Europe Visual Analytics Market Overview - Definition, scope, and significance

Visual analytics represents the integration of data visualization, human analytical reasoning, and advanced computational methods to enable effective analysis of complex data sets. In the European context, this market encompasses software solutions, platforms, and services that transform raw data into interactive visual representations, allowing organizations to discover patterns, identify trends, and make data-driven decisions. The European visual analytics market serves diverse industries including retail, manufacturing, healthcare, BFSI, and government sectors, addressing the growing need for sophisticated data interpretation tools in an increasingly digital economy. As European businesses face mounting pressure to optimize operations and enhance customer experiences, visual analytics has emerged as a critical technology for maintaining competitive advantage and driving innovation across the continent.

Europe Visual Analytics Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Europe visual analytics market is propelled by several key drivers, including the exponential growth of data generated across industries, increasing adoption of cloud-based solutions, and the rising demand for real-time business intelligence. Organizations across Europe are recognizing the value of data-driven decision-making, creating substantial demand for visual analytics tools. However, the market faces challenges such as data privacy concerns under GDPR regulations, high implementation costs, and the shortage of skilled professionals capable of interpreting complex visual analytics outputs. Despite these restraints, significant opportunities exist in emerging technologies like AI and machine learning integration, the expansion of IoT devices generating vast amounts of data, and the growing need for visual analytics in small and medium enterprises seeking to compete with larger organizations.

Europe Visual Analytics Market Growth Trends - Current and emerging trends shaping the market

The Europe visual analytics market is experiencing several transformative trends that are reshaping the competitive landscape. Cloud-based deployment models are gaining significant traction as organizations seek scalable and cost-effective solutions. The integration of artificial intelligence and machine learning capabilities is enhancing the sophistication of visual analytics platforms, enabling predictive and prescriptive analytics. Mobile-first approaches are becoming increasingly important as remote work continues to influence business operations across Europe. Additionally, there is a growing emphasis on self-service analytics, empowering business users to create their own visualizations without extensive technical expertise. The convergence of visual analytics with other technologies such as augmented reality and natural language processing is creating new possibilities for data exploration and interpretation.

COVID-19 Impact on the Europe Visual Analytics Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly accelerated the adoption of visual analytics solutions across European organizations as businesses faced unprecedented challenges requiring rapid decision-making based on complex, evolving data. The pandemic highlighted the critical need for real-time insights into supply chain disruptions, changing consumer behaviors, and operational efficiency. Healthcare organizations particularly increased their reliance on visual analytics for tracking infection rates, resource allocation, and treatment outcomes. As European economies recover, the visual analytics market continues to benefit from lessons learned during the pandemic, with organizations maintaining and expanding their investments in data visualization capabilities to enhance resilience and agility in future disruptions.

Europe Visual Analytics Market Competitive Landscape - Major competitors and market consolidation

The European visual analytics market features a dynamic competitive landscape characterized by both established technology giants and specialized analytics providers. Major players such as IBM, Microsoft, Oracle, and SAP leverage their extensive enterprise relationships and comprehensive product portfolios to maintain significant market presence. Meanwhile, specialized vendors like Tableau, Qlik, and Alteryx focus on delivering innovative, user-friendly solutions that address specific industry needs. The market is witnessing increasing consolidation through strategic acquisitions and partnerships as companies seek to expand their capabilities and market reach. Competition is intensifying around key differentiators including ease of use, integration capabilities, pricing models, and the ability to handle diverse data sources and complex analytical requirements.

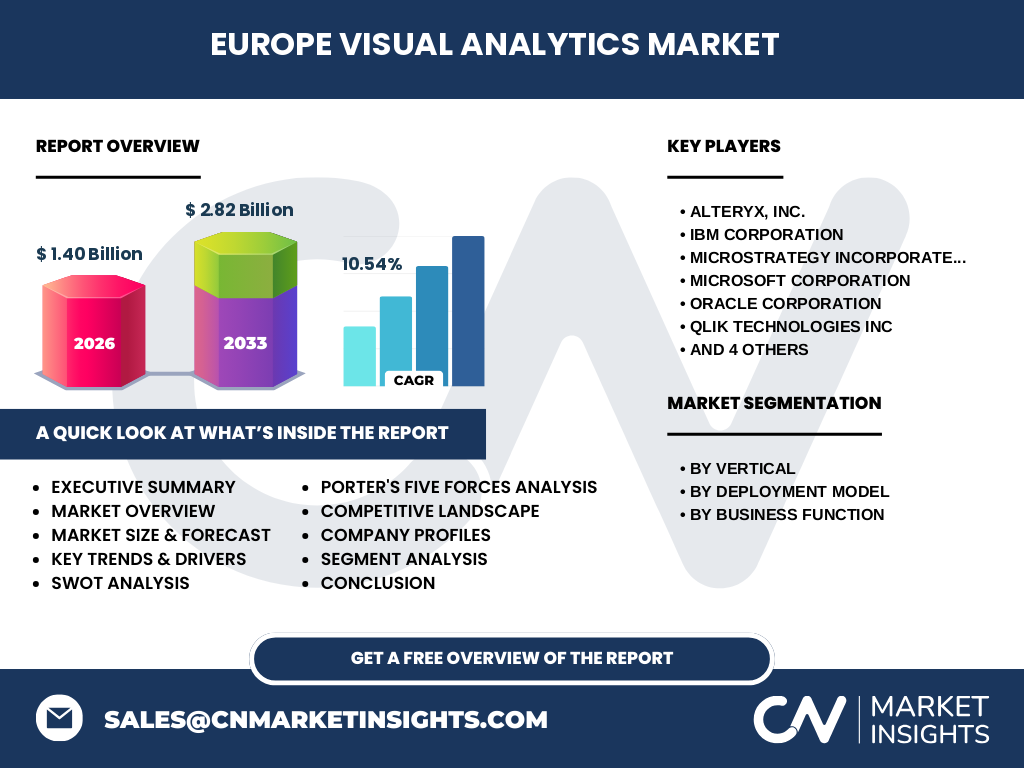

Executive Summary - High-level overview and key findings about Europe Visual Analytics Market

The Europe visual analytics market is positioned for substantial growth, driven by the increasing need for data-driven decision-making across industries and the proliferation of data generated by digital transformation initiatives. With a projected CAGR of 10.54% from 2027 to 2033, the market is expected to nearly double in size, reaching 2.82 billion by 2033. Key segments including retail, BFSI, and healthcare are leading adoption, while cloud deployment models are gaining preference over on-premises solutions. The competitive landscape remains robust with both global technology leaders and specialized analytics providers competing for market share. Despite challenges related to data privacy regulations and implementation complexities, the market presents significant opportunities for vendors who can deliver innovative, user-friendly solutions that address evolving business needs.

Europe Visual Analytics Market Forecast - Projections for 2025-2032 period

The Europe visual analytics market is projected to experience steady growth throughout the forecast period, with the market size reaching 1.40 billion by 2026 and expanding to 2.82 billion by 2033. This represents a compound annual growth rate of 10.54% from 2027 to 2033, indicating robust market momentum. The forecast period will be characterized by increasing adoption across all vertical segments, with particular strength in retail and consumer goods, BFSI, and healthcare sectors. Cloud-based deployment models are expected to show faster growth rates compared to on-premises solutions, reflecting the broader shift toward cloud computing across European enterprises. The forecast also suggests that business functions such as sales and marketing, operations, and supply chain management will be the primary drivers of visual analytics adoption.

Europe Visual Analytics Market Size and Share by Segmentation - Breakdown by {segmentData}

The Europe visual analytics market demonstrates distinct patterns across various segmentation dimensions. By vertical, the retail and consumer goods sector currently represents the largest market share, driven by the need for customer analytics and supply chain optimization. The BFSI sector follows closely, utilizing visual analytics for risk management, fraud detection, and customer insights. By deployment model, cloud-based solutions are gaining market share rapidly due to their scalability and lower upfront costs, though on-premises deployments maintain significant presence in industries with strict data governance requirements. Among business functions, sales and marketing applications command the largest share, followed by operations and supply chain management, reflecting the immediate impact of visual analytics on revenue generation and operational efficiency.

Global Europe Visual Analytics Market Size and Share by Region - Geographic distribution

The Europe visual analytics market exhibits varying adoption rates and growth patterns across different regions within the continent. Western European countries including Germany, France, the United Kingdom, and the Nordic nations represent the largest market share, driven by their advanced digital infrastructure, higher technology adoption rates, and concentration of enterprise organizations. Southern European markets including Spain, Italy, and Portugal are showing increasing adoption as digital transformation initiatives gain momentum. Eastern European countries are emerging as promising growth markets, with improving IT infrastructure and growing awareness of visual analytics benefits. The regional distribution reflects broader economic development patterns, with mature markets leading in adoption while emerging markets present significant growth opportunities.

Regional Analysis of the Europe Visual Analytics Market - Detailed regional market performance

Regional dynamics within the Europe visual analytics market reveal distinct adoption patterns and growth trajectories. The DACH region (Germany, Austria, Switzerland) leads in market maturity, with enterprises in manufacturing, automotive, and financial services driving substantial demand for sophisticated analytics solutions. The UK and Ireland market is characterized by strong cloud adoption and a vibrant fintech sector that leverages visual analytics extensively. Nordic countries demonstrate high digital maturity with particular emphasis on sustainability analytics and smart city initiatives. Southern European markets are experiencing accelerated growth as governments and enterprises invest in digital transformation, while Eastern European regions offer emerging opportunities with growing IT services sectors and increasing foreign direct investment in technology.

Leading Company Profiles in the Europe Visual Analytics Market - Industry players and strategies

The Europe visual analytics market features several prominent players employing diverse strategies to capture market share. Microsoft leverages its extensive enterprise ecosystem and Azure cloud platform to deliver integrated analytics solutions that appeal to organizations seeking unified technology environments. IBM focuses on enterprise-grade solutions with strong AI integration, targeting large organizations with complex analytics requirements. SAP emphasizes its strength in enterprise resource planning integration, offering visual analytics capabilities that complement its broader business software suite. Specialized vendors like Tableau and Qlik differentiate through user-friendly interfaces and innovative visualization capabilities, while Alteryx focuses on data preparation and advanced analytics workflows. These companies are increasingly pursuing partnerships, acquisitions, and product innovations to strengthen their market positions.

Porter's Five Forces Analysis of the Europe Visual Analytics Market - Competitive forces assessment

Porter's Five Forces analysis reveals a competitive landscape with moderate to high intensity across most forces. The threat of new entrants remains moderate due to high development costs and the need for substantial R&D investment, though cloud computing has lowered some barriers to entry. Bargaining power of buyers is increasing as organizations become more sophisticated in their analytics requirements and have multiple vendor options. Suppliers of complementary technologies and services hold moderate power, particularly those providing data sources and integration capabilities. The threat of substitutes exists from traditional BI tools and custom analytics solutions, though visual analytics' unique capabilities provide differentiation. Competitive rivalry is intense, with numerous global and regional players competing on features, pricing, and integration capabilities.

SWOT Analysis of the Europe Visual Analytics Market - Strengths, weaknesses, opportunities, threats

The Europe visual analytics market demonstrates significant strengths including strong technological infrastructure, high digital maturity among enterprises, and increasing recognition of data-driven decision-making value. However, weaknesses such as data privacy concerns under GDPR, skills shortages, and integration complexities with legacy systems present challenges. Opportunities abound in emerging technologies like AI and IoT integration, expansion into SMEs, and growing demand for real-time analytics across industries. Threats include intense competition, rapid technological changes requiring continuous innovation, and potential economic uncertainties affecting enterprise IT spending. The market's overall trajectory remains positive, with strengths and opportunities outweighing weaknesses and threats, particularly for vendors who can address key customer concerns while delivering innovative solutions.

Europe Visual Analytics Market Value Chain Analysis - Industry structure and value flow

The Europe visual analytics value chain encompasses multiple interconnected components that deliver value to end-users. At the foundation, data providers and integration specialists enable access to diverse data sources across organizations. Platform developers create the core visual analytics software with varying capabilities around visualization, dashboarding, and advanced analytics. Implementation partners and system integrators assist organizations in deploying and customizing solutions to meet specific business requirements. Training and support services ensure successful adoption and ongoing optimization of visual analytics capabilities. Value flows through this chain as organizations transform raw data into actionable insights, with each participant contributing specialized capabilities that collectively enable effective data visualization and analysis.

Key Investment Insights in the Europe Visual Analytics Market - Strategic investment recommendations

Strategic investment opportunities in the Europe visual analytics market center on several key areas. Cloud-based visual analytics platforms represent a particularly attractive investment segment, given the accelerating shift toward cloud computing across European enterprises. AI and machine learning integration capabilities offer significant differentiation potential as organizations seek more sophisticated analytical capabilities. Investments in user experience and interface design can yield competitive advantages, particularly as the market expands to include non-technical business users. Additionally, vertical-specific solutions that address unique industry requirements in sectors like healthcare, manufacturing, and retail present compelling investment opportunities. Companies that can navigate data privacy regulations while delivering innovative, user-friendly solutions are well-positioned for growth in this expanding market.

Europe Visual Analytics Market Conclusion - Summary and key takeaways

The Europe visual analytics market stands at a pivotal juncture, characterized by robust growth projections, technological innovation, and expanding adoption across industries. With the market expected to nearly double in size from 1.40 billion in 2026 to 2.82 billion by 2033, the growth trajectory remains strong despite challenges related to data privacy and implementation complexities. Success in this market requires vendors to balance innovation with usability, address industry-specific requirements, and navigate the complex regulatory environment. As organizations across Europe continue to recognize the strategic value of data-driven decision-making, visual analytics will remain a critical technology for competitive advantage, operational efficiency, and business transformation.

Research Methodology - How this research was conducted

This market research was conducted through a comprehensive methodology combining primary and secondary research approaches. Primary research included interviews with industry experts, technology vendors, and end-users across various European regions and industry verticals. Secondary research encompassed analysis of company financial reports, industry publications, market databases, and regulatory documents. The research methodology employed both top-down and bottom-up approaches to validate market size estimates and growth projections. Data triangulation techniques were used to ensure accuracy and reliability of findings. The research scope covered major European markets while acknowledging regional variations in adoption rates and market maturity.

Research Scope - Coverage and limitations

This research focuses specifically on the Europe visual analytics market, covering major Western, Southern, and Eastern European regions. The scope encompasses software solutions, platforms, and related services that enable data visualization and analysis. Market sizing and forecasting cover the period from 2026 to 2033, with historical context provided where relevant. The research includes analysis of key market segments, competitive landscape, and regional variations. Limitations include the exclusion of adjacent markets such as traditional business intelligence and the focus on commercial rather than academic or research applications. The research also acknowledges that rapid technological changes may impact market dynamics beyond the forecast period.

Key Companies and Recent Developments in the Europe Visual Analytics Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Leading companies in the Europe visual analytics market have been actively pursuing strategic initiatives to strengthen their market positions. Microsoft has expanded its Power BI platform with enhanced AI capabilities and deeper integration with Azure services, targeting enterprise customers seeking unified cloud solutions. IBM has focused on Watson Analytics enhancements, emphasizing cognitive computing capabilities for complex data analysis. SAP has strengthened its analytics portfolio through acquisitions and product enhancements, particularly in its SAP Analytics Cloud offering. Tableau continues to innovate with new visualization capabilities and mobile-first approaches, while Qlik has expanded its associative analytics engine to handle larger and more complex data sets. These companies, along with other market participants, are increasingly forming strategic partnerships with cloud providers, data integration specialists, and industry-specific solution providers to expand their market reach and capabilities.