What is the definition, scope, and significance of the Asia Pacific Automated Compounding Systems market?

The Asia Pacific Automated Compounding Systems market encompasses technologies that automate the preparation of sterile and non‑sterile medication mixtures for clinical use. Its scope includes gravimetric and volumetric systems deployed in hospitals and chemotherapy centers across the region. The market is significant because it enhances dosage accuracy, reduces contamination risk, and supports growing demand for personalized oncology therapies, driving adoption among healthcare providers seeking efficiency and patient safety improvements.

What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Automated Compounding Systems market?

Drivers include rising chronic disease prevalence, increasing chemotherapy procedures, and regulatory emphasis on medication safety. Restraints involve high capital expenditure and limited reimbursement frameworks in some economies. Challenges comprise integration with existing pharmacy workflows and the need for skilled operators. Opportunities lie in expanding outpatient oncology services, government health‑technology initiatives, and growing private‑hospital investments that can accelerate system deployment across the region.

What current and emerging trends are influencing the Asia Pacific Automated Compounding Systems market?

Key trends include a shift toward gravimetric systems for higher precision, adoption of cloud‑based data analytics for compounding traceability, and increasing use of robotic automation in large hospital pharmacies. Emerging trends feature AI‑driven dose verification, modular system designs for smaller chemotherapy centers, and strategic partnerships between equipment vendors and regional distributors to broaden market reach and service support.

How has COVID‑19 impacted the Asia Pacific Automated Compounding Systems market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and delayed capital projects, causing a short‑term slowdown in system installations. However, heightened focus on sterile preparation and infection control accelerated demand for automated compounding in hospitals treating COVID‑19 complications and oncology patients. Recovery is underway as health systems prioritize resilience, with projected growth resuming in line with the 7.06 % CAGR through 2033.

What does the competitive landscape look like for the Asia Pacific Automated Compounding Systems market?

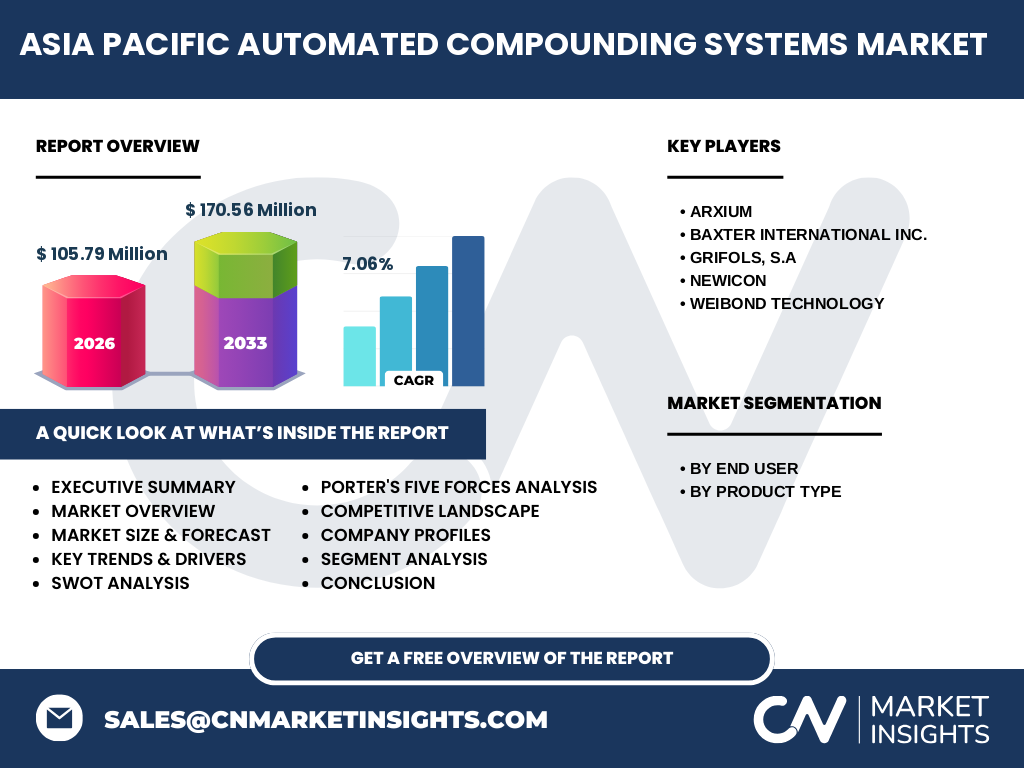

The market is moderately consolidated with five prominent players: ARxIUM, Baxter International Inc., Grifols, S.A., NewIcon, and Weibond Technology. These companies compete on technology differentiation, service networks, and regional partnerships. Market consolidation is evident through strategic collaborations and product portfolio expansions aimed at capturing hospital and chemotherapy center segments across diverse Asia Pacific economies.

What are the key findings from the executive summary of the Asia Pacific Automated Compounding Systems market?

The executive summary highlights a market valued at 105.79 million in 2026, forecast to reach 170.56 million by 2033, growing at a 7.06 % CAGR. Growth is driven by increasing oncology care, regulatory pressure for safer compounding, and technology advancements in gravimetric and volumetric systems. Leading vendors are investing in regional service infrastructure to capitalize on expanding hospital and chemotherapy center demand.

What are the market forecast projections for the Asia Pacific Automated Compounding Systems market from 2025 to 2032?

Forecasts indicate the market will expand from 105.79 million in 2026 to 170.56 million by 2033, reflecting a compound annual growth rate of 7.06 %. The 2025‑2032 period is expected to capture the bulk of this growth as hospitals modernize pharmacy operations and chemotherapy centers adopt automated solutions to meet rising patient volumes and safety standards.

How is the Asia Pacific Automated Compounding Systems market segmented by end user and product type?

Segmentation by end user comprises hospitals and chemotherapy centers, with hospitals representing the larger share due to broader medication preparation needs. By product type, the market splits into gravimetric automated compounding systems, favored for high‑precision weight‑based dosing, and volumetric automated compounding systems, which offer faster throughput for standard preparations. Both segments are projected to grow in tandem with overall market expansion.

What is the geographic distribution of the Asia Pacific Automated Compounding Systems market?

The market spans major Asia Pacific economies including China, Japan, India, South Korea, Australia, and Southeast Asian nations. While the provided data does not break down values by country, the regional aggregation reflects diverse healthcare infrastructure maturity, with higher adoption in advanced hospital systems and accelerating uptake in emerging markets driven by government health‑technology initiatives.

How does regional performance vary within the Asia Pacific Automated Compounding Systems market?

Regional analysis shows mature markets such as Japan and Australia leading in technology adoption due to established oncology networks and favorable reimbursement. Fast‑growing markets like China and India are experiencing rapid hospital expansion and increasing chemotherapy center establishment, creating strong demand pipelines. Southeast Asia presents incremental growth as private healthcare investment rises and regulatory frameworks evolve.

Who are the leading companies in the Asia Pacific Automated Compounding Systems market and what are their strategies?

Key players include ARxIUM, Baxter International Inc., Grifols, S.A., NewIcon, and Weibond Technology. Their strategies focus on product innovation — especially gravimetric precision — regional service center establishment, and partnerships with local distributors to enhance market penetration. Companies also invest in training programs to address the skilled‑operator gap and differentiate through integrated software platforms for compounding management.

What does Porter’s Five Forces analysis reveal about the Asia Pacific Automated Compounding Systems market?

Porter’s analysis indicates moderate supplier power due to specialized component providers, high buyer power as large hospital networks negotiate volume discounts, and moderate threat of substitutes given manual compounding remains an alternative but less safe. Competitive rivalry is intense among the five major vendors, while entry barriers are high because of regulatory compliance, capital intensity, and established service networks.

What are the strengths, weaknesses, opportunities, and threats (SWOT) for the Asia Pacific Automated Compounding Systems market?

Strengths include proven accuracy improvements, regulatory tailwinds, and strong vendor service ecosystems. Weaknesses involve high upfront costs and dependence on skilled technicians. Opportunities arise from expanding oncology services, digital health integration, and government funding for hospital modernization. Threats encompass economic volatility, reimbursement policy shifts, and potential technology obsolescence if innovation pacing slows.

How does the value chain operate in the Asia Pacific Automated Compounding Systems market?

The value chain begins with component suppliers providing sensors, pumps, and software modules to system manufacturers such as ARxIUM and Baxter. Manufacturers assemble gravimetric and volumetric units, which are then distributed through regional partners to end users — hospitals and chemotherapy centers. Post‑sale services, including installation, calibration, training, and maintenance, complete the chain and generate recurring revenue streams.

What are the key investment insights for stakeholders in the Asia Pacific Automated Compounding Systems market?

Investors should target companies with strong regional service footprints and scalable gravimetric platforms, as these align with the 7.06 % CAGR trajectory. Opportunities exist in financing hospital pharmacy upgrades, supporting chemotherapy center automation, and backing software‑enabled compounding analytics. Strategic acquisitions of local distributors can accelerate market access in high‑growth economies like China and India.

What are the concluding takeaways for the Asia Pacific Automated Compounding Systems market?

The market is poised for steady growth from 105.79 million in 2026 to 170.56 million by 2033, driven by oncology demand, safety regulations, and technology advances. Leading vendors ARxIUM, Baxter, Grifols, NewIcon, and Weibond Technology will shape competitive dynamics through innovation and service expansion. Stakeholders should monitor regulatory changes and reimbursement trends to maximize adoption across hospitals and chemotherapy centers.

What research methodology underpins this Asia Pacific Automated Compounding Systems market analysis?

The analysis combines primary research — interviews with key opinion leaders, hospital pharmacy directors, and vendor executives — with secondary research including regulatory filings, company financial reports, industry publications, and market databases. Quantitative modeling applies the provided market size, forecast, and CAGR to derive segment‑level projections, ensuring consistency with the stated 105.79 million base and 170.56 million forecast.

What is the scope and coverage of this Asia Pacific Automated Compounding Systems market research?

The research covers the period 2025‑2033, focusing on automated compounding systems used in hospitals and chemotherapy centers across the Asia Pacific region. It includes both gravimetric and volumetric product types and profiles five major vendors. The scope excludes manual compounding equipment, non‑sterile preparation devices, and markets outside Asia Pacific, ensuring a targeted view of the defined segment.

Which key companies have recent developments in the Asia Pacific Automated Compounding Systems market?

Recent announcements involve ARxIUM launching a next‑generation gravimetric platform with integrated AI verification, Baxter expanding its service network in Southeast Asia, Grifols entering a distribution partnership with a leading Chinese medical device distributor, NewIcon unveiling a compact volumetric system for small chemotherapy centers, and Weibond Technology securing a government tender for hospital pharmacy automation in India.