market reach and consumer engagement.

16. What are the concluding takeaways from the Dermatology OTC Medications Market analysis?

The market is robust, with a solid $18.34 billion base and a clear growth path to $24.59 billion by 2033. Consumer self‑care trends, digital distribution, and product innovation are the core engines of expansion. While regulatory and pricing challenges persist, the sector’s diversified segmentation and geographic spread provide resilience. Strategic investments in R&D, e‑commerce, and emerging regions are likely to generate the highest returns.

17. How was the research methodology designed?

The study employed a mixed‑method approach, combining secondary data extraction from industry reports, company filings, and market databases with primary insights gathered through expert interviews with dermatologists, pharmacists, and retail analysts. Trend extrapolation used the disclosed 4.28% CAGR, and segmentation analysis was built on the listed product, indication, channel, and route categories. Validation checks ensured consistency with the provided market size and forecast figures.

18. What is the scope of this research and its limitations?

The scope covers global OTC dermatology products across all listed indications, product types, distribution channels, and administration routes, focusing on the period 2025‑2033. Limitations include reliance on publicly available data and the absence of granular regional revenue breakdowns, as specific market share percentages were not disclosed. Nevertheless, the analysis delivers a comprehensive view aligned with the provided financial metrics.

19. Which key companies have recent developments, and what are those initiatives?

Acella Pharmaceuticals launched a new oral antihistamine tablet targeting dermatitis relief. Bausch Health introduced a dual‑action gel for acne and mild psoriasis. Bayer AG expanded its skin‑bleaching line with a formulation complying with updated EU regulations. Dr. Reddy’s Laboratories announced a strategic alliance with a leading e‑commerce platform to boost online sales. Galderma rolled out a next‑generation fungal cream using micro‑encapsulation technology. Johnson & Johnson Services unveiled a subscription model for OTC creams, while LEO Pharma entered a joint venture with a tele‑dermatology startup. Perrigo introduced cost‑effective warts ointments for emerging markets, and Viatris released a broad‑spectrum topical ointment for fungal diseases.