1. What is the Asia Pacific Aerospace & Defense Power Connector Market Overview – Definition, scope, and significance?

The Asia Pacific Aerospace & Defense Power Connector market comprises connectors that transmit electrical power in aircraft, military ground vehicles, body‑worn equipment, and naval ships. These connectors range from low‑current (5 A) to high‑current (>600 A) configurations and are engineered for rectangular or circular shapes to meet stringent aerospace and defense standards. The market is significant because reliable power distribution is critical for mission‑critical systems, safety, and performance in harsh operational environments across the rapidly expanding Asia Pacific region.

2. What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Aerospace & Defense Power Connector Market?

Key drivers include rising defense budgets, growth in commercial aviation fleets, and increasing adoption of electric propulsion and advanced avionics. Restraints stem from high certification costs and stringent regulatory compliance. Challenges involve supply‑chain disruptions and the need for miniaturization while maintaining high reliability. Opportunities arise from emerging unmanned platforms, integration of smart‑connected sensors, and government initiatives supporting domestic manufacturing of critical aerospace components.

3. What growth trends are currently influencing the Asia Pacific Aerospace & Defense Power Connector Market?

Current trends feature a shift toward high‑current (>150 A) connectors to support electric thrust systems, the adoption of circular connector designs for space‑saving in confined aircraft bays, and the rise of modular connector architectures that enable rapid re‑configuration of mission equipment. Additionally, the market is seeing greater incorporation of alloy‑based contacts for improved thermal performance and the use of predictive maintenance analytics linked to connector health monitoring.

4. How has COVID‑19 impacted the Asia Pacific Aerospace & Defense Power Connector Market and what is the recovery trajectory?

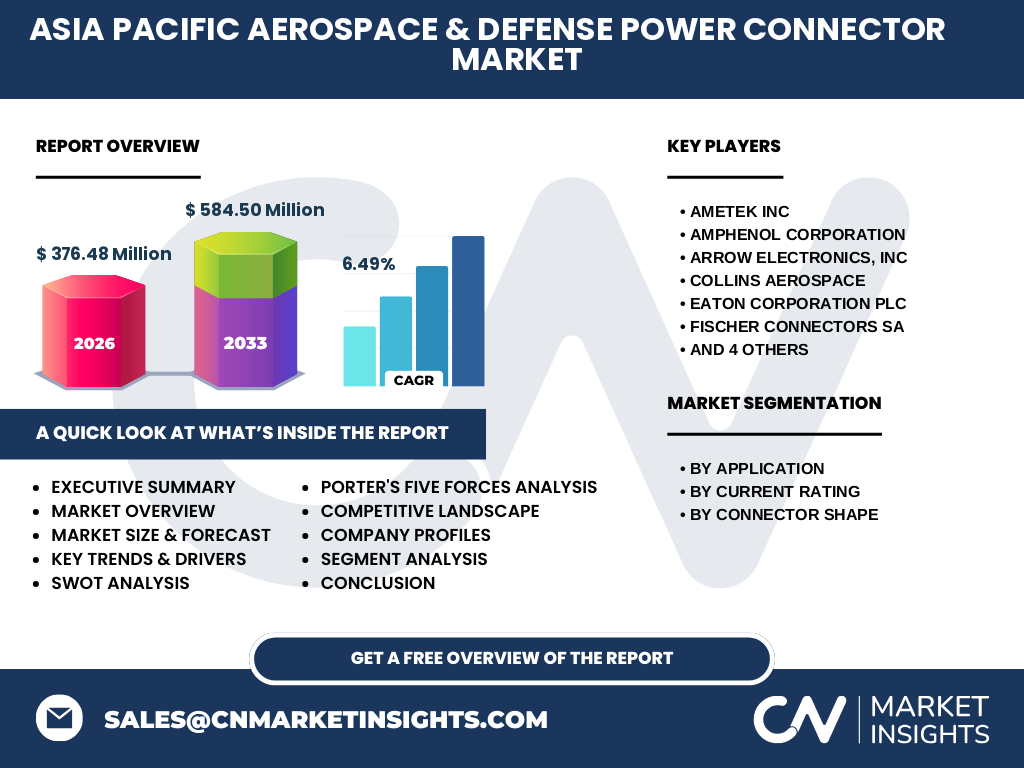

The pandemic caused temporary production slowdowns and delayed aircraft deliveries, which modestly reduced demand for new power connectors in 2020‑2021. However, defense procurement remained resilient, and post‑2022 recovery accelerated as airlines resumed operations and governments increased defense spending. The market is now on a steady upward trajectory, reflected in a projected CAGR of 6.49% through 2032.

5. Who are the major competitors in the Asia Pacific Aerospace & Defense Power Connector Market and what is the state of market consolidation?

Leading competitors include AMETEK Inc, Amphenol Corporation, Arrow Electronics, Inc, Collins Aerospace, Eaton Corporation plc, Fischer Connectors SA, ITT Inc., MOLEX, LLC, Radiall, and TE Connectivity. The market exhibits moderate consolidation, with large multinational firms leveraging extensive product portfolios and global supply networks. Recent strategic alliances and acquisitions aim to strengthen regional presence and broaden high‑current connector offerings.

6. What are the high‑level findings presented in the Executive Summary of the Asia Pacific Aerospace & Defense Power Connector Market?

The Executive Summary highlights a market size of USD 376.48 million in 2026, expanding to USD 584.50 million by 2033, driven by a 6.49% CAGR. Growth is anchored by defense modernization, commercial aircraft fleet expansion, and the shift to higher‑power electric systems. Key opportunities lie in smart connector technologies and regional manufacturing incentives, while regulatory complexity and supply‑chain resilience remain focal challenges.

7. What are the market forecasts for the Asia Pacific Aerospace & Defense Power Connector Market for 2025‑2032?

Forecasts project a steady increase from the 2026 base of USD 376.48 million to approximately USD 584.50 million by 2033, implying continued compound growth of 6.49% per annum. The outlook anticipates stronger demand in the aerospace segment, accelerated procurement of high‑current connectors (>150 A), and expanding share of circular‑shape connectors as aircraft designs prioritize weight reduction and space efficiency.

8. How is the Asia Pacific Aerospace & Defense Power Connector Market sized and shared by application, current rating, and connector shape?

By application, the market is segmented into Aerospace, Military Ground Vehicle, Body‑worn Equipment, and Naval Ships, each leveraging specific rating and shape requirements. Current rating categories span from 5 A–40 A up to >600 A–900 A, with a clear migration toward the >150 A tiers to accommodate electric propulsion and high‑power weapons systems. Shape segmentation includes rectangular and circular connectors, with circular forms gaining traction for density‑critical aerospace installations.

9. What is the geographic distribution of the Asia Pacific Aerospace & Defense Power Connector Market across the region?

The market covers key Asia Pacific economies, including China, Japan, South Korea, India, Australia, and Southeast Asian nations. While exact regional revenue shares are not disclosed, the overall regional market aligns with the total size of USD 376.48 million (2026) and reflects diversified demand across mature aerospace hubs (Japan, Australia) and rapidly growing defense purchasers (India, China).

10. What insights does the regional analysis provide for the Asia Pacific Aerospace & Defense Power Connector Market?

Regional analysis indicates that China and India are driving volume growth through accelerated defense procurement and expanding commercial aviation fleets. Japan and South Korea maintain high‑value, technology‑intensive demand, especially for advanced circular connectors. Australia’s market is propelled by naval modernization programs. Southeast Asian countries contribute incremental growth, largely through upgrades of military ground vehicles and body‑worn equipment.

11. Which companies lead the Asia Pacific Aerospace & Defense Power Connector Market and what strategies are they employing?

Leaders such as Amphenol, TE Connectivity, and Collins Aerospace focus on expanding high‑current product lines and securing long‑term defense contracts. AMETEK and Eaton emphasize diversification into smart connector solutions with embedded sensors. Fischer Connectors and Radiall pursue partnerships with aircraft manufacturers to co‑develop lightweight, circular connector families. MOLEX and ITT concentrate on enhancing supply‑chain agility and localized production in key Asia Pacific hubs.

12. How does Porter’s Five Forces analysis characterize the competitive dynamics of the Asia Pacific Aerospace & Defense Power Connector Market?

• Threat of new entrants – Low, due to high certification barriers and significant R&D investment.

• Bargaining power of suppliers – Moderate, as specialized raw materials (high‑grade alloys, sealed plastics) are sourced from limited vendors.

• Bargaining power of buyers – High, with defense ministries and major OEMs demanding strict compliance and price competitiveness.

• Threat of substitutes – Low, because functional alternatives to dedicated power connectors are limited in aerospace and defense applications.

• Rivalry among existing firms – High, driven by product innovation, strategic alliances, and regional market share battles.

13. What are the SWOT findings for the Asia Pacific Aerospace & Defense Power Connector Market?

Strengths: Robust demand from defense and aviation, advanced technical expertise, and established OEM relationships.

Weaknesses: High certification costs and dependency on a few raw‑material suppliers.

Opportunities: Growth of electric propulsion, smart‑connected connectors, and regional manufacturing incentives.

Threats: Geopolitical tensions affecting cross‑border supply chains and rapid technology shifts that could outpace product development cycles.

14. How is the value chain structured in the Asia Pacific Aerospace & Defense Power Connector Market?

The value chain starts with raw‑material suppliers (conductive alloys, high‑performance polymers), moves to component manufacturers that fabricate contacts and housings, then to connector assemblers who integrate rating‑specific designs. After assembly, testing and certification firms validate performance against aerospace and defense standards. Distributors and system integrators deliver finished connectors to OEMs, who incorporate them into aircraft, vehicles, or naval platforms. After‑sales service and lifecycle support complete the chain.

15. What key investment insights can be drawn for stakeholders interested in the Asia Pacific Aerospace & Defense Power Connector Market?

Investors should focus on companies expanding high‑current (>150 A) and circular‑shape portfolios, as these segments align with electric propulsion trends. Strategic investments in firms with strong defense contracts and regional manufacturing footprints can mitigate supply‑chain risk. Partnerships that integrate sensor‑enabled “smart” connectors present upside potential, while monitoring regulatory developments will be essential for risk management.

16. What are the concluding takeaways from the Asia Pacific Aerospace & Defense Power Connector Market report?

The market is on a clear growth path, moving from USD 376.48 million in 2026 to USD 584.50 million by 2033, driven by defense spending, aerospace fleet expansion, and the transition to higher‑power electric systems. Opportunities in smart connector technology and regional production incentives outweigh challenges related to certification and supply chain complexity. Companies that innovate in high‑current, lightweight designs will likely capture the most value.

17. Which research methodology was applied to develop the Asia Pacific Aerospace & Defense Power Connector Market report?

The study employed a mixed‑method approach, combining primary interviews with industry experts, OEMs, and suppliers, alongside secondary data collection from company filings, defense procurement records, and aviation industry publications. Quantitative analysis used historical sales data to calculate the base‑year market size and applied the stated CAGR of 6.49% for forward‑looking forecasts. Qualitative insights were derived from trend analysis and expert opinion.

18. What is the scope of the research and are there any limitations?

The research covers the Asia Pacific region, focusing on power connectors used in aerospace, military ground vehicles, body‑worn equipment, and naval ships. Segmentation includes application, current rating, and connector shape. Limitations stem from the confidentiality of some defense contract values and the reliance on publicly available financial disclosures, which may constrain the granularity of regional revenue breakdowns.

19. Which key companies have recent developments in the Asia Pacific Aerospace & Defense Power Connector Market?

Recent announcements include Amphenol’s launch of a new high‑current circular connector family for electric aircraft, TE Connectivity’s partnership with a Chinese naval shipbuilder to supply >300 A connectors, and Collins Aerospace’s acquisition of a specialist sensor‑enabled connector startup. Eaton Corporation announced expanded manufacturing capacity in India, while Fischer Connectors released lightweight rectangular connectors targeting body‑worn defense equipment. These developments underscore the market’s focus on higher power ratings, advanced materials, and regional production.