1. North America Bioreactors Market Overview - Definition, scope, and significance?

The North America Bioreactors Market encompasses the production, distribution, and utilization of bioreactor systems for cultivating mammalian, bacterial, and yeast cells across research, biopharma manufacturing, and contract manufacturing organizations. These vessels enable the synthesis of monoclonal antibodies, vaccines, recombinant proteins, stem cells, and gene‑therapy vectors. Their strategic importance lies in accelerating drug development, supporting personalized medicine, and underpinning the region’s leading role in biotechnology innovation.

2. North America Bioreactors Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising demand for biologics, expansion of cell‑therapy pipelines, and increasing investment in R&D by both established firms and startups. Restraints stem from high capital expenditure for large‑scale stainless‑steel systems and regulatory complexity. Challenges involve supply‑chain volatility for single‑use components and skilled‑labor shortages. Opportunities arise from the shift toward single‑use technology, growing contract manufacturing capacity, and emerging gene‑therapy applications that require flexible, scalable bioreactor platforms.

3. North America Bioreactors Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature rapid adoption of single‑use bioreactors, especially wave‑induced motion and bubble‑column designs, driven by reduced turnaround time and lower contamination risk. Emerging trends include integration of digital monitoring, AI‑based process control, and modular “plug‑and‑play” systems that cater to decentralized manufacturing of cell‑based therapies. The market also sees a rise in hybrid technologies combining stainless‑steel robustness with disposable accessories.

4. COVID-19 Impact on the North America Bioreactors Market - Pandemic effects and recovery trajectory?

The pandemic accelerated demand for vaccine production capacity, prompting bioreactor manufacturers to expand single‑use inventories and enhance rapid‑scale capabilities. Facilities were retrofitted to meet surge requirements, leading to temporary capacity constraints that have since eased. Recovery is characterized by sustained investment in flexible platforms, enabling quick response to future health emergencies while maintaining growth momentum established during the crisis.

5. North America Bioreactors Market Competitive Landscape - Major competitors and market consolidation?

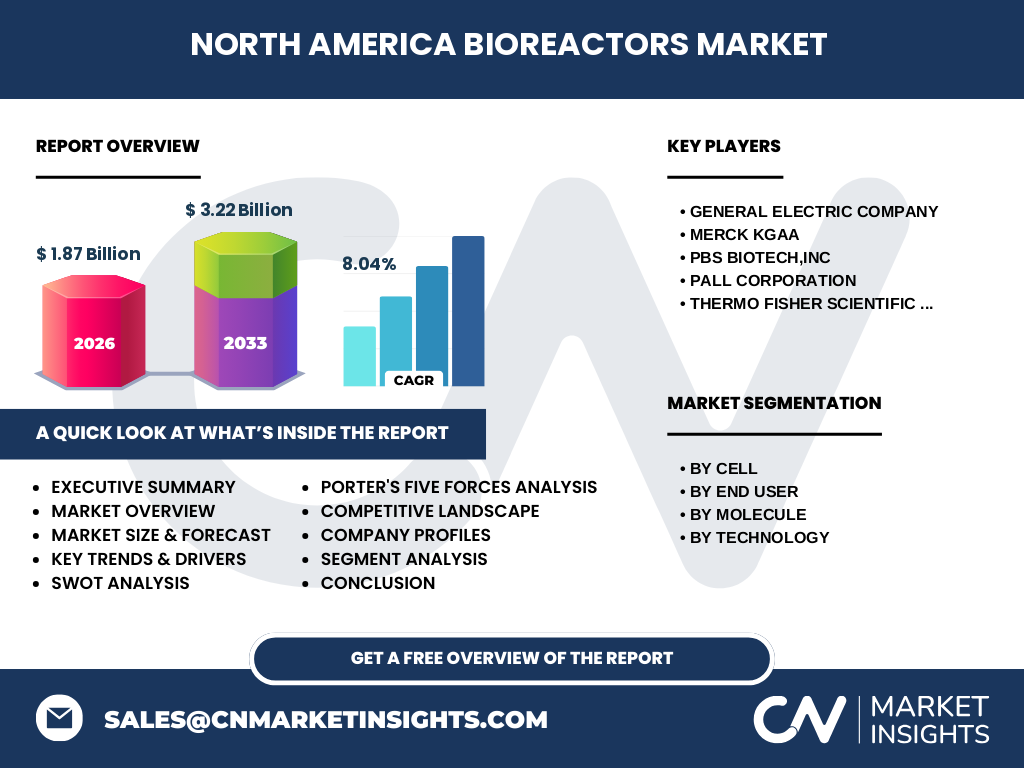

The competitive arena is led by multinational equipment providers such as General Electric Company, MERCK KGaA, PBS Biotech, Inc., Pall Corporation, and Thermo Fisher Scientific Inc. These firms compete on technology innovation, service networks, and single‑use ecosystem breadth. Recent consolidation includes strategic acquisitions of niche single‑use manufacturers, bolstering product portfolios and expanding geographic reach within the North American region.

6. Executive Summary - High-level overview and key findings about North America Bioreactors Market?

The North America Bioreactors Market is valued at 1.87 billion in 2026 and is projected to reach 3.22 billion by 2033, reflecting an 8.04% CAGR. Growth is fueled by strong biopharma pipelines, expanding cell‑therapy sectors, and a decisive shift toward single‑use technologies. Market leaders are investing in digital integration and strategic partnerships, while opportunities abound in gene‑therapy manufacturing and decentralized production models.

7. North America Bioreactors Market Forecast - Projections for 2025-2032 period?

Forecasts indicate continued robust expansion, with the market expected to nearly double from its 2026 baseline by 2033. The 8.04% compound annual growth rate suggests steady demand across all segments, particularly for single‑use systems and advanced cell‑culture applications. This trajectory underscores persistent capital allocation toward flexible, scalable bioprocessing infrastructure throughout the forecast horizon.

8. North America Bioreactors Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by cell type includes mammalian, bacterial, and yeast cells, each serving distinct therapeutic and research needs. By end‑user, research and development organizations, biopharma manufacturers, and contract manufacturing organizations drive usage, with biopharma manufacturers holding the largest share due to high‑volume biologics production. Molecule segmentation spans monoclonal antibodies, vaccines, recombinant proteins, stem cells, and gene therapy, reflecting the market’s breadth. Technology segmentation features wave‑induced motion single‑use bioreactors (SUB), stirred SUB, and single‑use bubble column systems, with wave‑induced motion currently leading adoption.

9. Global North America Bioreactors Market Size and Share by Region - Geographic distribution?

Within the global bioreactors landscape, North America commands a leading position, contributing the majority of the 1.87 billion market size in 2026. The region’s advanced biotech ecosystem, extensive manufacturing base, and robust funding environment underpin this dominant share, while complementary growth occurs in Europe and Asia‑Pacific, driven by similar biologics trends.

10. Regional Analysis of the North America Bioreactors Market - Detailed regional market performance?

In the United States, the market benefits from a dense concentration of biotech clusters, high R&D spending, and a supportive regulatory framework. Canada contributes through government‑backed biotech initiatives and a growing contract manufacturing sector. Both countries exhibit strong demand for single‑use platforms, with the U.S. leading in large‑scale commercial deployments and Canada focusing on innovative pilot‑scale projects.

11. Leading Company Profiles in the North America Bioreactors Market - Industry players and strategies?

General Electric Company leverages its engineering heritage to provide robust stainless‑steel and hybrid systems. MERCK KGaA focuses on integrated bioprocess solutions, emphasizing single‑use flexibility. PBS Biotech, Inc. specializes in wave‑induced motion SUBs, targeting high‑cell‑density cultures. Pall Corporation supplies filtration and consumable components that complement disposable bioreactors. Thermo Fisher Scientific Inc. offers end‑to‑end platforms combining instrumentation, software, and single‑use hardware, fostering a comprehensive value proposition.

12. Porter's Five Forces Analysis of the North America Bioreactors Market - Competitive forces assessment?

Threat of new entrants is moderate, as high capital requirements and technical expertise serve as barriers, yet single‑use niche players can enter with lower upfront costs. Bargaining power of suppliers is moderate; consumable manufacturers hold influence but are offset by multiple supplier options. Bargaining power of buyers is high, driven by large biopharma customers demanding cost‑effective, scalable solutions. Threat of substitutes is low, as alternative cultivation methods cannot match the productivity of modern bioreactors. Industry rivalry is intense, with major OEMs competing on technology, service, and ecosystem integration.

13. SWOT Analysis of the North America Bioreactors Market - Strengths, weaknesses, opportunities, threats?

Strengths: Advanced R&D infrastructure, high adoption of single‑use technology, and strong capital availability. Weaknesses: Dependence on high‑cost disposable components and regulatory complexity. Opportunities: Expansion of gene‑therapy manufacturing, growth of decentralized production, and increasing demand for rapid vaccine platforms. Threats: Supply‑chain disruptions for consumables and potential oversupply as more capacity comes online.

14. North America Bioreactors Market Value Chain Analysis - Industry structure and value flow?

The value chain starts with raw‑material suppliers (e.g., polymer films, sensors), proceeds to equipment manufacturers who design and assemble bioreactors, then to system integrators providing turnkey solutions. End‑users—research institutes, biopharma firms, and CMOs—receive the technology, implement processes, and generate biologic products. After production, downstream logistics handle product purification and distribution, completing the chain.

15. Key Investment Insights in the North America Bioreactors Market - Strategic investment recommendations?

Investors should target companies expanding single‑use portfolios, especially those with robust consumable supply chains. Partnerships that combine digital analytics with hardware present high‑growth potential. Funding opportunities exist in niche startups focusing on modular, AI‑driven bioreactor platforms for cell‑therapy manufacturing. Acquisitions of complementary technology firms can accelerate market share gains for established OEMs.

16. North America Bioreactors Market Conclusion - Summary and key takeaways?

The market demonstrates strong, sustained growth, underpinned by an 8.04% CAGR and a projected climb to 3.22 billion by 2033. Single‑use technologies, expanding biopharma pipelines, and digital integration drive momentum. Competitive dynamics favor innovators with flexible, scalable solutions, while supply‑chain resilience and regulatory navigation remain critical success factors.

17. Research Methodology - How this research was conducted?

Primary data were gathered through interviews with industry experts, supplier surveys, and direct engagements with key biotechnology firms. Secondary sources included company reports, regulatory filings, scientific publications, and reputable market databases. Data triangulation ensured consistency, while trend analysis and forecasting employed compound annual growth rate calculations based on the provided market size and forecast figures.

18. Research Scope - Coverage and limitations?

The study covers the North America Bioreactors market across cell type, end‑user, molecule, and technology segments, focusing on the period 2025‑2032. Geographic scope is limited to the United States and Canada. While the analysis incorporates the latest available figures, it does not extrapolate beyond the supplied market size, forecast, and CAGR data, and therefore refrains from presenting unverified numeric breakdowns.

19. Key Companies and Recent Developments in the North America Bioreactors Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

General Electric Company announced a new hybrid bioreactor line that combines stainless‑steel durability with disposable liners, targeting large‑scale antibody production. MERCK KGaA launched an integrated single‑use platform with built‑in analytics for real‑time monitoring of cell health. PBS Biotech, Inc. introduced a next‑generation wave‑induced motion system optimized for high‑density stem‑cell cultures. Pall Corporation expanded its filtration portfolio to include virus‑clearance modules compatible with single‑use bioreactors. Thermo Fisher Scientific Inc. unveiled a cloud‑based process‑control suite that synchronizes data across multiple bioreactor units, enhancing scalability for contract manufacturers.