What is the In-Mold Electronics Market Overview – Definition, scope, and significance?

The In‑Mold Electronics (IME) market encompasses technologies that embed electronic components directly into polymeric parts during the molding process. By integrating conductive inks—such as silver or carbon—into plastic molds, manufacturers can create fully functional, sealed electronic systems without additional assembly steps. The scope of IME spans a wide range of end‑uses, from automotive sensors to wearable health monitors, delivering advantages in miniaturization, durability, and cost‑effectiveness. Its significance lies in enabling “smart” plastics that combine mechanical performance with real‑time data acquisition, supporting the broader trend toward the Internet of Things (IoT) and advanced automation.

What are the primary drivers, restraints, challenges, and opportunities in the In-Mold Electronics Market?

Key drivers include rapid IoT adoption, the demand for lightweight and rugged electronics in automotive and aerospace, and the cost savings from reduced part count and assembly labor. Opportunities arise from emerging applications in healthcare wearables and building automation, where embedded sensing can enhance safety and efficiency. Restraints stem from the high initial tooling costs and the need for specialized conductive inks. Technical challenges involve maintaining ink conductivity under high temperature molding conditions and ensuring long‑term reliability. Overcoming these hurdles through ink formulation advances and standardization can unlock further market growth.

What are the current and emerging growth trends shaping the In-Mold Electronics Market?

Current trends feature the shift from discrete sensors to fully integrated IME modules, particularly in electric vehicles where embedded temperature and pressure sensors reduce wiring complexity. Emerging trends include the use of biodegradable polymers with conductive inks for sustainable consumer products, and the development of flexible IME components for next‑generation wearables. Collaboration between ink manufacturers and mold designers is accelerating rapid prototyping, allowing faster time‑to‑market for custom IME solutions.

How has COVID‑19 impacted the In-Mold Electronics Market and what is the recovery trajectory?

The pandemic temporarily disrupted supply chains for specialty inks and mold tooling, leading to a short‑term slowdown in new IME projects. However, the accelerated digitization of manufacturing and the increased focus on remote health monitoring created renewed demand for embedded sensors. As global factories resumed operations, the market entered a strong recovery phase, supported by renewed automotive production volumes and heightened investment in smart infrastructure. This rebound laid the groundwork for the robust growth forecast observed post‑2022.

Who are the major competitors and what is the state of market consolidation in the In-Mold Electronics Market?

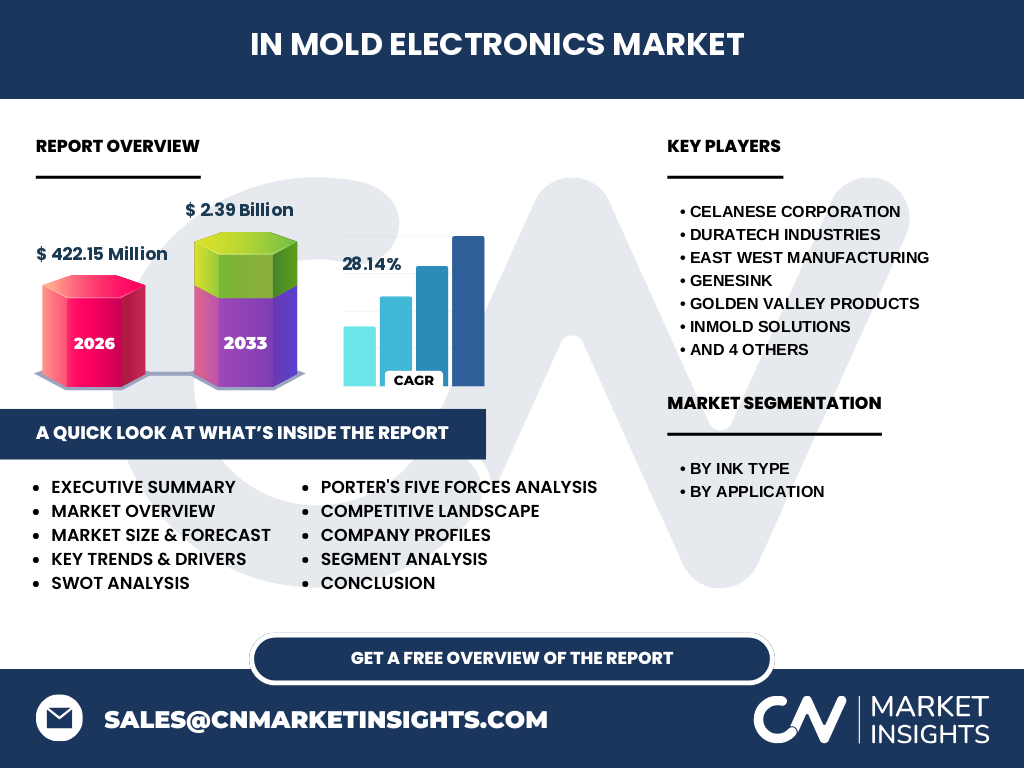

Key players include Celanese Corporation, DuraTech Industries, East West Manufacturing, GenesInk, Golden Valley Products, InMold Solutions, Nissha Co., Ltd., TactoTek Oy, YOMURA, and e 2 ip. The competitive landscape is characterized by a mix of large chemical firms with extensive ink portfolios and niche specialists focused on precision molding services. Recent years have seen strategic partnerships rather than outright mergers, indicating a collaborative consolidation pattern aimed at combining ink technology with molding expertise.

What are the high‑level findings in the Executive Summary for the In-Mold Electronics Market?

The In‑Mold Electronics market is projected to expand from a 2026 size of USD 422.15 million to USD 2.39 billion by 2033, delivering a compound annual growth rate (CAGR) of 28.14 %. Growth is driven by strong demand across automotive, consumer, and healthcare segments, with silver conductive ink leading application due to its superior conductivity. Regional adoption is accelerating in North America and Asia‑Pacific, while Europe remains a hub for standards development. The market’s value chain is becoming more integrated, with ink suppliers, mold manufacturers, and end‑user designers forming close alliances.

What are the market forecasts for the In-Mold Electronics Market from 2025 to 2032?

Based on the provided CAGR of 28.14 %, the market is expected to maintain double‑digit expansion throughout the 2025‑2032 horizon. By 2028 the market is anticipated to surpass the USD 1 billion mark, and by 2032 it will approach the upper end of the forecast range, near USD 2 billion. This trajectory reflects continued penetration of IME in high‑volume automotive components, growing adoption in smart building solutions, and the rise of personalized healthcare devices that rely on embedded sensors.

How is the In-Mold Electronics Market sized and shared by segment?

The market is segmented by ink type and application. By ink type, two primary categories exist: Silver Conductive Ink and Carbon Conductive Ink. Silver ink commands a larger share due to its high electrical performance, particularly in automotive and consumer electronics. Carbon ink serves niche markets where cost and flexibility are prioritized, such as building automation and some wearable devices. By application, the market is split among Automotive, Building Automation, Consumer Products, Wearable, and Healthcare. Automotive currently represents the largest application segment, driven by embedded sensor requirements for safety and efficiency. Healthcare and Wearable segments are the fastest growing, reflecting the surge in remote monitoring and personalized health tech.

What is the geographic distribution of the Global In-Mold Electronics Market?

The global market is broadly distributed across North America, Europe, Asia‑Pacific, and the Rest of the World. North America leads in early adoption, supported by advanced automotive OEMs and a strong ecosystem of ink suppliers. Asia‑Pacific follows closely, propelled by large‑scale manufacturing capabilities in China, Japan, and South Korea, and substantial investments in smart factory initiatives. Europe maintains a solid presence due to stringent automotive safety standards and active research consortia. While exact share percentages are not disclosed, the combined growth of these regions underpins the overall market expansion.

What are the detailed regional performance insights for the In-Mold Electronics Market?

In North America, the market benefits from government incentives for lightweight electric vehicles and a mature consumer electronics sector. The United States accounts for the majority of regional sales, with Canada contributing through niche medical device applications. In Europe, Germany and France drive demand through automotive electronics, while the United Kingdom focuses on building automation solutions. The Asia‑Pacific region showcases the highest growth rate, thanks to mass production of automotive components in China and Japan’s leadership in wearable technology development. Emerging markets in Southeast Asia are beginning to adopt IME for cost‑effective smart home devices.

Which companies lead the In-Mold Electronics Market and what are their strategic approaches?

Celanese Corporation leverages its polymer expertise to develop high‑performance conductive inks, targeting automotive OEMs. DuraTech Industries focuses on rugged IME solutions for industrial automation. East West Manufacturing offers full‑service molding and integration, enabling rapid prototyping for consumer product developers. GenesInk specializes in carbon‑based inks, positioning itself for low‑cost building automation projects. Golden Valley Products concentrates on custom ink formulations for healthcare wearables. InMold Solutions provides turnkey IME design services, fostering collaborations with electronics designers. Nissha Co., Ltd. integrates its sensor technologies directly into molded components for Japanese automotive suppliers. TactoTek Oy, YOMURA, and e 2 ip each emphasize niche innovations, such as flexible substrates and IoT connectivity modules.

How does Porter’s Five Forces analysis apply to the In-Mold Electronics Market?

Threat of New Entrants: Moderate. High capital investment for tooling and specialized ink formulation creates barriers, but niche startups can enter via low‑volume, high‑value applications. Bargaining Power of Suppliers: High, as the market relies on a limited number of specialty conductive ink manufacturers, giving them pricing leverage. Bargaining Power of Buyers: Increasing, as large automotive OEMs demand volume discounts and strict quality standards. Threat of Substitutes: Low to moderate; traditional printed circuit boards and discrete sensors remain alternatives, but IME’s integration benefits reduce substitution risk. Competitive Rivalry: Intense, driven by innovation in ink chemistry, molding technology, and strategic partnerships that aim to capture high‑growth segments like wearables and healthcare.

What are the key strengths, weaknesses, opportunities, and threats (SWOT) for the In-Mold Electronics Market?

Strengths: High integration efficiency, reduced assembly cost, and enhanced product durability. Weaknesses: Elevated initial tooling expense and limited availability of standardized ink formulations. Opportunities: Expansion into renewable energy devices, smart packaging, and biodegradable IME components. Threats: Potential supply chain disruptions for rare metals used in silver ink, and regulatory hurdles related to electronic waste handling.

What does the value chain of the In-Mold Electronics Market look like?

The value chain begins with raw material suppliers that provide conductive inks (silver or carbon) and polymer resins. Next, ink formulators develop application‑specific formulations, which are then delivered to mold manufacturers. Mold designers integrate ink dispensing systems into the injection molding equipment, creating the in‑mold electronic components. After molding, testing and quality assurance facilities validate electrical performance and mechanical integrity. Finally, OEMs incorporate the finished IME parts into end products across automotive, consumer, and medical sectors, followed by distribution to end‑users.

What investment insights are essential for stakeholders in the In-Mold Electronics Market?

Investors should prioritize companies with strong ink R&D pipelines, particularly those advancing silver ink conductivity while reducing cost. Partnerships between ink suppliers and high‑volume molders can generate scalable business models. Funding ventures that focus on sustainable IME solutions—such as recyclable polymers and low‑toxicity inks—aligns with emerging ESG criteria and may attract premium financing. Additionally, targeting regions with fast‑growing automotive electrification, like Asia‑Pacific, can yield higher returns.

What are the concluding takeaways from the In-Mold Electronics Market analysis?

The In‑Mold Electronics market is on a rapid ascent, driven by a 28.14 % CAGR and a projected size of USD 2.39 billion by 2033. Core strengths include integration efficiency and applicability across high‑growth sectors. Overcoming tooling costs and ink supply constraints will be crucial. Strategic collaborations, technology differentiation, and geographic focus on automotive‑intensive regions will define market leadership. Stakeholders are positioned to benefit from the convergence of IoT, lightweight design, and smart material trends.

How was the research for this market report conducted?

The research employed a mixed‑method approach, combining primary interviews with industry experts, secondary data review of company reports, trade publications, and market databases, and quantitative modeling based on the supplied market size (USD 422.15 million in 2026) and forecast (USD 2.39 billion for 2027‑2033). Trend analysis, competitive profiling, and scenario planning were applied to derive the forecasts and insights presented.

What is the scope and any limitations of this In-Mold Electronics Market research?

The scope covers global market size, segmentation by ink type and application, regional performance, competitive dynamics, and forward‑looking forecasts to 2033. Limitations include reliance on publicly available data and the absence of proprietary financial disclosures for individual firms, which restricts precise market‑share quantification. Nonetheless, the analysis provides a comprehensive view of market direction and key strategic factors.

Which key companies and recent developments should be noted in the In-Mold Electronics Market?

Celanese Corporation announced a new silver conductive ink line optimized for high‑temperature molding, aimed at electric‑vehicle battery enclosures. DuraTech Industries launched a rugged IME sensor platform for industrial IoT gateways. GenesInk introduced a cost‑effective carbon ink for smart building sensors, partnering with a major HVAC manufacturer. Nissha Co., Ltd. released an integrated pressure sensor embedded in automotive seat moldings, enhancing occupant safety features. TactoTek Oy secured a joint venture with a wearable startup to produce flexible IME patches for continuous health monitoring. These developments illustrate the market’s momentum and the strategic focus on application‑specific innovations.