What is the Europe Used Car Market Overview – definition, scope, and significance?

The Europe Used Car Market comprises the buying, selling, and financing of pre‑owned passenger vehicles across European territories. It includes a broad range of vehicle categories—hatchbacks, sedans, SUVs, pickups, vans, MPVs and others—distributed through organized dealers, online platforms, and unorganized brokers. The market is segmented by fuel type (gasoline, diesel, BEV, HEV/PHEV, and others), vehicle age, price band, ownership count, and financing structure (financed vs outright purchase). With a 2026 valuation of USD 64.17 billion, the market is a pivotal component of the regional automotive ecosystem, supporting circular economy goals, providing affordable mobility, and generating substantial revenue for dealers, leasing firms, and ancillary services.

What are the key drivers, restraints, challenges, and opportunities in the Europe Used Car Market?

Key drivers include growing demand for cost‑effective mobility, stricter new‑car emissions regulations that accelerate vehicle turnover, and the expansion of digital sales platforms that enhance market transparency. Restraints stem from fluctuating fuel prices, tightening credit conditions, and regulatory uncertainty around low‑emission zones that may depress demand for diesel‑powered used cars. Challenges involve the integration of electric vehicles into the used segment—limited charging infrastructure and residual value concerns hinder rapid adoption. Opportunities arise from the rising share of BEVs and HEV/PHEVs in the used pool, increased financing solutions from firms like ALD Automotive and LeasePlan, and the consolidation of fragmented broker networks into technology‑driven marketplaces.

What are the current growth trends shaping the Europe Used Car Market?

Trend analysis shows a steady shift toward electrified powertrains, with BEVs and HEV/PHEVs gaining traction among environmentally conscious buyers. Digitalization is another dominant trend: platforms such as Auto1 Group, AutoScout24, and Cazoo dominate organized sales, reducing reliance on traditional unorganized dealers. Age segmentation reveals a growing preference for relatively young cars (0‑2 years) due to warranty coverage and lower depreciation. Price‑band trends indicate sustained demand for vehicles priced between USD 10 k and 30 k, balancing affordability with modern features. Finally, subscription‑based ownership models are emerging, driven by leasing giants seeking recurring revenue streams.

How did COVID‑19 impact the Europe Used Car Market and what is the recovery trajectory?

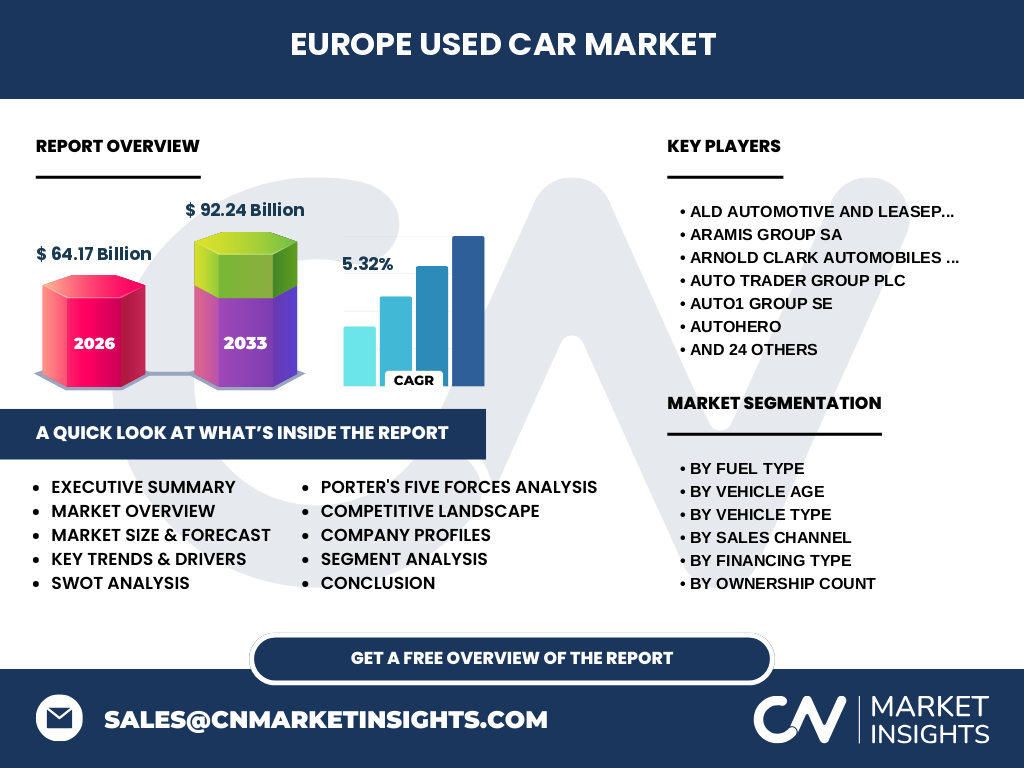

The pandemic caused a temporary dip in transaction volumes as lockdowns limited showroom access and disrupted supply chains. However, the market rebounded quickly once mobility restrictions eased, fueled by pent‑up demand for personal transportation and a shortage of new‑car inventory. Post‑COVID, buyers exhibited heightened price sensitivity, accelerating sales of sub‑30k vehicles and increasing reliance on organized online dealers. The recovery trajectory is positive, underpinned by a robust CAGR of 5.32 % projected through 2032, indicating that the market not only recovers but also expands beyond pre‑pandemic levels.

Who are the major competitors and what is the level of consolidation in the Europe Used Car Market?

The competitive landscape is characterized by a mix of large multinational dealers, specialist online platforms, and traditional broker networks. Prominent players include ALD Automotive, LeasePlan, Auto1 Group SE, AutoScout24, Cazoo Group, and Manheim Europe. Recent years have seen notable consolidation: Auto1’s acquisition of BCA Marketplace and Cazoo’s expansion through the purchase of automotive retailers have enhanced scale and geographic reach. Despite consolidation, the market remains moderately fragmented, offering opportunities for niche entrants that can differentiate through technology, financing options, or specialized vehicle segments.

What are the high‑level findings in the Executive Summary of the Europe Used Car Market?

The Europe Used Car Market is valued at USD 64.17 billion in 2026 and is projected to reach USD 92.24 billion by 2033, delivering a 5.32 % CAGR. Growth is propelled by digital sales channels, rising demand for low‑emission vehicles, and strong financing support from leasing firms. While diesel‑centric segments face regulatory pressure, BEV and hybrid segments are emerging as high‑growth opportunities. Market fragmentation offers room for consolidation, and strategic partnerships—particularly between fintech firms and dealerships—are likely to shape the next growth phase.

What is the forecast for the Europe Used Car Market from 2025 to 2032?

Based on the provided CAGR of 5.32 %, the market is expected to expand from the 2026 baseline of USD 64.17 billion to approximately USD 92.24 billion by the 2033 horizon. This steady increase reflects continued consumer preference for affordable mobility, the maturing of electric vehicle resale, and the scaling of organized digital platforms. Annual growth is anticipated to be fairly consistent, with slight acceleration in segments linked to electrified powertrains and financed purchases.

How is the Europe Used Car Market sized and shared across the defined segmentation?

Segmentation reveals diverse demand patterns: By fuel type, gasoline and diesel still dominate, but BEVs and HEV/PHEVs are gaining share due to emissions policies. Vehicle‑age distribution shows a strong preference for the 0‑2 year bracket, reflecting buyer interest in near‑new condition cars. In vehicle type, hatchbacks, sedans, and SUVs constitute the bulk of sales, while pickups and vans cater to commercial users. Organized dealers/platforms command a growing share compared with unorganized brokers, driven by consumer trust in online listings. Financing is split between outright purchases and financed purchases, with leasing firms expanding the latter. Single‑owner vehicles typically achieve higher resale values, whereas multi‑owner cars dominate the lower price bands (< USD 10 k). Price‑band analysis underscores the 10k‑30k range as the core market.

What is the geographic distribution of the Europe Used Car Market on a global scale?

Europe represents a substantial portion of the global used‑car landscape, reflecting mature automotive markets, high vehicle turnover rates, and strong regulatory frameworks encouraging vehicle replacement. While specific regional percentages are not disclosed, the market’s absolute size of USD 64.17 billion in 2026 positions Europe as a leading contributor to worldwide used‑car activity, surpassing many individual Asian and American markets combined.

What are the regional performance insights for the Europe Used Car Market?

Within Europe, market performance varies by economic strength and policy environment. Western Europe—particularly Germany, France, the UK, and the Netherlands—exhibits high transaction volumes, robust dealer networks, and rapid digital adoption. Southern regions such as Italy and Spain show strong demand for affordable hatchbacks and compact SUVs, often in the sub‑20k price band. Northern markets, including Scandinavia, demonstrate higher proportionate sales of BEVs and hybrids, aligning with aggressive carbon‑neutral targets. Eastern European countries present growth potential as disposable incomes rise and vehicle fleets modernize.

Which leading companies operate in the Europe Used Car Market and what are their strategies?

Key players include ALD Automotive and LeasePlan (finance‑focused leasing), Auto1 Group SE (online wholesale marketplace), AutoScout24 (digital classifieds), Cazoo Group Ltd (online retail with delivery), Manheim Europe (auction specialist), and BCA Marketplace (brokerage network). Strategies revolve around expanding digital capabilities, integrating financing solutions, and achieving scale through acquisitions. For example, Auto1’s purchase of BCA Marketplace broadens its wholesale reach, while Cazoo’s investment in logistics enhances end‑to‑end customer experience. Leasing firms are developing subscription models to capture recurring revenue and attract younger consumers.

How does Porter’s Five Forces framework apply to the Europe Used Car Market?

Threat of new entrants is moderate; high capital requirements and strong brand loyalty of established platforms create barriers, yet digital‑only entrants can leverage technology. Bargaining power of suppliers (vehicle owners) is low, as the market aggregates many sellers. Bargaining power of buyers is high, driven by price transparency on online platforms. Threat of substitutes is limited; alternatives such as public transit or ride‑hailing do not replace the need for personal vehicle ownership in many regions. Competitive rivalry is intense, with numerous dealers, brokers, and platforms competing on price, inventory breadth, and service quality.

What are the SWOT insights for the Europe Used Car Market?

Strengths: Large, mature fleet turnover, extensive dealer networks, and growing digital platforms. Weaknesses: Fragmented unorganized segment, residual value uncertainty for electrified cars. Opportunities: Expansion of BEV/HEV/PHEV resale, financing innovations, cross‑border online marketplaces. Threats: Regulatory pressures on diesel, potential supply constraints from new‑car shortages, and economic volatility affecting consumer purchasing power.

What does the value chain of the Europe Used Car Market look like?

The value chain begins with vehicle acquisition (trade‑ins, fleet disposals, auctions), followed by inspection, reconditioning, and certification. Next, inventory is listed on organized dealer networks or digital platforms, where pricing, financing options, and warranty packages are attached. The transaction stage includes financing (leasing firms), insurance, and paperwork processing. Post‑sale services—such as after‑sales support, warranties, and maintenance contracts—complete the chain, creating additional revenue streams for dealers and platform operators.

What key investment insights should investors consider for the Europe Used Car Market?

Investors should target companies that combine scale with technology, such as platforms offering end‑to‑end digital experiences and integrated financing. Funding electrified‑vehicle resale capabilities—battery health diagnostics, warranty extensions—will capture growth in the BEV segment. Strategic M&A in the unorganized broker space can consolidate market share and improve data quality. Partnerships with fintech firms to offer flexible financing or subscription models present attractive recurring‑revenue opportunities.

What are the concluding takeaways for the Europe Used Car Market?

The market is on a robust growth trajectory, moving from USD 64.17 billion in 2026 to USD 92.24 billion by 2033, driven by digitalization, financing innovation, and a shift toward low‑emission vehicles. While regulatory challenges affect diesel, they simultaneously create upside for BEVs and hybrids. Consolidation and technology integration will define competitive advantage, and investors should focus on firms that can deliver a seamless, financed, and electrified used‑car experience.

How was the research for this Europe Used Car Market report conducted?

The research combined primary interviews with industry executives, dealer networks, and financing providers, alongside secondary analysis of market reports, company filings, and regulatory publications. Data triangulation ensured accuracy of the 2026 market size, forecast, and CAGR. Segmentation definitions were aligned with standard industry classifications, and trend validation was performed through cross‑checking of sales channel growth and vehicle‑age distribution data.

What is the scope and any limitations of this Europe Used Car Market research?

The scope covers the entire European region, addressing all major vehicle types, fuel categories, age brackets, price bands, sales channels, financing structures, and ownership counts. It focuses on the period 2025‑2032 for forecasting. Limitations include the reliance on publicly available financial figures and company disclosures; proprietary transaction data from private dealers were not directly accessed, which may affect granularity of sub‑regional market share estimates.

Which key companies and recent developments are shaping the Europe Used Car Market?

Leading firms such as ALD Automotive and LeasePlan continue to expand financing options, introducing flexible subscription models. Auto1 Group’s acquisition of BCA Marketplace has increased its wholesale footprint. Cazoo Group announced a new logistics hub in the UK to accelerate delivery times. AutoScout24 launched AI‑driven price‑prediction tools, enhancing buyer confidence. Manheim Europe introduced a digital auction platform that integrates real‑time inspection data. These developments underscore a market-wide shift toward digitalisation, financing innovation, and consolidation.