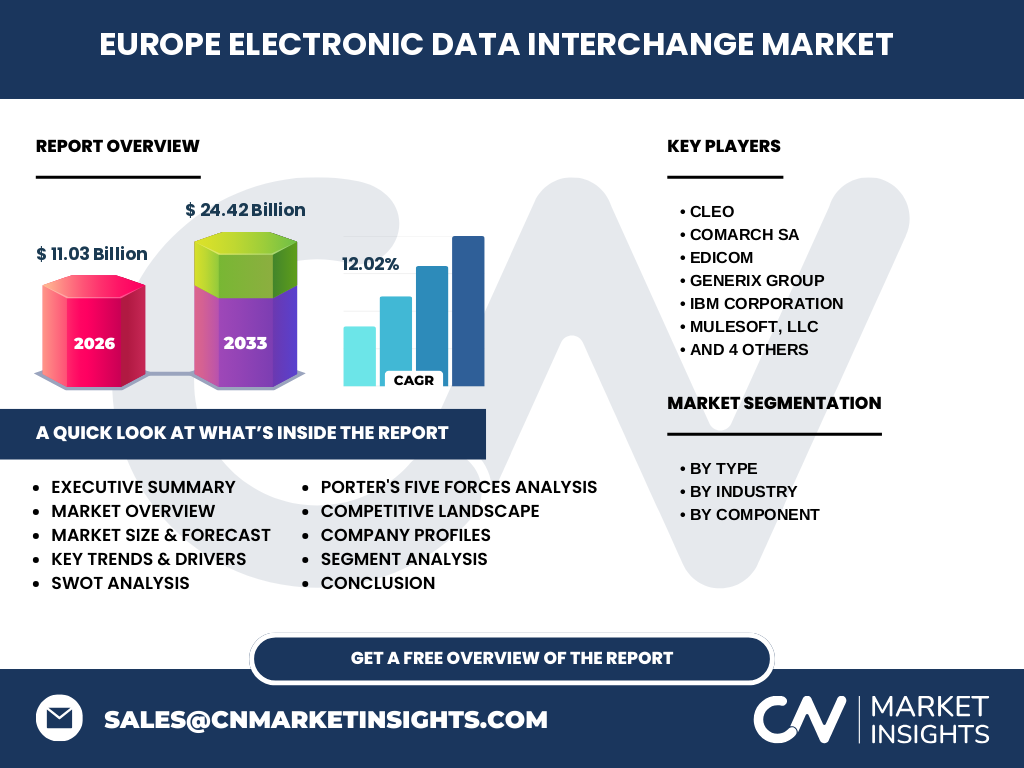

What is the Europe Electronic Data Interchange (EDI) Market Overview, including its definition, scope, and significance?

The Europe Electronic Data Interchange (EDI) Market refers to the structured electronic exchange of business documents between organizations, replacing paper-based processes. Its scope encompasses various deployment models such as VAN, web-based, outsourcing, software, and direct EDI across industries like BFSI, retail, healthcare, IT, and transportation. The market's significance lies in enabling supply chain automation, reducing errors, accelerating transaction speeds, and ensuring regulatory compliance across European economies. With a projected market size of 11.03 Billion in 2026 and a forecast of 24.42 Billion by 2033 at a CAGR of 12.02%, EDI is a critical digital infrastructure for European enterprises.

What are the key drivers, restraints, challenges, and opportunities shaping the Europe Electronic Data Interchange (EDI) Market?

Key drivers include increasing demand for supply chain visibility, government mandates for e-invoicing (e.g., EU Directive 2014/55/EU), and cloud adoption. Restraints involve high implementation costs for SMEs and legacy system integration complexities. Challenges include data security concerns, partner onboarding friction, and evolving standards like PEPPOL. Opportunities arise from AI-driven analytics integration, blockchain for audit trails, and expanding EDI in healthcare and cross-border logistics. The market's 12.02% CAGR reflects strong momentum from digital transformation initiatives across European industries.

What are the current and emerging growth trends in the Europe Electronic Data Interchange (EDI) Market?

Current trends include migration from traditional VAN to web-based and cloud-native EDI solutions, rise of EDI outsourcing for cost efficiency, and adoption of API-based integration alongside EDI. Emerging trends involve embedded EDI within ERP platforms, real-time transaction monitoring using IoT data, and sector-specific solutions for healthcare (HL7) and automotive (ODETTE). The shift towards "EDI as a Service" models and increased use in sustainability reporting (CSRD compliance) are reshaping the landscape, supporting the forecasted growth to 24.42 Billion by 2033.

How did COVID-19 impact the Europe Electronic Data Interchange (EDI) Market, and what is the recovery trajectory?

COVID-19 accelerated EDI adoption as lockdowns forced rapid digitization of procurement, invoicing, and logistics documentation. Companies with existing EDI infrastructure maintained operations, while others urgently invested in web-EDI and outsourcing to enable remote collaboration. The pandemic highlighted supply chain vulnerabilities, driving post-crisis investments in end-to-end visibility. Recovery is robust, with sustained demand from retail, healthcare, and manufacturing sectors. The market's trajectory from 11.03 Billion (2026) to 24.42 Billion (2033) reflects this structural shift toward resilient digital supply chains.

What is the competitive landscape of the Europe Electronic Data Interchange (EDI) Market, and who are the major competitors?

The market is moderately consolidated with a mix of global giants and specialized European providers. Major competitors include Cleo, Comarch SA, EDICOM, Generix Group, IBM Corporation, Mulesoft LLC, SPS Commerce Inc., The Descartes Systems Group Inc., TrueCommerce Inc., and Unifiedpost Group. These players compete on integration breadth, industry-specific compliance (e.g., PEPPOL, GDPR), cloud scalability, and managed services. Strategic partnerships with ERP vendors (SAP, Oracle) and acquisitions to expand geographic footprint are common. The competitive intensity drives innovation in low-code onboarding and AI-powered error resolution.

What is the Executive Summary of the Europe Electronic Data Interchange (EDI) Market, highlighting key findings?

The Europe EDI Market is experiencing strong growth driven by regulatory mandates, supply chain digitization, and cloud adoption. Valued at 11.03 Billion in 2026, it is forecast to reach 24.42 Billion by 2033 at a 12.02% CAGR. Key segments include VAN, Web-EDI, Outsourcing, Software, and Direct EDI across BFSI, Retail, Healthcare, IT, and Transportation. Solution and Services components both see demand. Leading vendors like Cleo, EDICOM, and SPS Commerce are investing in API hybridization and vertical solutions. The market offers significant investment potential in automation, compliance, and cross-border trade facilitation.

What is the Europe Electronic Data Interchange (EDI) Market Forecast for the 2025-2032 period?

While the provided data specifies a 2026 market size of 11.03 Billion and a forecast of 24.42 Billion for 2027-2033 at 12.02% CAGR, the 2025-2032 period aligns closely with this high-growth trajectory. The market is expected to sustain double-digit growth throughout, fueled by e-invoicing mandates, SME cloud migration, and logistics digitization. By 2032, the market will likely approach the 24.42 Billion forecast, with Web-EDI and Outsourcing segments outperforming. Investment in AI-enhanced mapping and real-time analytics will be key differentiators for vendors capturing this expanding opportunity.

What is the Europe Electronic Data Interchange (EDI) Market Size and Share by Segmentation, broken down by type, industry, and component?

The market is segmented by Type into Electronic Data Interchange VAN, Web Electronic Data Interchange, Electronic Data Interchange Outsourcing, Electronic Data Interchange Software, and Direct Electronic Data Interchange. By Industry, it covers BFSI, Retail and Consumer Goods, Healthcare, IT and Telecommunication, and Transportation and Logistics. By Component, it divides into Solution and Services. While exact segment shares are proprietary, Web-EDI and Outsourcing are gaining share due to lower TCO, while Healthcare and Transportation lead industry adoption due to regulatory and volume drivers. The overall market reaches 11.03 Billion in 2026.

What is the Global Europe Electronic Data Interchange (EDI) Market Size and Share by Region, showing geographic distribution?

The Europe EDI Market is a significant regional component of the global EDI landscape, with the provided data focusing specifically on Europe's valuation of 11.03 Billion in 2026 and 24.42 Billion forecast for 2033. Geographic distribution within Europe is led by Western European economies (Germany, UK, France, Benelux, Nordics) due to high industrial density, advanced logistics networks, and early regulatory adoption (e.g., PEPPOL). Eastern Europe shows accelerating growth from manufacturing nearshoring and EU-funded digitalization. Southern Europe adoption is driven by SME e-invoicing mandates. The 12.02% CAGR reflects broad-based regional expansion.

What is the Regional Analysis of the Europe Electronic Data Interchange (EDI) Market, detailing performance across European sub-regions?

Western Europe dominates with mature VAN and ERP-integrated EDI ecosystems, driven by automotive, retail, and pharma sectors. The DACH region (Germany, Austria, Switzerland) leads in Direct EDI and Industry 4.0 integration. Nordics excel in PEPPOL-based public procurement EDI. Southern Europe (Italy, Spain) sees rapid Web-EDI growth due to mandatory B2B e-invoicing. Eastern Europe (Poland, Czechia) benefits from logistics hub development and outsourcing demand. UK post-Brexit customs complexity fuels EDI in transportation. All regions contribute to the 12.02% CAGR toward 24.42 Billion by 2033.

Who are the Leading Company Profiles in the Europe Electronic Data Interchange (EDI) Market, and what are their strategies?

Key players include Cleo (ecosystem integration platform), Comarch SA (telecom/finance EDI), EDICOM (global compliance, PEPPOL), Generix Group (supply chain SaaS), IBM Corporation (Sterling B2B Integrator), Mulesoft LLC (API-led connectivity), SPS Commerce Inc. (retail-focused Fulfillment), The Descartes Systems Group Inc. (logistics network), TrueCommerce Inc. (SME-to-enterprise), and Unifiedpost Group (e-invoicing, FinTech). Strategies center on cloud-native platforms, pre-built industry maps, managed services, and ERP partnerships. Acquisitions target geographic expansion and vertical expertise. All align with the market's 12.02% CAGR trajectory toward 24.42 Billion.

What is the Porter's Five Forces Analysis of the Europe Electronic Data Interchange (EDI) Market?

Threat of new entrants is moderate: cloud lowers barriers but compliance certifications (PEPPOL, GDPR) and partner networks create moats. Bargaining power of buyers is high: many vendors, low switching costs for Web-EDI, but high for embedded VAN. Threat of substitutes (API, blockchain) is rising but EDI remains standard for high-volume, regulated B2B. Bargaining power of suppliers (network providers, ERP vendors) is moderate. Competitive rivalry is intense among the 10 key players, driving innovation in onboarding speed, error automation, and total cost of ownership reduction.

What is the SWOT Analysis of the Europe Electronic Data Interchange (EDI) Market?

Strengths: Established standards, regulatory tailwinds (e-invoicing mandates), high ROI from automation. Weaknesses: Legacy VAN complexity, perception as outdated tech, integration effort. Opportunities: Cloud/Web-EDI democratization for SMEs, API hybridization, sustainability reporting (CSRD), cross-border trade growth. Threats: API-first architectures displacing EDI in new integrations, cybersecurity risks, vendor lock-in concerns. The market's 12.02% CAGR to 24.42 Billion indicates strengths and opportunities outweigh weaknesses and threats, especially with solution modernization.

What is the Europe Electronic Data Interchange (EDI) Market Value Chain Analysis, describing industry structure and value flow?

The value chain comprises: Standards Bodies (GS1, UN/CEFACT, PEPPOL) → EDI Software Vendors (Cleo, Generix) → VAN/Network Providers (Descartes, SPS Commerce) → System Integrators (IBM, Mulesoft) → Industry-Specific Providers (EDICOM, TrueCommerce) → End-Users (BFSI, Retail, Healthcare, Transport). Value flows from document standardization through translation/mapping, secure transport, partner management, to ERP integration. Services (managed, consulting) capture increasing share. The chain is evolving toward platform ecosystems where vendors like Unifiedpost combine e-invoicing, financing, and compliance, enhancing value per transaction toward the 24.42 Billion forecast.

What are the Key Investment Insights in the Europe Electronic Data Interchange (EDI) Market?

Investment should target: 1) Cloud-native, multi-protocol platforms (EDI + API) for hybrid integration. 2) Vertical-specific compliance engines (healthcare HL7, automotive ODETTE, retail GS1). 3) AI/ML for auto-mapping, anomaly detection, and predictive supply chain analytics. 4) PEPPOL-certified access points for pan-European public procurement. 5) SME-focused Web-EDI and Outsourcing with low-code onboarding. 6) Embedded finance (dynamic discounting) via EDI data. The 12.02% CAGR to 24.42 Billion signals strong returns for solutions reducing TCO and accelerating partner onboarding.

What is the Europe Electronic Data Interchange (EDI) Market Conclusion, summarizing key takeaways?

The Europe EDI Market is a foundational digital infrastructure undergoing modernization. Driven by e-invoicing mandates, supply chain resilience needs, and cloud adoption, it is projected to grow from 11.03 Billion in 2026 to 24.42 Billion by 2033 at 12.02% CAGR. The shift from VAN to Web-EDI, Outsourcing, and API-hybrid models democratizes access for SMEs while meeting enterprise scalability. Key sectors—Retail, Healthcare, Transportation—lead adoption. Vendors investing in compliance automation, real-time visibility, and ecosystem integration will capture disproportionate value. EDI remains indispensable for structured, high-volume B2B exchange in Europe.

What is the Research Methodology used for this Europe Electronic Data Interchange (EDI) Market report?

The research employs a mixed-method approach: Primary research includes interviews with EDI vendors (Cleo, EDICOM, SPS Commerce), system integrators, end-users in retail/logistics/healthcare, and regulatory experts. Secondary research covers financial reports, EU directives (2014/55/EU, VAT in Digital Age), PEPPOL adoption data, industry association publications (GS1 Europe, EDIFICE), and proprietary databases. Market sizing uses bottom-up (vendor revenue aggregation) and top-down (IT spend allocation) triangulation. Forecasting incorporates driver-based modeling (mandate timelines, cloud migration rates, SME digitization indices) to derive the 12.02% CAGR and 24.42 Billion 2033 forecast.

What is the Research Scope and coverage limitations of this Europe Electronic Data Interchange (EDI) Market report?

The report covers the Europe EDI Market across 27 EU member states plus UK, Switzerland, Norway. It analyzes five deployment types (VAN, Web-EDI, Outsourcing, Software, Direct), five industry verticals (BFSI, Retail, Healthcare, IT/Telecom, Transport/Logistics), and two components (Solution, Services). The forecast period is 2027-2033 with 2026 base year (11.03 Billion). It profiles 10 key companies. Limitations: Excludes pure-play API management unless bundled with EDI; does not quantify informal/legacy FTP/AS2 exchanges; regional sub-segment shares are estimated; private company financials are approximated. The 12.02% CAGR reflects modeled assumptions.

Who are the Key Companies and what are the Recent Developments in the Europe Electronic Data Interchange (EDI) Market?

Key companies include Cleo (launch of Cleo Integration Cloud 24.1 with AI mapping), Comarch SA (PEPPOL Access Point expansion in CEE), EDICOM (new ViDA-compliant e-invoicing module), Generix Group (Generix Supply Chain Hub EDI+API), IBM Corporation (Sterling B2B Integrator on Red Hat OpenShift), Mulesoft LLC (Anypoint Platform EDI connector enhancements), SPS Commerce Inc. (Fulfillment EDI for omnichannel retail), The Descartes Systems Group Inc. (Descartes Global Logistics Network EDI expansion), TrueCommerce Inc. (Foundry platform for mid-market), Unifiedpost Group (Banqup e-invoicing/financing integration). Recent developments focus on cloud-native deployment, regulatory compliance automation (ViDA, CSRD), and embedded financial services.