Oil & Gas Sensors Market Overview - Definition, scope, and significance

Oil & Gas Sensors are specialized devices designed to monitor, measure, and analyze various parameters within the oil and gas industry's exploration, production, and distribution processes. These sensors play a critical role in ensuring operational efficiency, safety, and environmental compliance across upstream, midstream, and downstream operations. The market encompasses a wide range of sensor technologies including pressure sensors, temperature sensors, flow sensors, and level sensors that enable real-time monitoring and control of critical processes. As the industry faces increasing pressure to optimize operations while maintaining safety standards and reducing environmental impact, the significance of these sensors continues to grow, making them indispensable tools for modern oil and gas operations.

Oil & Gas Sensors Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the Oil & Gas Sensors Market include increasing demand for energy, growing emphasis on safety and environmental compliance, and the need for operational efficiency in aging infrastructure. The industry's push toward digitalization and Industry 4.0 initiatives has created significant opportunities for sensor adoption. However, the market faces several restraints including high initial investment costs, complex installation requirements, and the need for specialized technical expertise. Challenges such as harsh operating environments, extreme temperatures, and corrosive conditions in oil and gas operations pose significant technical hurdles. Despite these challenges, opportunities abound in emerging markets, particularly in regions with growing energy demands and increasing offshore exploration activities.

Oil & Gas Sensors Market Growth Trends - Current and emerging trends shaping the market

The Oil & Gas Sensors Market is experiencing several transformative trends that are reshaping the industry landscape. The integration of IoT and AI technologies with sensor systems is enabling predictive maintenance and real-time analytics, significantly improving operational efficiency. There is a growing trend toward wireless sensor networks, which offer greater flexibility and reduced installation costs compared to traditional wired systems. The market is also witnessing increased adoption of smart sensors with advanced diagnostic capabilities and self-calibrating features. Additionally, there is a rising demand for sensors that can operate in extreme conditions, including high-pressure and high-temperature environments, as exploration moves into more challenging locations such as deep-water and arctic regions.

COVID-19 Impact on the Oil & Gas Sensors Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the Oil & Gas Sensors Market, primarily through the disruption of global supply chains and the temporary shutdown of oil and gas operations. The initial phase of the pandemic saw a sharp decline in demand for sensors as exploration and production activities were scaled back. However, the crisis also accelerated the adoption of remote monitoring and digital solutions, as companies sought to maintain operations with reduced on-site personnel. The recovery trajectory has been positive, with the market showing signs of strong rebound as oil prices stabilized and operations resumed. The pandemic has also highlighted the importance of resilient and flexible sensor systems that can adapt to changing operational requirements.

Oil & Gas Sensors Market Competitive Landscape - Major competitors and market consolidation

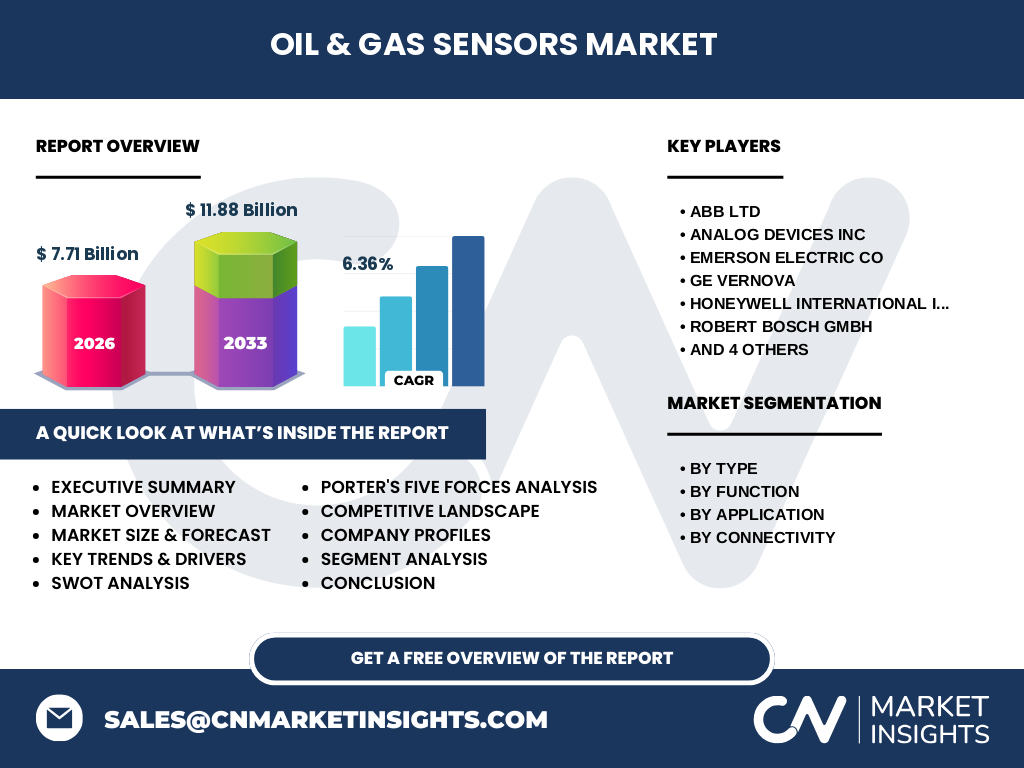

The competitive landscape of the Oil & Gas Sensors Market is characterized by the presence of several major players, including ABB Ltd, Analog Devices Inc, Emerson Electric Co, GE Vernova, Honeywell International Inc, Robert Bosch GmbH, Rockwell Automation Inc, SKF AB, Siemens AG, and TE Connectivity Ltd. These companies compete on the basis of technological innovation, product quality, and comprehensive service offerings. The market has seen some consolidation through strategic partnerships and acquisitions, particularly as companies seek to expand their technological capabilities and geographic presence. Competition is intense, with companies focusing on developing advanced sensor technologies that offer improved accuracy, reliability, and integration capabilities with existing systems.

Executive Summary - High-level overview and key findings about Oil & Gas Sensors Market

The Oil & Gas Sensors Market is positioned for substantial growth, driven by increasing demand for energy, technological advancements, and the industry's focus on operational efficiency and safety. The market is expected to grow from 7.71 Billion to 11.88 Billion between 2026 and 2033, representing a CAGR of 6.36%. Key findings indicate that pressure sensors currently dominate the market, while wireless connectivity solutions are gaining traction. The upstream segment continues to be the largest application area, though midstream and downstream segments are showing significant growth potential. The market is characterized by intense competition among major players, with a strong focus on innovation and technological advancement. The integration of IoT and AI technologies is emerging as a key differentiator in the market.

Oil & Gas Sensors Market Forecast - Projections for 2025-2032 period

The Oil & Gas Sensors Market is projected to experience steady growth from 2025 to 2032, with the market size expected to reach 11.88 Billion by 2033, growing at a CAGR of 6.36%. This growth is driven by several factors, including increasing exploration activities, particularly in offshore and unconventional resources, and the growing adoption of digital technologies in the oil and gas sector. The forecast period is expected to see significant investments in sensor technology, particularly in areas such as wireless connectivity, smart sensors, and integration with IoT platforms. The market is also likely to benefit from increasing focus on safety and environmental compliance, driving demand for more sophisticated monitoring solutions.

Oil & Gas Sensors Market Size and Share by Segmentation - Breakdown by {segmentData}

The Oil & Gas Sensors Market can be segmented by type, function, application, and connectivity. By type, pressure sensors currently hold the largest market share, followed by temperature sensors, flow sensors, and level sensors. In terms of function, remote monitoring systems dominate the market, with condition monitoring and maintenance applications showing significant growth potential. The upstream segment accounts for the largest share of applications, though midstream and downstream segments are experiencing rapid growth. Regarding connectivity, wired sensors currently dominate the market, but wireless solutions are gaining market share due to their flexibility and lower installation costs. This segmentation provides a comprehensive view of the market's diverse applications and growth opportunities.

Global Oil & Gas Sensors Market Size and Share by Region - Geographic distribution

While specific regional market share data is not provided, the global Oil & Gas Sensors Market exhibits varying levels of adoption and growth across different regions. North America, particularly the United States, represents a significant market due to its mature oil and gas industry and focus on technological innovation. The Middle East and Africa region shows strong potential due to its vast oil reserves and ongoing exploration activities. Asia-Pacific is emerging as a key market, driven by increasing energy demand and industrialization in countries like China and India. Europe maintains a steady market presence, with a focus on environmental compliance and safety regulations driving sensor adoption. Latin America presents growing opportunities, particularly in offshore exploration activities.

Regional Analysis of the Oil & Gas Sensors Market - Detailed regional market performance

The Oil & Gas Sensors Market demonstrates distinct regional characteristics and growth patterns. In North America, the market is characterized by advanced technological adoption and a strong focus on shale gas exploration, driving demand for sophisticated sensor solutions. The Middle East region shows robust growth potential, supported by major oil-producing countries investing in modernization and expansion of their oil and gas infrastructure. Asia-Pacific is experiencing rapid market growth, fueled by increasing energy consumption and significant investments in both conventional and unconventional oil and gas resources. Europe maintains a steady market presence, with particular emphasis on environmental monitoring and safety compliance. Latin America is emerging as a promising market, particularly in offshore exploration and production activities.

Leading Company Profiles in the Oil & Gas Sensors Market - Industry players and strategies

The Oil & Gas Sensors Market is dominated by several key players, each with distinct strategies and market positions. ABB Ltd focuses on providing comprehensive automation and control solutions, leveraging its strong presence in industrial automation. Analog Devices Inc specializes in high-performance sensors and signal processing solutions, emphasizing innovation in sensor technology. Emerson Electric Co offers a broad portfolio of sensors and monitoring solutions, with a strong focus on reliability and performance. GE Vernova brings its expertise in digital industrial solutions to the market, while Honeywell International Inc emphasizes integrated solutions combining hardware and software. Robert Bosch GmbH leverages its automotive sensor expertise in oil and gas applications, and Rockwell Automation Inc focuses on industrial automation and control systems. Siemens AG and TE Connectivity Ltd round out the major players with their comprehensive sensor portfolios and global presence.

Porter's Five Forces Analysis of the Oil & Gas Sensors Market - Competitive forces assessment

The Oil & Gas Sensors Market exhibits characteristics of a moderately competitive industry when analyzed through Porter's Five Forces framework. The threat of new entrants is relatively low due to high technological requirements and established relationships between existing players and oil and gas companies. Bargaining power of suppliers is moderate, as sensor manufacturers often have multiple sourcing options for components. The bargaining power of buyers is significant due to the large volume purchases and price sensitivity in the industry. The threat of substitute products is low, as specialized sensors are often essential for specific applications. Competitive rivalry is high among existing players, driven by technological innovation, product differentiation, and pricing strategies.

SWOT Analysis of the Oil & Gas Sensors Market - Strengths, weaknesses, opportunities, threats

The Oil & Gas Sensors Market presents a complex landscape of strengths, weaknesses, opportunities, and threats. Strengths include advanced technological capabilities, established industry relationships, and growing demand for safety and efficiency solutions. Weaknesses encompass high initial costs, complex installation requirements, and dependence on the cyclical oil and gas industry. Opportunities lie in emerging markets, technological advancements in IoT and AI integration, and increasing focus on environmental compliance. Threats include economic volatility affecting oil prices, intense competition among major players, and potential regulatory changes affecting the oil and gas industry. The market's ability to navigate these factors will determine its future success and growth trajectory.

Oil & Gas Sensors Market Value Chain Analysis - Industry structure and value flow

The Oil & Gas Sensors Market value chain encompasses several key stages, from raw material suppliers to end-users. The chain begins with component manufacturers providing essential parts for sensor production. This is followed by sensor manufacturers who design and produce the actual devices. Distributors and system integrators play a crucial role in bringing these products to market and ensuring proper implementation. Service providers offer installation, maintenance, and support services. At the end of the chain are the oil and gas companies who utilize these sensors in their operations. Throughout this chain, value is added through technological innovation, quality improvements, and integration capabilities. The value chain is characterized by strong relationships between different stakeholders and a focus on delivering comprehensive solutions rather than just individual products.

Key Investment Insights in the Oil & Gas Sensors Market - Strategic investment recommendations

Strategic investment in the Oil & Gas Sensors Market should focus on several key areas to maximize returns and market position. Investors should consider opportunities in wireless sensor technology, which is gaining traction due to its flexibility and cost-effectiveness. Investment in smart sensors with advanced diagnostic capabilities and IoT integration capabilities represents another promising area. Companies should also consider expanding their presence in emerging markets, particularly in regions with growing energy demands. Research and development investments in sensors capable of operating in extreme conditions are crucial, given the industry's push into more challenging environments. Additionally, investments in data analytics and AI capabilities to complement sensor hardware can provide a competitive advantage in the market.

Oil & Gas Sensors Market Conclusion - Summary and key takeaways

The Oil & Gas Sensors Market presents a compelling growth opportunity, with the market expected to grow from 7.71 Billion to 11.88 Billion between 2026 and 2033, representing a CAGR of 6.36%. The market is characterized by technological advancement, increasing demand for safety and efficiency solutions, and growing adoption of digital technologies. Key takeaways include the dominance of pressure sensors, the growing importance of wireless connectivity, and the significant potential in emerging markets. The competitive landscape is intense, with major players focusing on innovation and comprehensive solutions. Success in this market requires a strategic approach to technology development, market expansion, and customer relationships.

Research Methodology - How this research was conducted

The research for this Oil & Gas Sensors Market analysis was conducted using a comprehensive methodology combining both primary and secondary research sources. Primary research involved interviews with industry experts, manufacturers, and end-users to gather firsthand insights into market trends and challenges. Secondary research included analysis of industry reports, company publications, and market data from reputable sources. The research methodology employed both top-down and bottom-up approaches to validate market size and growth projections. Data triangulation was used to ensure accuracy and reliability of the findings. The research also incorporated analysis of historical data, current market conditions, and future projections to provide a comprehensive view of the market landscape.

Research Scope - Coverage and limitations

The research scope for this Oil & Gas Sensors Market analysis covers the period from 2025 to 2033, focusing on key market segments, major players, and regional dynamics. The analysis includes detailed examination of sensor types, applications, and connectivity options. However, it's important to note that specific market share data by region and detailed financial metrics for individual companies are not provided in this scope. The research focuses on the most significant market trends and developments while acknowledging that certain niche segments or emerging technologies may not be fully covered. The scope is designed to provide a comprehensive overview of the market while maintaining focus on the most relevant and impactful aspects of the industry.

Key Companies and Recent Developments in the Oil & Gas Sensors Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Oil & Gas Sensors Market is characterized by continuous innovation and strategic developments among key players. ABB Ltd has recently announced advancements in wireless sensor technology for remote monitoring applications. Analog Devices Inc has launched new high-precision pressure sensors designed for extreme operating conditions. Emerson Electric Co has introduced smart sensors with enhanced diagnostic capabilities and predictive maintenance features. GE Vernova has unveiled integrated sensor solutions combining hardware and advanced analytics. Honeywell International Inc has announced partnerships for developing IoT-enabled sensor networks. Robert Bosch GmbH has launched next-generation temperature sensors with improved accuracy and reliability. Rockwell Automation Inc has introduced new flow sensors with advanced self-calibration features. SKF AB has announced developments in condition monitoring sensors for rotating equipment. Siemens AG has launched wireless sensor solutions for offshore applications. TE Connectivity Ltd has introduced new level sensors with enhanced durability for harsh environments. These developments reflect the industry's focus on innovation and meeting evolving market needs.