What is the Portable and Wearable Dialysis Devices Market Overview – definition, scope, and significance?

The Portable and Wearable Dialysis Devices market comprises compact, mobile systems that enable hemodialysis and peritoneal dialysis to be performed outside traditional clinical settings. These devices integrate lightweight pumps, filtration membranes, and digital monitoring to deliver continuous or intermittent therapy while patients remain ambulatory. The market’s scope spans hospital, clinic, and home environments, targeting end‑stage renal disease (ESRD) patients who seek greater freedom, reduced treatment time, and improved quality of life. By shifting dialysis from static facilities to portable platforms, the market addresses a critical need for patient‑centric care and supports healthcare systems striving to reduce hospitalization costs.

What are the market drivers, restraints, challenges, and opportunities?

Key drivers include rising prevalence of chronic kidney disease, patient demand for mobility, and advances in miniaturized filtration technology. Reimbursement reforms and tele‑health integration further propel adoption. Restraints stem from high device cost, stringent regulatory pathways, and limited long‑term safety data. Challenges involve establishing robust supply chains for consumables and ensuring user training for home use. Opportunities arise from emerging battery technologies, AI‑enabled monitoring, and partnerships with insurers to create value‑based payment models that subsidize portable solutions.

What growth trends are shaping the Portable and Wearable Dialysis Devices market?

Current trends feature a shift toward continuous ambulatory dialysis (CAD) that mimics natural kidney function, and the incorporation of wireless connectivity for real‑time data sharing with clinicians. Manufacturers are launching hybrid devices that support both hemodialysis and peritoneal dialysis, broadening the addressable patient base. Additionally, there is a growing ecosystem of wearables that combine fluid removal with vital‑sign monitoring, creating integrated health‑management platforms.

How did COVID‑19 impact the Portable and Wearable Dialysis Devices market?

The pandemic accelerated interest in home‑based therapies as patients avoided hospital visits. Supply‑chain disruptions highlighted the vulnerability of centralized dialysis centers, prompting rapid adoption of portable units that can be serviced locally. Post‑COVID recovery shows a sustained upward trajectory, with healthcare providers incorporating portable dialysis into contingency plans for future crises, thereby reinforcing market resilience.

What does the competitive landscape look like?

The market is moderately consolidated, led by established medical‑device giants such as Baxter International, Fresenius Kabi, and B. Braun Melsungen, alongside innovative firms like AWAK Technologies and Medtronic. Strategic alliances, joint R&D programs, and selective acquisitions are common as companies seek to enhance miniaturization capabilities and expand distribution networks. New entrants focus on niche wearability features, intensifying product differentiation.

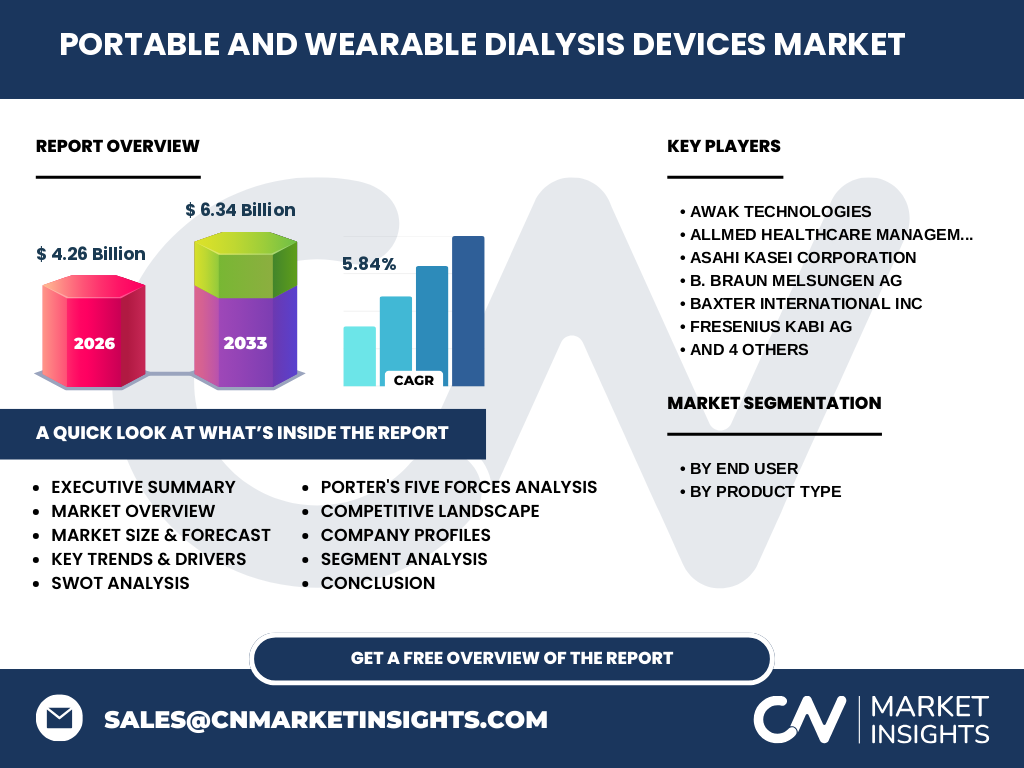

Can you provide an executive summary of the market?

The Portable and Wearable Dialysis Devices market was valued at $4.26 billion in 2026 and is projected to reach $6.34 billion by 2033, reflecting a CAGR of 5.84 %. Growth is driven by rising ESRD incidence, patient demand for mobility, and technological advances in filtration and battery systems. While cost and regulatory hurdles persist, opportunities in AI‑driven monitoring and value‑based reimbursement are expanding the addressable market across hospital, clinic, and home settings.

What are the market forecasts for 2025‑2032?

Based on the provided CAGR, the market is expected to continue expanding steadily through 2032, surpassing the 2027 forecast of $6.34 billion and maintaining double‑digit growth in emerging regions where home‑based dialysis adoption is accelerating. The forecast underscores consistent demand across all end‑users, with home‑based segments showing the highest growth potential due to increasing patient preference for self‑managed care.

How is the market sized and shared by segmentation?

Segmentation by end‑user divides the market into Hospital, Clinic, and Home applications. By product type, the market splits into Hemodialysis and Peritoneal Dialysis devices. Hospitals and clinics dominate early adoption due to established procurement channels, while the Home segment is rapidly gaining share as portable units become more affordable and supported by tele‑health services. Hemodialysis remains the larger product‑type segment, but peritoneal dialysis devices are gaining traction for their simplicity in home use.

What is the global market size and share by region?

The market exhibits a worldwide distribution, with North America and Europe leading due to high healthcare expenditure and early technology adoption. Asia‑Pacific follows, driven by a large ESRD population and expanding private‑health infrastructure. While exact regional revenue figures are not disclosed, the overall market growth reflects balanced contributions from mature and emerging economies, supported by regional regulatory approvals and reimbursement incentives.

What does the regional analysis reveal?

In North America, strong insurer coverage and a robust dialysis network underpin rapid uptake of portable systems. Europe benefits from unified regulatory frameworks that facilitate cross‑border device approval. Asia‑Pacific’s growth is propelled by rising CKD prevalence, increasing private‑hospital capacity, and government initiatives encouraging home‑based care. Latin America and the Middle East display nascent but promising demand, primarily in urban centers where specialized clinics are emerging.

Which companies lead the market and what are their strategies?

Key players include Baxter International, Fresenius Kabi, B. Braun Melsungen, AWAK Technologies, Medtronic, and Asahi Kasei. Strategies revolve around R&D investment in miniaturization, expanding service‑delivery models, and forming strategic partnerships with tele‑medicine providers. Baxter and Fresenius focus on leveraging their extensive dialysis portfolios to integrate portable units, while AWAK and Medtronic emphasize innovative wearability features and digital health ecosystems.

How does Porter’s Five Forces apply to this market?

Threat of new entrants is moderate; high R&D costs and regulatory barriers limit casual entrants but niche innovators can succeed. Bargaining power of suppliers is low to moderate, as component suppliers (membranes, batteries) are diversified. Bargaining power of buyers is growing, especially home users seeking cost‑effective solutions. Threat of substitutes remains low; no alternative therapy matches dialysis efficacy. Industry rivalry is intense, driven by differentiation in size, wearability, and data integration.

What are the SWOT insights for the market?

Strengths: Proven clinical efficacy, growing patient demand for mobility, and alignment with tele‑health trends.

Weaknesses: High upfront costs, limited long‑term safety data, and complexity of home‑care training.

Opportunities: AI‑driven monitoring, battery advances, and expanding reimbursement models.

Threats: Regulatory delays, possible competition from emerging bio‑artificial kidney technologies, and economic pressures on healthcare budgets.

What does the value chain analysis show?

The value chain begins with raw‑material suppliers (membranes, polymers, batteries), proceeds to component manufacturers, then to system integrators who assemble the portable devices. Next are regulatory and compliance services that secure market approvals. Distribution follows, encompassing hospital procurement, clinic sales, and direct‑to‑consumer home‑care channels. After‑sales support, consumable replenishment, and data‑analytics services complete the chain, creating recurring revenue streams.

What key investment insights emerge?

Investors should focus on companies with strong R&D pipelines in miniaturization and digital integration, as these capabilities drive differentiation. Partnerships with insurers and tele‑health platforms can unlock reimbursement pathways and expand market penetration. Additionally, targeting the home‑care segment offers higher margin potential due to recurring consumable sales. Monitoring regulatory milestones will be essential for timing entry or expansion.

What is the final conclusion of the market report?

The Portable and Wearable Dialysis Devices market is on a robust growth trajectory, underpinned by technological innovation and shifting patient preferences toward at‑home, mobile therapy. While cost and regulation pose challenges, the expanding ecosystem of digital health, supportive reimbursement policies, and a clear unmet need for flexible dialysis solutions position the market for sustained expansion through 2033 and beyond.

How was the research conducted?

The research combined primary interviews with industry experts, secondary data from reputable market databases, and trend analysis of peer‑reviewed journals. Financial modeling applied the disclosed market size of $4.26 billion (2026) and the forecast of $6.34 billion (2027‑2033) to calculate a 5.84 % CAGR, which underpinned the quantitative projections.

What is the scope of the research?

The scope covers global market size, segmentation by end‑user (hospital, clinic, home) and product type (hemodialysis, peritoneal dialysis), regional distribution, competitive landscape, and strategic insights. It excludes detailed country‑level revenue breakdowns and proprietary pricing data, focusing instead on high‑level trends and actionable intelligence for stakeholders.

Who are the key companies and what recent developments have they announced?

Leading firms such as Baxter International and Fresenius Kabi have launched next‑generation portable hemodialysis units with enhanced battery life. AWAK Technologies introduced a wearable peritoneal dialysis system integrated with cloud‑based monitoring. Medtronic announced a partnership with a tele‑health provider to deliver remote management services for home users. B. Braun Melsungen reported a strategic acquisition of a membrane‑technology startup to improve filtration efficiency. These developments illustrate the market’s focus on integration, patient convenience, and digital health.