Food Service Packaging Market Overview - Definition, scope, and significance

Food service packaging encompasses the materials and solutions used to store, transport, and serve food in restaurants, cafeterias, catering services, and other food service establishments. This market plays a crucial role in food safety, preservation, and convenience across the global food service industry. The scope includes various packaging formats such as containers, wraps, bags, trays, and specialized packaging for different food categories. With the food service industry expanding rapidly worldwide, packaging solutions have become increasingly important for maintaining food quality, extending shelf life, and meeting evolving consumer demands for convenience and sustainability. The market's significance is further amplified by changing consumer lifestyles, the growth of delivery services, and increasing focus on food safety and hygiene standards.

Food Service Packaging Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The food service packaging market is driven by several key factors including the rapid expansion of the food service industry, growing demand for convenience foods, and increasing adoption of online food delivery services. Rising consumer awareness about food safety and hygiene, particularly post-pandemic, has further accelerated demand for reliable packaging solutions. However, the market faces challenges such as environmental concerns over single-use plastics, stringent regulations on packaging waste, and fluctuating raw material prices. Opportunities exist in the development of sustainable packaging alternatives, smart packaging technologies, and innovative solutions for emerging food service formats. The growing trend toward eco-friendly materials and circular economy principles presents significant opportunities for market players to differentiate their offerings and capture new market segments.

Food Service Packaging Market Growth Trends - Current and emerging trends shaping the market

The food service packaging market is experiencing several transformative trends that are reshaping the industry landscape. A significant trend is the shift toward sustainable and eco-friendly packaging materials, with increasing adoption of biodegradable, compostable, and recyclable alternatives to traditional plastics. Smart packaging technologies incorporating QR codes, freshness indicators, and temperature sensors are gaining traction, enhancing food safety and consumer engagement. The market is also witnessing growing demand for customized packaging solutions that reflect brand identity and improve customer experience. Another emerging trend is the development of portion-controlled and multi-compartment packaging to cater to changing consumer preferences for convenience and portion management. Additionally, the rise of ghost kitchens and cloud kitchens is creating new packaging requirements for delivery-focused operations.

COVID-19 Impact on the Food Service Packaging Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a profound impact on the food service packaging market, initially causing significant disruptions due to lockdowns and restaurant closures. However, the crisis also accelerated certain trends, particularly the surge in food delivery and takeout services, which dramatically increased demand for food packaging solutions. The pandemic heightened awareness about hygiene and food safety, leading to increased adoption of tamper-evident packaging and single-use solutions. As the industry recovers, the market is experiencing a hybrid recovery pattern, with some segments rebounding faster than others. The pandemic has permanently altered consumer behavior, with increased preference for contactless delivery and takeaway options, creating sustained demand for food service packaging. This shift has prompted manufacturers to innovate and develop packaging solutions that address new safety and convenience requirements.

Food Service Packaging Market Competitive Landscape - Major competitors and market consolidation

The food service packaging market features a mix of global packaging giants and specialized regional players competing for market share. Major companies such as Amcor plc, Sealed Air, and Berry Global Inc. dominate the market with their extensive product portfolios and global distribution networks. The competitive landscape is characterized by ongoing consolidation through mergers and acquisitions, as companies seek to expand their capabilities and market presence. Key players are investing heavily in research and development to create innovative packaging solutions that address sustainability concerns and evolving customer needs. Competition is particularly intense in the development of eco-friendly alternatives and smart packaging technologies. Companies are also focusing on vertical integration strategies to control costs and ensure supply chain resilience, while smaller players are finding opportunities in niche markets and regional specialties.

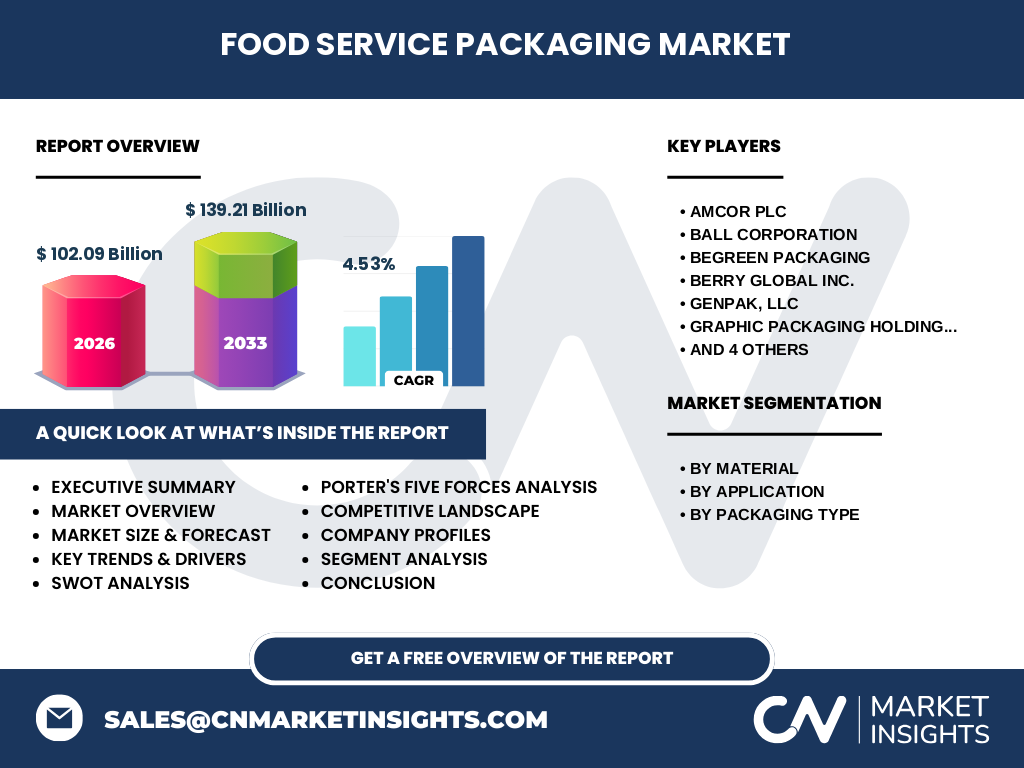

Executive Summary - High-level overview and key findings about Food Service Packaging Market

The food service packaging market is poised for significant growth, with the market size expected to reach 102.09 billion by 2026, demonstrating the industry's robust expansion trajectory. The market is experiencing a steady compound annual growth rate (CAGR) of 4.53%, with projections indicating growth to 139.21 billion by 2033. This growth is driven by increasing demand from the food service sector, evolving consumer preferences, and technological advancements in packaging solutions. The market is segmented by material type, including plastic and metal options, and by application across beverages, prepared meals, fruits and vegetables, bakery and confectionery, and dairy products. Companies operating in this space must navigate a complex landscape of sustainability requirements, regulatory compliance, and changing consumer expectations while capitalizing on opportunities in emerging markets and innovative packaging solutions.

Food Service Packaging Market Forecast - Projections for 2025-2032 period

The food service packaging market is projected to experience steady growth during the 2025-2032 period, with the market expected to reach 139.21 billion by 2033. This represents a compound annual growth rate (CAGR) of 4.53%, indicating sustained market expansion. The forecast period will likely see continued growth in demand for sustainable packaging solutions, driven by increasing environmental awareness and regulatory pressures. The market is expected to benefit from technological advancements in packaging materials and design, as well as the ongoing expansion of the global food service industry. Regional markets are anticipated to show varying growth rates, with emerging economies potentially experiencing faster growth due to increasing urbanization and changing consumer lifestyles. The forecast also suggests continued innovation in packaging solutions to address evolving food safety requirements and consumer preferences.

Food Service Packaging Market Size and Share by Segmentation - Breakdown by {segmentData}

The food service packaging market is segmented across multiple dimensions, with each segment contributing differently to the overall market size. By material type, the market is divided between plastic and metal packaging solutions, with plastic currently dominating due to its versatility and cost-effectiveness. In terms of application, the market serves various food categories including beverages, prepared meals, fruits and vegetables, bakery and confectionery, and dairy products. Each application segment has distinct packaging requirements and growth patterns. The packaging type segment is categorized into flexible and rigid packaging, with flexible packaging gaining popularity due to its convenience and material efficiency. While specific market share data for each segment is not provided, the segmentation structure helps understand the diverse nature of the market and the different growth opportunities within each category.

Global Food Service Packaging Market Size and Share by Region - Geographic distribution

The global food service packaging market exhibits varying growth patterns and market shares across different regions. While specific regional market share data is not provided, the market's geographic distribution is influenced by factors such as economic development, food service industry maturity, and consumer preferences. Developed regions typically show higher adoption rates of advanced packaging solutions and sustainable materials, while emerging markets are experiencing rapid growth due to expanding food service sectors and changing consumer lifestyles. The Asia-Pacific region is expected to be a key growth driver, supported by increasing urbanization and rising disposable incomes. North America and Europe continue to be significant markets, driven by high standards for food safety and growing demand for convenience foods. Latin America and the Middle East & Africa regions are also showing promising growth potential as their food service industries expand.

Regional Analysis of the Food Service Packaging Market - Detailed regional market performance

The food service packaging market demonstrates distinct characteristics and growth patterns across different regions. North America represents a mature market with high adoption of advanced packaging technologies and strong emphasis on sustainability. The region's well-established food service industry drives consistent demand for innovative packaging solutions. Europe follows similar trends, with additional focus on strict regulatory compliance and circular economy initiatives. The Asia-Pacific region emerges as the fastest-growing market, fueled by rapid urbanization, expanding middle class, and growing food service sector. Countries like China and India are experiencing particularly strong growth due to changing consumer preferences and increasing adoption of Western food service formats. Latin America and the Middle East & Africa regions are showing promising growth potential, though at different rates, influenced by economic development and evolving food service landscapes in these regions.

Leading Company Profiles in the Food Service Packaging Market - Industry players and strategies

The food service packaging market is characterized by the presence of several key players, each bringing unique strengths and capabilities to the industry. Amcor plc stands out as a global leader in packaging solutions, offering a comprehensive range of products across multiple segments. Ball Corporation specializes in metal packaging solutions, particularly for beverages and food products. BeGreen Packaging focuses on sustainable packaging alternatives, aligning with the growing demand for eco-friendly solutions. Berry Global Inc. provides a wide range of packaging products across various materials and applications. Genpak, LLC specializes in food packaging solutions for the food service industry. Graphic Packaging Holding Company offers innovative paper-based packaging solutions. Huhtamaki is known for its sustainable packaging solutions and global presence. Sealed Air provides packaging solutions with focus on food safety and preservation. Stora Enso specializes in renewable packaging solutions, while WestRock Company offers comprehensive packaging solutions across multiple segments.

Porter's Five Forces Analysis of the Food Service Packaging Market - Competitive forces assessment

The food service packaging market's competitive dynamics can be analyzed through Porter's Five Forces framework. The threat of new entrants is moderate due to high initial capital requirements and the need for established distribution networks. Bargaining power of suppliers is relatively low as there are multiple material suppliers and alternatives available. The bargaining power of buyers is moderate to high, particularly for large food service chains that can negotiate favorable terms. The threat of substitute products is significant, especially with the growing availability of sustainable alternatives and innovative packaging solutions. Competitive rivalry is intense, with numerous global and regional players competing on price, quality, and innovation. The market also faces pressure from environmental regulations and changing consumer preferences, which influence the competitive landscape and force companies to continuously innovate and adapt their strategies.

SWOT Analysis of the Food Service Packaging Market - Strengths, weaknesses, opportunities, threats

The food service packaging market exhibits several key strengths, including established global supply chains, technological expertise in packaging solutions, and strong relationships with food service providers. The market benefits from consistent demand driven by the growing food service industry and increasing consumer preference for convenience. However, weaknesses include dependence on raw material prices, environmental concerns regarding packaging waste, and regulatory compliance challenges. Opportunities exist in developing sustainable packaging solutions, expanding into emerging markets, and leveraging technological advancements in smart packaging. The market faces threats from stringent environmental regulations, increasing competition from alternative packaging materials, and potential disruptions in raw material supply chains. Companies must navigate these factors while capitalizing on opportunities in sustainable innovation and market expansion.

Food Service Packaging Market Value Chain Analysis - Industry structure and value flow

The food service packaging value chain encompasses multiple stages, from raw material suppliers to end-users in the food service industry. The chain begins with suppliers of raw materials such as plastics, metals, paper, and other packaging materials. These materials are then processed by packaging manufacturers who transform them into various packaging solutions through processes like molding, printing, and assembly. Distributors and wholesalers play a crucial role in connecting manufacturers with food service providers. The final stage involves food service operators who utilize these packaging solutions for their operations. Value is added at each stage through innovation, quality improvements, and service enhancements. The value chain is increasingly focusing on sustainability and efficiency, with growing emphasis on circular economy principles and waste reduction throughout the process.

Key Investment Insights in the Food Service Packaging Market - Strategic investment recommendations

Investors in the food service packaging market should focus on companies demonstrating strong capabilities in sustainable packaging solutions and technological innovation. Key investment opportunities lie in businesses developing eco-friendly alternatives to traditional packaging materials and those incorporating smart packaging technologies. The market shows particular promise in regions with growing food service sectors and increasing environmental awareness. Companies with strong research and development capabilities and established relationships with major food service providers present attractive investment prospects. Strategic investments in emerging markets, particularly in Asia-Pacific, could yield significant returns given the region's rapid growth potential. Additionally, investments in companies focusing on circular economy solutions and waste reduction technologies align with long-term market trends and regulatory developments.

Food Service Packaging Market Conclusion - Summary and key takeaways

The food service packaging market presents a dynamic landscape with significant growth potential, driven by evolving consumer preferences, technological advancements, and sustainability requirements. The market is expected to grow from 102.09 billion in 2026 to 139.21 billion by 2033, representing a steady CAGR of 4.53%. Success in this market requires a balanced approach to innovation, sustainability, and operational efficiency. Companies must navigate complex regulatory environments while meeting changing consumer demands for convenience and environmental responsibility. The market's future will be shaped by continued technological advancement, increasing focus on sustainable solutions, and the ongoing evolution of the global food service industry. Strategic investments in innovation and sustainability will be crucial for long-term success in this competitive market.

Research Methodology - How this research was conducted

The research methodology for this market analysis involved comprehensive data collection from multiple sources, including industry reports, company financial statements, and market databases. Primary research was conducted through interviews with industry experts, packaging manufacturers, and food service providers to validate findings and gather insights. Secondary research included analysis of industry publications, trade journals, and government databases to ensure comprehensive coverage of market trends and developments. The research incorporated both qualitative and quantitative analysis to provide a holistic view of the market. Data triangulation was employed to verify information from multiple sources, ensuring accuracy and reliability of the findings. The methodology also included analysis of historical trends and future projections based on market dynamics and industry expert opinions.

Research Scope - Coverage and limitations

This research covers the global food service packaging market, focusing on key segments including material types (plastic and metal), applications (beverages, prepared meals, fruits and vegetables, bakery and confectionery, dairy products), and packaging types (flexible and rigid). The scope encompasses major geographic regions and key market players, providing a comprehensive analysis of market dynamics, trends, and competitive landscape. The research timeframe extends from historical data through current market conditions to future projections up to 2033. While the study provides detailed insights into market structure and trends, it is important to note that specific regional market shares and detailed financial data for individual companies are not included in this analysis. The research focuses on providing actionable insights while maintaining confidentiality of sensitive business information.

Key Companies and Recent Developments in the Food Service Packaging Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The food service packaging market features several prominent companies driving innovation and market growth. Amcor plc has been focusing on expanding its sustainable packaging solutions and recently announced investments in advanced recycling technologies. Ball Corporation continues to strengthen its position in metal packaging, particularly for beverage applications, with new product launches emphasizing sustainability. BeGreen Packaging has gained attention for its innovative plant-based packaging solutions and recent partnerships with major food service chains. Berry Global Inc. has been expanding its product portfolio through strategic acquisitions and new product development initiatives. Genpak, LLC has introduced new compostable packaging lines and strengthened its distribution network. Graphic Packaging Holding Company has launched several new paper-based packaging solutions and formed partnerships with food service providers. Huhtamaki has been investing in sustainable packaging technologies and expanding its global presence. Sealed Air has introduced new food safety solutions and smart packaging technologies. Stora Enso continues to focus on renewable packaging solutions and has announced several new product innovations. WestRock Company has been expanding its sustainable packaging offerings and strengthening its market position through strategic partnerships.