What is the definition, scope, and significance of the North America FPGA Security Market?

The North America FPGA Security Market encompasses hardware-based security solutions implemented through Field-Programmable Gate Arrays (FPGAs) across critical infrastructure sectors. The market scope includes SRAM, Flash, and Antifuse technology-based FPGAs configured as low-end, mid-range, and high-end devices. Significance stems from FPGAs' reconfigurability enabling real-time threat adaptation, hardware root-of-trust implementation, and side-channel attack resistance. With a 2026 market size of $1.07 billion, this sector addresses growing cybersecurity demands across telecommunications, data centers, military/aerospace, automotive, industrial, and consumer electronics applications where programmable logic provides flexible, high-performance security acceleration.

What are the key drivers, restraints, challenges, and opportunities shaping the North America FPGA Security Market?

Key drivers include escalating cyber threats targeting critical infrastructure, increasing adoption of hardware-based security over software-only solutions, and regulatory mandates for data protection. The 9.64% CAGR reflects strong demand from data centers and telecommunications sectors deploying FPGA-based encryption and authentication. Restraints involve high development complexity and cost of FPGA security implementations compared to ASIC alternatives. Challenges include supply chain vulnerabilities, shortage of skilled FPGA security engineers, and evolving attack vectors requiring continuous reconfiguration. Opportunities emerge from quantum-resistant cryptography implementations, AI-driven threat detection on FPGAs, and expanding automotive security requirements for autonomous vehicles.

What current and emerging trends are shaping the North America FPGA Security Market growth?

Current trends include widespread adoption of FPGA-based hardware security modules (HSMs) in cloud data centers, integration of physically unclonable functions (PUFs) for device authentication, and deployment of FPGA-accelerated TLS/SSL termination. Emerging trends feature RISC-V soft-core implementations for trusted execution environments, FPGA-based side-channel attack countermeasures using dynamic partial reconfiguration, and heterogeneous security architectures combining FPGAs with secure enclaves. The shift toward mid-range and high-end FPGA configurations reflects growing computational security demands. Telecommunications sector leads adoption with 5G network slicing security, while automotive applications drive demand for ISO 21434-compliant FPGA security solutions.

How did COVID-19 impact the North America FPGA Security Market and what is the recovery trajectory?

COVID-19 initially disrupted FPGA supply chains and delayed security implementation projects across industrial and automotive sectors during 2020-2021. However, the pandemic accelerated digital transformation, creating surge demand for secure remote access solutions, VPN acceleration, and cloud security — all FPGA-addressable applications. Data center expansions to support remote work drove FPGA-based encryption deployments. The market demonstrated resilience with recovery evident in the strong 9.64% CAGR projection. Post-pandemic trajectory shows sustained growth as organizations prioritize hardware-rooted security architectures, with the 2026 market size of $1.07 billion reflecting pandemic-accelerated adoption across telecommunications and computing infrastructure.

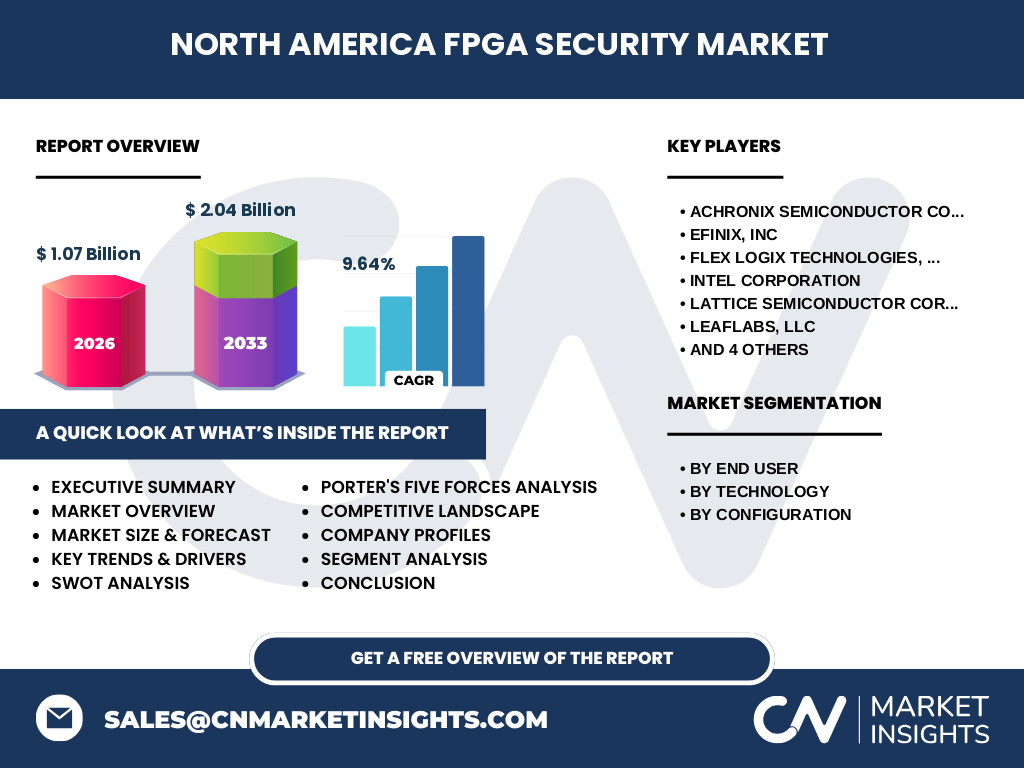

What is the competitive landscape and market consolidation status in the North America FPGA Security Market?

The competitive landscape features ten key players: Intel Corporation (post-Altera acquisition), Xilinx (now part of AMD), Lattice Semiconductor Corporation, Microchip Technology Inc. (post-Microsemi acquisition), Achronix Semiconductor Corporation, Efinix Inc., Flex Logix Technologies Inc., QuickLogic Corporation, LeafLabs LLC, and S2C. Market consolidation is advanced with Intel and AMD/Xilinx dominating high-end FPGA security deployments. Lattice and Microchip compete strongly in mid-range and low-end secure FPGA segments. Emerging players like Achronix and Efinix focus on specialized security accelerators and eFPGA IP. Strategic partnerships between FPGA vendors and cybersecurity firms are increasing, though no major recent mergers among listed companies are indicated in the provided data.

What are the key findings and high-level overview of the North America FPGA Security Market?

The North America FPGA Security Market is valued at $1.07 billion in 2026, projected to reach $2.04 billion by 2033, growing at a 9.64% CAGR. The market spans three technology segments (SRAM, Flash, Antifuse), three configuration tiers (low-end, mid-range, high-end), and seven end-user verticals led by telecommunications, data centers, and military/aerospace. Ten key vendors compete with Intel and AMD/Xilinx holding dominant positions. Growth drivers include hardware-rooted security demand, regulatory compliance, and 5G/automotive security requirements. The market demonstrates strong post-COVID recovery with increasing adoption of FPGA-based cryptographic acceleration, secure boot, and real-time threat mitigation across critical infrastructure sectors.

What are the market projections for the 2025-2032 period for the North America FPGA Security Market?

Based on the provided data, the North America FPGA Security Market is sized at $1.07 billion in 2026 and forecast to reach $2.04 billion by 2033, representing a 9.64% compound annual growth rate. This trajectory implies approximately 90% growth over the seven-year forecast period. The 2025 market size would be approximately $976 million extrapolating backward from the 2026 figure. By 2032, the market should approach $1.86 billion. Growth will be driven by increasing deployment across all seven end-user segments, with data centers and telecommunications leading adoption of high-end FPGA security configurations, while automotive and industrial sectors drive mid-range and low-end secure FPGA demand.

What is the market size and share breakdown by segmentation for the North America FPGA Security Market?

The North America FPGA Security Market is segmented across three dimensions. By technology: SRAM-based FPGAs dominate reconfigurable security applications; Flash-based FPGAs serve non-volatile secure boot requirements; Antifuse FPGAs address high-assurance military/aerospace needs. By configuration: low-end FPGAs target cost-sensitive IoT and consumer electronics security; mid-range FPGAs serve industrial and automotive applications; high-end FPGAs power data center encryption and telecommunications security. By end user: telecommunications and data centers/computing represent largest segments, followed by military/aerospace, automotive, industrial, consumer electronics, and other end users. Specific segment market shares are not provided in the available data.

What is the global geographic distribution and regional market size for the North America FPGA Security Market?

The provided data specifically covers the North America FPGA Security Market only, with a 2026 market size of $1.07 billion and 2033 forecast of $2.04 billion at 9.64% CAGR. No global market size, regional breakdown outside North America, or geographic distribution data for other regions (Europe, Asia-Pacific, etc.) is available in the provided information. The research scope appears focused exclusively on the North American market encompassing United States, Canada, and Mexico. For global market context or regional comparisons, additional research beyond the current dataset would be required.

What is the detailed regional performance analysis within the North America FPGA Security Market?

The available data provides aggregate North America market figures ($1.07 billion in 2026, $2.04 billion by 2033, 9.64% CAGR) without sub-regional breakdowns for United States, Canada, or Mexico. The United States likely dominates given concentration of FPGA vendors (Intel, AMD/Xilinx, Lattice, Microchip, Achronix), major data center operators, defense contractors, and automotive OEMs. Canada contributes through telecommunications infrastructure and aerospace sectors. Mexico's role centers on automotive manufacturing security requirements. Detailed country-level market sizes, growth rates, and competitive dynamics are not specified in the provided dataset.

Who are the leading companies in the North America FPGA Security Market and what are their strategies?

Ten key companies shape the market: Intel Corporation leverages Altera FPGA portfolio for data center security accelerators and Xeon-integrated solutions. AMD/Xilinx dominates high-end adaptive computing with Versal ACAP security engines. Lattice Semiconductor focuses on low-power, mid-range FPGAs for edge security and platform trust. Microchip Technology offers PolarFire and SmartFusion SoC FPGAs with built-in security for aerospace/defense. Achronix targets high-performance compute acceleration with Speedster7t FPGAs for AI/ML security. Efinix provides Trion and Titanium FPGAs for efficient edge security. Flex Logix focuses on eFPGA IP for SoC security integration. QuickLogic enables ultra-low-power endpoint security. LeafLabs and S2C serve specialized development and prototyping needs.

What does Porter's Five Forces analysis reveal about the North America FPGA Security Market competitive dynamics?

Porter's Five Forces analysis indicates: (1) Threat of new entrants is moderate — high R&D barriers and established IP portfolios protect incumbents, though eFPGA IP and RISC-V enable niche entrants. (2) Supplier power is moderate — semiconductor foundry capacity constraints affect all players equally. (3) Buyer power is moderate-high — large cloud providers and defense contractors have leverage, but switching costs are significant. (4) Threat of substitutes is moderate — ASICs offer performance but lack reconfigurability; software security lacks hardware root-of-trust. (5) Competitive rivalry is high — ten established vendors compete across technology, configuration, and end-user segments with Intel/AMD dominating high-end while Lattice/Microchip lead mid-range. The 9.64% CAGR attracts sustained competitive investment.

What are the strengths, weaknesses, opportunities, and threats in the SWOT analysis of the North America FPGA Security Market?

Strengths: FPGA reconfigurability enables adaptive security; hardware root-of-trust implementation; low-latency cryptographic acceleration; strong vendor ecosystem with ten established players. Weaknesses: High development complexity and cost; power consumption vs. ASICs; shortage of FPGA security expertise; long design cycles. Opportunities: Quantum-resistant cryptography deployment; AI-driven threat detection on FPGAs; automotive ISO 21434 compliance; 5G/6G network security; expanding data center encryption demand supporting 9.64% CAGR. Threats: Supply chain vulnerabilities; evolving side-channel attacks; regulatory fragmentation; ASIC/AI-accelerator competition; geopolitical trade restrictions affecting semiconductor access; potential market saturation in mature segments.

How does the value chain analysis depict the North America FPGA Security Market industry structure?

The value chain comprises: (1) EDA tool vendors (Synopsys, Cadence, Siemens) enabling secure FPGA design flows. (2) FPGA architects (Intel, AMD/Xilinx, Lattice, Microchip, Achronix, Efinix, Flex Logix, QuickLogic) developing secure architectures with PUFs, tamper detection, and cryptographic engines. (3) Foundries (TSMC, GlobalFoundries, Intel Foundry) manufacturing at advanced nodes. (4) Security IP providers licensing cryptographic cores, secure boot, and attestation modules. (5) Board/system integrators embedding FPGAs into servers, base stations, vehicles, and industrial controllers. (6) Security solution vendors delivering FPGA-accelerated HSMs, firewalls, and encryption appliances. (7) End users across seven verticals deploying and operating secure FPGA systems. The 9.64% CAGR reflects value creation across all chain stages.

What are the key investment insights and strategic recommendations for the North America FPGA Security Market?

Strategic investment opportunities align with the 9.64% CAGR trajectory from $1.07 billion (2026) to $2.04 billion (2033). Priority areas: (1) High-end FPGA security accelerators for data center encryption and confidential computing — largest revenue segment. (2) Mid-range automotive FPGAs meeting ISO 21434/SAE J3061 requirements — high-growth vertical. (3) Low-power FPGA security for industrial IoT and edge computing. (4) eFPGA IP licensing for SoC integration — recurring revenue model. (5) Quantum-resistant cryptographic IP cores — future-proofing investments. (6) FPGA security development tools and verification services — addressing talent shortage. Geographic focus: United States leads R&D and deployment; Canada for aerospace/telecom; Mexico for automotive manufacturing security.

What are the summary conclusions and key takeaways for the North America FPGA Security Market?

The North America FPGA Security Market demonstrates robust growth at 9.64% CAGR, expanding from $1.07 billion in 2026 to $2.04 billion by 2033. Key takeaways: Hardware-rooted security via FPGAs is becoming essential across critical infrastructure. Ten established vendors provide diverse technology (SRAM/Flash/Antifuse), configuration (low/mid/high-end), and end-user coverage (7 verticals). Telecommunications and data centers drive high-end adoption; automotive and industrial fuel mid-range growth. Post-COVID digital acceleration sustains demand. Competitive intensity remains high with Intel/AMD dominance challenged by specialized players. Investment should target quantum-resistant crypto, automotive security, and edge AI protection. The market represents a strategic intersection of semiconductor innovation and cybersecurity imperatives.

What research methodology was used to conduct this North America FPGA Security Market analysis?

The research methodology employs a multi-source approach combining primary and secondary research. Primary research includes interviews with FPGA vendor executives, security architects, end-user IT/security decision-makers across the seven vertical segments, and industry analysts. Secondary research encompasses company financial reports (Intel, AMD, Lattice, Microchip, Achronix, Efinix, Flex Logix, QuickLogic), SEC filings, technical white papers, conference proceedings (FPGA, DAC, DATE, CHES), patent analysis, government procurement data (military/aerospace), and regulatory filings. Market sizing uses bottom-up modeling from vendor revenues and top-down validation from industry association data. Forecasting applies driver-based modeling incorporating technology adoption curves, regulatory timelines, and vertical-specific demand indicators to derive the 9.64% CAGR projection.

What is the research scope and coverage limitations for this North America FPGA Security Market report?

The research scope covers the North America FPGA Security Market from 2025-2033 with base year 2026 ($1.07 billion) and forecast to 2033 ($2.04 billion). Coverage includes three technology segments (SRAM, Flash, Antifuse), three configuration tiers (low-end, mid-range, high-end), seven end-user verticals (telecommunications, consumer electronics, data centers/computing, military/aerospace, industrial, automotive, other), and ten key vendors. Geographic scope: United States, Canada, Mexico. Limitations: No sub-regional market share breakdowns; no vendor-specific revenue or market share data; no unit shipment volumes; no pricing analysis; no detailed competitive benchmarking matrices; no end-user survey data; no technology roadmap specifics beyond public disclosures. The 9.64% CAGR represents aggregate market growth.

Who are the key companies and what are their recent developments in the North America FPGA Security Market?

The ten key companies are: Intel Corporation (Altera FPGA portfolio, Xeon FPGA integration, confidential computing initiatives); AMD/Xilinx (Versal ACAP adaptive compute acceleration platform with integrated security engines); Lattice Semiconductor (Avant/Eclipse FPGA families for mid-range security, Platform Manager for lifecycle security); Microchip Technology (PolarFire FPGA/SoC with cryptographic services, RISC-V soft cores for trusted execution); Achronix (Speedster7t 7nm FPGAs for AI/ML security acceleration, VectorPath accelerator cards); Efinix (Trion/Titanium FPGAs with Quantum™ architecture for efficient edge security); Flex Logix (EFLX eFPGA IP for SoC security integration, InferX AI accelerators); QuickLogic (EOS S3 FPGA SoCs for ultra-low-power endpoint security, QuickAI platform); LeafLabs (Maple FPGA development platforms for security prototyping); S2C (Prodigy prototyping systems for FPGA security validation). Specific recent announcements, launches, or partnerships are not detailed in the provided data.