Parenteral Nutrition Market Overview - Definition, scope, and significance

Parenteral nutrition (PN) refers to the intravenous administration of nutrients directly into the bloodstream when a patient's gastrointestinal tract cannot be used for digestion and absorption. This specialized medical therapy provides essential nutrients including carbohydrates, proteins, fats, vitamins, and minerals to patients who cannot obtain adequate nutrition through oral or enteral routes. The market encompasses various components such as single-dose amino acid solutions, parenteral lipid emulsions, carbohydrates, trace elements, vitamins, and minerals, along with delivery systems and administration devices. The significance of this market lies in its critical role in supporting patients with severe medical conditions, including short bowel syndrome, severe pancreatitis, cancer, Crohn's disease, and other gastrointestinal disorders that impair nutrient absorption. As medical technology advances and the prevalence of chronic diseases increases globally, the parenteral nutrition market continues to evolve as a vital component of modern healthcare delivery systems.

Parenteral Nutrition Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The parenteral nutrition market is driven by several key factors including the rising prevalence of chronic diseases, increasing geriatric population, growing number of premature births, and advancements in medical technology. The increasing incidence of gastrointestinal disorders, cancer, and metabolic diseases that require specialized nutritional support significantly contributes to market growth. Additionally, the expansion of home healthcare services and improved reimbursement policies in developed countries create favorable conditions for market expansion. However, the market faces restraints such as the risk of complications associated with parenteral nutrition therapy, including infections, metabolic imbalances, and liver dysfunction. The high cost of treatment and the need for specialized healthcare infrastructure also pose challenges to market growth. Despite these obstacles, opportunities exist in emerging markets, technological innovations in delivery systems, and the development of more efficient and safer nutritional formulations. The growing trend toward personalized medicine and the increasing focus on patient-specific nutritional requirements present significant opportunities for market players to develop innovative solutions.

Parenteral Nutrition Market Growth Trends - Current and emerging trends shaping the market

The parenteral nutrition market is experiencing several notable growth trends that are reshaping the industry landscape. One significant trend is the increasing adoption of three-in-one (3-in-1) parenteral nutrition solutions, which combine amino acids, glucose, and lipids in a single bag, offering convenience and reducing the risk of contamination. Another emerging trend is the growing preference for ready-to-use parenteral nutrition products over compounded formulations, driven by concerns about sterility and consistency. The market is also witnessing a shift toward lipid emulsions with improved safety profiles, such as those based on olive oil or fish oil, which offer better metabolic outcomes. Technological advancements in delivery systems, including smart pumps and monitoring devices, are enhancing the safety and efficacy of parenteral nutrition therapy. Additionally, there is a growing focus on developing specialized formulations for specific patient populations, such as premature infants and critically ill patients. The increasing emphasis on home parenteral nutrition and the development of user-friendly administration systems are further contributing to market growth and accessibility.

COVID-19 Impact on the Parenteral Nutrition Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the parenteral nutrition market, presenting both challenges and opportunities. During the initial phases of the pandemic, the market experienced disruptions in supply chains, manufacturing operations, and distribution networks due to lockdowns and travel restrictions. However, the increased demand for critical care services, including parenteral nutrition for severely ill COVID-19 patients, partially offset these challenges. The pandemic highlighted the importance of maintaining adequate nutritional support for patients with compromised gastrointestinal function, particularly those requiring mechanical ventilation. As healthcare systems adapted to the new normal, the market witnessed accelerated adoption of home parenteral nutrition services to reduce hospital stays and minimize infection risks. The recovery trajectory has been characterized by strengthened supply chain resilience, increased focus on product safety and quality, and accelerated digital transformation in healthcare delivery. Moving forward, the lessons learned during the pandemic are expected to drive long-term improvements in parenteral nutrition practices and market growth.

Parenteral Nutrition Market Competitive Landscape - Major competitors and market consolidation

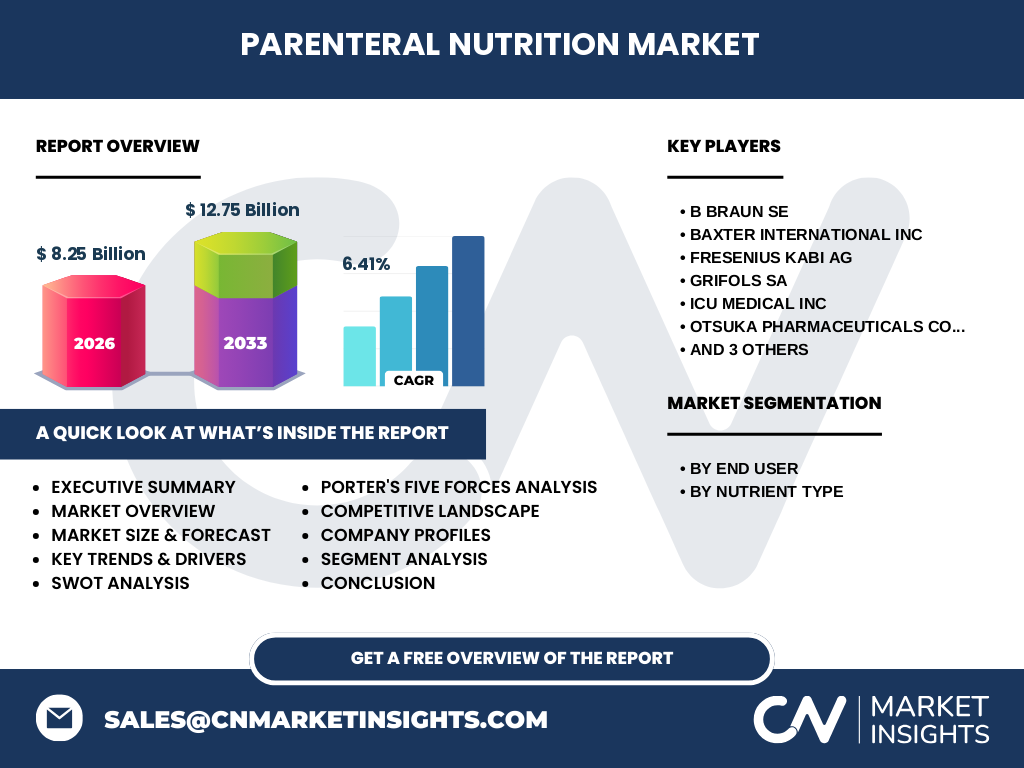

The parenteral nutrition market features a moderately consolidated competitive landscape with several key players dominating the global market. Major competitors include B. Braun SE, Baxter International Inc., Fresenius Kabi AG, Grifols S.A., ICU Medical Inc., Otsuka Pharmaceutical Co. Ltd., Pfizer Inc., Sichuan Kelun-Biotech Biopharmaceutical Co. Ltd., and Vifor Pharma Management AG. These companies compete based on product quality, innovation, pricing strategies, and distribution networks. The market has witnessed strategic initiatives such as mergers and acquisitions, partnerships, and collaborations aimed at expanding product portfolios and geographical presence. For instance, companies are focusing on developing advanced lipid emulsions and specialized nutritional formulations to gain competitive advantage. The competitive landscape is characterized by continuous research and development efforts to improve product safety, efficacy, and patient outcomes. Additionally, companies are investing in expanding their manufacturing capabilities and strengthening their presence in emerging markets to capitalize on growing demand for parenteral nutrition solutions.

Executive Summary - High-level overview and key findings about Parenteral Nutrition Market

The parenteral nutrition market represents a critical segment of the healthcare industry, providing essential nutritional support to patients who cannot obtain adequate nutrition through conventional means. With a market size of 8.25 billion in 2026 and projected to reach 12.75 billion by 2033, the market demonstrates robust growth potential with a CAGR of 6.41%. The market is segmented by end-user into hospitals and clinics, and by nutrient type into single-dose amino acid solutions, parenteral lipid emulsions, carbohydrates, trace elements, vitamins, and minerals. Key market drivers include the rising prevalence of chronic diseases, increasing geriatric population, and advancements in medical technology. The competitive landscape features major players such as B. Braun SE, Baxter International Inc., and Fresenius Kabi AG, who are focusing on product innovation and strategic partnerships. The market faces challenges related to complications associated with parenteral nutrition therapy and high treatment costs, but opportunities exist in emerging markets and technological advancements. The COVID-19 pandemic has highlighted the importance of parenteral nutrition in critical care, potentially accelerating market growth in the post-pandemic era.

Parenteral Nutrition Market Forecast - Projections for 2025-2032 period

The parenteral nutrition market is projected to experience steady growth during the forecast period of 2025-2032, with the market size expected to increase from 8.25 billion in 2026 to 12.75 billion by 2033, representing a compound annual growth rate (CAGR) of 6.41%. This growth trajectory is driven by several factors, including the increasing prevalence of chronic diseases, rising geriatric population, and growing demand for advanced nutritional therapies. The market is expected to witness significant expansion in emerging economies due to improving healthcare infrastructure and increasing healthcare expenditure. Technological advancements in parenteral nutrition formulations and delivery systems are anticipated to further fuel market growth. The hospital segment is likely to maintain its dominance as the primary end-user, while the clinics segment is expected to show substantial growth due to the increasing trend of outpatient care. Among nutrient types, single-dose amino acid solutions and parenteral lipid emulsions are projected to witness higher growth rates due to their critical role in patient recovery and improved formulations. The market is also expected to benefit from increasing awareness about the importance of adequate nutrition in patient care and the growing adoption of home parenteral nutrition services.

Parenteral Nutrition Market Size and Share by Segmentation - Breakdown by {segmentData}

The parenteral nutrition market is segmented by end-user and nutrient type, with each segment contributing differently to the overall market size and share. In terms of end-users, hospitals represent the largest segment, accounting for the majority of market share due to the high volume of patients requiring parenteral nutrition therapy and the availability of specialized healthcare infrastructure. Hospitals are followed by clinics, which are experiencing growing demand for parenteral nutrition services as outpatient care becomes more prevalent. Regarding nutrient types, single-dose amino acid solutions hold a significant market share as they are essential components of parenteral nutrition therapy. Parenteral lipid emulsions represent another substantial segment, with increasing preference for advanced formulations based on olive oil or fish oil. Carbohydrates, trace elements, vitamins, and minerals collectively form the remaining segments, each playing a crucial role in providing comprehensive nutritional support. The market share distribution among these segments is influenced by factors such as clinical requirements, regulatory approvals, and technological advancements in formulation development. As the market evolves, the relative importance of each segment may shift based on emerging clinical evidence and changing patient needs.

Global Parenteral Nutrition Market Size and Share by Region - Geographic distribution

While specific regional market share data is not provided, the global parenteral nutrition market exhibits varying growth patterns and market dynamics across different geographic regions. North America, particularly the United States, is expected to maintain a significant market share due to advanced healthcare infrastructure, high healthcare expenditure, and the presence of major market players. Europe is likely to follow closely, driven by well-established healthcare systems and increasing adoption of advanced nutritional therapies. The Asia-Pacific region is anticipated to witness the highest growth rate during the forecast period, attributed to improving healthcare infrastructure, rising awareness about parenteral nutrition, and increasing prevalence of chronic diseases in countries like China and India. Latin America and the Middle East & Africa regions are expected to show moderate growth, with opportunities arising from expanding healthcare access and growing medical tourism. The regional distribution of the parenteral nutrition market is influenced by factors such as healthcare policies, economic conditions, disease prevalence, and the availability of specialized healthcare services. As the market continues to evolve, regional variations in growth rates and market share are expected to reflect the diverse healthcare landscapes and economic conditions across different parts of the world.

Regional Analysis of the Parenteral Nutrition Market - Detailed regional market performance

The parenteral nutrition market demonstrates distinct regional characteristics and performance metrics across different geographical areas. In North America, the market benefits from advanced healthcare infrastructure, high healthcare expenditure, and a well-established regulatory framework. The presence of major market players and ongoing research and development activities contribute to the region's strong market position. Europe shows steady growth, supported by comprehensive healthcare systems and increasing adoption of advanced nutritional therapies. The region's focus on patient safety and quality of care drives demand for high-quality parenteral nutrition products. The Asia-Pacific region presents significant growth opportunities, with countries like China, Japan, and India experiencing rapid market expansion due to improving healthcare infrastructure, rising disposable incomes, and increasing awareness about specialized nutritional support. Latin America and the Middle East & Africa regions are gradually developing their parenteral nutrition markets, with growth driven by expanding healthcare access and increasing prevalence of chronic diseases. Regional variations in market performance are influenced by factors such as healthcare policies, economic conditions, disease burden, and the availability of specialized healthcare services. As the market evolves, regional dynamics are expected to shift based on local healthcare priorities and economic development.

Leading Company Profiles in the Parenteral Nutrition Market - Industry players and strategies

The parenteral nutrition market is characterized by the presence of several leading companies, each employing distinct strategies to maintain and expand their market positions. B. Braun SE, a prominent player in the market, focuses on product innovation and quality, offering a comprehensive range of parenteral nutrition solutions. Baxter International Inc. leverages its global presence and extensive distribution network to maintain a strong market position. Fresenius Kabi AG emphasizes research and development to introduce advanced formulations and delivery systems. Grifols S.A. specializes in plasma-derived products and has been expanding its portfolio to include parenteral nutrition solutions. ICU Medical Inc. focuses on developing innovative delivery systems and safety devices for parenteral nutrition administration. Otsuka Pharmaceutical Co. Ltd. invests in developing specialized formulations for specific patient populations. Pfizer Inc. utilizes its extensive research capabilities and global reach to maintain a competitive edge. Sichuan Kelun-Biotech Biopharmaceutical Co. Ltd. is expanding its presence in the Asian market with a focus on cost-effective solutions. Vifor Pharma Management AG specializes in developing iron-based products and has been expanding into the parenteral nutrition segment. These companies employ various strategies such as mergers and acquisitions, partnerships, and product launches to strengthen their market positions and expand their geographical presence.

Porter's Five Forces Analysis of the Parenteral Nutrition Market - Competitive forces assessment

The parenteral nutrition market is influenced by several competitive forces as analyzed through Porter's Five Forces framework. The threat of new entrants is moderate due to the high capital requirements for manufacturing facilities, stringent regulatory approvals, and the need for extensive distribution networks. However, the growing demand for parenteral nutrition solutions may attract new players, particularly in emerging markets. The bargaining power of buyers, including hospitals and clinics, is relatively high due to the availability of multiple suppliers and the critical nature of parenteral nutrition products. Buyers can negotiate on price and quality, putting pressure on manufacturers to maintain competitive pricing while ensuring product excellence. The bargaining power of suppliers is moderate, as the market relies on specialized raw materials and components. Suppliers of key ingredients such as amino acids and lipids may have some leverage, but the presence of multiple suppliers helps balance this power. The threat of substitute products is low, as parenteral nutrition is often the only viable option for patients who cannot receive nutrition through the gastrointestinal tract. The intensity of competitive rivalry is high among existing players, driven by the presence of several major companies competing on product quality, innovation, pricing, and distribution. This intense competition encourages continuous improvement and innovation in product offerings and services.

SWOT Analysis of the Parenteral Nutrition Market - Strengths, weaknesses, opportunities, threats

The parenteral nutrition market exhibits several strengths, weaknesses, opportunities, and threats that shape its overall dynamics. Among the strengths, the market benefits from the critical nature of its products, ensuring consistent demand regardless of economic conditions. The presence of established players with strong R&D capabilities and extensive distribution networks further strengthens the market's position. Additionally, the increasing awareness about the importance of adequate nutrition in patient care supports market growth. However, the market faces weaknesses such as the high cost of treatment, which can limit accessibility in some regions. The risk of complications associated with parenteral nutrition therapy and the need for specialized healthcare infrastructure also pose challenges. Opportunities in the market include the growing demand in emerging economies, technological advancements in formulations and delivery systems, and the increasing trend toward home parenteral nutrition. The market also has the potential to benefit from personalized nutrition approaches and the development of specialized formulations for specific patient populations. Threats to the market include stringent regulatory requirements, potential supply chain disruptions, and the risk of product recalls due to quality issues. Additionally, the market faces competition from alternative nutritional support methods and the potential for economic downturns to impact healthcare spending.

Parenteral Nutrition Market Value Chain Analysis - Industry structure and value flow

The parenteral nutrition market value chain encompasses several key stages, from raw material sourcing to end-user delivery. The chain begins with the procurement of high-quality raw materials, including amino acids, lipids, carbohydrates, vitamins, and minerals from specialized suppliers. These materials undergo rigorous quality control and testing to ensure compliance with regulatory standards. The manufacturing stage involves the formulation and production of parenteral nutrition solutions, requiring specialized facilities and expertise to maintain sterility and product integrity. Following manufacturing, the products enter the distribution phase, where they are transported through various channels, including direct sales to hospitals and clinics, as well as distribution through medical supply companies. The end-users, primarily hospitals and clinics, administer these products to patients under the supervision of healthcare professionals. Throughout this value chain, quality control and regulatory compliance play crucial roles in ensuring product safety and efficacy. Value is added at each stage through technological innovations, improved formulations, and enhanced distribution efficiency. The market also includes support services such as clinical nutrition consultation and patient education, which contribute to the overall value proposition. As the market evolves, there is a growing emphasis on streamlining the value chain to improve efficiency, reduce costs, and enhance patient outcomes.

Key Investment Insights in the Parenteral Nutrition Market - Strategic investment recommendations

The parenteral nutrition market presents several attractive investment opportunities for stakeholders looking to capitalize on the growing demand for specialized nutritional therapies. Strategic investments in research and development are crucial for developing innovative formulations and delivery systems that address unmet clinical needs and improve patient outcomes. Investors should consider opportunities in emerging markets, where improving healthcare infrastructure and increasing healthcare expenditure create favorable conditions for market expansion. The trend toward home parenteral nutrition services presents investment opportunities in developing user-friendly administration systems and support services. Additionally, investments in digital health technologies that enhance the safety and efficacy of parenteral nutrition therapy, such as smart pumps and monitoring devices, are likely to yield significant returns. Partnerships and collaborations between pharmaceutical companies, medical device manufacturers, and healthcare providers can create synergies and drive innovation in the market. Investors should also consider opportunities in expanding manufacturing capabilities to meet growing demand and ensure supply chain resilience. As the market continues to evolve, investments in personalized nutrition approaches and specialized formulations for specific patient populations are expected to offer promising returns. However, potential investors should carefully evaluate regulatory requirements, market dynamics, and competitive landscapes before making investment decisions.

Parenteral Nutrition Market Conclusion - Summary and key takeaways

The parenteral nutrition market represents a vital segment of the healthcare industry, providing essential nutritional support to patients who cannot obtain adequate nutrition through conventional means. With a market size of 8.25 billion in 2026 and projected to reach 12.75 billion by 2033, growing at a CAGR of 6.41%, the market demonstrates robust growth potential. Key drivers of this growth include the rising prevalence of chronic diseases, increasing geriatric population, and advancements in medical technology. The market is segmented by end-user into hospitals and clinics, and by nutrient type into single-dose amino acid solutions, parenteral lipid emulsions, carbohydrates, trace elements, vitamins, and minerals. Major players such as B. Braun SE, Baxter International Inc., and Fresenius Kabi AG dominate the competitive landscape, focusing on product innovation and strategic partnerships. While the market faces challenges related to treatment costs and potential complications, opportunities exist in emerging markets, technological advancements, and the growing trend toward home parenteral nutrition. The COVID-19 pandemic has highlighted the importance of parenteral nutrition in critical care, potentially accelerating market growth in the post-pandemic era. As the market continues to evolve, stakeholders must focus on innovation, quality, and accessibility to meet the growing demand for specialized nutritional therapies.

Research Methodology - How this research was conducted

The research methodology for this parenteral nutrition market analysis involved a comprehensive approach combining primary and secondary research techniques. Primary research included interviews with industry experts, healthcare professionals, and key opinion leaders to gather insights on market trends, challenges, and opportunities. These interviews provided valuable qualitative data on market dynamics, technological advancements, and regulatory landscapes. Secondary research involved an extensive review of industry reports, scientific publications, company annual reports, and regulatory databases to collect quantitative data on market size, growth rates, and competitive landscapes. Market sizing and forecasting were conducted using both top-down and bottom-up approaches, considering factors such as disease prevalence, healthcare expenditure, and technological adoption rates. Data triangulation techniques were employed to validate findings and ensure accuracy. The analysis also incorporated Porter's Five Forces framework and SWOT analysis to provide a comprehensive understanding of market dynamics and competitive forces. Regional analysis was conducted by examining country-specific healthcare policies, economic conditions, and market maturity levels. The research methodology was designed to provide a holistic view of the parenteral nutrition market, balancing quantitative data with qualitative insights to deliver actionable intelligence for stakeholders.

Research Scope - Coverage and limitations

The research scope for this parenteral nutrition market analysis encompasses a comprehensive examination of the global market, focusing on key segments, regional dynamics, and competitive landscapes. The study covers the period from 2025 to 2032, with historical data and future projections to provide a complete market perspective. The analysis includes detailed segmentation by end-user (hospitals and clinics) and nutrient type (single-dose amino acid solutions, parenteral lipid emulsions, carbohydrates, trace elements, vitamins, and minerals). Regional coverage extends to North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, providing insights into geographical variations in market performance and growth opportunities. The research also examines key industry players, their strategies, and recent developments to provide a comprehensive competitive landscape analysis. However, it is important to note certain limitations in the research scope. The study does not provide specific market share percentages for individual companies or regions, as this information was not available in the provided data. Additionally, the analysis does not delve into granular sub-segmentations within each nutrient type or end-user category. The research also does not cover detailed pricing analyses or specific reimbursement scenarios across different regions. Despite these limitations, the study aims to provide a thorough overview of the parenteral nutrition market, offering valuable insights for stakeholders and decision-makers in the healthcare industry.

Key Companies and Recent Developments in the Parenteral Nutrition Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The parenteral nutrition market features several key companies that are driving innovation and shaping the industry landscape through strategic developments and product launches. B. Braun SE has been focusing on expanding its portfolio of parenteral nutrition solutions, with recent announcements highlighting advancements in lipid emulsion formulations and smart delivery systems. The company has also strengthened its presence in emerging markets through strategic partnerships and acquisitions. Baxter International Inc. has made significant strides in developing ready-to-use parenteral nutrition products, with recent product launches emphasizing convenience and reduced contamination risks. The company has also announced collaborations with healthcare institutions to improve patient outcomes through optimized nutritional support. Fresenius Kabi AG has been at the forefront of developing specialized formulations for specific patient populations, with recent announcements focusing on lipid emulsions based on fish oil for improved metabolic outcomes. Grifols S.A. has expanded its parenteral nutrition offerings through strategic acquisitions, enhancing its position in the global market. ICU Medical Inc. has introduced innovative delivery systems and safety devices, with recent developments focusing on smart pumps with integrated monitoring capabilities. Otsuka Pharmaceutical Co. Ltd. has announced advancements in amino acid solutions, emphasizing personalized nutrition approaches. Pfizer Inc. has been strengthening its parenteral nutrition portfolio through strategic partnerships and research collaborations. Sichuan Kelun-Biotech Biopharmaceutical Co. Ltd. has announced plans for expanding its manufacturing capabilities to meet growing demand in the Asian market. Vifor Pharma Management AG has been focusing on developing iron-based products for parenteral nutrition, with recent announcements highlighting clinical trial results and product efficacy. These companies continue to drive market growth through ongoing research, product innovations, and strategic initiatives aimed at improving patient care and expanding market reach.