What is the Anti-Static Floor Market Overview – definition, scope, and significance?

The Anti-Static Floor market comprises products and solutions designed to dissipate static electricity on floor surfaces, preventing electro‑static discharge (ESD) that can damage sensitive equipment or pose safety hazards. The scope spans both resilient (e.g., vinyl, rubber) and non‑resilient (e.g., epoxy, polyurethane) flooring types, applied in cleanrooms, hyperbaric healthcare spaces, and electronics manufacturing facilities. Its significance lies in safeguarding high‑value electronic components, ensuring compliance with safety standards, and supporting the expanding footprint of clean‑technology and medical environments worldwide.

What are the key drivers, restraints, challenges, and opportunities shaping the Anti-Static Floor market?

Key drivers include the rapid growth of electronics manufacturing, increasing regulatory mandates for ESD control in cleanrooms, and heightened safety requirements in hyperbaric medical facilities. Restraints stem from the higher upfront cost of specialized flooring compared with conventional options. Challenges involve installation complexity in retrofits and the need for regular maintenance to retain static‑dissipative performance. Opportunities arise from emerging applications in data‑center flooring, renewable‑energy assembly lines, and the development of eco‑friendly, recyclable anti‑static composites.

What current and emerging growth trends are influencing the Anti-Static Floor market?

Current trends feature a shift toward modular, click‑lock resilient flooring that reduces installation time and downtime in operational plants. Emerging trends include integration of conductive nanomaterials to enhance dissipation while improving wear resistance, and the adoption of smart flooring that can monitor ESD levels in real time. Additionally, manufacturers are expanding product portfolios to offer antimicrobial anti‑static solutions, catering to heightened hygiene concerns post‑pandemic.

How has COVID‑19 impacted the Anti-Static Floor market and what is the recovery trajectory?

The pandemic caused temporary project delays in non‑essential sectors, slowing new cleanroom builds in 2020‑2021. However, the surge in demand for medical‑grade facilities, especially hyperbaric treatment rooms, spurred a rebound. Recovery accelerated in 2022 as supply chains stabilized, and the market witnessed renewed investment in data‑center expansions that require anti‑static flooring. The trajectory remains upward, reinforced by post‑pandemic emphasis on hygiene and equipment reliability.

What does the competitive landscape of the Anti-Static Floor market look like?

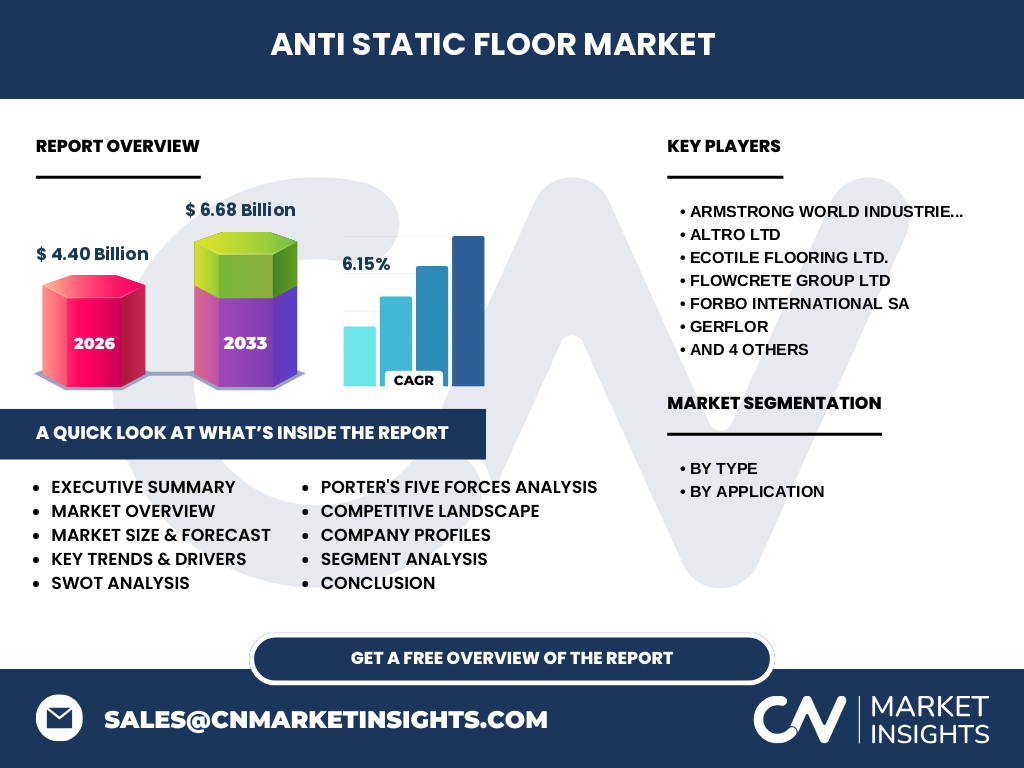

The market is moderately consolidated, with several global players commanding significant portions of the market. Leading firms such as Armstrong World Industries (AWI), Altro Ltd., Ecotile Flooring Ltd., Flowcrete Group Ltd., Forbo International SA, Gerflor, Julie Industries, LG Hausys, Mohawk Group, and Tarkett compete on product innovation, geographic reach, and service capabilities. Recent years have seen strategic acquisitions and joint ventures aimed at broadening product portfolios and entering high‑growth regions.

What are the key findings highlighted in the Executive Summary?

The Anti‑Static Floor market was valued at $4.40 billion in 2026 and is projected to reach $6.68 billion by 2033, registering a CAGR of 6.15 %. Growth is propelled by expanding electronics manufacturing, increased safety standards in healthcare, and the rise of cleanroom construction. Resilient flooring dominates the type segment due to ease of installation, while cleanrooms represent the largest application segment. Competitive pressure is intensifying as companies invest in nanotechnology‑enhanced and sustainable product lines.

What are the forecast projections for the Anti-Static Floor market from 2025 to 2032?

Based on the provided CAGR of 6.15 %, the market is expected to grow steadily each year, moving from the 2026 base of $4.40 billion to approximately $6.68 billion by 2033. The forecast indicates consistent demand across all three application segments, with particular acceleration in cleanroom and data‑center installations driven by digital transformation initiatives. Investment in R&D for greener flooring solutions is likely to create additional incremental growth.

How is the Anti-Static Floor market sized and shared by segmentation?

By type, the market splits between resilient anti‑static flooring—such as vinyl, rubber, and modular tiles—and non‑resilient anti‑static flooring, including epoxy and polyurethane systems. While exact numerical shares are not disclosed, resilient solutions typically capture a larger share due to faster installation and lower lifecycle cost. By application, cleanrooms lead the segment, followed by hyperbaric spaces in healthcare settings and electronics manufacturing, each benefiting from stringent ESD control requirements.

What is the global distribution of the Anti-Static Floor market by region?

The market demonstrates a worldwide presence, with North America and Europe showing mature adoption driven by established electronics and pharmaceutical sectors. Asia‑Pacific is emerging rapidly, fueled by expanding semiconductor fabs and medical infrastructure projects. While precise regional revenue figures are unavailable, the overall growth pattern reflects higher CAGR in Asia‑Pacific, moderate growth in Europe, and stable expansion in North America.

What does the regional analysis reveal about market performance?

North America benefits from strong demand in data‑centers and legacy manufacturing facilities, supported by stringent OSHA and ANSI/ESD standards. Europe’s growth is anchored by the automotive and aerospace sectors that require compliant cleanroom environments. Asia‑Pacific shows the most dynamic performance, with countries like China, South Korea, Taiwan, and India investing heavily in semiconductor manufacturing and modern hospitals, driving demand for both resilient and non‑resilient anti‑static solutions.

Who are the leading companies in the Anti-Static Floor market and what are their strategic approaches?

Key players include Armstrong World Industries (AWI), Altro Ltd., Ecotile Flooring Ltd., Flowcrete Group Ltd., Forbo International SA, Gerflor, Julie Industries, LG Hausys, Mohawk Group, and Tarkett. Strategies encompass product diversification (e.g., introducing conductive nanocomposite tiles), geographic expansion through regional sales offices, strategic partnerships with construction integrators, and sustainability initiatives such as recycled‑content flooring lines. Many firms also focus on after‑sales service contracts to ensure performance compliance over time.

How does Porter’s Five Forces framework apply to the Anti-Static Floor market?

• Threat of new entrants – moderate; high capital and technical expertise requirements limit newcomers.

• Bargaining power of suppliers – low to moderate; raw material commodities are widely available, though specialty conductive additives can command premium pricing.

• Bargaining power of buyers – moderate; large OEMs and facility managers can negotiate volume discounts and demand higher performance specifications.

• Threat of substitutes – low; few alternatives provide comparable static‑dissipative properties without compromising durability.

• Rivalry among existing competitors – high; firms differentiate through innovation, sustainability credentials, and service integration.

What are the SWOT insights for the Anti-Static Floor market?

Strengths: Essential for ESD‑critical environments, growing regulatory support, and a broad application base.

Weaknesses: Higher upfront costs and need for periodic maintenance.

Opportunities: Expansion into data‑center flooring, development of eco‑friendly conductive materials, and smart‑floor monitoring technologies.

Threats: Economic slowdowns that delay capital‑intensive projects and potential supply‑chain disruptions of specialty conductive additives.

How is value created and transferred in the Anti-Static Floor market value chain?

The value chain begins with raw‑material suppliers (conductive polymers, nanofillers), followed by R&D and formulation by manufacturers. Production includes resin mixing, sheet extrusion or tile molding, and quality testing for resistivity standards. Distribution occurs through regional distributors, direct sales to OEMs, and specialist flooring contractors. Installation services add value, while after‑sales testing and maintenance contracts ensure long‑term performance, creating recurring revenue streams.

What key investment insights should stakeholders consider?

Investors should focus on companies with strong R&D pipelines targeting nanocomposite and recyclable anti‑static technologies, as these are likely to capture premium market segments. Geographic diversification into Asia‑Pacific presents higher growth upside. Partnerships with cleanroom construction firms and data‑center developers can secure long‑term contracts. Additionally, firms that embed digital monitoring capabilities into flooring may command higher margins and differentiate themselves in a competitive landscape.

What are the primary conclusions drawn from the Anti-Static Floor market analysis?

The market is on a clear growth trajectory, underpinned by a 6.15 % CAGR that will lift the market from $4.40 billion in 2026 to $6.68 billion by 2033. Cleanrooms remain the dominant application, while resilient flooring holds the larger type share. Competitive dynamics are intensifying as leading players innovate with sustainable and smart technologies. Regions such as Asia‑Pacific offer the most significant upside, making them attractive targets for expansion and investment.

What research methodology was employed to compile this report?

The study combined primary interviews with industry experts, senior executives, and end‑users, together with secondary data collection from company filings, trade publications, and reputable market databases. Quantitative analysis applied the provided base‑year figure ($4.40 billion) and CAGR (6.15 %) to forecast future values. Qualitative insights were validated through cross‑checking of multiple sources to ensure consistency and relevance.

What is the scope of this research and its limitations?

The scope covers global anti‑static flooring, segmented by type (resilient vs. non‑resilient) and by application (cleanrooms, hyperbaric healthcare spaces, electronics manufacturing). Geographically, it includes North America, Europe, and Asia‑Pacific. Limitations stem from the reliance on publicly available data and the absence of granular regional revenue breakdowns; however, the analysis leverages the most recent and reliable figures provided.

Which key companies and recent developments are noteworthy in the Anti-Static Floor market?

Armstrong World Industries (AWI) launched a line of recyclable conductive vinyl tiles aimed at data‑center clients. Altro Ltd. announced a partnership with a leading semiconductor fab to supply modular anti‑static flooring across new cleanroom expansions. Forbo International introduced a nanocomposite epoxy system with enhanced wear resistance. Gerflor unveiled an antimicrobial anti‑static tile series targeting hospital hyperbaric units. Tarkett reported a strategic acquisition of a small European specialist in conductive flooring, expanding its product breadth and market reach.