Software Defined Networking (SDN) Market Overview - Definition, scope, and significance

Software Defined Networking (SDN) represents a transformative approach to network architecture that decouples the control plane from the data plane, enabling centralized network intelligence and programmability. This innovative framework allows network administrators to manage network services through abstraction of lower-level functionality, providing unprecedented flexibility and control over network infrastructure. The SDN market encompasses a comprehensive ecosystem of hardware, software, and services designed to modernize traditional networking paradigms. As organizations increasingly demand agile, scalable, and cost-effective network solutions, SDN has emerged as a critical technology for enabling digital transformation across industries. The significance of SDN lies in its ability to address the limitations of conventional networking by offering dynamic resource allocation, simplified management, and enhanced security capabilities that align with the evolving needs of cloud computing, IoT, and 5G technologies.

Software Defined Networking (SDN) Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The SDN market is propelled by several compelling drivers, including the escalating demand for network automation, the proliferation of cloud-based services, and the need for enhanced network security and performance. Organizations are increasingly adopting SDN to reduce operational costs, improve network agility, and support emerging technologies such as IoT and edge computing. However, the market faces significant restraints, including the complexity of migration from legacy systems, concerns about vendor lock-in, and the shortage of skilled professionals capable of managing SDN environments. Challenges persist in terms of interoperability between different vendor solutions and the need for standardization across the industry. Despite these obstacles, substantial opportunities exist in the form of 5G network deployment, the expansion of data center virtualization, and the growing adoption of hybrid cloud architectures. The increasing focus on network security and the demand for real-time analytics present additional avenues for market growth and innovation.

Software Defined Networking (SDN) Market Growth Trends - Current and emerging trends shaping the market

The SDN market is experiencing several transformative trends that are reshaping the networking landscape. One prominent trend is the convergence of SDN with Network Functions Virtualization (NFV), creating more flexible and efficient network architectures that support both enterprise and service provider requirements. Another significant trend is the increasing adoption of intent-based networking, where networks can automatically configure themselves based on predefined business policies and objectives. The rise of edge computing is driving demand for distributed SDN architectures that can manage networks across multiple locations with centralized control. Additionally, the integration of artificial intelligence and machine learning into SDN platforms is enabling predictive analytics, automated troubleshooting, and intelligent traffic management. The market is also witnessing a shift toward open-source SDN solutions, with initiatives like OpenFlow and ONOS gaining traction among organizations seeking vendor-agnostic alternatives. These trends collectively indicate a movement toward more intelligent, automated, and open networking ecosystems that can adapt to rapidly changing business requirements.

COVID-19 Impact on the Software Defined Networking (SDN) Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic has had a profound impact on the SDN market, accelerating digital transformation initiatives across industries as organizations rapidly adapted to remote work models and increased reliance on cloud services. The pandemic exposed the limitations of traditional network architectures, driving organizations to invest in SDN solutions that could provide the agility and scalability needed to support distributed workforces and surge in digital traffic. While the initial phase of the pandemic caused supply chain disruptions and project delays, the long-term effect has been overwhelmingly positive for the SDN market. Organizations recognized the critical importance of flexible, programmable networks that could quickly adapt to changing business conditions. The recovery trajectory has been robust, with increased budget allocations for network modernization and a heightened focus on building resilient IT infrastructures. The pandemic has effectively served as a catalyst for SDN adoption, demonstrating the technology's value in enabling business continuity and supporting the new normal of hybrid work environments.

Software Defined Networking (SDN) Market Competitive Landscape - Major competitors and market consolidation

The SDN market features a dynamic competitive landscape characterized by a mix of established networking giants, innovative startups, and specialized solution providers. Major players such as Cisco Systems, VMware, and Huawei Technologies dominate the market with comprehensive SDN portfolios that span hardware, software, and services. These industry leaders are engaged in continuous innovation and strategic partnerships to maintain their market positions and expand their technological capabilities. The market has witnessed significant consolidation through mergers and acquisitions, as larger companies acquire innovative startups to enhance their SDN offerings and gain competitive advantages. Emerging players like Cumulus Networks and Big Switch Networks are challenging incumbents by offering open-source and cloud-native SDN solutions that appeal to organizations seeking greater flexibility and cost-effectiveness. The competitive dynamics are further intensified by the growing importance of interoperability and open standards, forcing vendors to collaborate while simultaneously competing for market share. This competitive environment is driving rapid technological advancement and creating a diverse ecosystem of solutions that cater to various industry verticals and use cases.

Executive Summary - High-level overview and key findings about Software Defined Networking (SDN) Market

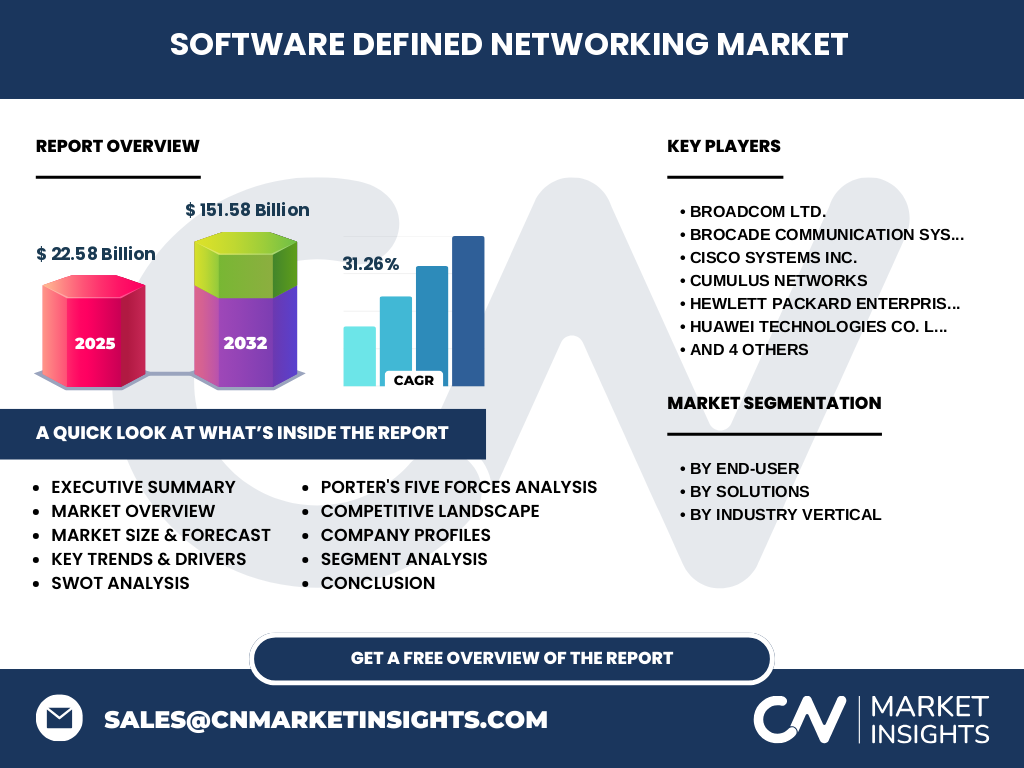

The Software Defined Networking market is experiencing unprecedented growth, driven by the increasing demand for agile, scalable, and intelligent network infrastructures across industries. With a projected market size of $22.58 billion in 2025 and an impressive CAGR of 31.26% through 2032, the SDN market represents a significant opportunity for technology providers and investors alike. The market's expansion is fueled by the convergence of several technological trends, including cloud computing, 5G deployment, and the Internet of Things, which collectively demand more flexible and programmable network architectures. Enterprise adoption is particularly strong, with organizations recognizing SDN's potential to reduce operational costs, enhance security, and improve network performance. The market is characterized by rapid innovation, with vendors continuously enhancing their offerings to address emerging use cases and industry-specific requirements. As organizations increasingly prioritize digital transformation and network modernization, SDN has evolved from a niche technology to a mainstream networking solution that is fundamentally reshaping how networks are designed, deployed, and managed.

Software Defined Networking (SDN) Market Forecast - Projections for 2025-2032 period

The SDN market is poised for remarkable growth over the forecast period from 2025 to 2032, with projections indicating a substantial expansion from $22.58 billion to $151.58 billion. This exceptional growth trajectory, representing a CAGR of 31.26%, reflects the accelerating adoption of SDN solutions across various industry verticals and use cases. The forecast period will be characterized by several key developments, including the widespread deployment of 5G networks, which will create significant demand for SDN-enabled infrastructure capable of supporting ultra-low latency and high-bandwidth applications. The continued growth of cloud computing and edge computing will further drive SDN adoption, as organizations seek to optimize their network architectures for distributed computing environments. Additionally, the increasing focus on network security and compliance requirements will propel demand for SDN solutions that offer enhanced visibility and control over network traffic. The forecast also anticipates the maturation of open-source SDN initiatives, which will contribute to market growth by reducing barriers to entry and fostering innovation through community-driven development.

Software Defined Networking (SDN) Market Size and Share by Segmentation - Breakdown by {segmentData}

The SDN market exhibits diverse segmentation across end-users, solutions, and industry verticals, each contributing uniquely to the overall market dynamics. In terms of end-users, enterprises represent the largest segment, driven by the need for network modernization and digital transformation initiatives. Telecommunication service providers constitute another significant segment, leveraging SDN to optimize their network infrastructure and support emerging technologies like 5G. Cloud service providers are increasingly adopting SDN solutions to enhance their service offerings and improve operational efficiency. Regarding solutions, virtualization/control software commands a substantial market share, as organizations prioritize software-based network management capabilities. Physical network infrastructure, while representing a smaller segment, remains critical for enabling SDN deployments. The industry vertical segmentation reveals that the banking, financial services, and insurance sector leads adoption due to stringent security requirements and the need for high-performance networks. Telecommunication and IT follow closely, driven by the demand for scalable and flexible network architectures to support digital services and content delivery.

Global Software Defined Networking (SDN) Market Size and Share by Region - Geographic distribution

The global SDN market demonstrates varied adoption patterns across different regions, reflecting diverse technological maturity, regulatory environments, and economic conditions. North America currently leads the market, driven by early technology adoption, the presence of major technology vendors, and significant investments in cloud infrastructure and 5G deployment. The region's strong enterprise sector and focus on digital transformation initiatives contribute to its dominant market position. Europe represents the second-largest market, characterized by robust adoption in countries like Germany, the United Kingdom, and France, where organizations are increasingly investing in network modernization to support Industry 4.0 initiatives and comply with data sovereignty regulations. The Asia-Pacific region is emerging as the fastest-growing market, fueled by rapid digitalization, expanding telecommunications infrastructure, and the proliferation of cloud services in countries such as China, Japan, and India. The region's growing manufacturing sector and increasing adoption of IoT technologies are creating substantial demand for SDN solutions. Latin America and the Middle East & Africa regions, while currently representing smaller market shares, are experiencing growing interest in SDN as organizations recognize the technology's potential to address their networking challenges and support economic development initiatives.

Regional Analysis of the Software Defined Networking (SDN) Market - Detailed regional market performance

Regional analysis of the SDN market reveals distinct adoption patterns and growth drivers across different geographic areas. In North America, the market is characterized by mature adoption, with enterprises and service providers leading implementation efforts. The region benefits from a robust technology ecosystem, significant R&D investments, and favorable regulatory frameworks that encourage innovation. European markets demonstrate strong adoption in Northern and Western European countries, where digital transformation initiatives and strict data protection regulations drive demand for sophisticated networking solutions. The region's focus on sustainability and energy efficiency is also influencing SDN adoption, as organizations seek to optimize their network infrastructure for reduced power consumption. The Asia-Pacific region presents a dynamic market landscape, with developed economies like Japan and South Korea showcasing advanced SDN deployments, while emerging economies in Southeast Asia are rapidly catching up. The region's diverse economic conditions create opportunities for both high-end enterprise solutions and cost-effective implementations tailored to local requirements. Regional variations in network infrastructure maturity, IT spending patterns, and regulatory environments significantly influence SDN adoption rates and implementation strategies across different markets.

Leading Company Profiles in the Software Defined Networking (SDN) Market - Industry players and strategies

The SDN market features several prominent companies that are shaping the industry through innovative solutions and strategic initiatives. Cisco Systems Inc. stands as a market leader, offering a comprehensive SDN portfolio that includes hardware, software, and services designed to address enterprise and service provider requirements. The company's strategy focuses on providing end-to-end solutions that integrate seamlessly with existing infrastructure while offering advanced capabilities for network automation and security. VMware has established itself as a key player through its NSX platform, which provides software-defined networking and security solutions that are particularly well-suited for virtualized environments and cloud deployments. The company's approach emphasizes the convergence of networking and security to create integrated solutions for modern data centers. Hewlett Packard Enterprise has developed a strong position in the market through its Composable Infrastructure strategy, which combines SDN with compute and storage resources to create flexible, scalable IT environments. Huawei Technologies Co. Ltd. has gained significant market share, particularly in the Asia-Pacific region, by offering cost-effective SDN solutions that cater to both enterprise and service provider markets. These companies, along with other key players like Juniper Networks and Broadcom Ltd., are continuously innovating and forming strategic partnerships to expand their market presence and address evolving customer needs.

Porter's Five Forces Analysis of the Software Defined Networking (SDN) Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the SDN market. The threat of new entrants remains moderate, as the market requires significant capital investment, technical expertise, and established distribution channels to compete effectively with incumbent players. However, the growing popularity of open-source solutions is lowering barriers to entry for smaller companies and startups that can innovate quickly and address niche market segments. The bargaining power of buyers is increasing as organizations become more knowledgeable about SDN technologies and demand greater customization and interoperability from vendors. This trend is driving vendors to offer more flexible solutions and competitive pricing to maintain customer relationships. The bargaining power of suppliers is relatively low for software components but moderate for specialized hardware components, as a few key manufacturers dominate the supply of network infrastructure equipment. The threat of substitute technologies remains low, as SDN continues to evolve and address limitations of traditional networking approaches. Competitive rivalry is intense, with established players competing on technological innovation, product features, pricing, and customer service, while also engaging in strategic partnerships and acquisitions to strengthen their market positions.

SWOT analysis of the SDN market reveals critical insights into its internal strengths and weaknesses, as well as external opportunities and threats. The market's primary strengths include the technology's ability to provide unprecedented network flexibility, scalability, and programmability, which directly addresses the evolving needs of modern digital enterprises. SDN's centralized control architecture enables efficient network management and reduces operational complexity, while its support for automation and orchestration aligns with broader IT modernization initiatives. However, the market faces notable weaknesses, including the complexity of implementation and migration from legacy systems, which can deter adoption among organizations with limited technical resources. The shortage of skilled professionals capable of designing and managing SDN environments represents another significant weakness that could constrain market growth. External opportunities abound in the form of 5G network deployment, edge computing expansion, and the increasing adoption of hybrid cloud architectures, all of which require the advanced networking capabilities that SDN provides. Threats to the market include potential security vulnerabilities associated with centralized control architectures, the risk of vendor lock-in with proprietary solutions, and the ongoing challenge of achieving true interoperability between different vendor implementations. Additionally, the market faces threats from evolving regulatory requirements and compliance standards that may impact SDN deployment strategies across different regions and industries.

Software Defined Networking (SDN) Market Value Chain Analysis - Industry structure and value flow

The SDN market value chain encompasses a complex ecosystem of stakeholders that contribute to the development, deployment, and maintenance of SDN solutions. At the foundation of the value chain are semiconductor and hardware component manufacturers who provide the essential building blocks for SDN infrastructure, including specialized processors, network interface cards, and switching equipment. Network equipment vendors then integrate these components into SDN-capable hardware platforms that form the physical layer of SDN deployments. Software developers and platform providers create the control plane software, management applications, and orchestration tools that enable the programmability and automation features that define SDN. System integrators and solution providers play a crucial role in bridging the gap between technology vendors and end-users, offering consulting, implementation, and support services that ensure successful SDN deployments. Value-added resellers and distributors facilitate market access and provide localized support to customers across different regions. At the apex of the value chain are end-users across various industry verticals who derive value from SDN through improved network performance, reduced operational costs, and enhanced business agility. The value chain is characterized by increasing collaboration and partnership among stakeholders to create integrated solutions that address complex customer requirements and drive market growth.

Key Investment Insights in the Software Defined Networking (SDN) Market - Strategic investment recommendations

The SDN market presents compelling investment opportunities driven by its strong growth trajectory and transformative potential across industries. Strategic investors should focus on companies that demonstrate technological leadership in key areas such as network automation, security integration, and cloud-native architectures. The convergence of SDN with emerging technologies like 5G, edge computing, and artificial intelligence represents particularly attractive investment themes, as these synergies are likely to create new market opportunities and drive innovation. Investors should also consider the growing importance of open-source SDN solutions and platforms that support interoperability and avoid vendor lock-in, as these approaches are gaining traction among enterprise customers. The market's regional dynamics offer diversification opportunities, with the Asia-Pacific region showing particularly strong growth potential due to rapid digitalization and infrastructure development. Strategic investments in companies that offer comprehensive solutions spanning hardware, software, and services are likely to yield strong returns, as customers increasingly prefer integrated offerings that address their complete networking needs. Additionally, companies that demonstrate strong partnerships with cloud service providers and telecommunications operators are well-positioned to capitalize on the growing demand for SDN-enabled services and infrastructure.

Software Defined Networking (SDN) Market Conclusion - Summary and key takeaways

The Software Defined Networking market stands at the forefront of networking innovation, offering transformative solutions that address the evolving demands of modern digital enterprises. With a projected market size of $151.58 billion by 2032 and a robust CAGR of 31.26%, the SDN market represents a significant technological and economic opportunity. The market's growth is driven by the increasing need for network agility, the proliferation of cloud services, and the deployment of emerging technologies such as 5G and IoT. While challenges exist in terms of implementation complexity and skills shortages, the market's strengths and opportunities far outweigh its weaknesses and threats. The competitive landscape is dynamic, with established players and innovative startups continuously pushing the boundaries of what's possible with SDN technology. As organizations across industries recognize the strategic value of programmable, intelligent networks, SDN adoption will continue to accelerate, fundamentally reshaping how networks are designed, deployed, and managed. The market's future success will depend on continued innovation, standardization efforts, and the ability to address evolving customer needs in an increasingly complex and interconnected digital world.

Research Methodology - How this research was conducted

This comprehensive market research was conducted using a rigorous methodology that combines multiple data collection and analysis techniques to ensure accuracy and reliability. The research process began with extensive secondary research, including analysis of industry reports, company financial statements, technical publications, and market databases to establish a foundational understanding of the SDN market landscape. Primary research was then conducted through interviews with industry experts, technology vendors, and end-users to validate findings and gain insights into market trends, challenges, and opportunities. The research methodology employed both top-down and bottom-up approaches to estimate market size and forecast growth, triangulating data from multiple sources to ensure accuracy. Market segmentation analysis was performed using detailed classification criteria based on end-users, solutions, and industry verticals, with each segment analyzed for growth potential and market dynamics. Regional analysis incorporated economic indicators, technology adoption rates, and regulatory environments to provide a comprehensive geographic perspective. The research also included competitive analysis through Porter's Five Forces framework and SWOT analysis to understand market structure and competitive dynamics. All data was subjected to rigorous validation processes, including cross-verification with multiple sources and expert review, to ensure the highest level of accuracy and reliability in the final market assessment.

Research Scope - Coverage and limitations

This research report provides comprehensive coverage of the global Software Defined Networking market, encompassing market size analysis, growth forecasts, segmentation by end-users, solutions, and industry verticals, as well as regional market dynamics. The scope includes detailed analysis of market drivers, restraints, challenges, and opportunities, along with competitive landscape assessment and strategic recommendations for stakeholders. The research covers the period from 2025 to 2032, with particular focus on the forecast period and emerging trends that will shape market development. The report examines key companies operating in the market, their strategies, and recent developments, providing insights into competitive positioning and market dynamics. However, the research has certain limitations, including the availability of granular data for specific sub-segments and regional markets, particularly in developing economies where market information may be less readily accessible. Additionally, the rapidly evolving nature of SDN technology means that some emerging trends and use cases may not be fully captured in the current analysis. The research also focuses primarily on commercial SDN deployments and may not fully account for experimental or academic implementations that could influence future market development.

Key Companies and Recent Developments in the Software Defined Networking (SDN) Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The SDN market features several key companies that are driving innovation and shaping industry trends through strategic initiatives and technological advancements. Cisco Systems Inc. has recently announced enhanced SDN capabilities within its Catalyst portfolio, focusing on improved automation and security integration for enterprise networks. The company has also formed strategic partnerships with major cloud providers to expand its SDN offerings in hybrid cloud environments. VMware continues to strengthen its position with the launch of new features in its NSX platform, including enhanced support for multi-cloud deployments and improved integration with container orchestration platforms. The company's recent acquisition of networking startups has expanded its capabilities in edge computing and 5G network slicing. Hewlett Packard Enterprise has made significant strides with its Composable Infrastructure strategy, introducing new SDN-enabled solutions that provide greater flexibility for enterprise data centers. The company's partnership with major telecommunications operators aims to accelerate 5G network deployment using SDN technologies. Huawei Technologies Co. Ltd. has announced advancements in its CloudFabric solution, focusing on AI-driven network optimization and enhanced security features for enterprise customers. The company's recent collaborations with regional telecommunications providers demonstrate its commitment to expanding SDN adoption in emerging markets. These developments, along with initiatives from other key players like Juniper Networks and Broadcom Ltd., highlight the dynamic nature of the SDN market and the continuous innovation driving its growth.