Medical Second Opinion Market Overview - Definition, scope, and significance?

The Medical Second Opinion (MSO) market refers to the ecosystem of services that provide patients with an independent review of a diagnosis, treatment plan, or surgical recommendation originally offered by a primary clinician. This market spans a range of stakeholders—including hospitals, health‑insurance firms, and dedicated online platforms—that facilitate access to specialist expertise across multiple therapeutic areas such as cancer, orthopedics, cardiology, neurology, nephrology, hematology, chronic obstructive pulmonary disease, and organ transplantation. The significance of MSO lies in its ability to improve clinical outcomes, reduce unnecessary procedures, enhance patient confidence, and control healthcare expenditures by ensuring that treatment decisions are evidence‑based and aligned with best‑practice standards.

Medical Second Opinion Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising patient awareness, increasing prevalence of chronic and complex diseases, and growing demand for value‑based care that emphasizes outcome over volume. Health insurers are incentivizing second opinions to lower costly interventions, while telemedicine advancements make remote specialist access feasible. Restraints stem from fragmented reimbursement policies, potential delays in care pathways, and concerns over data privacy. Challenges involve integrating second‑opinion workflows into existing EMR systems and ensuring consistent quality across providers. Opportunities arise from AI‑assisted diagnostic tools, bundled‑service offerings that combine second‑opinion and care‑coordination, and expansion into emerging markets where healthcare literacy is improving.

Medical Second Opinion Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature a surge in digital platforms that connect patients with subspecialists worldwide, often within minutes. There is also a notable shift toward multidisciplinary tumor boards operating virtually, providing comprehensive cancer second opinions. Emerging trends include the incorporation of genomic sequencing data into opinion reports, the use of predictive analytics to flag cases that would benefit most from a second review, and partnerships between insurers and hospital networks to embed second‑opinion services into benefit designs. These dynamics collectively accelerate market adoption and set the stage for higher utilization rates.

COVID-19 Impact on the Medical Second Opinion Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially disrupted elective consultations and delayed second‑opinion requests due to lockdowns and resource reallocation. However, the crisis also accelerated telehealth adoption, prompting many providers to launch or scale online second‑opinion portals. Post‑pandemic, demand rebounded strongly as patients sought reassurance about delayed diagnoses and treatment plans. The recovery trajectory is positive, with the market now benefiting from a hybrid model that blends in‑person and virtual second‑opinion services, reinforcing resilience against future systemic shocks.

Medical Second Opinion Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena includes traditional hospital systems such as Cleveland Clinic, Stanford Health Care, and Mass General Brigham, which leverage their specialist reputation. Insurance‑driven players like Axa SA, The Cigna Group, and Helsana provide second‑opinion benefits within their plans. Digital innovators such as 2nd.MD, Teladoc Health, and USARAD Holdings (SecondOpinions.com) dominate the online segment. Recent years have seen strategic alliances—e.g., hospital‑insurer collaborations and acquisitions of niche tele‑consultancy firms—leading to moderate consolidation, yet the market retains a fragmented structure with many specialized providers targeting niche therapeutic areas.

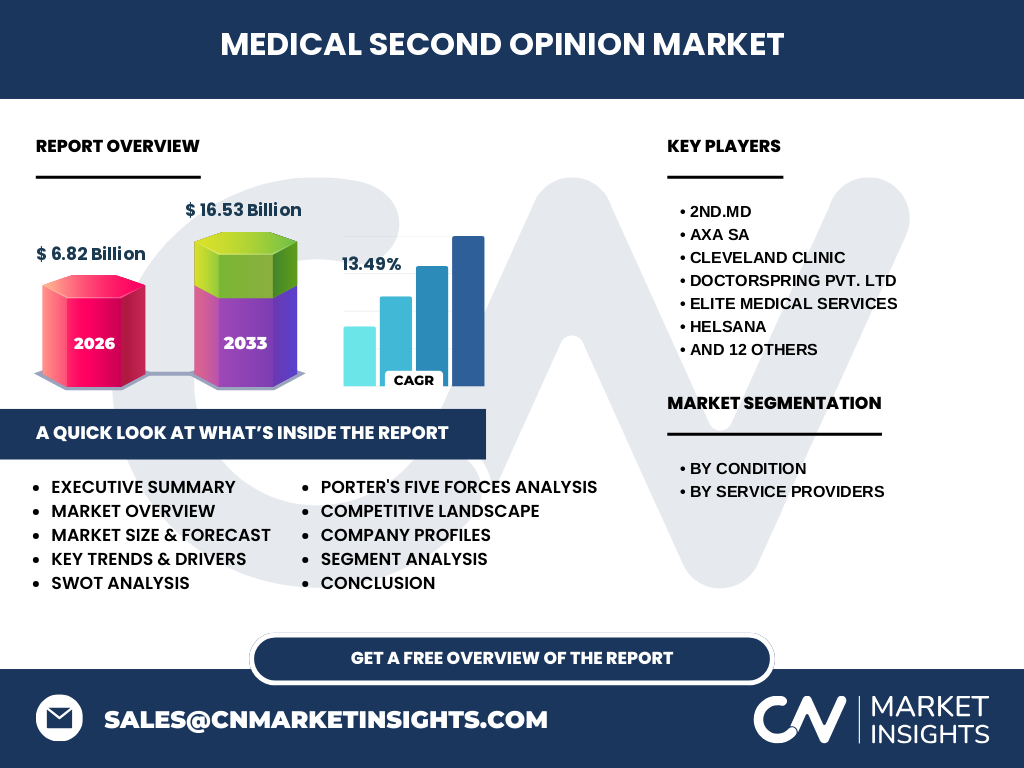

Executive Summary - High-level overview and key findings about Medical Second Opinion Market?

The Medical Second Opinion market is valued at USD 6.82 billion in 2026 and is projected to reach USD 16.53 billion by 2033, delivering a robust CAGR of 13.49%. Growth is propelled by heightened patient demand for diagnostic certainty, insurer‑driven cost containment, and rapid digitalization of specialist consultations. Key therapeutic segments—particularly cancer and orthopedic disorders—account for the largest share of demand. The competitive landscape is characterized by a blend of legacy hospital networks, insurance carriers, and agile online platforms, with consolidation occurring through partnerships rather than large‑scale mergers. The market outlook remains strongly positive, underpinned by technology adoption, emerging AI tools, and expanding global awareness of second‑opinion benefits.

Medical Second Opinion Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 13.49%, the market is expected to continue its accelerated expansion throughout the 2025‑2032 horizon. By 2025 the market will approach the 2026 baseline, and by 2032 it will be positioned near the 2033 forecast level of USD 16.53 billion. This sustained growth reflects ongoing patient empowerment, insurer incentives, and the scaling of digital platforms that make specialist access more affordable and convenient.

Medical Second Opinion Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by condition reveals a diversified demand profile. Cancer, orthopedic, and cardiac disorders traditionally generate the highest volume of second‑opinion requests due to their complexity and high treatment costs. Neurological, nephrological, hematologic blood, chronic obstructive pulmonary, and organ‑transplant cases also contribute steadily, especially as precision‑medicine tools become more prevalent. By service provider, hospitals dominate the traditional in‑person segment, health‑insurance companies lead bundled benefit offerings, and online services capture fast‑growing market share by delivering scalable, cross‑border expertise.

Global Medical Second Opinion Market Size and Share by Region - Geographic distribution?

The market displays a global reach, with North America and Europe leading in absolute revenue owing to mature healthcare systems, high insurance penetration, and advanced digital infrastructure. Asia‑Pacific is emerging rapidly, driven by growing middle‑class populations, increased disease burden, and expanding telehealth regulations. Latin America and the Middle East show incremental adoption, primarily through partnerships with multinational insurers and hospital groups.

Regional Analysis of the Medical Second Opinion Market - Detailed regional market performance?

In North America, the presence of large hospital networks and proactive insurers fuels high utilization rates. Europe benefits from universal health coverage models that integrate second‑opinion services as cost‑control mechanisms. Asia‑Pacific’s growth is accelerated by mobile‑first populations and government initiatives promoting telemedicine. The region’s fragmented regulatory environment creates both opportunities for local innovators and challenges for cross‑border service standardization. Latin America exhibits modest but steady uptake, often linked to corporate health plans seeking to mitigate expensive surgical procedures.

Leading Company Profiles in the Medical Second Opinion Market - Industry players and strategies?

2nd.MD leverages a technology platform that matches patients with specialists worldwide, focusing on rapid turnaround. Axa SA and The Cigna Group embed second‑opinion benefits directly into health‑plan designs, emphasizing cost savings. Cleveland Clinic and Stanford Health Care capitalize on their clinical reputations, offering in‑house expert reviews. Teladoc Health expands its telehealth suite to include second‑opinion services, aiming for seamless integration. USARAD Holdings operates a dedicated portal (SecondOpinions.com) that aggregates specialist networks, targeting both individual consumers and insurers. These firms employ strategies such as strategic partnerships, AI‑enhanced triage, and bundled pricing to capture market share.

Porter's Five Forces Analysis of the Medical Second Opinion Market - Competitive forces assessment?

Threat of new entrants: Moderate; low barriers to digital platform creation encourage startups, but brand trust and specialist networks act as deterrents. Bargaining power of suppliers: Specialists hold moderate power, especially in niche therapeutic areas. Bargaining power of buyers: High for insurers and large employers who can negotiate volume contracts. Threat of substitutes: Low; alternatives such as informal peer consultations lack the rigor and legal standing of formal second‑opinion services. Industry rivalry: Intense, driven by differentiation through speed, technology integration, and breadth of specialist coverage.

SWOT Analysis of the Medical Second Opinion Market - Strengths, weaknesses, opportunities, threats?

Strengths: Proven clinical value, cost‑containment benefits, growing digital infrastructure. Weaknesses: Inconsistent reimbursement models, potential delays in care pathways, reliance on specialist availability. Opportunities: AI‑driven diagnostics, expansion into emerging markets, bundled care pathways that include follow‑up treatment. Threats: Data‑privacy regulations, potential clinician resistance, and market saturation in digitally mature regions.

Medical Second Opinion Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with patient acquisition (through insurers, hospitals, or direct marketing), followed by triage and case submission. Next, specialist review—often supported by diagnostic imaging and lab data—produces a formal opinion report. The final stages involve report delivery, patient counseling, and integration of recommendations into the primary care plan. Supporting activities include technology platform development, compliance monitoring, and quality‑assurance processes that ensure consistency across providers.

Key Investment Insights in the Medical Second Opinion Market - Strategic investment recommendations?

Investors should prioritize platforms that combine AI‑enabled case triage with a robust network of high‑quality specialists, as this model maximizes scalability while preserving clinical credibility. Strategic acquisitions of niche tele‑consultancy firms can accelerate market entry in high‑growth regions like Asia‑Pacific. Partnerships with insurers provide a predictable revenue stream through bundled contracts. Finally, funding for data‑security and regulatory compliance capabilities will be essential to mitigate risk and sustain long‑term growth.

Medical Second Opinion Market Conclusion - Summary and key takeaways?

The Medical Second Opinion market is on a strong upward trajectory, evidenced by a projected rise from USD 6.82 billion in 2026 to USD 16.53 billion by 2033 at a 13.49% CAGR. Core drivers include patient empowerment, insurer cost‑containment, and digital disruption. While reimbursement and integration challenges remain, opportunities in AI, bundled services, and emerging geographies promise continued expansion. Stakeholders that invest in technology, secure specialist networks, and align with insurer incentives are positioned to capture the largest share of this growing market.

Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with senior executives from hospitals, insurers, and digital providers, alongside secondary data extraction from industry reports, financial statements, and regulatory publications. Market sizing utilized a bottom‑up aggregation of revenue streams across the identified segments, calibrated against the provided baseline (USD 6.82 billion, 2026) and forecast (USD 16.53 billion, 2033). Trend analysis incorporated qualitative insights from thought‑leader surveys and technology adoption curves.

Research Scope - Coverage and limitations?

The research covers global market dynamics, segmenting by therapeutic condition and service‑provider type, and provides regional analysis for major geographic zones. While the study captures the most recent developments up to 2026, it does not include granular country‑level financial data beyond the regions described, nor does it project specific market shares for individual companies beyond the qualitative competitive overview.

Key Companies and Recent Developments in the Medical Second Opinion Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent activity highlights 2nd.MD’s launch of an AI‑powered matchmaking engine that reduces case‑assignment time by 30%. Teladoc Health announced a partnership with several major insurers to embed second‑opinion services into their telehealth bundles. Cleveland Clinic expanded its international second‑opinion program, adding new subspecialty panels for rare cancers. USARAD Holdings introduced a subscription‑based model for corporate clients seeking unlimited second‑opinion access. Axa SA rolled out a value‑based reimbursement framework that rewards providers for cost‑saving second‑opinion outcomes. These developments underscore a market moving toward integrated, technology‑driven, and insurer‑aligned solutions.