Rigid Foam Market Overview - Definition, scope, and significance

Rigid foam refers to a category of high-performance polymer materials characterized by their closed-cell structure and low density, providing exceptional thermal insulation, structural support, and lightweight properties. These materials are manufactured through chemical reactions that create a cellular matrix, resulting in products that offer superior insulation capabilities compared to traditional building materials. The rigid foam market encompasses various polymer types including polyurethane, polystyrene, polypropylene, polyethylene, and polyvinyl chloride foams, each serving distinct applications across multiple industries. The significance of this market lies in its critical role in energy conservation, building efficiency, and sustainable development, as rigid foams contribute substantially to reducing energy consumption in buildings and industrial applications while supporting lightweight design in automotive and aerospace sectors.

Rigid Foam Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The rigid foam market is driven by several key factors including increasing global demand for energy-efficient buildings, stringent government regulations on energy conservation, and growing awareness about sustainable construction practices. The construction industry's expansion, particularly in emerging economies, creates substantial demand for thermal insulation materials. Additionally, the automotive sector's focus on lightweight materials for fuel efficiency and electric vehicle development presents significant growth opportunities. However, the market faces restraints such as volatile raw material prices, particularly petroleum-based feedstocks, and environmental concerns regarding the production and disposal of certain foam types. Challenges include the development of eco-friendly alternatives, compliance with evolving environmental regulations, and competition from alternative insulation materials. Opportunities exist in the development of bio-based and recyclable foam materials, expansion into emerging markets, and technological advancements in foam manufacturing processes that enhance performance while reducing environmental impact.

Rigid Foam Market Growth Trends - Current and emerging trends shaping the market

Current growth trends in the rigid foam market include the increasing adoption of polyurethane foams due to their superior insulation properties and versatility across applications. The market is witnessing a shift toward environmentally friendly materials, with manufacturers developing foams with lower global warming potential (GWP) and improved recyclability. Smart foam technologies incorporating phase change materials and advanced thermal management systems are gaining traction, particularly in building and automotive applications. The integration of digital manufacturing technologies and automation in foam production is improving efficiency and product consistency. Emerging trends include the development of bio-based rigid foams derived from renewable resources, the use of nanotechnology to enhance foam properties, and the growing demand for customized foam solutions tailored to specific application requirements. The market is also experiencing increased focus on circular economy principles, driving innovations in foam recycling and end-of-life management.

COVID-19 Impact on the Rigid Foam Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly impacted the rigid foam market through supply chain disruptions, reduced construction activity, and temporary manufacturing shutdowns across key industries. The initial lockdowns and social distancing measures led to decreased demand from the construction and automotive sectors, which are major consumers of rigid foam products. However, the pandemic also accelerated certain trends, including increased focus on building energy efficiency and indoor air quality, driving demand for high-performance insulation materials. The recovery trajectory shows positive momentum as construction activities resume and economic activities normalize, with particular growth in residential construction and renovation projects. The market is benefiting from government stimulus packages focused on infrastructure development and green building initiatives. Additionally, the pandemic has heightened awareness about sustainable materials and energy efficiency, potentially accelerating long-term market growth as industries prioritize resilience and sustainability in their operations.

Rigid Foam Market Competitive Landscape - Major competitors and market consolidation

The rigid foam market features a mix of global chemical conglomerates and specialized foam manufacturers, with significant competition based on product innovation, technological capabilities, and global reach. Major players include BASF SE, Dow Chemical Corporation, and Covestro AG, which leverage their extensive research and development capabilities to maintain market leadership. Market consolidation is evident through strategic mergers, acquisitions, and partnerships aimed at expanding product portfolios and geographic presence. Companies are increasingly focusing on vertical integration to control supply chains and reduce costs. The competitive landscape is characterized by intense rivalry in product development, with manufacturers competing on performance characteristics, environmental compliance, and cost-effectiveness. Regional players maintain strong positions in local markets, while global companies compete for market share through technological innovation and strategic partnerships with end-use industries.

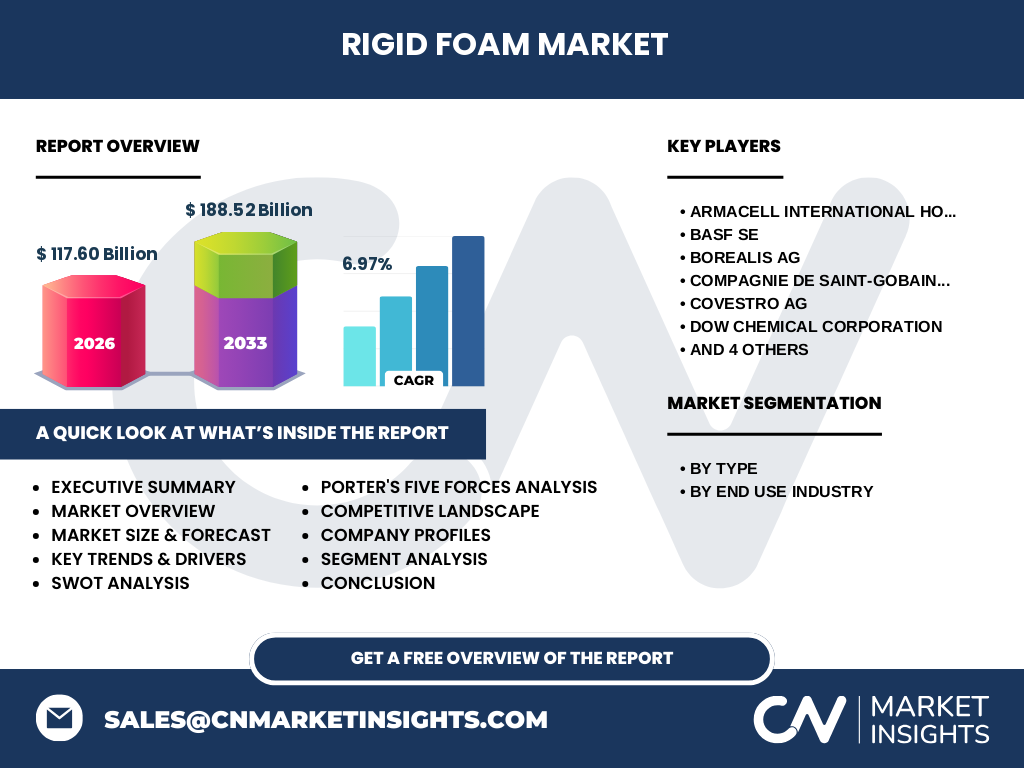

Executive Summary - High-level overview and key findings about Rigid Foam Market

The rigid foam market demonstrates robust growth potential driven by increasing demand for energy-efficient materials across construction, automotive, and industrial applications. With a projected market size of $117.60 billion by 2026 and a compound annual growth rate of 6.97%, the industry is positioned for substantial expansion through 2033. Polyurethane foams dominate the market due to their superior insulation properties and versatility, while polystyrene foams maintain significant market share in packaging and construction applications. The Asia-Pacific region emerges as a key growth driver, supported by rapid urbanization and infrastructure development in countries like China and India. Environmental regulations and sustainability concerns are reshaping product development strategies, with manufacturers investing in eco-friendly alternatives and recycling technologies. The market's future growth will be influenced by technological advancements, regulatory frameworks, and the ability of companies to address environmental challenges while meeting increasing demand for high-performance insulation materials.

Rigid Foam Market Forecast - Projections for 2025-2032 period

The rigid foam market is projected to experience steady growth from 2025 through 2032, with the market expanding from $117.60 billion in 2026 to an estimated $188.52 billion by 2033. This represents a compound annual growth rate of 6.97%, driven by sustained demand across key end-use industries and technological advancements in foam manufacturing. The forecast period will likely see increased adoption of polyurethane foams, which are expected to maintain their market leadership due to superior performance characteristics. Regional growth will be particularly strong in Asia-Pacific and emerging markets, supported by infrastructure development and urbanization trends. The market will also benefit from increased focus on energy efficiency regulations and sustainable building practices. Technological innovations in foam chemistry and manufacturing processes are expected to create new growth opportunities, while environmental regulations will drive the development of eco-friendly alternatives and recycling solutions.

Rigid Foam Market Size and Share by Segmentation - Breakdown by {segmentData}

The rigid foam market segmentation reveals distinct patterns across different types and end-use industries. By type, polyurethane foams command the largest market share due to their excellent insulation properties and versatility across applications, followed by polystyrene foams which are widely used in packaging and construction. Polypropylene, polyethylene, and polyvinyl chloride foams occupy smaller but significant market segments, each serving specialized applications. In terms of end-use industries, the building and construction sector represents the largest consumer of rigid foams, driven by increasing demand for energy-efficient buildings and infrastructure development. The appliances segment follows as a major consumer, utilizing foams for thermal insulation in refrigerators and other household appliances. The automotive industry represents a growing segment, leveraging rigid foams for lightweight design and improved fuel efficiency. Packaging applications continue to show steady demand, particularly for protective packaging solutions.

Global Rigid Foam Market Size and Share by Region - Geographic distribution

The global rigid foam market exhibits varied regional distribution patterns, with Asia-Pacific emerging as the dominant region due to rapid industrialization, urbanization, and infrastructure development in countries like China, India, and Southeast Asian nations. North America and Europe maintain significant market shares, driven by established construction industries, stringent energy efficiency regulations, and technological innovation. The Middle East and Africa region shows growing potential, particularly in the Gulf Cooperation Council countries where construction activities and energy-efficient building initiatives are expanding. Latin America represents a developing market with increasing demand for insulation materials in residential and commercial construction. Regional market dynamics are influenced by local regulations, economic conditions, and industrial development patterns, with each region presenting unique opportunities and challenges for market participants.

Regional Analysis of the Rigid Foam Market - Detailed regional market performance

Regional analysis of the rigid foam market reveals distinct growth patterns and market dynamics across different geographic areas. Asia-Pacific leads in market growth, driven by massive infrastructure projects, rapid urbanization, and increasing energy efficiency awareness in developing economies. China and India represent particularly strong growth markets due to government initiatives promoting green building practices and energy conservation. North America demonstrates steady growth, supported by renovation activities, energy efficiency regulations, and technological advancements in foam manufacturing. Europe maintains a mature market with strong emphasis on environmental compliance and sustainable materials, driving innovation in eco-friendly foam solutions. The Middle East shows increasing adoption of rigid foams in construction projects, particularly in energy-efficient building designs. Latin America presents emerging opportunities, particularly in Brazil and Mexico, where construction activity and industrial development are expanding. Regional variations in regulatory frameworks, economic conditions, and industrial development create diverse market opportunities and challenges for manufacturers.

Leading Company Profiles in the Rigid Foam Market - Industry players and strategies

Leading companies in the rigid foam market employ diverse strategies to maintain competitive advantage and market leadership. BASF SE focuses on innovation and sustainability, developing advanced foam solutions with reduced environmental impact while expanding its global production capabilities. Dow Chemical Corporation leverages its extensive research and development resources to create high-performance foam products and maintain strong relationships with key end-use industries. Covestro AG emphasizes technological innovation and sustainable manufacturing processes, positioning itself as a leader in eco-friendly foam solutions. ARMACELL INTERNATIONAL HOLDING GMBH specializes in flexible foam technologies while expanding into rigid foam applications for construction and industrial markets. Compagnie de Saint-Gobain S.A. integrates rigid foam production with its broader building materials portfolio, offering comprehensive solutions to construction industry clients. These companies differentiate themselves through product innovation, global presence, and strategic partnerships with key industry players.

Porter's Five Forces Analysis of the Rigid Foam Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the rigid foam market. The threat of new entrants remains moderate due to high capital requirements for manufacturing facilities and the need for technological expertise. Bargaining power of suppliers is significant, particularly for petrochemical-based raw materials, though this is somewhat mitigated by the presence of multiple suppliers and the potential for backward integration by large manufacturers. The bargaining power of buyers varies across segments, with large construction companies and automotive manufacturers wielding considerable influence due to their volume purchases. The threat of substitutes exists from alternative insulation materials such as fiberglass, mineral wool, and emerging bio-based materials, though rigid foams maintain advantages in performance and versatility. Competitive rivalry is intense, driven by numerous global and regional players competing on price, quality, and innovation. The market's growth potential and technological complexity create barriers to entry while encouraging continuous innovation among existing players.

SWOT Analysis of the Rigid Foam Market - Strengths, weaknesses, opportunities, threats

The rigid foam market exhibits distinct strengths including superior insulation properties, lightweight characteristics, and versatility across multiple applications. The material's proven track record in energy conservation and building efficiency represents a significant advantage in markets increasingly focused on sustainability. However, weaknesses include dependence on petrochemical feedstocks, environmental concerns regarding production and disposal, and vulnerability to raw material price volatility. Opportunities abound in the development of bio-based and recyclable foam materials, expansion into emerging markets, and technological advancements in foam manufacturing processes. The growing emphasis on energy efficiency and sustainable construction practices creates substantial market potential. Threats include increasing environmental regulations, competition from alternative insulation materials, and potential supply chain disruptions. The market must also address challenges related to end-of-life management and recycling infrastructure development to maintain long-term sustainability.

Rigid Foam Market Value Chain Analysis - Industry structure and value flow

The rigid foam market value chain encompasses multiple stages from raw material sourcing through end-use applications. The chain begins with petrochemical companies supplying basic raw materials such as isocyanates, polyols, and blowing agents. These materials are processed by foam manufacturers who combine them through specialized chemical reactions to produce various types of rigid foam products. The manufacturing stage involves significant investment in production technology and quality control systems to ensure consistent product performance. Distribution channels include direct sales to large industrial customers, partnerships with building materials distributors, and relationships with original equipment manufacturers. End-use industries such as construction, automotive, and appliances integrate rigid foams into their products or use them directly for insulation purposes. Value is added at each stage through technological innovation, quality improvements, and customization to meet specific application requirements. The value chain is characterized by close relationships between suppliers and manufacturers, with increasing emphasis on sustainability and environmental compliance throughout the process.

Key Investment Insights in the Rigid Foam Market - Strategic investment recommendations

Strategic investment opportunities in the rigid foam market focus on several key areas that promise strong returns and market growth. Investment in research and development of eco-friendly foam materials represents a critical opportunity, as environmental regulations become increasingly stringent and demand for sustainable materials grows. Expansion of production capacity in emerging markets, particularly in Asia-Pacific and Latin America, offers significant growth potential due to rapid urbanization and infrastructure development. Investment in advanced manufacturing technologies, including automation and digital production systems, can improve efficiency and product quality while reducing costs. Strategic partnerships and acquisitions of specialized foam manufacturers can provide access to new technologies and market segments. Additionally, investment in recycling technologies and circular economy initiatives addresses environmental concerns while creating new revenue streams. Companies should also consider investments in supply chain optimization and vertical integration to mitigate raw material price volatility and ensure consistent quality.

Rigid Foam Market Conclusion - Summary and key takeaways

The rigid foam market presents a compelling growth opportunity characterized by strong demand drivers, technological innovation, and expanding applications across multiple industries. With a projected market size of $188.52 billion by 2033 and a steady CAGR of 6.97%, the industry demonstrates robust long-term potential. Key success factors include the ability to develop environmentally sustainable products, maintain technological leadership, and effectively serve diverse end-use markets. The market's future will be shaped by environmental regulations, raw material availability, and technological advancements in foam chemistry and manufacturing processes. Companies that successfully navigate these challenges while capitalizing on growth opportunities in emerging markets and sustainable product development will be well-positioned for success. The industry's evolution toward more sustainable practices and materials will likely define competitive advantage in the coming years, while maintaining focus on performance and cost-effectiveness remains essential for market leadership.

Research Methodology - How this research was conducted

The research methodology employed for this rigid foam market analysis combines multiple approaches to ensure comprehensive and accurate market assessment. Primary research involved interviews with industry experts, manufacturers, and end-users to gather firsthand insights on market trends, challenges, and opportunities. Secondary research encompassed extensive review of industry publications, company reports, technical journals, and market databases to validate findings and establish market size estimates. Data triangulation techniques were applied to cross-verify information from multiple sources, ensuring reliability of market projections and segment analysis. The research process included detailed analysis of historical market data, current industry dynamics, and future growth drivers to develop accurate market forecasts. Geographic segmentation was determined through analysis of regional economic indicators, construction activity, and industrial development patterns. The methodology also incorporated assessment of competitive landscape through analysis of company profiles, product portfolios, and strategic initiatives of key market players.

Research Scope - Coverage and limitations

The research scope for this rigid foam market analysis encompasses comprehensive coverage of major market segments, geographic regions, and industry applications. The study focuses on five primary foam types: polyurethane, polystyrene, polypropylene, polyethylene, and polyvinyl chloride foams, analyzing their respective market sizes, growth rates, and application areas. Geographic coverage includes major regions such as North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America, with detailed analysis of key countries within each region. The research examines major end-use industries including building & construction, appliances, packaging, and automotive sectors. Limitations of the study include the availability of certain regional market data, potential variations in reporting standards across different countries, and the dynamic nature of raw material prices affecting market projections. The analysis also acknowledges that emerging technologies and regulatory changes could impact market dynamics beyond the forecast period, requiring periodic updates to maintain accuracy.

Key Companies and Recent Developments in the Rigid Foam Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Key companies in the rigid foam market have demonstrated significant strategic developments and innovations in recent years. BASF SE has announced investments in bio-based foam technologies and expanded its production capacity in Asia-Pacific to meet growing regional demand. Dow Chemical Corporation launched new low-global-warming-potential foam products and formed strategic partnerships with construction companies to promote energy-efficient building solutions. Covestro AG introduced advanced polyurethane foam systems with improved insulation properties and reduced environmental impact, while expanding its recycling initiatives. Huntsman International LLC developed innovative foam solutions for electric vehicle applications and strengthened its presence in emerging markets through strategic acquisitions. ARMACELL INTERNATIONAL HOLDING GMBH launched new flexible-to-rigid foam conversion technologies and expanded its product portfolio for industrial applications. These companies continue to focus on sustainability, technological innovation, and geographic expansion to maintain competitive advantage in the evolving market landscape. Recent developments include investments in recycling technologies, partnerships for circular economy initiatives, and product launches targeting specific industry applications.