North America Fourth Party Logistics Market Overview - Definition, scope, and significance

The North America Fourth Party Logistics (4PL) market represents a sophisticated segment of supply chain management where an independent entity orchestrates and manages an entire supply chain on behalf of a client. Unlike traditional third-party logistics providers, 4PL providers assume a more comprehensive role, integrating multiple logistics services, technology platforms, and transportation modes to create end-to-end supply chain solutions. This market encompasses strategic planning, network design, carrier selection, and performance optimization across various industry verticals. The significance of this market lies in its ability to provide businesses with enhanced visibility, cost optimization, and operational efficiency through a single point of contact for complex logistics operations. As supply chains become increasingly complex and globalized, the demand for 4PL services has grown substantially, driven by the need for specialized expertise in managing multi-modal transportation, inventory optimization, and digital transformation initiatives.

North America Fourth Party Logistics Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The North America 4PL market is propelled by several key drivers, including the increasing complexity of global supply chains, the need for cost optimization, and the growing adoption of digital technologies. Companies are seeking to outsource their logistics operations to focus on core competencies, driving demand for comprehensive 4PL solutions. The rise of e-commerce and omnichannel retail has further accelerated the need for sophisticated logistics management. However, the market faces certain restraints, such as the high initial investment required for technology integration and the challenge of finding qualified 4PL providers with the necessary expertise and resources. Additionally, concerns about data security and the potential loss of control over critical supply chain operations can hinder adoption. Despite these challenges, significant opportunities exist in the market, particularly in the areas of sustainability initiatives, last-mile delivery optimization, and the integration of advanced technologies such as artificial intelligence and blockchain. The growing emphasis on supply chain resilience and risk management also presents opportunities for 4PL providers to offer value-added services.

North America Fourth Party Logistics Market Growth Trends - Current and emerging trends shaping the market

The North America 4PL market is experiencing several notable growth trends that are reshaping the industry landscape. One prominent trend is the increasing adoption of cloud-based logistics platforms, which enable real-time visibility and data-driven decision-making across the supply chain. Another significant trend is the integration of Internet of Things (IoT) devices and sensors, allowing for enhanced tracking and monitoring of shipments and inventory. The market is also witnessing a growing emphasis on sustainability, with 4PL providers offering green logistics solutions and helping clients reduce their carbon footprint. Additionally, there is a trend towards the consolidation of logistics services, with larger players acquiring specialized providers to offer more comprehensive solutions. The emergence of digital freight marketplaces and the use of predictive analytics for demand forecasting are also shaping the market. Furthermore, the COVID-19 pandemic has accelerated the adoption of 4PL services as companies seek to build more resilient and flexible supply chains capable of withstanding future disruptions.

COVID-19 Impact on the North America Fourth Party Logistics Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a profound impact on the North America 4PL market, initially causing significant disruptions to supply chains and logistics operations. The sudden shift in consumer behavior, with a surge in e-commerce demand and changes in inventory management practices, forced companies to rapidly adapt their logistics strategies. This crisis highlighted the importance of supply chain resilience and flexibility, leading to increased interest in 4PL services as a means to optimize and diversify logistics networks. During the pandemic, 4PL providers played a crucial role in helping clients navigate supply chain disruptions, implement contingency plans, and maintain business continuity. The recovery trajectory has been characterized by a renewed focus on digital transformation and the adoption of advanced technologies to enhance supply chain visibility and agility. As the market recovers, there is a growing emphasis on building more robust and diversified supply chains, with 4PL providers offering expertise in risk management and scenario planning. The pandemic has also accelerated the trend towards nearshoring and regionalization of supply chains, creating new opportunities for 4PL providers to offer localized logistics solutions.

North America Fourth Party Logistics Market Competitive Landscape - Major competitors and market consolidation

The North America 4PL market features a competitive landscape characterized by a mix of global logistics giants and specialized regional players. Major competitors in this market include Allyn International Services Inc., CEVA Logistics AG, DAMCO, DB Schenker, Deutsche Post AG, GEFCO Group, GEODIS, Logistics Plus Inc., UPS Supply Chain Solutions, and XPO Logistics, Inc. These companies compete on various factors, including technological capabilities, industry expertise, geographic coverage, and service offerings. The market has witnessed significant consolidation in recent years, with larger players acquiring smaller, specialized firms to expand their service portfolios and enhance their technological capabilities. This trend towards consolidation is driven by the need to offer comprehensive, end-to-end supply chain solutions and to compete effectively in an increasingly complex logistics environment. The competitive landscape is also shaped by the entry of technology-driven startups that offer innovative solutions in areas such as digital freight matching and supply chain analytics. As the market continues to evolve, competition is intensifying, with providers focusing on differentiation through value-added services, industry-specific expertise, and advanced technology integration.

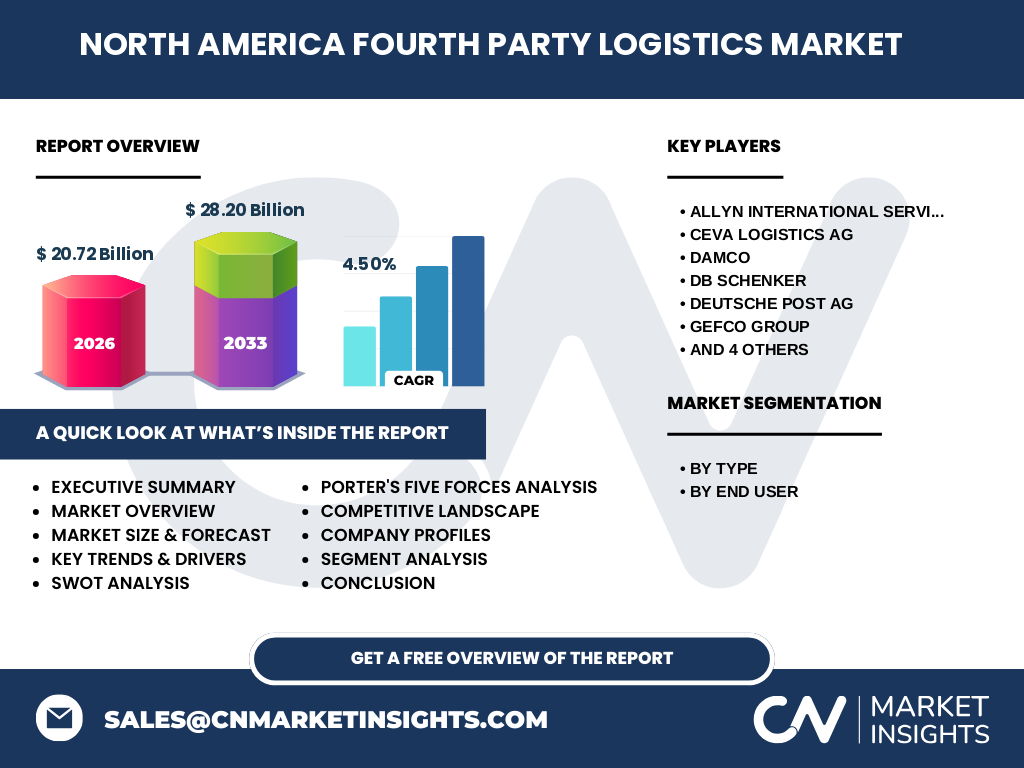

Executive Summary - High-level overview and key findings about North America Fourth Party Logistics Market

The North America Fourth Party Logistics market is poised for significant growth, with the market size projected to reach 20.72 billion in 2026 and expand to 28.20 billion by 2033, representing a compound annual growth rate (CAGR) of 4.50%. This growth is driven by the increasing complexity of supply chains, the need for cost optimization, and the growing adoption of digital technologies across various industry verticals. The market is segmented by type, including Synergy Plus Operating Model, Solution Integrator Model, and Industry Innovator Model, catering to diverse end-user sectors such as Aerospace & Defense, Automotive, Consumer Electronics, Food & Beverage, Industrial, Healthcare, and Retail. Key players in the market, including Allyn International Services Inc., CEVA Logistics AG, and UPS Supply Chain Solutions, are focusing on technological innovation and strategic partnerships to maintain their competitive edge. The COVID-19 pandemic has accelerated the adoption of 4PL services, highlighting the importance of supply chain resilience and flexibility. As the market continues to evolve, opportunities exist in areas such as sustainability initiatives, last-mile delivery optimization, and the integration of advanced technologies like artificial intelligence and blockchain.

North America Fourth Party Logistics Market Forecast - Projections for 2025-2032 period

The North America Fourth Party Logistics market is expected to experience steady growth over the forecast period from 2025 to 2032. Based on current projections, the market size is anticipated to reach 20.72 billion in 2026, with a compound annual growth rate (CAGR) of 4.50%. This growth trajectory is expected to continue, with the market expanding to 28.20 billion by 2033. The forecast period is likely to be characterized by several key trends and developments. Firstly, the increasing adoption of digital technologies and advanced analytics is expected to drive efficiency gains and cost savings for 4PL providers and their clients. Secondly, the growing emphasis on sustainability and green logistics solutions is likely to create new opportunities for market expansion. Thirdly, the ongoing consolidation in the logistics industry is expected to result in the emergence of larger, more comprehensive 4PL providers capable of offering end-to-end supply chain solutions. Additionally, the market is likely to see increased investment in last-mile delivery capabilities and the integration of emerging technologies such as autonomous vehicles and drones. As supply chains continue to evolve in response to changing consumer demands and global economic conditions, the role of 4PL providers in optimizing and managing complex logistics networks is expected to become increasingly critical.

North America Fourth Party Logistics Market Size and Share by Segmentation - Breakdown by {segmentData}

The North America Fourth Party Logistics market is segmented by type and end-user, providing a comprehensive breakdown of the market's composition and growth potential. By type, the market is divided into three main segments: Synergy Plus Operating Model, Solution Integrator Model, and Industry Innovator Model. Each of these models offers distinct approaches to supply chain management and caters to different client needs. The Synergy Plus Operating Model focuses on optimizing existing logistics networks and processes, while the Solution Integrator Model emphasizes the integration of multiple logistics services and technologies. The Industry Innovator Model, on the other hand, is geared towards developing customized, industry-specific solutions that drive innovation and competitive advantage. By end-user, the market serves a diverse range of industries, including Aerospace & Defense, Automotive, Consumer Electronics, Food & Beverage, Industrial, Healthcare, and Retail. Each of these sectors has unique logistics requirements and challenges, driving demand for specialized 4PL services. For instance, the Aerospace & Defense sector requires stringent security measures and complex supply chain management, while the Food & Beverage industry demands specialized handling and temperature-controlled transportation. The Healthcare sector, with its focus on timely delivery of critical medical supplies, presents another significant opportunity for 4PL providers. As the market continues to evolve, these segmentation trends are expected to shape the development of tailored 4PL solutions across various industry verticals.

Global North America Fourth Party Logistics Market Size and Share by Region - Geographic distribution

The North America Fourth Party Logistics market exhibits distinct geographic patterns and regional variations in terms of market size and share. The United States dominates the market, accounting for the largest share due to its advanced logistics infrastructure, high adoption of technology, and diverse industrial base. The U.S. market benefits from a well-developed transportation network, including extensive highway systems, major ports, and a robust air cargo industry, which facilitates efficient logistics operations. Canada, while smaller in market size, represents a significant portion of the North American 4PL market, driven by its strong manufacturing sector and increasing focus on cross-border trade with the United States. Mexico, as part of the North American trade bloc, is emerging as an important market for 4PL services, particularly in industries such as automotive and electronics manufacturing. The regional distribution of the market is also influenced by factors such as population density, industrial concentration, and trade patterns. For instance, the northeastern United States, with its high population density and concentration of manufacturing and distribution centers, represents a key region for 4PL services. Similarly, the west coast, with its major ports and proximity to Asian markets, plays a crucial role in international trade and logistics. As the market continues to evolve, regional variations in economic growth, industrial development, and technological adoption are likely to shape the geographic distribution of 4PL services across North America.

Regional Analysis of the North America Fourth Party Logistics Market - Detailed regional market performance

The North America Fourth Party Logistics market exhibits varying performance across different regions, reflecting the diverse economic landscapes and industrial concentrations within the continent. In the United States, the market is characterized by high maturity and widespread adoption of 4PL services across multiple industry verticals. The northeastern region, including states like New York, New Jersey, and Pennsylvania, represents a significant portion of the market due to its dense population, major ports, and concentration of manufacturing and distribution centers. The Midwest, with its strong manufacturing base and extensive transportation infrastructure, also plays a crucial role in the 4PL market, particularly in industries such as automotive and agriculture. The southern United States, including states like Texas and Georgia, has seen rapid growth in 4PL adoption, driven by the expansion of e-commerce and the region's strategic location for international trade. In Canada, the 4PL market is concentrated in major urban centers such as Toronto, Vancouver, and Montreal, with a focus on cross-border trade with the United States and serving the country's diverse industrial sectors. Mexico's 4PL market is experiencing significant growth, particularly in the northern states bordering the United States, driven by the maquiladora industry and increasing foreign direct investment in manufacturing. The regional analysis also reveals variations in the types of 4PL services in demand, with some regions focusing more on international trade facilitation while others prioritize domestic supply chain optimization.

Leading Company Profiles in the North America Fourth Party Logistics Market - Industry players and strategies

The North America Fourth Party Logistics market is dominated by several key players, each with distinct strategies and areas of expertise. Allyn International Services Inc. is known for its comprehensive supply chain solutions and strong focus on technology integration. The company has been expanding its service offerings through strategic acquisitions and partnerships to enhance its capabilities in areas such as freight forwarding and customs brokerage. CEVA Logistics AG, a subsidiary of CMA CGM, leverages its global network and expertise in contract logistics to offer tailored 4PL solutions across various industries. The company's strategy focuses on digital transformation and sustainability initiatives to meet evolving customer needs. DAMCO, part of the Maersk Group, emphasizes its end-to-end supply chain management capabilities and strong presence in the Asia-Pacific region, which is crucial for North American importers. DB Schenker, with its extensive global network and diverse service portfolio, focuses on providing integrated logistics solutions that combine air, sea, and land transportation with value-added services. Deutsche Post AG, through its DHL Supply Chain division, leverages its strong brand recognition and technological capabilities to offer innovative 4PL solutions, particularly in the e-commerce and healthcare sectors. GEFCO Group, while smaller in scale, specializes in automotive logistics and has been expanding its presence in North America through strategic partnerships. GEODIS, known for its expertise in high-tech and aerospace industries, focuses on providing customized supply chain solutions and has been investing in digital platforms to enhance customer experience. Logistics Plus Inc. differentiates itself through its personalized service approach and strong focus on customer relationships. UPS Supply Chain Solutions leverages its parent company's extensive transportation network to offer integrated logistics solutions, with a particular emphasis on small and medium-sized businesses. XPO Logistics, Inc. has been focusing on technology-driven solutions and has been divesting non-core assets to concentrate on its most profitable segments, including last-mile delivery and less-than-truckload services.

Porter's Five Forces Analysis of the North America Fourth Party Logistics Market - Competitive forces assessment

The North America Fourth Party Logistics market is characterized by a complex interplay of competitive forces, as analyzed through Porter's Five Forces framework. The threat of new entrants in the 4PL market is moderate, as establishing a comprehensive logistics network and gaining client trust requires significant capital investment and industry expertise. However, the market is not entirely closed to new players, particularly those offering innovative technological solutions or niche services. The bargaining power of buyers in the 4PL market is relatively high, as large corporations have the ability to negotiate contracts and demand customized solutions. This is particularly true in industries with complex supply chain requirements, where buyers can leverage their volume and strategic importance to secure favorable terms. The bargaining power of suppliers, primarily referring to transportation and warehousing providers, is moderate. While there are numerous suppliers in the market, capacity constraints and specialized equipment needs can give certain suppliers more leverage. The threat of substitute products or services is low, as 4PL providers offer unique value propositions that combine multiple logistics services and strategic planning capabilities. However, the increasing sophistication of in-house logistics operations and the emergence of digital freight marketplaces present potential alternatives to traditional 4PL services. The intensity of competitive rivalry in the North American 4PL market is high, with numerous global and regional players competing for market share. This competition is driven by factors such as technological innovation, service differentiation, and pricing strategies. The market is also witnessing consolidation through mergers and acquisitions, further intensifying the competitive landscape. Overall, the 4PL market in North America presents a dynamic environment where companies must continually innovate and adapt to maintain their competitive position.

SWOT Analysis of the North America Fourth Party Logistics Market - Strengths, weaknesses, opportunities, threats

The North America Fourth Party Logistics market exhibits a complex set of strengths, weaknesses, opportunities, and threats that shape its competitive landscape and growth potential. Among the key strengths of the market is the presence of well-established logistics infrastructure and a highly skilled workforce, particularly in the United States. This strong foundation enables 4PL providers to offer comprehensive and efficient supply chain solutions. Additionally, the region's advanced technological capabilities and high adoption of digital solutions provide a significant advantage in developing innovative logistics services. The diverse industrial base across North America also presents opportunities for 4PL providers to offer specialized solutions across various sectors. However, the market also faces certain weaknesses, including the high initial investment required for technology integration and the challenge of finding qualified personnel with the necessary expertise in complex supply chain management. Furthermore, concerns about data security and the potential loss of control over critical supply chain operations can be perceived as weaknesses by some potential clients. In terms of opportunities, the market is well-positioned to capitalize on the growing trend towards supply chain digitization and the increasing demand for end-to-end visibility. The emphasis on sustainability and green logistics solutions also presents significant growth opportunities for 4PL providers. Additionally, the ongoing consolidation in the logistics industry creates opportunities for larger players to expand their service offerings and market reach. However, the market also faces threats, including the potential for economic downturns that could impact logistics spending, increasing regulatory scrutiny on data privacy and cross-border trade, and the emergence of disruptive technologies that could challenge traditional 4PL business models. The intensifying competition from both global and regional players also poses a threat to market share and profitability.

North America Fourth Party Logistics Market Value Chain Analysis - Industry structure and value flow

The North America Fourth Party Logistics market value chain is a complex network of interconnected activities and stakeholders that work together to deliver comprehensive supply chain solutions. At the core of this value chain are the 4PL providers, who act as strategic orchestrators, coordinating and managing various logistics services on behalf of their clients. These providers typically engage with multiple tiers of suppliers and partners to create end-to-end supply chain solutions. The primary activities in the 4PL value chain include strategic planning and network design, carrier selection and management, freight forwarding, customs brokerage, warehousing and distribution, and technology integration. Supporting these primary activities are a range of secondary functions such as procurement, human resource management, and financial services. The value chain also encompasses a network of technology providers who supply the digital platforms and analytics tools necessary for effective supply chain management. These technology partners play a crucial role in enabling real-time visibility, data-driven decision-making, and the integration of various logistics services. Additionally, the value chain includes a range of specialized service providers, such as freight auditors, packaging specialists, and reverse logistics experts, who offer niche capabilities that enhance the overall value proposition of 4PL services. The flow of value in this chain is characterized by the aggregation and optimization of logistics services, with 4PL providers leveraging their expertise and scale to create efficiencies and cost savings for their clients. This value creation process is further enhanced by the integration of advanced technologies, which enable improved visibility, predictive analytics, and automation across the supply chain. As the market continues to evolve, the value chain is likely to see further integration and specialization, with 4PL providers focusing on core competencies while partnering with specialized service providers to offer comprehensive solutions.

Key Investment Insights in the North America Fourth Party Logistics Market - Strategic investment recommendations

The North America Fourth Party Logistics market presents several compelling investment opportunities for both existing players and new entrants looking to capitalize on the growing demand for comprehensive supply chain solutions. One key area for investment is in advanced technologies, particularly artificial intelligence and machine learning capabilities that can enhance predictive analytics and optimize supply chain operations. Investors should consider funding the development of digital platforms that offer real-time visibility and seamless integration across multiple logistics services. Another strategic investment opportunity lies in last-mile delivery capabilities, as the e-commerce boom continues to drive demand for efficient and cost-effective final-mile solutions. Investments in automation and robotics for warehousing and distribution centers can also yield significant returns, improving operational efficiency and reducing labor costs. The growing emphasis on sustainability presents opportunities for investments in green logistics solutions, including electric vehicle fleets and energy-efficient warehousing facilities. Additionally, there is potential for investment in specialized 4PL services catering to emerging industries such as healthcare logistics and cold chain management. Strategic acquisitions of smaller, niche players can provide a quick route to market expansion and access to specialized expertise. Investors should also consider funding initiatives focused on enhancing data security and privacy measures, as these become increasingly critical in the management of complex supply chains. Furthermore, investments in talent development and training programs can help address the industry's growing need for skilled professionals capable of managing sophisticated logistics operations. As the market continues to evolve, investments that focus on creating flexible and resilient supply chain solutions are likely to yield the highest returns, given the increasing emphasis on risk management and business continuity in the post-pandemic era.

North America Fourth Party Logistics Market Conclusion - Summary and key takeaways

The North America Fourth Party Logistics market is poised for significant growth and transformation in the coming years, driven by the increasing complexity of global supply chains and the growing demand for comprehensive, technology-driven logistics solutions. With a projected market size of 20.72 billion in 2026 and an expected expansion to 28.20 billion by 2033, representing a CAGR of 4.50%, the market presents substantial opportunities for both established players and new entrants. The market's segmentation by type and end-user highlights the diverse range of services and industries served by 4PL providers, from the Synergy Plus Operating Model to specialized solutions for sectors such as Aerospace & Defense and Healthcare. Key players in the market, including Allyn International Services Inc., CEVA Logistics AG, and UPS Supply Chain Solutions, are focusing on technological innovation, strategic partnerships, and service differentiation to maintain their competitive edge. The COVID-19 pandemic has accelerated the adoption of 4PL services, emphasizing the importance of supply chain resilience and flexibility. As the market continues to evolve, investments in advanced technologies, sustainability initiatives, and last-mile delivery capabilities are likely to be key drivers of growth. The competitive landscape is characterized by intense rivalry and ongoing consolidation, with companies striving to offer end-to-end supply chain solutions that combine multiple logistics services with strategic planning capabilities. Overall, the North America 4PL market presents a dynamic and promising landscape for companies capable of navigating its complexities and delivering value-added solutions to meet the evolving needs of modern supply chains.

Research Methodology - How this research was conducted

The research for this North America Fourth Party Logistics market report was conducted using a comprehensive and rigorous methodology to ensure the accuracy and reliability of the findings. The study employed a combination of primary and secondary research methods to gather and analyze data from various sources. Primary research involved conducting interviews with industry experts, including executives from leading 4PL providers, logistics consultants, and supply chain professionals. These interviews provided valuable insights into market trends, competitive dynamics, and future growth prospects. Additionally, surveys were distributed to a wide range of stakeholders across the logistics industry to gather quantitative data on market size, growth rates, and adoption patterns. Secondary research involved an extensive review of industry reports, company annual reports, press releases, and relevant trade publications. Data from government sources, such as trade statistics and economic indicators, were also analyzed to provide context for market trends. The research team utilized advanced data analytics tools to process and interpret the collected information, ensuring a robust and data-driven analysis. Market size and forecast figures were derived using a combination of top-down and bottom-up approaches, cross-validated with multiple data sources to ensure accuracy. The segmentation analysis was based on a thorough examination of industry classifications and end-user requirements. Competitive landscape assessments were conducted through detailed company profiling and analysis of recent developments, partnerships, and strategic initiatives. The research methodology also incorporated a Porter's Five Forces analysis and a SWOT analysis to provide a comprehensive understanding of the market's competitive dynamics and growth potential. Throughout the research process, data triangulation techniques were employed to verify the consistency and reliability of the findings across different sources and methodologies.

Research Scope - Coverage and limitations

The research scope for this North America Fourth Party Logistics market report encompasses a comprehensive analysis of the market across the United States, Canada, and Mexico. The study covers the period from 2025 to 2033, with historical data provided for context and future projections based on current market trends and growth drivers. The research focuses on the 4PL market as defined by the integration of multiple logistics services under a single strategic provider, excluding traditional third-party logistics (3PL) services. The scope includes an analysis of market size, growth trends, competitive landscape, and key industry players. Segmentation analysis covers both the type of 4PL services offered (Synergy Plus Operating Model, Solution Integrator Model, and Industry Innovator Model) and the end-user industries served (Aerospace & Defense, Automotive, Consumer Electronics, Food & Beverage, Industrial, Healthcare, and Retail). The research also examines regional variations within North America, highlighting differences in market maturity, adoption rates, and growth potential across different geographic areas. However, it's important to note certain limitations in the research scope. The study primarily focuses on the formal 4PL market and may not capture informal or emerging logistics arrangements that fall outside traditional definitions. Additionally, while the research provides insights into key market trends and drivers, it may not fully account for unforeseen disruptive events or technological breakthroughs that could significantly impact the market in the future. The analysis is based on available public information and may not include proprietary data held by individual companies. Furthermore, the research scope does not extend to a detailed analysis of regulatory environments across different countries, which can have a significant impact on logistics operations. Despite these limitations, the research provides a comprehensive overview of the North America 4PL market, offering valuable insights for industry stakeholders, investors, and decision-makers.

Key Companies and Recent Developments in the North America Fourth Party Logistics Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The North America Fourth Party Logistics market is characterized by the presence of several key players, each making significant strides in expanding their service offerings and market presence through various strategic initiatives. Allyn International Services Inc. has recently announced the launch of an advanced supply chain analytics platform, leveraging artificial intelligence to provide clients with enhanced visibility and predictive capabilities. The company has also formed a strategic partnership with a leading e-commerce platform to offer integrated logistics solutions for online retailers. CEVA Logistics AG has made headlines with its acquisition of a specialized pharmaceutical logistics provider, strengthening its position in the healthcare sector. The company has also unveiled a new sustainability initiative aimed at reducing carbon emissions across its North American operations. DAMCO, in collaboration with its parent company Maersk, has introduced a digital freight forwarding platform that integrates ocean, air, and inland transportation services, offering clients a seamless end-to-end logistics experience. DB Schenker has recently expanded its last-mile delivery capabilities through the acquisition of a regional courier service, enhancing its ability to serve e-commerce clients. The company has also launched a new blockchain-based solution for supply chain traceability in the food and beverage industry. Deutsche Post AG, through its DHL Supply Chain division, has announced a major investment in automation technology for its warehousing facilities across North America, aiming to improve efficiency and reduce operational costs. GEFCO Group has formed a strategic alliance with a leading automotive manufacturer to provide integrated logistics solutions for electric vehicle production and distribution. GEODIS has unveiled a new industry-specific 4PL solution for the aerospace sector, leveraging its expertise in complex supply chain management. Logistics Plus Inc. has expanded its service offerings through the acquisition of a customs brokerage firm, enhancing its capabilities in international trade compliance. UPS Supply Chain Solutions has launched a new digital platform for small and medium-sized businesses, offering access to a range of logistics services through a user-friendly interface. XPO Logistics, Inc. has announced the spin-off of its contract logistics business, allowing it to focus on its core less-than-truckload and last-mile delivery services. The company has also introduced a new predictive analytics tool for freight optimization, leveraging machine learning algorithms to improve routing and capacity utilization.