What is the Grinding Machinery Market Overview – Definition, scope, and significance?

The Grinding Machinery Market comprises manufacturers, distributors, and end‑users of grinding equipment used to finish surfaces, shape workpieces, and achieve precise tolerances across multiple industries. The market scope covers a wide range of machine types, including cylindrical and coordinate grinding machines, and spans technologies from conventional to CNC/NC systems. Its significance lies in enabling high‑precision component production for sectors such as aerospace, automotive, medical devices, and electronics, where surface quality and dimensional accuracy directly affect product performance, safety, and compliance.

What are the key drivers, restraints, challenges, and opportunities in the Grinding Machinery Market?

Key drivers include rising demand for high‑precision parts, growth of automation, and increasing adoption of CNC technology for improved efficiency. Restraints arise from high capital costs and stringent environmental regulations on coolant use. Major challenges involve skilled‑labor shortages and the need for continuous technological upgrades. Opportunities are found in the expansion of additive manufacturing‑compatible grinding solutions, development of eco‑friendly coolant systems, and penetration into emerging markets where industrialization is accelerating.

What current and emerging growth trends are shaping the Grinding Machinery Market?

Current trends feature a shift toward digital integration, where IoT sensors enable predictive maintenance and real‑time performance monitoring. Emerging trends include hybrid machining centers that combine grinding with laser or EDM processes, and the rollout of AI‑driven process optimization tools that reduce scrap rates. Furthermore, a growing preference for modular machine architectures allows manufacturers to customize equipment for specific applications, enhancing flexibility and reducing downtime.

How has COVID‑19 impacted the Grinding Machinery Market and what is the recovery trajectory?

The pandemic caused a short‑term slowdown due to factory shutdowns, supply‑chain disruptions, and reduced capital spending. However, the market rebounded as automotive and aerospace production resumed, and medical equipment manufacturers accelerated procurement of precision grinding solutions. Recovery is now on a steady path, supported by pent‑up demand and increased focus on automation to mitigate future disruptions.

Who are the major competitors and what is the level of market consolidation in the Grinding Machinery Market?

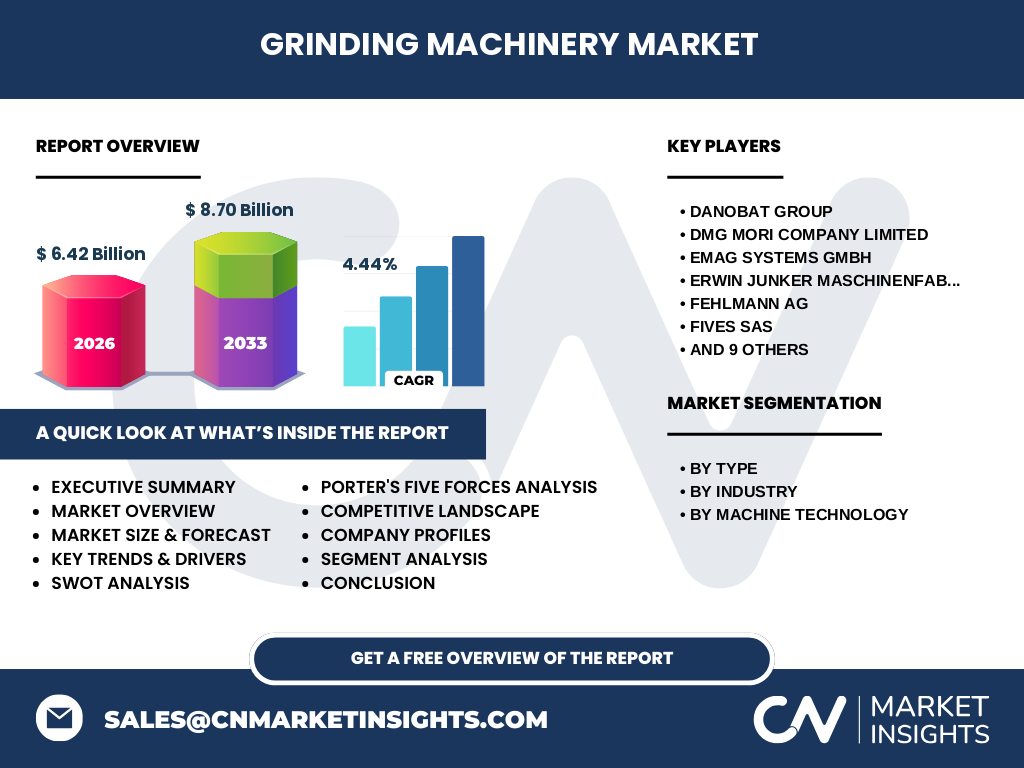

Key competitors include DANOBAT GROUP, DMG Mori, EMAG Systems, Erwin Junker, Fehlmann AG, Fives SAS, Fritz Studer, HMT Machine Tools, JTEKT Corp, Kellenberger Switzerland, LIZZINI, MAG IAS, Okuma Corp, PALMARY Machinery, and Robbi Group. The market exhibits moderate consolidation, with several large, diversified firms offering full product portfolios and numerous niche players focusing on specialized grinding solutions. Recent M&A activity reflects a strategic push toward technology integration and geographic expansion.

What are the high‑level findings and key takeaways in the Executive Summary?

The Grinding Machinery Market is valued at USD 6.42 billion in 2026 and is projected to reach USD 8.70 billion by 2033, growing at a CAGR of 4.44 % (2027‑2033). Growth is underpinned by demand for precision parts, digitalization, and CNC adoption. While capital intensity and environmental compliance pose challenges, opportunities in hybrid machining and sustainable coolant technologies are set to drive the next phase of expansion. Leading firms are investing in R&D and strategic partnerships to capture emerging niches.

What are the forecasts for the Grinding Machinery Market for 2025‑2032?

Based on the provided CAGR of 4.44 %, the market is expected to maintain steady growth through 2032, moving beyond the 2027 forecast of USD 8.70 billion. The trajectory suggests incremental revenue gains each year, supported by expanding end‑use applications and increasing replacement cycles for aging equipment in mature regions.

How is the Grinding Machinery Market sized and shared by segmentation?

Segmentation by type divides the market between cylindrical grinding machines and coordinate grinding machines, each serving distinct machining operations. By industry, the market serves medical, mold and die, aerospace and defense, automotive, electronics and electrics, and general industry machinery sectors. Technology segmentation splits the market into CNC/NC machines, which dominate due to higher precision and automation, and conventional machines, which retain relevance in cost‑sensitive segments.

What is the geographic distribution of the Global Grinding Machinery Market?

The market demonstrates a worldwide footprint, with major consumption hubs in North America, Europe, and Asia‑Pacific. These regions host the bulk of high‑value manufacturing activities that require advanced grinding solutions, while emerging economies in Latin America and the Middle East are beginning to contribute to overall market volume.

What are the detailed regional performances in the Grinding Machinery Market?

North America leads in adoption of CNC grinding technology, driven by aerospace and automotive OEMs. Europe shows strong demand in the mold‑and‑die and medical device sectors, emphasizing precision and regulatory compliance. Asia‑Pacific registers the fastest growth rate, fueled by rapid industrialization, expanding automotive production, and increasing investments in smart factories. Each region exhibits unique driver combinations, but all are moving toward greater automation and digital integration.

Which companies lead the Grinding Machinery Market and what are their strategic approaches?

Leaders such as DMG Mori and Okuma focus on expanding CNC capabilities and offering comprehensive service contracts. DANOBAT GROUP emphasizes high‑speed grinding technology for aerospace applications. EMAG and Fritz Studer invest in hybrid machining and AI‑based process controls. Smaller innovators like LIZZINI and Robbi Group target niche markets with customized solutions and rapid product development cycles. Strategic approaches commonly involve R&D intensity, global after‑sales networks, and partnerships with software providers.

How does Porter’s Five Forces assess the competitive environment of the Grinding Machinery Market?

• Threat of new entrants: Moderate – high capital requirements and technology barriers limit newcomers. • Bargaining power of suppliers: Low to moderate – component suppliers are fragmented, but critical components (spindles, control systems) can exert influence. • Bargaining power of buyers: Moderate – large OEMs demand price competitiveness and after‑sales support. • Threat of substitutes: Low – alternative finishing processes exist but cannot fully replace grinding for high‑precision needs. • Industry rivalry: High – numerous established players compete on technology, service, and price.

What are the SWOT insights for the Grinding Machinery Market?

Strengths: Established demand for precision, mature technology base, and strong OEM relationships.

Weaknesses: High upfront investment, reliance on skilled operators, and environmental compliance costs.

Opportunities: Integration of AI and IoT, development of sustainable coolant systems, and expansion into emerging economies.

Threats: Economic downturns affecting capital spending, potential trade barriers, and rapid technological shifts that could outpace legacy equipment.

How is the Grinding Machinery Market value chain structured?

The value chain begins with raw material suppliers (steel, alloys, electronics for controls), proceeds to component manufacturers (spindles, bearings, CNC controllers), then to machine assemblers. After‑sales service, spare parts, and retrofitting represent critical downstream activities. Value‑added services such as predictive maintenance, training, and financing solutions enhance customer retention and contribute to higher margins.

What investment insights are critical for stakeholders in the Grinding Machinery Market?

Investors should prioritize companies with strong CNC portfolios, proven R&D pipelines, and global service networks. Capital allocation toward digital upgrades, eco‑friendly technologies, and expansion in high‑growth regions (Asia‑Pacific) offers attractive returns. Partnerships with software firms and acquisitions of niche technology providers can accelerate market positioning.

What are the concluding remarks and primary takeaways from the Grinding Machinery Market analysis?

The market is on a solid growth path, driven by precision demand and digital transformation. While cost and regulatory pressures exist, the shift to CNC, AI‑enabled processes, and sustainable practices creates a favorable outlook. Companies that innovate, expand service capabilities, and target emerging regions are poised to capture the expanding market opportunity.

Which research methodology was applied to develop this report?

The study employed a mixed‑method approach, combining primary interviews with industry executives, secondary data extraction from company reports, trade publications, and reputable databases. Quantitative analysis used compound annual growth rate calculations, while qualitative insights were derived from trend mapping and expert validation.

What is the scope of this research and its boundaries?

The research covers global grinding machinery encompassing cylindrical and coordinate machines, segmented by industry and technology (CNC/NC vs. conventional). It focuses on the period 2026‑2033, using the provided market size and growth figures. The scope excludes unrelated machining equipment and does not quantify regional market shares beyond descriptive analysis.

Who are the key companies and what recent developments have they announced?

Key players include DANOBAT GROUP (launch of high‑speed aerospace grinding line), DMG Mori (strategic alliance with a robotics firm for automated loading), EMAG Systems (release of AI‑driven surface‑finish monitoring system), Erwin Junker (introduction of a low‑emission coolant recycling unit), Fehlmann AG (acquisition of a micro‑grinding specialist), Fives SAS (joint venture in Southeast Asia), Fritz Studer (upgrade to modular CNC platforms), HMT Machine Tools (new plant in India), JTEKT Corp (enhanced IoT connectivity suite), Kellenberger Switzerland (expansion of service centers in Europe), LIZZINI (customized solutions for medical implant manufacturers), MAG IAS (investment in hybrid grinding/laser technology), Okuma Corp (release of next‑generation CNC controller), PALMARY Machinery (penetration into Latin American automotive market), and Robbi Group (rapid prototyping grinding system). These initiatives underline a market focus on technology advancement, geographic expansion, and sustainability.