North America Automotive Sensors Market Overview - Definition, scope, and significance

Automotive sensors are electronic devices that detect, measure, and transmit data about various vehicle parameters to the electronic control units (ECUs) for monitoring and control purposes. In the North American automotive industry, these sensors play a critical role in enhancing vehicle performance, safety, fuel efficiency, and overall driving experience. The market encompasses a wide range of sensor types including position sensors, temperature sensors, pressure sensors, image sensors, MEMS, and LED sensors, which are integrated across different vehicle systems such as chassis, powertrain, safety & security, body electronics, and ADAS applications. The significance of this market lies in its fundamental contribution to the evolution of modern vehicles, particularly as the automotive industry transitions toward electrification, autonomous driving, and connected vehicle technologies.

North America Automotive Sensors Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The North American automotive sensors market is primarily driven by increasing vehicle production, stringent government regulations regarding emissions and safety, and growing consumer demand for advanced driver assistance systems (ADAS). The rising adoption of electric vehicles and the push toward autonomous driving technologies are creating substantial demand for sophisticated sensor systems. However, the market faces restraints such as high development costs, complex integration challenges, and supply chain disruptions. Challenges include maintaining sensor accuracy in harsh environmental conditions, managing electromagnetic interference, and addressing cybersecurity concerns in connected vehicles. Significant opportunities exist in the development of multi-functional sensors, miniaturization technologies, and the integration of artificial intelligence with sensor systems to enhance predictive capabilities and overall vehicle intelligence.

North America Automotive Sensors Market Growth Trends - Current and emerging trends shaping the market

The North American automotive sensors market is experiencing several transformative trends that are reshaping the industry landscape. There is a notable shift toward the integration of multiple sensor functionalities into single units, reducing overall system complexity and cost. The market is witnessing increased adoption of MEMS (Micro-Electro-Mechanical Systems) sensors due to their small size, low power consumption, and high reliability. Another significant trend is the growing demand for high-resolution image sensors for advanced driver assistance systems and autonomous driving applications. The transition toward electric vehicles is driving demand for specialized sensors for battery management, thermal monitoring, and power electronics. Additionally, the market is seeing increased focus on sensor fusion technologies that combine data from multiple sensors to provide more accurate and reliable information for vehicle control systems.

COVID-19 Impact on the North America Automotive Sensors Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially caused significant disruptions to the North American automotive sensors market, with production halts, supply chain interruptions, and reduced vehicle sales during 2020 and early 2021. However, the market demonstrated resilience and began showing signs of recovery as automotive manufacturing resumed and demand for vehicles increased. The pandemic accelerated certain trends, including the adoption of contactless technologies and the need for enhanced vehicle safety features. The recovery trajectory has been supported by government stimulus measures, pent-up consumer demand, and the automotive industry's focus on building more resilient supply chains. As of 2023, the market has largely recovered to pre-pandemic levels, with continued growth driven by technological advancements and the automotive industry's transition toward electrification and autonomous driving.

North America Automotive Sensors Market Competitive Landscape - Major competitors and market consolidation

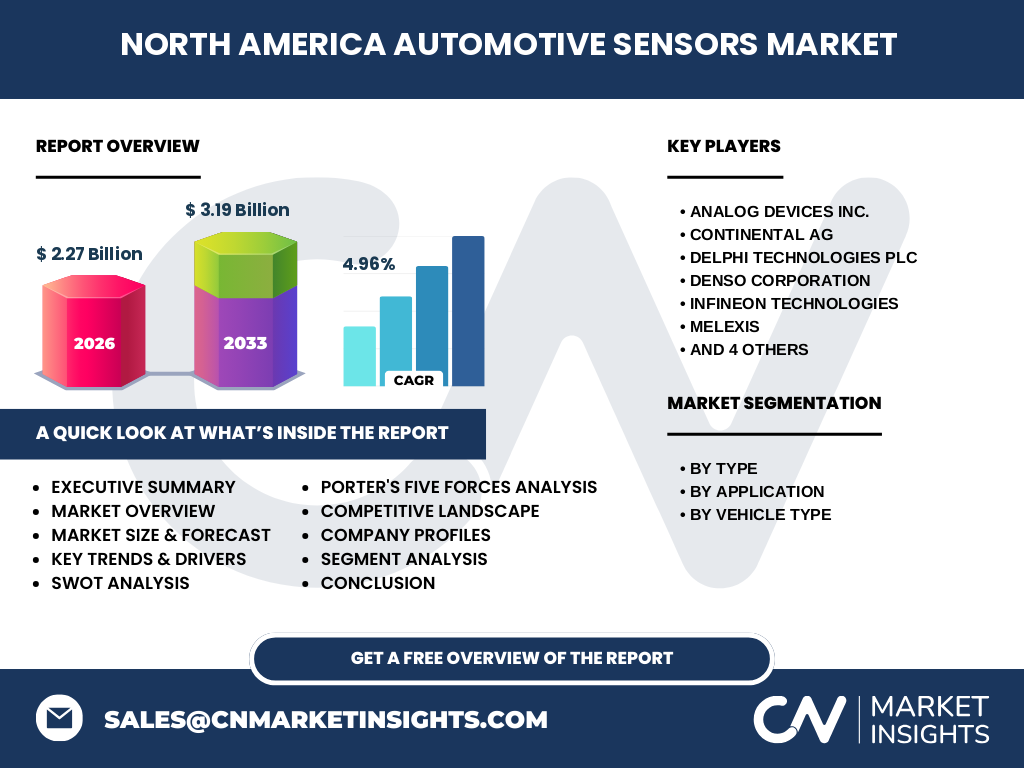

The North American automotive sensors market features a mix of established global players and specialized sensor manufacturers competing for market share. The competitive landscape is characterized by intense rivalry among key players such as Analog Devices Inc., Continental AG, Delphi Technologies PLC, Denso Corporation, Infineon Technologies, Melexis, NXP Semiconductors NV, ON Semiconductors, Robert Bosch GmbH, and Texas Instruments Incorporated. These companies are engaged in continuous innovation, strategic partnerships, and mergers & acquisitions to strengthen their market positions. The market is witnessing increasing consolidation as larger players acquire smaller specialized companies to expand their sensor portfolios and technological capabilities. Competition is primarily based on product innovation, pricing strategies, quality, and the ability to provide comprehensive sensor solutions for emerging automotive technologies.

Executive Summary - High-level overview and key findings about North America Automotive Sensors Market

The North American automotive sensors market is positioned for steady growth, with the market size projected to reach 2.27 billion in 2026 and expand to 3.19 billion by 2033, representing a CAGR of 4.96%. The market is segmented by type, application, and vehicle type, with position sensors, temperature sensors, and pressure sensors being key sensor categories. Applications span across chassis, safety & security, body electronics, powertrain, and ADAS systems, with passenger cars representing the largest vehicle segment. The market is characterized by strong competition among major players and is driven by technological advancements, regulatory requirements, and the automotive industry's evolution toward electrification and autonomy. Key growth opportunities exist in the development of advanced sensor technologies for electric vehicles and autonomous driving systems.

North America Automotive Sensors Market Forecast - Projections for 2025-2032 period

The North American automotive sensors market is expected to demonstrate steady growth throughout the forecast period from 2025 to 2032, with the market expanding from 2.27 billion in 2026 to 3.19 billion by 2033. This growth trajectory reflects a compound annual growth rate of 4.96%, driven by increasing vehicle production, technological advancements, and the automotive industry's transition toward more sophisticated vehicle systems. The forecast period will likely see accelerated adoption of advanced sensors for electric vehicles, autonomous driving systems, and connected car technologies. Market growth will be particularly strong in segments related to ADAS applications, electric vehicle components, and safety systems, as regulatory requirements become more stringent and consumer demand for advanced vehicle features continues to rise.

North America Automotive Sensors Market Size and Share by Segmentation - Breakdown by {segmentData}

The North American automotive sensors market is segmented by type, application, and vehicle type. By type, the market includes LED sensors, image sensors, position sensors, temperature sensors, pressure sensors, and MEMS, with position sensors and temperature sensors typically holding significant market share due to their widespread application across vehicle systems. By application, the market is divided into chassis, safety & security, body electronics, powertrain, and ADAS, with the powertrain and safety & security segments traditionally commanding substantial shares. By vehicle type, the market is categorized into LCV (Light Commercial Vehicles), HCV (Heavy Commercial Vehicles), and passenger cars, with passenger cars representing the largest segment due to higher production volumes and greater sensor integration per vehicle. Each segment shows distinct growth patterns based on technological trends and regulatory requirements.

Global North America Automotive Sensors Market Size and Share by Region - Geographic distribution

The North American automotive sensors market encompasses the United States, Canada, and Mexico, with the United States representing the largest market share due to its substantial automotive manufacturing base and high vehicle ownership rates. The U.S. market benefits from the presence of major automotive OEMs, advanced technological infrastructure, and strong research and development capabilities. Canada contributes to the market through its automotive manufacturing facilities and focus on electric vehicle technologies. Mexico has emerged as an important automotive manufacturing hub, driving demand for sensors through its growing vehicle production capabilities. The regional distribution reflects varying levels of automotive industry maturity, technological adoption rates, and regulatory environments across the three countries, with the United States leading in terms of market size and technological sophistication.

Regional Analysis of the North America Automotive Sensors Market - Detailed regional market performance

The North American automotive sensors market exhibits distinct characteristics across different regions within the continent. The United States dominates the market, accounting for the largest share due to its extensive automotive manufacturing infrastructure, presence of major OEMs, and high adoption rates of advanced vehicle technologies. The U.S. market is characterized by strong demand for sensors in autonomous driving systems, electric vehicles, and advanced safety features. Canada's market is driven by its focus on electric vehicle development and automotive research, with particular emphasis on cold-weather sensor performance. Mexico has experienced rapid growth in automotive sensor demand due to its expanding manufacturing capabilities and increasing vehicle production, particularly in the automotive clusters of Guanajuato and Puebla. Each region presents unique opportunities and challenges based on local manufacturing capabilities, regulatory requirements, and technological adoption patterns.

Leading Company Profiles in the North America Automotive Sensors Market - Industry players and strategies

The North American automotive sensors market is led by several prominent companies, each with distinct strategic approaches and technological strengths. Analog Devices Inc. focuses on high-performance sensor solutions with advanced signal processing capabilities. Continental AG leverages its comprehensive automotive expertise to provide integrated sensor systems for various vehicle applications. Delphi Technologies PLC specializes in powertrain and safety sensor technologies with a strong emphasis on innovation. Denso Corporation brings Japanese technological excellence to the North American market, particularly in thermal management and environmental sensors. Infineon Technologies is a leader in semiconductor-based sensor solutions, while Melexis focuses on intelligent sensor systems for automotive applications. NXP Semiconductors NV provides advanced sensor solutions for connected and autonomous vehicles. ON Semiconductors emphasizes energy-efficient sensor technologies, Robert Bosch GmbH offers comprehensive sensor portfolios, and Texas Instruments Incorporated brings extensive experience in analog and embedded processing solutions for automotive sensors.

Porter's Five Forces Analysis of the North America Automotive Sensors Market - Competitive forces assessment

The North American automotive sensors market is influenced by several competitive forces as analyzed through Porter's framework. The threat of new entrants is moderate due to high capital requirements, technological complexity, and the need for established relationships with automotive OEMs. Bargaining power of suppliers is relatively low as sensor manufacturers have multiple component suppliers and can often backward integrate. The bargaining power of buyers (automotive OEMs) is high given their large purchase volumes and ability to switch between suppliers. The threat of substitute products is moderate, as alternative sensing technologies may emerge but face integration challenges. Competitive rivalry is intense among the major players, driven by technological innovation, pricing pressures, and the need to differentiate through quality and reliability. The overall industry attractiveness is moderate to high, supported by steady market growth and technological advancement opportunities.

SWOT Analysis of the North America Automotive Sensors Market - Strengths, weaknesses, opportunities, threats

The North American automotive sensors market exhibits several key strengths, including advanced technological infrastructure, strong presence of leading sensor manufacturers, and high demand for sophisticated vehicle systems. The market benefits from robust research and development capabilities and a well-established automotive manufacturing base. However, weaknesses include high development costs, complex integration requirements, and vulnerability to supply chain disruptions. Significant opportunities exist in the growing electric vehicle market, autonomous driving technologies, and the increasing demand for advanced safety systems. The market also benefits from supportive government regulations regarding vehicle safety and emissions. Threats include intense competition, rapid technological changes that may render existing technologies obsolete, and potential economic downturns affecting automotive production. Additionally, cybersecurity concerns and data privacy issues pose challenges as vehicles become more connected and sensor-dependent.

North America Automotive Sensors Market Value Chain Analysis - Industry structure and value flow

The value chain of the North American automotive sensors market encompasses several interconnected stages, starting with raw material suppliers who provide semiconductor materials, ceramics, and other essential components. These materials flow to component manufacturers who produce individual sensor elements and integrated circuits. The components are then assembled by sensor manufacturers into complete sensor units, incorporating signal processing and packaging technologies. These finished sensors are distributed through various channels to automotive OEMs and Tier-1 suppliers, who integrate them into vehicle systems. The value chain also includes testing and validation services, calibration facilities, and aftermarket distribution networks. Throughout this chain, value is added through technological innovation, quality improvements, miniaturization, and the development of multi-functional sensors. The industry structure is characterized by close collaboration between sensor manufacturers and automotive OEMs to ensure compatibility and performance optimization.

Key Investment Insights in the North America Automotive Sensors Market - Strategic investment recommendations

The North American automotive sensors market presents compelling investment opportunities, particularly in emerging technologies and growing application areas. Strategic investments should focus on the development of advanced sensors for electric vehicles, including battery management systems, thermal monitoring, and power electronics. The autonomous driving segment offers significant potential for investments in high-resolution image sensors, LiDAR technologies, and sensor fusion systems. Investments in MEMS technology for miniaturized, multi-functional sensors are recommended due to their growing adoption across vehicle systems. The safety and ADAS segments represent attractive investment targets, driven by regulatory requirements and consumer demand for advanced safety features. Additionally, investments in artificial intelligence integration with sensor systems, cybersecurity solutions for connected vehicles, and sustainable manufacturing processes for sensors are likely to yield strong returns. Companies should also consider strategic partnerships and acquisitions to acquire specialized technologies and expand market presence.

North America Automotive Sensors Market Conclusion - Summary and key takeaways

The North American automotive sensors market is on a steady growth trajectory, projected to expand from 2.27 billion in 2026 to 3.19 billion by 2033, representing a CAGR of 4.96%. The market is characterized by technological advancement, increasing vehicle electrification, and growing demand for autonomous driving capabilities. Key sensor types including position sensors, temperature sensors, and pressure sensors continue to dominate, while applications in safety & security, powertrain, and ADAS systems drive significant demand. The competitive landscape features major global players engaged in continuous innovation and strategic partnerships. Despite challenges such as high development costs and integration complexities, the market presents substantial opportunities in electric vehicles, autonomous driving, and advanced safety systems. The future of the market will be shaped by technological innovation, regulatory requirements, and the automotive industry's evolution toward more connected and intelligent vehicles.

Research Methodology - How this research was conducted

The research methodology for this market analysis employed a comprehensive approach combining primary and secondary research techniques. Primary research involved interviews with industry experts, sensor manufacturers, automotive OEMs, and technology providers to gather firsthand insights into market trends, challenges, and opportunities. Secondary research included extensive analysis of industry reports, company financial statements, technical publications, regulatory documents, and market databases. The research methodology incorporated data triangulation to validate findings across multiple sources and ensure accuracy. Market sizing was conducted using both top-down and bottom-up approaches, considering factors such as vehicle production volumes, sensor penetration rates, and average sensor content per vehicle. The analysis also considered macroeconomic factors, technological trends, and regulatory environments affecting the North American automotive sensors market.

Research Scope - Coverage and limitations

This research focuses specifically on the North American automotive sensors market, covering the United States, Canada, and Mexico. The scope encompasses various sensor types including LED, image sensors, position sensors, temperature sensors, pressure sensors, and MEMS, across applications such as chassis, safety & security, body electronics, powertrain, and ADAS systems. The research covers vehicle segments including LCV, HCV, and passenger cars. The analysis period extends from historical data through 2026, with forecasts provided through 2033. Limitations include the exclusion of certain niche sensor technologies not widely adopted in the North American market, and the focus on automotive applications rather than industrial or consumer sensor markets. The research also acknowledges that rapid technological changes may impact future market dynamics in ways that are difficult to predict with complete accuracy.

Key Companies and Recent Developments in the North America Automotive Sensors Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The North American automotive sensors market features several leading companies that have recently announced significant developments. Analog Devices Inc. has expanded its automotive sensor portfolio with new high-precision MEMS accelerometers for vehicle dynamics and safety applications. Continental AG announced strategic partnerships to develop advanced radar sensors for autonomous driving systems, while also launching new pressure sensor technologies for electric vehicle battery management. Delphi Technologies PLC introduced innovative position sensor solutions for electric power steering systems and powertrain applications. Denso Corporation has made significant investments in thermal management sensors for electric vehicles and announced collaborations with AI companies for smart sensor development. Infineon Technologies launched new semiconductor-based sensor solutions with enhanced cybersecurity features for connected vehicles. Melexis introduced advanced magnetic position sensors with improved accuracy for electric vehicle applications. NXP Semiconductors NV announced new radar sensor chips for ADAS systems and expanded its automotive sensor manufacturing capacity. ON Semiconductors developed energy-efficient image sensors for surround-view camera systems. Robert Bosch GmbH unveiled next-generation MEMS sensors with improved reliability for autonomous driving, and Texas Instruments Incorporated announced new integrated sensor solutions combining multiple sensing functions for space and cost optimization in vehicles.