Automated Test Equipment Market Overview - Definition, scope, and significance

Automated Test Equipment (ATE) refers to highly sophisticated systems used for testing electronic devices and components to ensure they meet specified performance standards and quality requirements. These systems are designed to automatically perform tests on semiconductor devices, integrated circuits, printed circuit boards, and other electronic components with minimal human intervention. The Automated Test Equipment Market encompasses a wide range of testing solutions including testers for digital, analog, mixed-signal, and RF/microwave devices. The significance of this market lies in its critical role in the electronics manufacturing industry, where ATE systems help reduce testing time, improve accuracy, lower costs, and increase production throughput. As electronic devices become increasingly complex and miniaturized, the demand for advanced ATE solutions continues to grow, making this market essential for maintaining quality standards across various industries including consumer electronics, automotive, aerospace, and telecommunications.

Automated Test Equipment Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Automated Test Equipment Market is driven by several key factors including the increasing complexity of semiconductor devices, growing demand for consumer electronics, and the rapid advancement of technologies such as 5G, IoT, and artificial intelligence. The automotive industry's shift towards electric vehicles and autonomous driving systems has created substantial demand for sophisticated testing solutions. However, the market faces restraints such as high initial investment costs for ATE systems and the complexity of testing advanced semiconductor nodes. Challenges include the need for continuous technological upgrades to keep pace with evolving device architectures and the shortage of skilled professionals to operate advanced ATE systems. Opportunities exist in emerging applications such as medical devices, renewable energy systems, and the expansion of 5G infrastructure, which require specialized testing solutions. Additionally, the growing trend towards miniaturization and the integration of multiple functions into single chips presents opportunities for innovative ATE solutions that can handle increasingly complex testing requirements.

Automated Test Equipment Market Growth Trends - Current and emerging trends shaping the market

The Automated Test Equipment Market is experiencing several significant growth trends that are reshaping the industry landscape. One prominent trend is the increasing adoption of modular and scalable ATE architectures that offer flexibility and cost-effectiveness for testing diverse device types. The integration of artificial intelligence and machine learning algorithms into ATE systems is enabling predictive maintenance, automated test optimization, and enhanced fault detection capabilities. Another emerging trend is the development of cloud-based ATE solutions that facilitate remote monitoring, data analytics, and collaborative testing environments. The market is also witnessing a shift towards the use of advanced probe technologies and high-speed digital interfaces to accommodate the testing of next-generation semiconductor devices. Additionally, the growing emphasis on energy efficiency and sustainability is driving the development of ATE systems with lower power consumption and reduced environmental impact. The convergence of ATE with other manufacturing technologies, such as automated optical inspection and X-ray inspection systems, is creating integrated testing solutions that offer comprehensive quality control across the production process.

COVID-19 Impact on the Automated Test Equipment Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the Automated Test Equipment Market, causing disruptions across the global supply chain and manufacturing operations. During the initial phases of the pandemic, many semiconductor fabrication facilities experienced temporary shutdowns or reduced capacity, leading to a decline in demand for ATE systems. However, the pandemic also highlighted the critical importance of electronics in enabling remote work, online education, and digital healthcare solutions, which subsequently drove demand for semiconductor devices and, consequently, ATE systems. The market demonstrated resilience as manufacturers adapted to new operating procedures and implemented safety measures to maintain production continuity. As economies recover and vaccination efforts progress, the ATE market is experiencing a strong rebound, driven by pent-up demand and the acceleration of digital transformation initiatives. The pandemic has also accelerated the adoption of automation and remote testing capabilities, which is expected to create new opportunities for ATE providers in the post-pandemic era.

Automated Test Equipment Market Competitive Landscape - Major competitors and market consolidation

The Automated Test Equipment Market features a competitive landscape characterized by the presence of several established players and a few emerging companies. Major competitors include industry leaders such as Advantest Corporation, Teradyne Inc., and National Instruments Corporation, which hold significant market shares due to their extensive product portfolios and global presence. These companies compete based on technological innovation, product performance, and customer service. The market has witnessed some consolidation through mergers and acquisitions, as larger companies seek to expand their technological capabilities and market reach. For instance, Teradyne's acquisition of companies like LitePoint and Mobile Automation has strengthened its position in wireless and automotive testing segments. The competitive landscape is also influenced by the entry of new players offering specialized testing solutions for emerging applications such as 5G, automotive electronics, and IoT devices. Companies are increasingly focusing on strategic partnerships and collaborations to enhance their product offerings and address the evolving needs of end-users across different industries.

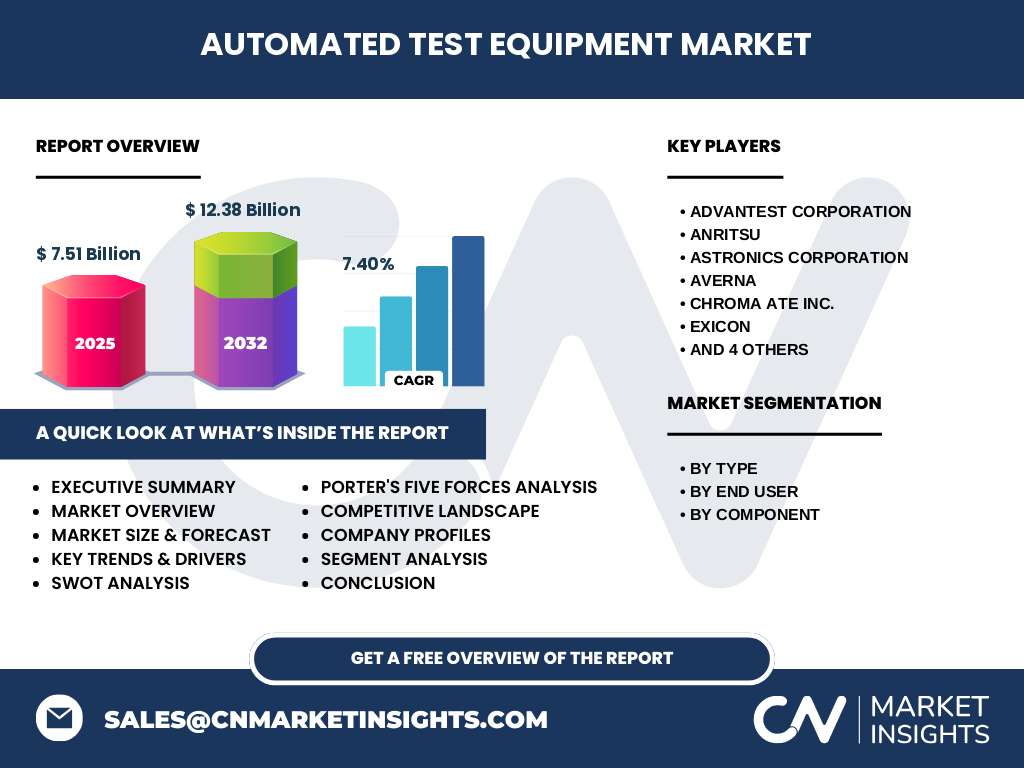

Executive Summary - High-level overview and key findings about Automated Test Equipment Market

The Automated Test Equipment Market is experiencing robust growth, driven by the increasing complexity of semiconductor devices and the expanding electronics industry. The market, valued at 7.51 Billion in 2025, is projected to reach 12.38 Billion by 2032, reflecting a compound annual growth rate of 7.40%. This growth is fueled by the rising demand for consumer electronics, the proliferation of 5G technology, and the automotive industry's shift towards electric and autonomous vehicles. The market is segmented by type, end-user industry, and component, with integrated circuits representing a significant portion of the testing requirements. Key players such as Advantest Corporation, Teradyne Inc., and National Instruments Corporation are leading the market through continuous innovation and strategic expansions. The Asia-Pacific region dominates the market due to the presence of major semiconductor manufacturing hubs, while North America and Europe also contribute significantly to market growth. Despite challenges such as high initial costs and the need for skilled operators, the market presents substantial opportunities in emerging applications and the development of advanced testing solutions for next-generation devices.

Automated Test Equipment Market Forecast - Projections for 2025-2032 period

The Automated Test Equipment Market is poised for substantial growth over the forecast period from 2025 to 2032, with projections indicating a market size expansion from 7.51 Billion to 12.38 Billion. This represents a compound annual growth rate of 7.40%, reflecting the increasing demand for sophisticated testing solutions across various industries. The growth trajectory is expected to be driven by several factors, including the continued advancement of semiconductor technology, the proliferation of 5G networks, and the rising adoption of electric vehicles. The forecast period will likely see increased investments in research and development by key players to address the testing challenges posed by emerging technologies such as artificial intelligence, machine learning, and quantum computing. Additionally, the market is expected to benefit from the growing trend towards Industry 4.0 and the increasing emphasis on quality control in electronics manufacturing. Regional growth will be particularly strong in Asia-Pacific, driven by the presence of major semiconductor foundries and the expansion of electronics manufacturing capabilities in countries like China, South Korea, and Taiwan.

Automated Test Equipment Market Size and Share by Segmentation - Breakdown by {segmentData}

The Automated Test Equipment Market is segmented by type, end-user, and component, each contributing differently to the overall market size and share. By type, Integrated Circuits (ICs) represent a significant segment due to their widespread use in electronic devices and the increasing complexity of chip designs. The end-user segmentation reveals that the consumer electronics sector holds a substantial market share, driven by the constant demand for smartphones, tablets, and other personal devices. The automotive industry is emerging as a key growth segment, particularly with the rise of electric vehicles and advanced driver assistance systems. In terms of components, Industrial PCs and Mass Interconnect systems are crucial elements of ATE setups, with the Handler/Prober segment also playing a significant role in the testing process. The market share distribution across these segments is influenced by factors such as technological advancements, industry-specific requirements, and the overall demand for electronic devices in each sector. As the market evolves, we can expect shifts in segment dominance, with emerging applications in areas like medical devices and aerospace potentially gaining larger shares.

Global Automated Test Equipment Market Size and Share by Region - Geographic distribution

The global Automated Test Equipment Market exhibits a diverse geographic distribution, with significant variations in market size and share across different regions. Asia-Pacific dominates the market, accounting for the largest share due to the presence of major semiconductor manufacturing hubs in countries such as China, Taiwan, South Korea, and Japan. This region's strong electronics manufacturing ecosystem and the increasing investments in semiconductor fabrication facilities contribute to its market leadership. North America holds the second-largest market share, driven by the presence of leading ATE manufacturers, a robust semiconductor industry, and significant R&D activities in emerging technologies. Europe represents another important market, with countries like Germany, France, and the Netherlands contributing to growth through their strong automotive and industrial electronics sectors. The Middle East and Africa, along with Latin America, represent smaller but growing markets, with increasing investments in technology infrastructure and electronics manufacturing capabilities. The regional distribution of the ATE market is influenced by factors such as local manufacturing capabilities, technological adoption rates, and government initiatives supporting the electronics industry.

Regional Analysis of the Automated Test Equipment Market - Detailed regional market performance

The regional performance of the Automated Test Equipment Market varies significantly across different geographical areas, reflecting the unique characteristics and growth drivers of each region. In Asia-Pacific, the market is experiencing rapid growth, fueled by the presence of major semiconductor foundries and the increasing demand for consumer electronics. Countries like China and Taiwan are investing heavily in advanced semiconductor manufacturing capabilities, driving the demand for sophisticated ATE systems. North America's market performance is characterized by strong technological innovation and the presence of leading ATE manufacturers, with the United States being a key contributor to market growth. The region's focus on emerging technologies such as 5G, artificial intelligence, and autonomous vehicles is creating new opportunities for ATE providers. Europe's market performance is closely tied to its strong automotive and industrial electronics sectors, with countries like Germany leading in automotive electronics testing requirements. The region is also seeing growth in renewable energy and medical device testing applications. While regions like the Middle East, Africa, and Latin America currently represent smaller markets, they are showing promising growth potential as they develop their electronics manufacturing capabilities and adopt advanced technologies.

Leading Company Profiles in the Automated Test Equipment Market - Industry players and strategies

The Automated Test Equipment Market is characterized by the presence of several leading companies, each with distinct strategies and market positions. Advantest Corporation stands out as a global leader, known for its advanced semiconductor test systems and strong presence in the memory and logic testing segments. The company's strategy focuses on continuous innovation and expanding its product portfolio to address emerging testing requirements. Teradyne Inc. is another major player, recognized for its comprehensive range of ATE solutions across various applications. Teradyne's strategy involves strategic acquisitions and partnerships to strengthen its market position and expand into new application areas such as 5G and automotive testing. National Instruments Corporation has established itself as a key player through its modular and flexible testing solutions, with a strategy centered on software-defined testing and the integration of AI and machine learning capabilities. Other notable companies such as Anritsu, Astronics Corporation, and Chroma ATE Inc. are also making significant contributions to the market through their specialized testing solutions and regional strengths. These companies are focusing on developing advanced testing technologies, expanding their global presence, and forming strategic alliances to address the evolving needs of the electronics industry.

Porter's Five Forces Analysis of the Automated Test Equipment Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the Automated Test Equipment Market. The threat of new entrants is relatively low due to the high capital requirements for R&D and manufacturing facilities, as well as the need for specialized technical expertise. However, the market does face the risk of substitute products or alternative testing methods, particularly as new technologies emerge. The bargaining power of buyers is moderate to high, as large semiconductor manufacturers and electronics companies have significant influence over pricing and product specifications. Conversely, the bargaining power of suppliers is relatively low due to the availability of multiple component suppliers and the ability of major ATE manufacturers to integrate vertically. The intensity of competitive rivalry is high, with several established players competing on technological innovation, product performance, and customer service. This intense competition drives continuous product development and can lead to pricing pressures. The analysis suggests that companies in this market need to focus on innovation, customer relationships, and operational efficiency to maintain their competitive positions and navigate the complex market dynamics.

SWOT Analysis of the Automated Test Equipment Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the Automated Test Equipment Market reveals several key factors influencing its growth and development. Strengths of the market include the increasing complexity of semiconductor devices, which necessitates advanced testing solutions, and the growing demand for high-quality electronic products across various industries. The market also benefits from strong technological expertise among leading manufacturers and the continuous innovation in testing methodologies. However, weaknesses exist in the form of high initial costs for ATE systems and the complexity of testing advanced semiconductor nodes, which can limit adoption among smaller manufacturers. Opportunities in the market are abundant, particularly in emerging applications such as 5G technology, electric vehicles, and the Internet of Things (IoT), which require specialized testing solutions. The growing trend towards miniaturization and the integration of multiple functions into single chips also presents opportunities for innovative ATE solutions. Threats to the market include the cyclical nature of the semiconductor industry, which can lead to fluctuations in demand for ATE systems, and the potential for economic downturns that may impact electronics manufacturing. Additionally, the rapid pace of technological change poses a threat in terms of the need for continuous upgrades and the risk of obsolescence for existing ATE systems.

Automated Test Equipment Market Value Chain Analysis - Industry structure and value flow

The value chain analysis of the Automated Test Equipment Market reveals a complex structure involving multiple stages and participants. At the beginning of the chain, semiconductor and electronics manufacturers drive demand for ATE systems based on their production requirements and quality standards. ATE manufacturers, such as Advantest Corporation and Teradyne Inc., form the core of the value chain, designing and producing sophisticated testing systems that incorporate advanced hardware and software components. These manufacturers rely on a network of suppliers providing critical components such as industrial PCs, mass interconnect systems, and specialized testing probes. The value chain also includes system integrators and solution providers who offer customized ATE configurations and support services to end-users. Distribution channels play a crucial role in delivering ATE systems to customers across different regions, with some manufacturers maintaining direct sales teams while others work through authorized distributors. After-sales service and support, including maintenance, upgrades, and training, represent important value-adding activities in the chain. The flow of value in this market is characterized by continuous innovation, with each participant contributing to the development of increasingly sophisticated and efficient testing solutions that meet the evolving needs of the electronics industry.

Key Investment Insights in the Automated Test Equipment Market - Strategic investment recommendations

The Automated Test Equipment Market presents several compelling investment opportunities for stakeholders looking to capitalize on the growth of the electronics industry. Key investment insights suggest focusing on companies that are at the forefront of developing advanced testing solutions for emerging technologies such as 5G, artificial intelligence, and electric vehicles. Investors should consider companies with strong R&D capabilities and a track record of innovation in addressing the testing challenges posed by increasingly complex semiconductor devices. Strategic investments in companies that offer modular and scalable ATE solutions are particularly promising, as these products provide flexibility and cost-effectiveness for manufacturers dealing with diverse product lines. The integration of artificial intelligence and machine learning into ATE systems represents a significant growth area, offering opportunities for investments in companies that are pioneering these technologies. Additionally, investments in companies with a strong presence in high-growth regions such as Asia-Pacific, particularly those with established relationships with major semiconductor foundries, could yield substantial returns. It's also worth considering investments in companies that are expanding their capabilities in adjacent markets such as automotive electronics testing and medical device testing, as these sectors are expected to drive future demand for specialized ATE solutions.

Automated Test Equipment Market Conclusion - Summary and key takeaways

The Automated Test Equipment Market is positioned for significant growth over the coming years, driven by the increasing complexity of electronic devices and the expanding electronics industry. With a projected market size increase from 7.51 Billion to 12.38 Billion by 2032, representing a CAGR of 7.40%, the market offers substantial opportunities for both established players and new entrants. Key takeaways from this analysis include the critical role of ATE in ensuring the quality and reliability of semiconductor devices, the importance of technological innovation in maintaining competitive advantage, and the growing demand for specialized testing solutions in emerging applications such as 5G, electric vehicles, and IoT devices. The market's regional dynamics, with Asia-Pacific leading in terms of market share, highlight the importance of a global perspective in strategic planning. While challenges such as high initial costs and the need for continuous technological upgrades exist, the overall market outlook remains positive, driven by the relentless advancement of electronics technology and the increasing emphasis on quality control in manufacturing processes.

Research Methodology - How this research was conducted

The research for this Automated Test Equipment Market report was conducted using a comprehensive methodology that combines primary and secondary research techniques. Primary research involved interviews with industry experts, including executives from leading ATE manufacturers, semiconductor companies, and industry analysts. These interviews provided valuable insights into market trends, technological developments, and competitive dynamics. Secondary research encompassed a thorough review of company annual reports, financial statements, press releases, and industry publications. Additionally, data from trade associations, government publications, and market research databases were analyzed to validate findings and provide a broader context for the market analysis. The research methodology also included a detailed analysis of patent filings and academic literature to identify emerging technologies and innovation trends in the ATE sector. Market size and forecast estimates were derived using a combination of top-down and bottom-up approaches, considering factors such as semiconductor production volumes, electronics manufacturing trends, and technological adoption rates across different industries and regions.

Research Scope - Coverage and limitations

The scope of this research on the Automated Test Equipment Market encompasses a comprehensive analysis of the global market, covering key segments such as type, end-user industry, and component. The research focuses on major geographic regions including North America, Europe, Asia-Pacific, and the Rest of the World, providing insights into regional market dynamics and growth opportunities. The study covers the period from 2025 to 2032, with historical data and current market size estimates provided for context. The research includes detailed profiles of leading companies in the ATE market, an analysis of competitive forces, and an examination of key market trends and drivers. However, it's important to note that the research has certain limitations. The analysis is primarily based on publicly available information and may not capture all nuances of private company operations or unpublicized strategic developments. Additionally, the rapidly evolving nature of technology means that some projections may be subject to change based on unforeseen technological breakthroughs or shifts in market dynamics. The research also focuses on the ATE market specifically and may not fully capture the broader ecosystem of electronics manufacturing and testing technologies.

Key Companies and Recent Developments in the Automated Test Equipment Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Automated Test Equipment Market is characterized by the presence of several key companies that are driving innovation and shaping the industry landscape. Advantest Corporation, a global leader in semiconductor test systems, has recently announced advancements in its SOC (System on Chip) test platforms, focusing on improving test efficiency for complex integrated circuits. The company has also formed strategic partnerships with major semiconductor manufacturers to develop customized testing solutions for next-generation devices. Teradyne Inc. has made significant strides in expanding its product portfolio, with recent launches of advanced testers for automotive electronics and 5G applications. The company's acquisition of a leading provider of wireless test solutions has strengthened its position in the rapidly growing 5G testing market. National Instruments Corporation has been focusing on the integration of AI and machine learning capabilities into its ATE systems, with recent product announcements highlighting enhanced data analytics and predictive maintenance features. Anritsu has expanded its presence in the RF and microwave testing segment, launching new solutions for 5G NR (New Radio) and millimeter-wave applications. Chroma ATE Inc. has strengthened its position in the power electronics testing market, with recent developments in electric vehicle battery testing solutions. These companies, along with others in the market, continue to invest in research and development, form strategic partnerships, and launch innovative products to address the evolving testing requirements of the electronics industry.