Aircraft Interface Device Market Overview - Definition, scope, and significance

An Aircraft Interface Device (AID) is a critical avionics component that serves as a bridge between an aircraft's flight management system and portable electronic devices used by pilots and crew. These devices facilitate the transfer of real-time flight data, including navigation information, weather updates, and aircraft performance metrics, to tablets and other mobile platforms. The AID market encompasses both hardware and software solutions that enable seamless connectivity between aircraft systems and personal electronic devices, revolutionizing cockpit operations and flight planning processes. As aviation technology continues to evolve, AIDs have become increasingly significant in enhancing operational efficiency, reducing pilot workload, and improving overall flight safety.

Aircraft Interface Device Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Aircraft Interface Device market is primarily driven by the growing adoption of electronic flight bags (EFBs) and the aviation industry's push toward digital transformation. Airlines and operators are increasingly recognizing the operational benefits of AIDs, including reduced paper usage, improved fuel efficiency through optimized flight planning, and enhanced situational awareness for pilots. The rising demand for real-time data connectivity and the need for more efficient cockpit management systems further fuel market growth. However, the market faces restraints such as high initial implementation costs and concerns regarding cybersecurity and data protection. Challenges include the complexity of integrating AIDs with existing aircraft systems and ensuring compatibility across different aircraft models and generations. Despite these obstacles, significant opportunities exist in the retrofit segment, as older aircraft fleets seek to modernize their avionics systems, and in the development of advanced wireless connectivity solutions that offer greater flexibility and ease of use.

Aircraft Interface Device Market Growth Trends - Current and emerging trends shaping the market

The Aircraft Interface Device market is witnessing several notable growth trends that are reshaping the industry landscape. One prominent trend is the shift toward wireless connectivity solutions, which offer greater flexibility and reduce installation complexity compared to traditional wired systems. The integration of artificial intelligence and machine learning capabilities into AIDs is another emerging trend, enabling predictive maintenance and advanced data analytics. There is also a growing focus on developing lightweight and compact AID solutions to minimize aircraft weight and improve fuel efficiency. The market is experiencing increased demand for cloud-based data storage and processing capabilities, allowing for more comprehensive flight data analysis and improved decision-making. Additionally, the rise of connected aircraft concepts and the Internet of Things (IoT) in aviation are driving the development of more sophisticated AID systems that can seamlessly integrate with other onboard systems and ground-based operations.

COVID-19 Impact on the Aircraft Interface Device Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the Aircraft Interface Device market, mirroring the broader challenges faced by the aviation industry. During the height of the pandemic, many airlines and aircraft operators postponed or canceled their AID implementation plans due to financial constraints and reduced flight operations. The global travel restrictions and decline in passenger traffic led to a temporary slowdown in market growth as airlines focused on immediate survival rather than long-term technology investments. However, the pandemic also highlighted the importance of digital solutions in aviation, accelerating the industry's digital transformation efforts. As the aviation sector recovers, there is renewed interest in AIDs as airlines seek to optimize operations, reduce costs, and improve efficiency in the post-pandemic era. The market is expected to experience a strong recovery trajectory, driven by the need for enhanced operational capabilities and the gradual return to pre-pandemic flight volumes.

Aircraft Interface Device Market Competitive Landscape - Major competitors and market consolidation

The Aircraft Interface Device market features a mix of established aerospace giants and specialized technology providers, creating a dynamic competitive landscape. Major players such as Boeing, Honeywell International Inc., Collins Aerospace, and Thales Group leverage their extensive experience in aviation technology and strong relationships with airlines to maintain significant market presence. These companies often offer comprehensive avionics solutions that include AID systems as part of larger product portfolios. Meanwhile, specialized companies like Astronics Corporation, Teledyne Controls LLC, and Viasat, Inc. focus on developing innovative AID technologies and compete by offering niche solutions or superior technical capabilities. The market has seen some consolidation through strategic partnerships and acquisitions, as larger companies seek to expand their technological capabilities and market reach. Competition is intensifying as companies strive to differentiate themselves through advanced features, improved connectivity options, and enhanced data analytics capabilities.

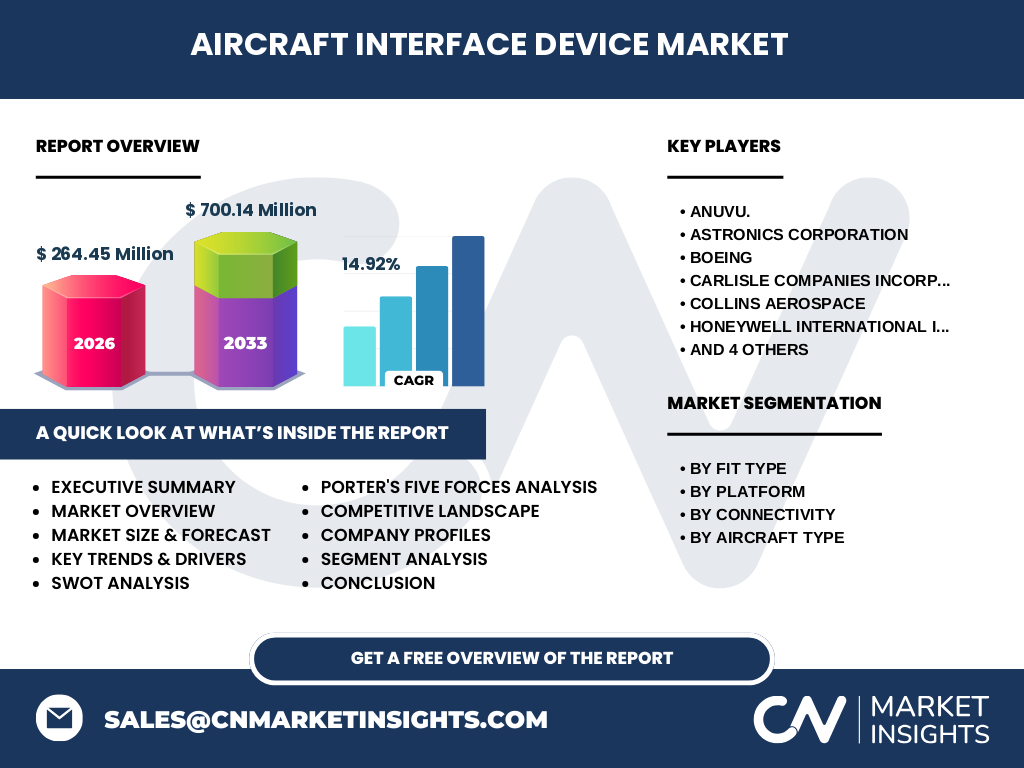

Executive Summary - High-level overview and key findings about Aircraft Interface Device Market

The Aircraft Interface Device market is experiencing robust growth, driven by the aviation industry's digital transformation and the increasing adoption of electronic flight bags. The market, valued at 264.45 Million in 2026, is projected to reach 700.14 Million by 2033, reflecting a strong compound annual growth rate of 14.92%. This growth is fueled by the rising demand for real-time data connectivity, improved operational efficiency, and enhanced flight safety features. The market is characterized by a diverse range of solutions, including both hardware and software components, with connectivity options spanning wired and wireless technologies. Key segments include line fit and retrofit installations, catering to both fixed-wing and rotary-wing aircraft. As airlines and operators continue to prioritize digital solutions and operational optimization, the AID market is poised for significant expansion, presenting substantial opportunities for both established players and innovative newcomers in the aviation technology sector.

Aircraft Interface Device Market Forecast - Projections for 2025-2032 period

The Aircraft Interface Device market is poised for substantial growth over the forecast period from 2025 to 2032. Starting from a base of 264.45 Million in 2026, the market is expected to experience a compound annual growth rate of 14.92%, reaching an impressive 700.14 Million by 2033. This robust growth trajectory is underpinned by several factors, including the ongoing digital transformation in aviation, increasing demand for real-time data connectivity, and the rising adoption of electronic flight bags across commercial and general aviation sectors. The forecast period is likely to see accelerated growth in the retrofit segment as airlines seek to modernize their existing fleets with advanced AID solutions. Additionally, the development of more sophisticated wireless connectivity options and the integration of artificial intelligence capabilities are expected to drive market expansion. Regional variations in growth rates may occur, with emerging markets potentially showing higher growth rates as they invest in modernizing their aviation infrastructure.

Aircraft Interface Device Market Size and Share by Segmentation - Breakdown by {segmentData}

The Aircraft Interface Device market can be segmented across several key dimensions, each contributing to the overall market dynamics. In terms of fit type, both line fit and retrofit segments play crucial roles, with the retrofit segment potentially showing higher growth rates as airlines seek to upgrade existing aircraft with modern AID solutions. The platform segmentation reveals a balanced market between hardware and software components, with software solutions gaining prominence due to their flexibility and ease of updates. Connectivity options are divided between wired and wireless solutions, with wireless technologies expected to see increased adoption due to their ease of installation and reduced aircraft weight. The aircraft type segmentation distinguishes between fixed-wing and rotary-wing aircraft, with fixed-wing aircraft currently dominating the market due to their larger fleet sizes and higher adoption rates of advanced avionics systems. Each of these segments presents unique growth opportunities and challenges, contributing to the overall market expansion and technological evolution of Aircraft Interface Devices.

Global Aircraft Interface Device Market Size and Share by Region - Geographic distribution

The global Aircraft Interface Device market exhibits varying growth patterns and adoption rates across different regions, reflecting the diverse aviation landscapes and technological readiness of each area. North America, with its large commercial aviation sector and numerous technology companies, is expected to maintain a significant market share, driven by early adoption of advanced avionics systems and the presence of major aircraft manufacturers. Europe, known for its strong aviation industry and emphasis on technological innovation, is likely to show steady growth, particularly in Western European countries with well-established airline networks. The Asia-Pacific region is anticipated to experience the highest growth rates, fueled by the rapid expansion of commercial aviation, increasing air travel demand, and significant investments in modernizing aviation infrastructure. The Middle East, with its focus on becoming a global aviation hub, presents substantial opportunities for AID market growth. Latin America and Africa, while currently smaller markets, are expected to see gradual adoption of AID technologies as their aviation sectors develop and modernize.

Regional Analysis of the Aircraft Interface Device Market - Detailed regional market performance

A detailed regional analysis of the Aircraft Interface Device market reveals distinct growth patterns and market dynamics across different geographical areas. In North America, the market is characterized by high adoption rates of advanced avionics technologies, driven by the presence of major aircraft manufacturers and a large commercial aviation sector. The region benefits from strong technological infrastructure and significant investments in aviation R&D, positioning it as a leader in AID innovation and implementation. Europe follows closely, with countries like Germany, France, and the UK showing strong demand for AID solutions, supported by stringent aviation safety regulations and a focus on operational efficiency. The Asia-Pacific region presents a dynamic market landscape, with countries like China and India experiencing rapid growth in air travel demand, leading to increased investments in modern aircraft and avionics systems. The Middle East, particularly the Gulf Cooperation Council (GCC) countries, shows strong potential for AID market growth, driven by ambitious aviation expansion plans and the region's strategic focus on becoming global aviation hubs. Latin America and Africa, while currently smaller markets, are expected to see gradual adoption of AID technologies as their aviation sectors continue to develop and modernize.

Leading Company Profiles in the Aircraft Interface Device Market - Industry players and strategies

The Aircraft Interface Device market features a diverse array of leading companies, each employing distinct strategies to capture market share and drive innovation. Boeing, a global aerospace giant, leverages its extensive industry experience and strong relationships with airlines to offer comprehensive avionics solutions, including advanced AID systems. Honeywell International Inc. focuses on developing cutting-edge connectivity solutions and integrating artificial intelligence capabilities into its AID offerings. Collins Aerospace emphasizes the development of lightweight and compact AID solutions to address fuel efficiency concerns. Thales Group, known for its expertise in aerospace and defense technologies, concentrates on enhancing cybersecurity features in its AID products. Astronics Corporation and Teledyne Controls LLC specialize in innovative hardware solutions and wireless connectivity options. Viasat, Inc. differentiates itself through its focus on satellite-based connectivity solutions for aircraft. These companies employ various strategies, including strategic partnerships, acquisitions of innovative startups, and continuous investment in R&D, to maintain their competitive edge and address the evolving needs of the aviation industry.

Porter's Five Forces Analysis of the Aircraft Interface Device Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the Aircraft Interface Device market. The threat of new entrants is moderate, as the market requires significant technological expertise and established relationships with aircraft manufacturers and airlines, creating barriers to entry. However, the growing demand for advanced avionics solutions may attract new players, particularly in the software and wireless connectivity segments. The bargaining power of buyers, primarily airlines and aircraft operators, is relatively high due to the availability of multiple AID solutions and the significant investment involved in implementation. Suppliers of critical components and technologies hold moderate bargaining power, as the market relies on specialized electronic components and software platforms. The threat of substitute products or technologies is low, given the unique functionality of AIDs in connecting aircraft systems with portable devices. Competitive rivalry within the market is intense, with both established aerospace companies and specialized technology providers competing on factors such as technological innovation, product features, and pricing. This competitive landscape drives continuous innovation and improvement in AID solutions, benefiting end-users but also challenging companies to differentiate their offerings.

SWOT Analysis of the Aircraft Interface Device Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the Aircraft Interface Device market reveals a complex landscape of strengths, weaknesses, opportunities, and threats. The market's primary strengths include the growing demand for digital solutions in aviation, the increasing adoption of electronic flight bags, and the potential for significant operational efficiencies through AID implementation. The technology's ability to enhance flight safety and reduce pilot workload further strengthens its market position. However, weaknesses exist in the form of high initial implementation costs and concerns regarding cybersecurity and data protection, which may hinder adoption in some segments. Opportunities abound in the retrofit market, as airlines seek to modernize existing aircraft fleets, and in the development of advanced wireless connectivity solutions. The market also benefits from the aviation industry's overall trend toward digital transformation and connected aircraft concepts. Threats to the market include potential regulatory challenges, the complexity of integrating AIDs with diverse aircraft systems, and the rapid pace of technological change, which may render some solutions obsolete quickly. Additionally, economic uncertainties and fluctuations in the aviation industry could impact investment in AID technologies.

Aircraft Interface Device Market Value Chain Analysis - Industry structure and value flow

The Aircraft Interface Device market value chain encompasses a complex network of activities and stakeholders, each contributing to the development and delivery of AID solutions. At the core of the value chain are the technology developers and manufacturers who design and produce AID hardware and software components. These companies work closely with suppliers of specialized electronic components, sensors, and connectivity modules to create integrated AID systems. The value chain also includes system integrators who ensure seamless compatibility between AIDs and existing aircraft avionics systems. Aircraft manufacturers play a crucial role in the value chain by incorporating AIDs into new aircraft designs or certifying retrofit installations. Airlines and aircraft operators represent the end-users who derive value from AID implementations through improved operational efficiency and enhanced flight safety. Additionally, maintenance, repair, and overhaul (MRO) service providers contribute to the value chain by offering installation, integration, and ongoing support services for AID systems. The value chain is further supported by regulatory bodies that establish certification standards and ensure compliance with aviation safety regulations.

Key Investment Insights in the Aircraft Interface Device Market - Strategic investment recommendations

The Aircraft Interface Device market presents several compelling investment opportunities for stakeholders looking to capitalize on the aviation industry's digital transformation. Investors should consider focusing on companies that are developing advanced wireless connectivity solutions, as this segment is expected to see significant growth due to its flexibility and ease of installation. There is also strong potential in firms specializing in artificial intelligence and machine learning integration for AIDs, as these technologies promise to enhance predictive maintenance capabilities and improve data analytics. The retrofit segment offers attractive investment prospects, given the large number of existing aircraft that could benefit from AID upgrades. Strategic investments in cybersecurity solutions for AID systems are recommended, as data protection becomes increasingly critical in connected aircraft environments. Additionally, companies focusing on developing lightweight and compact AID solutions to address fuel efficiency concerns present interesting investment opportunities. Investors should also consider the potential of emerging markets, particularly in the Asia-Pacific region, where rapid aviation sector growth is driving demand for modern avionics systems.

Aircraft Interface Device Market Conclusion - Summary and key takeaways

The Aircraft Interface Device market stands at the forefront of aviation's digital transformation, offering significant potential for growth and innovation. With a projected compound annual growth rate of 14.92%, the market is set to expand from 264.45 Million in 2026 to 700.14 Million by 2033, driven by the increasing adoption of electronic flight bags, the demand for real-time data connectivity, and the aviation industry's push for operational efficiency. The market's diverse segmentation, including line fit and retrofit installations, hardware and software platforms, and wired and wireless connectivity options, provides multiple avenues for growth and specialization. While challenges exist in terms of implementation costs and cybersecurity concerns, the overall market trajectory remains positive, supported by the industry's focus on enhancing flight safety and reducing pilot workload. As airlines and aircraft operators continue to prioritize digital solutions and connected aircraft concepts, the Aircraft Interface Device market is poised to play a crucial role in shaping the future of aviation technology and operations.

Research Methodology - How this research was conducted

This comprehensive market research on the Aircraft Interface Device industry was conducted using a robust and multi-faceted methodology to ensure accuracy and reliability of findings. The research process began with extensive secondary research, involving the analysis of industry reports, company annual reports, regulatory filings, and relevant publications from aviation authorities and technology associations. Primary research was then conducted through interviews with key industry stakeholders, including AID manufacturers, airline executives, aviation technology experts, and regulatory officials. This combination of top-down and bottom-up approaches allowed for the triangulation of data and validation of market size estimates and growth projections. Market segmentation was performed based on fit type, platform, connectivity, and aircraft type, with careful consideration given to regional variations and emerging trends. The research team employed advanced data analysis techniques to interpret complex market dynamics and forecast future growth scenarios. Throughout the process, particular attention was paid to recent developments in the aviation industry, technological advancements, and regulatory changes that could impact the AID market.

Research Scope - Coverage and limitations

This research report on the Aircraft Interface Device market provides comprehensive coverage of the global industry, focusing on key aspects such as market size, growth trends, competitive landscape, and regional dynamics. The scope encompasses both hardware and software components of AID systems, including wired and wireless connectivity solutions for fixed-wing and rotary-wing aircraft. The research covers the period from 2025 to 2032, with historical data and future projections analyzed to provide a complete market overview. While the report aims to offer detailed insights into major market segments and regions, it is important to note certain limitations. The research primarily focuses on commercial and general aviation sectors, with limited coverage of military applications. Additionally, while regional analysis is provided, the level of detail may vary across different geographical areas due to data availability and market maturity. The report does not delve into highly technical specifications of individual AID products but rather focuses on market trends and strategic insights. Despite these limitations, the research provides a robust foundation for understanding the current state and future potential of the Aircraft Interface Device market.

Key Companies and Recent Developments in the Aircraft Interface Device Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Aircraft Interface Device market features several key players who are driving innovation and shaping industry trends through their recent developments and strategic initiatives. Boeing continues to expand its avionics portfolio with advanced AID solutions, focusing on integration with next-generation aircraft systems. Honeywell International Inc. recently announced the launch of its next-generation wireless AID, emphasizing enhanced connectivity and data analytics capabilities. Collins Aerospace has formed strategic partnerships with major airlines to implement its lightweight AID solutions across retrofit programs. Thales Group has made significant strides in cybersecurity for AID systems, introducing advanced encryption technologies to protect flight data. Astronics Corporation unveiled a new line of compact AID hardware designed for easy installation in both new and existing aircraft. Teledyne Controls LLC has expanded its wireless connectivity offerings, introducing solutions that support multiple portable device platforms. Viasat, Inc. has strengthened its position in the market through partnerships with satellite communication providers, enhancing global connectivity options for AID systems. These companies, along with others in the market, continue to drive technological advancements through product launches, strategic collaborations, and investments in research and development, shaping the future of Aircraft Interface Devices in the aviation industry.