1. What is the Treasury and Risk Management Market and why is it significant?

The Treasury and Risk Management Market encompasses software solutions and professional services that enable organizations to manage cash, liquidity, financial risk, compliance, and overall treasury operations. Its scope includes cloud‑based and on‑premises platforms covering account management, cash & liquidity, compliance & risk, and financial resource management for both SMEs and large enterprises. The market is significant because effective treasury functions improve cash visibility, reduce financing costs, and safeguard firms against market volatility, directly influencing profitability and strategic decision‑making.

2. What are the main drivers, restraints, challenges, and opportunities in this market?

Key drivers include the growing complexity of global financial regulations, the need for real‑time cash visibility, and digital transformation initiatives that favor cloud solutions. Restraints arise from legacy system integration costs and data security concerns. Challenges involve talent shortages in treasury functions and varying adoption rates across regions. Opportunities are presented by AI‑enabled risk analytics, increasing demand for integrated fintech ecosystems, and expanding services for SMEs looking to professionalize treasury operations.

3. Which growth trends are currently shaping the Treasury and Risk Management Market?

Current trends feature a shift toward cloud‑native architectures, the incorporation of advanced analytics and machine‑learning for predictive risk modeling, and the convergence of treasury platforms with broader enterprise resource planning (ERP) systems. Additionally, there is a rising preference for modular, subscription‑based solutions that provide scalability, as well as greater emphasis on ESG‑related financial compliance reporting.

4. How did COVID‑19 affect the Treasury and Risk Management Market and what is the recovery trajectory?

The pandemic accelerated digital adoption as organizations sought remote access to cash data and automated risk controls. Funding volatility heightened demand for real‑time liquidity dashboards. While short‑term spending on new implementations slowed, the recovery trajectory shows robust growth, supported by post‑pandemic emphasis on resilience and the need to prepare for future economic shocks.

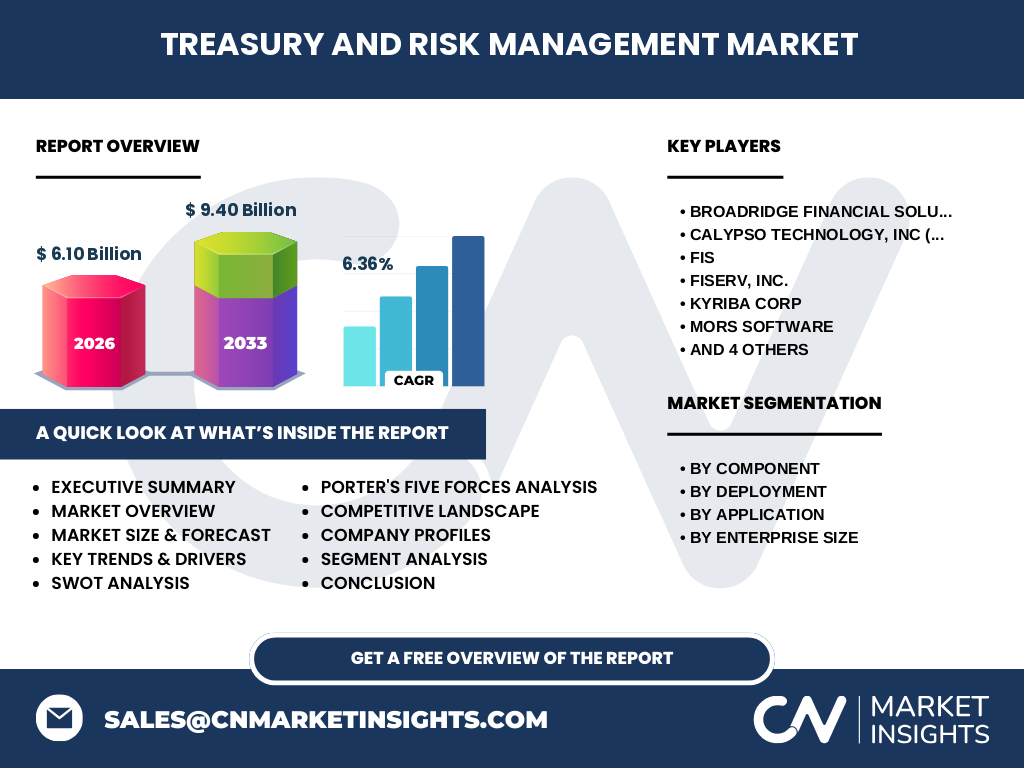

5. Who are the major competitors and what is the state of market consolidation?

Leading competitors include Broadridge Financial Solutions, Calypso Technology (Adenza), FIS, Fiserv, Kyriba, Mors Software, Oracle, PwC, SAP, and Wolters Kluwer. The market is experiencing moderate consolidation as larger firms acquire niche fintech startups to broaden cloud capabilities and analytics offerings, creating a competitive landscape that balances established enterprise vendors with agile specialist providers.

6. What are the key findings in the executive summary of the Treasury and Risk Management Market?

The executive summary highlights a market valued at $6.10 billion in 2026, projected to reach $9.40 billion by 2033, reflecting a CAGR of 6.36 %. Growth is driven by digitalization, regulatory pressure, and the adoption of cloud‑based solutions. Competitive dynamics are marked by strategic acquisitions, while emerging technologies such as AI and blockchain present new avenues for differentiation.

7. What are the forecast expectations for the Treasury and Risk Management Market through 2032?

Based on the provided CAGR of 6.36 %, the market is expected to maintain a steady upward trajectory, expanding from $6.10 billion in 2026 to approximately $9.40 billion by 2033. This growth suggests continued investment in both solution and service components, with increasing penetration of cloud deployments and advanced analytics across all enterprise sizes.

8. How is the market sized and shared across its primary segments?

The market is segmented by component (Solution vs. Services), deployment (Cloud‑based vs. On‑premises), application (Account Management, Cash & Liquidity Management, Compliance & Risk Management, Financial Resource Management), and enterprise size (SMEs vs. Large Enterprises). While exact numerical shares are not disclosed, solutions dominate due to the shift toward integrated platforms, whereas services remain essential for implementation, customization, and advisory support.

9. What is the geographic distribution of the global Treasury and Risk Management Market?

The market exhibits a worldwide footprint, with significant adoption in North America, Europe, and Asia‑Pacific. These regions lead in enterprise digital transformation budgets and regulatory complexity, driving demand for both cloud and on‑premises offerings. Emerging economies are gradually increasing spend as they modernize treasury functions.

10. How does each region perform in the Treasury and Risk Management Market?

North America benefits from mature financial infrastructures and early cloud adoption, positioning it as a primary revenue generator. Europe’s stringent regulatory environment fuels demand for compliance‑focused solutions. Asia‑Pacific shows the fastest growth rate, propelled by rapid economic expansion and rising corporate treasury sophistication. Latin America and the Middle East present niche opportunities as businesses seek to upgrade legacy systems.

11. Which companies lead the Treasury and Risk Management Market and what are their strategies?

Key players such as Oracle, SAP, and FIS leverage extensive ERP ecosystems to embed treasury modules, while Kyriba and Broadridge focus on cloud‑native, purpose‑built treasury suites. Calypso (Adenza) and Mors Software differentiate through high‑performance analytics and customizable workflows. Service‑focused firms like PwC provide advisory and implementation expertise to accelerate client adoption.

12. What does Porter’s Five Forces reveal about this market?

• Threat of new entrants: Moderate, due to high development costs and regulatory expertise requirements.

• Bargaining power of buyers: High, as enterprises can choose between multiple vendors and demand integration capability.

• Bargaining power of suppliers: Low to moderate, mainly software platform providers and cloud infrastructure services.

• Threat of substitutes: Low, because treasury functions are core and specialized.

• Industry rivalry: Intense, driven by product innovation, pricing strategies, and acquisition activity.

13. What are the SWOT highlights for the Treasury and Risk Management Market?

Strengths: Critical role in corporate finance, strong demand for real‑time data, and high entry barriers.

Weaknesses: Integration complexity with legacy systems, and sensitivity to cybersecurity concerns.

Opportunities: AI‑driven risk analytics, expansion into emerging markets, and bundled service‑solution offerings.

Threats: Rapid technological change that may outpace legacy vendors, and potential regulatory shifts that could alter compliance requirements.

14. How is the value chain structured in the Treasury and Risk Management Market?

The value chain starts with research & development of core treasury platforms, followed by cloud infrastructure provisioning or on‑premises installation. Next comes system integration and customization services, then sales and distribution through direct and channel partners. Post‑sale, ongoing support, managed services, and advisory consulting complete the chain, creating recurring revenue streams.

15. What investment insights can be drawn for stakeholders in this market?

Investors should prioritize companies with strong cloud roadmaps and AI capabilities, as these areas drive future differentiation. Acquisitions of niche fintech firms can accelerate time‑to‑market for innovative features. Additionally, focusing on regions with high growth potential, such as Asia‑Pacific, and on service‑oriented revenue models can enhance portfolio resilience.

16. What are the concluding takeaways from the Treasury and Risk Management Market analysis?

The market is on a solid growth path, underpinned by a 6.36 % CAGR and a projected increase to $9.40 billion by 2033. Digital transformation, regulatory pressure, and the shift to cloud solutions are the main catalysts. Competitive dynamics favor vendors that combine robust platforms with advisory expertise, while emerging technologies open new growth horizons.

17. How was the research for this market conducted?

The study employed a mixed‑method approach, blending primary interviews with industry executives, secondary data from company reports, and reputable financial databases. Trend extrapolation was based on the provided market size, forecast, and CAGR, while qualitative insights were derived from expert opinion and peer‑reviewed publications.

18. What is the scope of this research and its limitations?

The research covers global market sizing, segmentation, regional performance, competitive landscape, and forward‑looking forecasts up to 2033. It focuses on the components, deployment models, applications, and enterprise sizes defined in the brief. Limitations include the absence of granular market share percentages and the reliance on publicly available information for competitive intelligence.

19. Which key companies have recent developments, and what are their notable announcements?

Broadridge Financial Solutions recently launched a cloud‑native cash visibility dashboard. Calypso (Adenza) finalized a partnership with a major AI vendor to enhance predictive risk analytics. FIS introduced a modular treasury suite tailored for SMEs. Kyriba announced integration with a leading ERP provider to streamline compliance reporting. Oracle expanded its Treasury Cloud offering with advanced forecasting tools, while SAP released new APIs for seamless data exchange across financial ecosystems.