What is the Food Inclusions Market Overview?

The Food Inclusions Market represents a dynamic segment of the food industry focused on ingredients added to food products to enhance texture, flavor, visual appeal, and nutritional value. These inclusions encompass a wide range of products including chocolates, fruit and nuts, flavored sugars, caramels, and various other ingredients that manufacturers incorporate into dairy products, frozen desserts, bakery items, breakfast cereals, and confectionery products. The market plays a crucial role in product differentiation and consumer appeal, as food inclusions allow manufacturers to create premium, innovative products that stand out in competitive retail environments. With increasing consumer demand for indulgent yet convenient food options, the food inclusions market has become integral to product development strategies across multiple food categories.

What are the key drivers, restraints, challenges, and opportunities in the Food Inclusions Market?

The Food Inclusions Market is driven by several key factors including growing consumer demand for premium and indulgent food experiences, increasing innovation in product development, and the rising popularity of customized and artisanal food products. The trend toward clean label and natural ingredients has also created opportunities for manufacturers to develop healthier inclusion options. However, the market faces restraints such as fluctuating raw material prices, particularly for commodities like cocoa and nuts, and stringent food safety regulations that increase compliance costs. Challenges include maintaining product stability during processing and storage, as well as meeting diverse consumer preferences across different regions. Opportunities exist in developing plant-based and functional inclusions, expanding into emerging markets, and creating sustainable sourcing solutions to address environmental concerns.

What are the current growth trends shaping the Food Inclusions Market?

The Food Inclusions Market is experiencing several significant growth trends that are reshaping the industry landscape. Plant-based and vegan inclusions are gaining substantial traction as consumers increasingly seek alternative protein sources and dairy-free options. There is also a strong trend toward clean label products, with manufacturers focusing on natural, minimally processed inclusions that appeal to health-conscious consumers. Customization and personalization are becoming increasingly important, with brands offering unique flavor combinations and textures to differentiate their products. The market is also seeing growth in functional inclusions that provide added health benefits, such as protein-fortified pieces or inclusions with added vitamins and minerals. Additionally, there is a rising demand for premium and artisanal inclusions that offer sophisticated flavor profiles and unique textures, catering to consumers seeking gourmet experiences in everyday products.

How did COVID-19 impact the Food Inclusions Market?

The COVID-19 pandemic had a mixed impact on the Food Inclusions Market, initially causing disruptions in supply chains and manufacturing operations due to lockdowns and restrictions. The closure of foodservice channels, including restaurants, cafes, and bakeries, significantly affected demand for certain types of inclusions. However, the market demonstrated resilience as consumer behavior shifted toward at-home consumption, driving increased demand for retail-packaged products containing inclusions. The pandemic accelerated trends toward comfort foods and indulgent treats, benefiting categories like chocolate and confectionery inclusions. Manufacturers had to adapt quickly to changing consumer preferences, with increased focus on shelf-stable products and e-commerce channels. As the market recovers, there is renewed emphasis on supply chain resilience, local sourcing, and products that offer both indulgence and functional benefits to address evolving consumer needs in the post-pandemic landscape.

What is the competitive landscape of the Food Inclusions Market?

The Food Inclusions Market features a competitive landscape characterized by the presence of both global food ingredient giants and specialized inclusion manufacturers. Major players such as ADM, Cargill, Barry Callebaut, and Kerry Group dominate the market with their extensive product portfolios, global distribution networks, and significant R&D capabilities. These companies compete on factors such as product innovation, quality, pricing, and customer service. The market also includes regional players like AGRANA BETEILIGUNGS-AG and Georgia Nut Company, who focus on specific geographic markets or product niches. Competition is intensifying as companies invest in new product development, strategic partnerships, and acquisitions to expand their market presence. The landscape is also shaped by increasing consolidation, with larger companies acquiring smaller, innovative firms to enhance their product offerings and technological capabilities in the inclusions space.

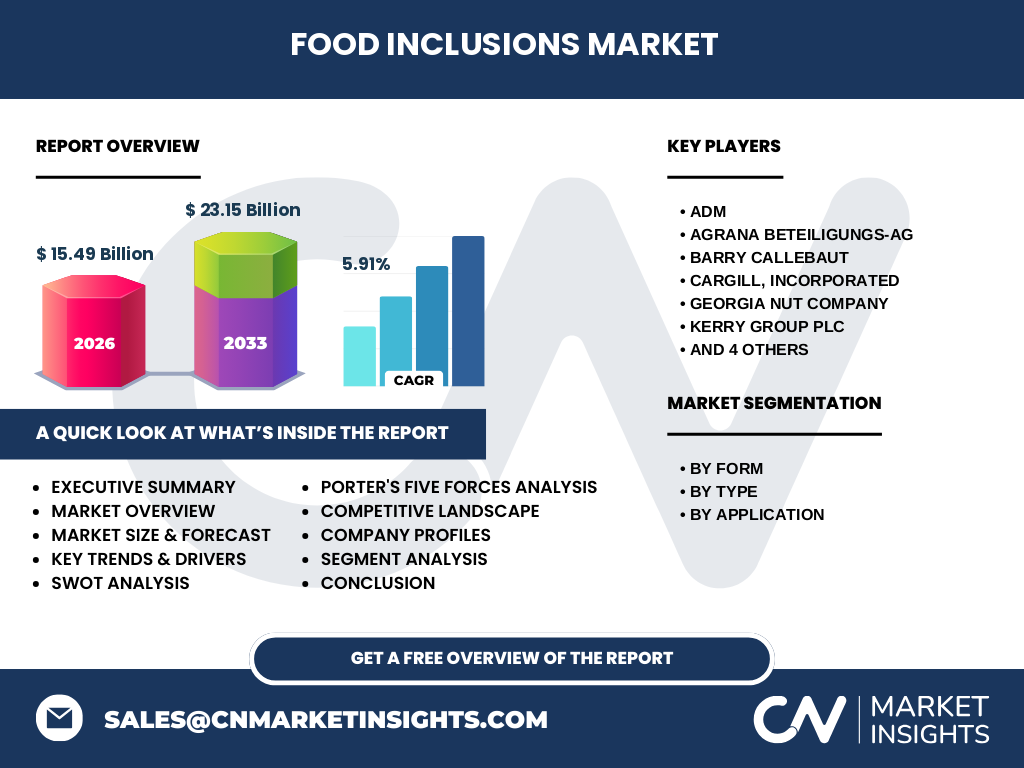

What are the key findings in the Executive Summary of the Food Inclusions Market?

The Food Inclusions Market is positioned for steady growth, with the market size projected to reach $15.49 billion by 2026, expanding to $23.15 billion by 2033, representing a compound annual growth rate of 5.91%. This growth is driven by increasing consumer demand for premium and innovative food products across multiple applications, including dairy and frozen desserts, bakery products, breakfast cereals, and chocolate and confectionery items. The market is characterized by diverse product segments, with chocolates, fruit and nuts, and flavored sugars and caramels being the primary types of inclusions. Solid and semi-solid forms dominate the market, catering to different application requirements. Key players such as ADM, Barry Callebaut, and Kerry Group are leading the market through continuous innovation and strategic expansion. The market faces challenges related to raw material price volatility and regulatory compliance, but opportunities in plant-based and functional inclusions present significant growth potential for forward-thinking manufacturers.

What are the market forecasts for the Food Inclusions Market from 2025 to 2032?

The Food Inclusions Market is projected to experience robust growth during the forecast period of 2025 to 2032, building on the established trajectory from 2026's $15.49 billion valuation. The market is expected to reach approximately $23.15 billion by 2033, representing a compound annual growth rate of 5.91%. This growth will be driven by sustained consumer demand for innovative and premium food products, particularly in emerging markets where disposable incomes are rising and Western food consumption patterns are gaining popularity. The forecast period will likely see continued expansion in plant-based and functional inclusions, as health and wellness trends remain prominent. Technological advancements in processing and formulation will enable the development of new inclusion types with enhanced functionality and stability. The market will also benefit from increasing applications in non-traditional categories such as plant-based dairy alternatives and functional beverages, creating new revenue streams for inclusion manufacturers.

What is the market size and share by segmentation in the Food Inclusions Market?

The Food Inclusions Market exhibits distinct segmentation patterns across form, type, and application categories. In terms of form, solid inclusions dominate the market due to their versatility and widespread use in various applications, while semi-solid inclusions are gaining traction in premium and artisanal product segments. By type, chocolates represent a significant share of the market, driven by their popularity in confectionery and bakery applications. Fruit and nuts constitute another major segment, appealing to health-conscious consumers seeking natural and nutritious options. Flavored sugars and caramels form a substantial portion of the market, particularly in dessert and confectionery applications. Regarding applications, dairy and frozen desserts represent a major market segment, benefiting from the inclusion trend in ice creams and yogurt products. Bakery products, breakfast cereals, and chocolate and confectionery products also command significant market shares, each with unique inclusion requirements and growth dynamics.

What is the global market size and share by region in the Food Inclusions Market?

The global Food Inclusions Market demonstrates varying regional dynamics, with developed regions like North America and Europe currently holding significant market shares due to established food processing industries and high consumer spending on premium products. North America, in particular, shows strong demand for innovative inclusions in bakery and confectionery applications, while Europe leads in premium and artisanal inclusion segments. The Asia-Pacific region is emerging as a high-growth market, driven by rapid urbanization, changing dietary preferences, and increasing disposable incomes in countries like China and India. Latin America shows promising growth potential, particularly in chocolate and fruit-based inclusions, leveraging the region's abundant natural resources. The Middle East and Africa region, while currently smaller in market size, presents opportunities for growth in bakery and dessert applications as Western food culture gains popularity. Regional differences in consumer preferences, regulatory environments, and economic conditions create diverse market dynamics across geographic areas.

What is the regional analysis of the Food Inclusions Market?

The regional analysis of the Food Inclusions Market reveals distinct patterns and growth drivers across different geographic areas. North America represents a mature market with strong demand for innovative and premium inclusions, particularly in the bakery and confectionery sectors. The region benefits from advanced food processing technologies and a culture of product experimentation. Europe shows similar maturity but with a stronger emphasis on artisanal and clean label inclusions, driven by consumer preference for natural and traditional ingredients. The Asia-Pacific region demonstrates the highest growth potential, with rapid expansion in countries like China, India, and Southeast Asian nations where Western-style bakery and dessert products are gaining popularity. Latin America leverages its rich agricultural resources, particularly in fruit and nut inclusions, while also showing growing demand for chocolate-based inclusions. The Middle East and Africa region presents emerging opportunities, particularly in the premium and indulgent segments, as urbanization and changing lifestyles drive demand for Western-style baked goods and desserts.

Who are the leading companies in the Food Inclusions Market and what are their strategies?

The Food Inclusions Market is led by several prominent companies that have established strong market positions through diverse strategies. ADM leverages its global presence and extensive product portfolio to serve multiple industries, focusing on innovation and sustainability in its inclusion offerings. AGRANA BETEILIGUNGS-AG specializes in fruit-based inclusions, capitalizing on its expertise in fruit processing and natural ingredients. Barry Callebaut, a global leader in chocolate manufacturing, dominates the chocolate inclusion segment through its premium quality products and innovative solutions for the confectionery and bakery industries. Cargill, Incorporated utilizes its vast agricultural supply chain to provide diverse inclusion options, with a focus on sustainable sourcing and clean label products. Georgia Nut Company specializes in nut-based inclusions, serving the bakery and confectionery markets with high-quality products. Kerry Group PLC emphasizes functional and nutritional inclusions, aligning with health and wellness trends. Meadow Foods focuses on dairy-based inclusions, leveraging its expertise in dairy ingredients. Puratos offers a wide range of inclusion solutions for the bakery sector, while Sensient Technologies provides color and flavor inclusions across multiple applications. Taura Natural Ingredients LTD specializes in fruit-based inclusions, focusing on natural and clean label products.

What is the Porter's Five Forces Analysis of the Food Inclusions Market?

The Porter's Five Forces Analysis of the Food Inclusions Market reveals a moderately competitive industry structure. The threat of new entrants is moderate, as establishing production facilities and distribution networks requires significant capital investment and technical expertise. However, niche players can enter the market with innovative products or specialized offerings. The bargaining power of buyers is relatively high, particularly for large food manufacturers who can negotiate prices and demand customized solutions. The bargaining power of suppliers varies depending on the raw material; for instance, suppliers of specialty ingredients like exotic fruits or premium chocolate may have higher bargaining power. The threat of substitutes is moderate, as alternative ingredients or technologies could potentially replace traditional inclusions in some applications. Competitive rivalry is intense, with numerous global and regional players competing on product quality, innovation, pricing, and customer service. The market is characterized by ongoing consolidation as larger companies acquire smaller, innovative firms to enhance their product portfolios and market presence.

What is the SWOT Analysis of the Food Inclusions Market?

The SWOT Analysis of the Food Inclusions Market reveals several key factors influencing the industry. Strengths include the diverse range of inclusion types available, strong demand across multiple food categories, and the ability of inclusions to add value and differentiation to products. The market benefits from established distribution networks and the presence of major global players with significant R&D capabilities. Weaknesses include vulnerability to raw material price fluctuations, particularly for commodities like cocoa and nuts, and the challenges of maintaining product stability during processing and storage. The market also faces regulatory compliance costs and the need for continuous innovation to meet changing consumer preferences. Opportunities exist in developing plant-based and functional inclusions, expanding into emerging markets, and creating sustainable sourcing solutions. The growing trend toward clean label and natural ingredients presents opportunities for manufacturers to develop healthier inclusion options. Threats include increasing competition, particularly from regional players and new entrants, and potential disruptions in supply chains due to geopolitical or environmental factors. Changing consumer preferences and regulatory requirements also pose ongoing challenges for market participants.

What is the value chain analysis of the Food Inclusions Market?

The value chain analysis of the Food Inclusions Market reveals a complex network of activities from raw material sourcing to end-product delivery. The chain begins with raw material suppliers who provide essential ingredients such as cocoa, fruits, nuts, sugars, and other base materials. These suppliers range from large agricultural commodity producers to specialized growers of exotic ingredients. Food ingredient manufacturers then process these raw materials into various inclusion forms, including chocolate chips, fruit pieces, nut clusters, and flavored sugar inclusions. This processing stage involves significant investment in technology and quality control to ensure product consistency and safety. Distribution partners, including wholesalers and specialty ingredient distributors, play a crucial role in delivering inclusions to food manufacturers. Food manufacturers, such as bakery companies, dairy producers, and confectionery manufacturers, incorporate these inclusions into their products, adding value through formulation and branding. Finally, retailers and foodservice operators sell the finished products to consumers. Supporting activities throughout the value chain include research and development for new inclusion types, marketing and sales efforts, and regulatory compliance to ensure food safety and quality standards are met.

What are the key investment insights in the Food Inclusions Market?

The Food Inclusions Market presents several compelling investment opportunities for stakeholders looking to capitalize on industry growth. Investment in research and development is crucial, particularly in developing innovative inclusion types that address emerging consumer trends such as plant-based, functional, and clean label products. Companies that can create inclusions with enhanced nutritional profiles, extended shelf life, or unique textures and flavors are likely to gain competitive advantages. Strategic acquisitions of smaller, specialized inclusion manufacturers can provide quick access to new technologies, product lines, and market segments. Investment in sustainable sourcing and production methods is increasingly important, as consumers and regulatory bodies demand greater transparency and environmental responsibility in the food supply chain. Expanding production capacity in high-growth regions, particularly in Asia-Pacific and Latin America, offers opportunities to capture emerging market demand. Additionally, investment in digital technologies for supply chain optimization, quality control, and customer engagement can improve operational efficiency and market responsiveness. Partnerships with food manufacturers to co-develop customized inclusion solutions can also create value-added revenue streams and strengthen market positions.

What are the key takeaways from the Food Inclusions Market conclusion?

The Food Inclusions Market represents a dynamic and growing segment of the food industry, characterized by innovation, diverse product offerings, and strong demand across multiple applications. The market's projected growth from $15.49 billion in 2026 to $23.15 billion by 2033, at a CAGR of 5.91%, underscores its significant potential for continued expansion. Key drivers of this growth include consumer demand for premium and innovative food products, the trend toward clean label and natural ingredients, and the increasing popularity of plant-based and functional inclusions. While the market faces challenges such as raw material price volatility and regulatory compliance, opportunities in emerging markets and product innovation present substantial growth potential. The competitive landscape is shaped by major global players and specialized regional manufacturers, with ongoing consolidation and strategic partnerships defining industry dynamics. Success in this market will depend on companies' ability to innovate, adapt to changing consumer preferences, and develop sustainable and value-added inclusion solutions that meet the evolving needs of food manufacturers and consumers alike.

What is the research methodology used for this Food Inclusions Market analysis?

The research methodology for this Food Inclusions Market analysis employed a comprehensive and multi-faceted approach to ensure accurate and reliable findings. Primary research formed a significant component, involving interviews with industry experts, food manufacturers, and key opinion leaders to gather firsthand insights on market trends, challenges, and opportunities. These interviews provided valuable qualitative data on market dynamics and future projections. Secondary research was conducted using a wide range of sources, including company annual reports, industry publications, trade journals, and government databases to validate and supplement primary findings. Market size and share calculations were derived using both top-down and bottom-up approaches, ensuring triangulation of data from multiple sources. Historical data analysis was performed to identify growth patterns and market trends, while current market conditions were assessed through recent financial reports and industry news. The research also incorporated data from industry associations and regulatory bodies to understand the impact of policies and standards on market development. This comprehensive methodology ensures a robust and well-rounded analysis of the Food Inclusions Market.

What is the research scope of this Food Inclusions Market study?

The research scope of this Food Inclusions Market study encompasses a comprehensive analysis of the global market, covering key aspects from 2026 to 2033. The study focuses on market size, growth trends, competitive landscape, and regional dynamics across major geographic areas including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The research examines market segmentation by form (solid and semi-solid), type (chocolates, fruit and nuts, flavored sugars and caramels), and application (dairy and frozen desserts, bakery products, breakfast cereals, chocolate and confectionery products). The study includes detailed profiles of leading companies such as ADM, AGRANA BETEILIGUNGS-AG, Barry Callebaut, Cargill, Georgia Nut Company, Kerry Group, Meadow Foods, Puratos, Sensient Technologies, and Taura Natural Ingredients LTD. The research scope also covers market drivers, restraints, challenges, and opportunities, along with strategic analyses including Porter's Five Forces and SWOT analysis. The study provides market forecasts, investment insights, and a comprehensive value chain analysis to offer stakeholders a complete understanding of the Food Inclusions Market landscape.

Who are the key companies in the Food Inclusions Market and what are their recent developments?

The Food Inclusions Market features several key companies that are driving innovation and shaping industry trends through their recent developments. ADM has been focusing on expanding its clean label and plant-based inclusion offerings, investing in sustainable sourcing initiatives and new product development to meet evolving consumer demands. AGRANA BETEILIGUNGS-AG has strengthened its position in fruit-based inclusions, launching new product lines with enhanced functionality and natural ingredients to cater to health-conscious consumers. Barry Callebaut has made significant strides in sustainable cocoa sourcing and has introduced innovative chocolate inclusions with improved nutritional profiles and unique flavor combinations. Cargill, Incorporated has expanded its portfolio of functional inclusions, particularly in the protein-enriched segment, and has made strategic acquisitions to enhance its market presence in emerging regions. Georgia Nut Company has focused on developing premium nut-based inclusions with clean label positioning, responding to the growing demand for natural and minimally processed ingredients. Kerry Group PLC has launched several new functional inclusion products targeting the health and wellness segment, including inclusions with added probiotics and plant-based proteins. Meadow Foods has introduced innovative dairy-based inclusions with extended shelf life and improved texture stability. Puratos has expanded its range of clean label inclusions for the bakery sector, focusing on natural ingredients and traditional processing methods. Sensient Technologies has developed new color and flavor inclusions using natural sources, addressing the trend toward clean label products. Taura Natural Ingredients LTD has launched new fruit-based inclusions with enhanced nutritional benefits and improved processing characteristics for various applications.