What is System in Package (SiP) Technology and why is it significant in the electronics industry?

System in Package (SiP) Technology represents an advanced packaging approach that integrates multiple integrated circuits (ICs) or dies, along with passive components, into a single package. Unlike traditional packaging methods, SiP technology enables the combination of diverse semiconductor components such as processors, memory, sensors, and power management units into a compact, unified solution. This integration approach offers significant advantages including reduced form factor, enhanced performance through shorter interconnection distances, improved power efficiency, and lower overall system costs. The technology has become increasingly vital in modern electronics, particularly for applications requiring miniaturization without compromising functionality, such as smartphones, wearables, IoT devices, and automotive electronics. As electronic devices continue to demand higher functionality in smaller footprints, SiP technology serves as a critical enabler for next-generation product development across multiple industries.

What are the primary drivers, restraints, challenges, and opportunities in the SiP technology market?

The SiP technology market is primarily driven by the escalating demand for compact, high-performance electronic devices across consumer electronics, automotive, and telecommunications sectors. The growing adoption of 5G technology, increasing IoT device proliferation, and the automotive industry's shift toward electric and autonomous vehicles are creating substantial growth opportunities. However, the market faces several restraints including high initial development costs, complex manufacturing processes, and technical challenges related to thermal management and signal integrity. The industry also encounters challenges in achieving standardization across different packaging technologies and maintaining quality control during mass production. Despite these obstacles, significant opportunities exist in emerging applications such as AI accelerators, medical devices, and advanced driver-assistance systems (ADAS). The ongoing miniaturization trend in electronics, coupled with the need for enhanced functionality in portable devices, continues to drive innovation and investment in SiP technology solutions.

What are the current and emerging trends shaping the SiP technology market?

The SiP technology market is experiencing several transformative trends that are reshaping the industry landscape. One prominent trend is the increasing adoption of advanced packaging technologies such as 2.5D and 3D integration, which enable higher component density and improved performance. The market is also witnessing a shift toward fan-out wafer-level packaging (FOWLP) and embedded die packaging solutions, driven by the need for thinner form factors and enhanced electrical performance. Another significant trend is the integration of heterogeneous components, allowing the combination of different semiconductor technologies within a single package. The industry is also seeing increased focus on sustainable packaging solutions and the development of environmentally friendly materials. Additionally, the rise of edge computing and AI applications is driving demand for specialized SiP solutions that can handle complex computational requirements while maintaining power efficiency. These trends collectively indicate a market moving toward more sophisticated, application-specific packaging solutions.

How did the COVID-19 pandemic impact the SiP technology market and what is the recovery trajectory?

The COVID-19 pandemic initially disrupted the SiP technology market through supply chain interruptions, manufacturing delays, and reduced consumer spending on electronic devices. The pandemic caused temporary factory closures, logistics challenges, and workforce limitations, particularly during the early stages of the crisis. However, the market demonstrated remarkable resilience as the pandemic accelerated digital transformation across industries, leading to increased demand for electronic devices supporting remote work, online education, and digital healthcare solutions. The recovery trajectory has been characterized by a strong rebound in demand for consumer electronics, automotive electronics, and telecommunications infrastructure. As economies reopened, the market experienced a surge in orders, particularly for 5G infrastructure and advanced computing solutions. The pandemic also highlighted the importance of supply chain resilience, prompting companies to diversify their supplier base and invest in more robust manufacturing capabilities, which is expected to strengthen the market's long-term growth prospects.

Who are the major competitors in the SiP technology market and how is market consolidation occurring?

The SiP technology market features a mix of established semiconductor companies and specialized packaging service providers competing for market share. Major players include ASE Group, Amkor Technology, Qualcomm Technologies, Samsung Electronics, and Texas Instruments, each bringing unique capabilities and market focus. The competitive landscape is characterized by continuous innovation, strategic partnerships, and mergers and acquisitions aimed at expanding technological capabilities and market reach. Market consolidation is occurring through several mechanisms, including vertical integration by semiconductor companies seeking to control the entire value chain, and horizontal expansion by packaging specialists acquiring complementary technologies. Companies are increasingly forming strategic alliances to combine expertise in design, manufacturing, and testing services. The competition is particularly intense in advanced packaging technologies, with companies investing heavily in research and development to differentiate their offerings and capture market share in high-growth segments such as 5G, automotive electronics, and AI applications.

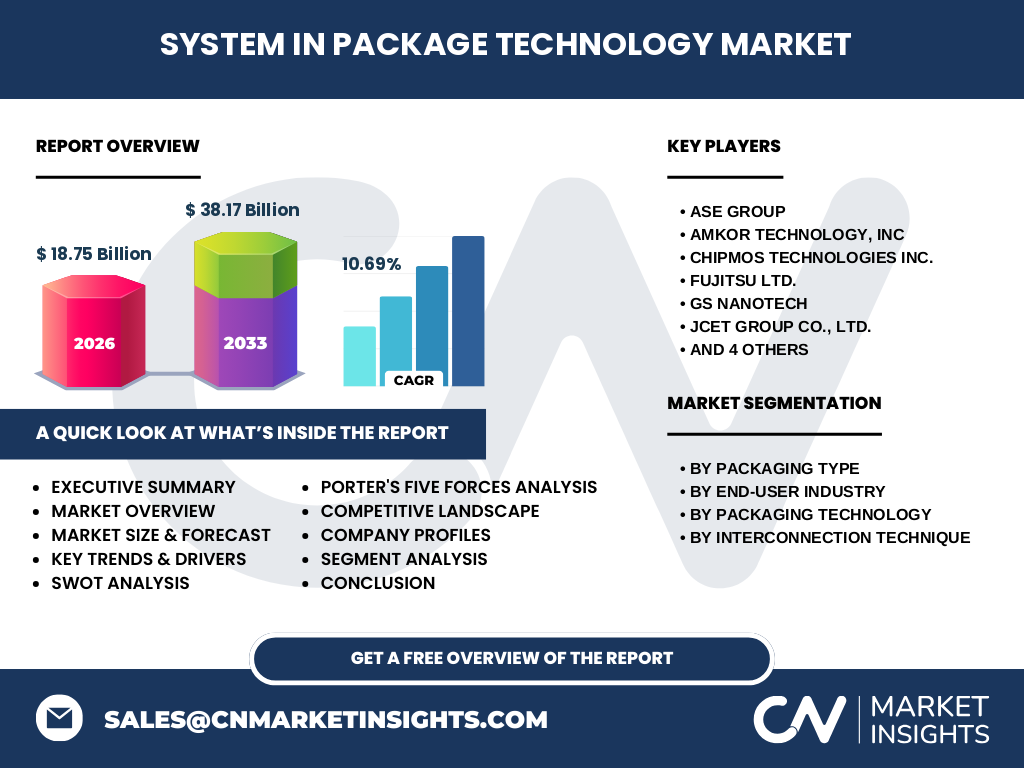

What are the key findings and high-level overview of the SiP technology market?

The SiP technology market is experiencing robust growth driven by the increasing demand for miniaturized, high-performance electronic devices across multiple industries. The market is projected to grow from $18.75 billion in 2026 to $38.17 billion by 2033, representing a compound annual growth rate (CAGR) of 10.69%. This growth is fueled by technological advancements in packaging solutions, expanding applications in automotive and telecommunications sectors, and the rising adoption of IoT devices. The market demonstrates strong potential across various packaging types, with flip-chip/wire-bond SiP, fan-out SiP, and embedded SiP technologies gaining significant traction. End-user industries such as automotive, consumer electronics, and telecommunications are driving demand, while packaging technologies like 2D, 2.5D, and 3D IC are evolving to meet increasingly complex requirements. The competitive landscape remains dynamic, with key players focusing on innovation, strategic partnerships, and capacity expansion to maintain their market positions.

What are the market projections for the SiP technology market from 2025 to 2032?

The SiP technology market is projected to experience substantial growth over the forecast period, with market size expected to reach $38.17 billion by 2033, up from $18.75 billion in 2026. This represents a compound annual growth rate (CAGR) of 10.69% during the forecast period. The growth trajectory indicates strong market momentum driven by increasing demand across various end-user industries and technological advancements in packaging solutions. The forecast period is expected to witness significant investments in research and development, particularly in advanced packaging technologies such as 2.5D and 3D integration. Market expansion is anticipated to be particularly strong in regions with robust electronics manufacturing capabilities and high adoption rates of advanced technologies. The growth projections also reflect the increasing importance of SiP technology in emerging applications such as 5G infrastructure, automotive electronics, and IoT devices, which are expected to drive sustained demand throughout the forecast period.

How is the SiP technology market segmented by packaging type, end-user industry, and packaging technology?

The SiP technology market exhibits diverse segmentation across multiple dimensions, reflecting the varied applications and technological requirements of different industries. By packaging type, the market encompasses flip-chip/wire-bond SiP, fan-out SiP, and embedded SiP solutions, each offering distinct advantages for specific applications. The end-user industry segmentation reveals strong demand from automotive, aerospace and defense, consumer electronics, and telecommunications sectors, with each vertical presenting unique requirements for performance, reliability, and form factor. In terms of packaging technology, the market is divided into 2D IC, 2.5D IC, and 3D IC solutions, with each technology level offering different capabilities in terms of component density and performance. The interconnection technique segment further diversifies the market, including small outline packages, flat packages, pin grid arrays, and surface mount technologies, each catering to specific design and manufacturing requirements. This comprehensive segmentation structure enables market participants to target specific applications and customer needs effectively.

How is the global SiP technology market distributed across different regions?

The global SiP technology market demonstrates varied distribution patterns across different geographic regions, influenced by factors such as manufacturing capabilities, technological adoption rates, and industry presence. Asia-Pacific region, particularly countries like China, South Korea, and Taiwan, dominates the market due to their established electronics manufacturing ecosystems and strong semiconductor industry presence. North America represents a significant market share, driven by advanced technological adoption, particularly in automotive and aerospace applications, and the presence of major technology companies. Europe shows steady growth, supported by the automotive industry's increasing adoption of advanced electronics and the region's focus on industrial automation. The market in emerging economies is also showing promising growth potential, driven by increasing electronics manufacturing activities and rising consumer demand for advanced electronic devices. Regional variations in market dynamics are influenced by factors such as government policies, infrastructure development, and the presence of key industry players.

What is the detailed regional performance of the SiP technology market?

The regional performance of the SiP technology market varies significantly across different geographic areas, reflecting diverse economic conditions, technological adoption rates, and industry concentrations. Asia-Pacific continues to lead the market, driven by strong electronics manufacturing capabilities in countries like China, South Korea, and Taiwan, where major semiconductor foundries and packaging facilities are concentrated. The region benefits from established supply chains, skilled workforce, and significant investments in advanced manufacturing technologies. North America demonstrates robust growth, particularly in automotive electronics and aerospace applications, supported by technological innovation and the presence of major technology companies. Europe shows steady advancement, with particular strength in automotive electronics and industrial applications, though facing some challenges related to manufacturing capacity and supply chain dependencies. Emerging markets in Latin America and the Middle East are showing increasing potential, driven by growing electronics consumption and expanding manufacturing capabilities, though from a smaller base compared to established markets.

Who are the leading companies in the SiP technology market and what are their key strategies?

The SiP technology market features several prominent companies that have established strong positions through technological innovation and strategic market approaches. Leading players include ASE Group, Amkor Technology, Qualcomm Technologies, Samsung Electronics, and Texas Instruments, each employing distinct strategies to maintain their competitive advantage. These companies focus on continuous research and development to advance packaging technologies, particularly in areas such as 2.5D and 3D integration. Strategic partnerships and collaborations are common, enabling companies to combine expertise and expand their technological capabilities. Many players are also investing in expanding their manufacturing capacities and establishing new facilities in strategic locations to better serve regional markets. Additionally, companies are increasingly focusing on developing application-specific solutions for high-growth segments such as automotive electronics, 5G infrastructure, and IoT devices. The competitive strategies also include vertical integration efforts to control more aspects of the value chain and enhance operational efficiency.

How does Porter's Five Forces analysis apply to the SiP technology market?

Porter's Five Forces analysis reveals important insights about the competitive dynamics of the SiP technology market. The threat of new entrants remains moderate due to the high capital requirements for advanced packaging facilities and the need for specialized technical expertise. The bargaining power of suppliers is significant, particularly for specialized materials and equipment required for advanced packaging processes. Buyer power varies across segments, with large electronics manufacturers having considerable influence due to their volume requirements and technical specifications. The threat of substitute technologies exists but is limited, as SiP solutions offer unique advantages in terms of miniaturization and performance integration. Competitive rivalry is intense, with numerous established players competing on technological innovation, cost efficiency, and service quality. The analysis indicates that while the market presents opportunities for growth, success requires significant investment in technology development and the ability to maintain strong relationships with both suppliers and customers.

What are the strengths, weaknesses, opportunities, and threats (SWOT) for the SiP technology market?

The SiP technology market demonstrates several key strengths, including its ability to enable miniaturization of electronic devices, improved performance through reduced interconnection distances, and cost advantages in high-volume production. The technology's flexibility in combining different semiconductor components and its suitability for various applications represent additional strengths. However, the market faces weaknesses such as high initial development costs, complex manufacturing processes, and technical challenges in thermal management and signal integrity. Significant opportunities exist in emerging applications such as 5G infrastructure, automotive electronics, and IoT devices, along with the potential for continued technological advancement in packaging solutions. Threats include intense competition from alternative packaging technologies, potential supply chain disruptions, and the rapid pace of technological change that could render current solutions obsolete. The market also faces challenges related to standardization and quality control across different manufacturing processes and regions.

How does the value chain analysis reveal the structure and flow of the SiP technology industry?

The value chain analysis of the SiP technology market reveals a complex ecosystem involving multiple stakeholders and processes. The chain begins with raw material suppliers providing essential components such as substrates, encapsulants, and interconnect materials. Semiconductor manufacturers then produce the individual dies that will be integrated into SiP solutions. Design houses and packaging specialists develop and implement the integration strategies, while testing and quality control facilities ensure product reliability. Distribution channels and electronics manufacturers complete the chain by incorporating SiP solutions into final products. Each stage adds value through specialized processes and expertise, with significant opportunities for differentiation and competitive advantage. The analysis also highlights potential bottlenecks and areas for optimization, particularly in testing and quality control processes, which are critical for ensuring the reliability of complex integrated packages. Understanding this value chain structure is essential for identifying strategic opportunities and potential areas for vertical integration or partnership development.

What are the key investment insights for the SiP technology market?

The SiP technology market presents several compelling investment opportunities driven by strong growth projections and technological advancement potential. Key investment insights suggest focusing on companies with strong research and development capabilities in advanced packaging technologies, particularly those working on 2.5D and 3D integration solutions. Investments in companies with established relationships with major electronics manufacturers and those positioned in high-growth application segments such as automotive electronics and 5G infrastructure appear particularly promising. The market also presents opportunities for investment in manufacturing capacity expansion, especially in regions with growing electronics production capabilities. Strategic investments in companies developing innovative solutions for thermal management and signal integrity challenges could yield significant returns as these technical issues become increasingly critical. Additionally, investments in companies focusing on sustainable packaging solutions and environmentally friendly materials align with growing industry trends and regulatory requirements. The market's projected CAGR of 10.69% and the increasing demand for miniaturized, high-performance electronic devices suggest strong long-term investment potential.

What are the key conclusions and takeaways from the SiP technology market analysis?

The SiP technology market analysis reveals a dynamic and growing industry with significant potential for continued expansion. The market's projected growth from $18.75 billion in 2026 to $38.17 billion by 2033, representing a CAGR of 10.69%, underscores its importance in the evolving electronics landscape. Key takeaways include the technology's critical role in enabling miniaturization and performance enhancement in electronic devices, the strong demand across multiple end-user industries, and the ongoing technological advancements in packaging solutions. The market's resilience, demonstrated through its recovery from COVID-19 disruptions, indicates robust underlying demand drivers. However, success in this market requires continuous innovation, significant investment in manufacturing capabilities, and the ability to address technical challenges such as thermal management and signal integrity. The competitive landscape remains intense, with companies focusing on strategic partnerships, vertical integration, and application-specific solutions to maintain their market positions. Overall, the SiP technology market represents a vital component of the electronics industry's future, with substantial opportunities for growth and innovation.

How was this research on the SiP technology market conducted?

This research on the SiP technology market was conducted through a comprehensive methodology combining multiple research approaches to ensure accuracy and reliability. The study utilized both primary and secondary research methods, including interviews with industry experts, analysis of company financial reports, and review of technical publications and market data. Primary research involved direct engagement with key industry participants, including manufacturers, technology providers, and end-users, to gather insights on market trends, technological developments, and future outlook. Secondary research encompassed extensive review of industry databases, trade publications, technical journals, and company websites to validate findings and gather additional market intelligence. The research methodology also incorporated data triangulation techniques to cross-verify information from multiple sources and ensure the accuracy of market projections. Market size calculations were based on both top-down and bottom-up approaches, considering various factors such as regional demand, application segments, and technological trends. The research team employed rigorous validation processes to ensure the reliability of all data points and projections presented in the analysis.

What is the scope and coverage of this SiP technology market research?

This SiP technology market research provides comprehensive coverage of the industry, focusing on key aspects that influence market dynamics and growth potential. The research scope encompasses detailed analysis of market segments including packaging types, end-user industries, packaging technologies, and interconnection techniques. Geographic coverage includes major regional markets, with particular attention to Asia-Pacific, North America, and Europe, while also considering emerging markets in other regions. The research examines various packaging technologies including 2D, 2.5D, and 3D IC solutions, along with different interconnection techniques and their applications across industries. The study also covers competitive landscape analysis, including profiles of major market players and their strategic initiatives. However, the research has certain limitations, primarily related to the availability of specific market data in some regions and the rapid pace of technological change that may affect long-term projections. The scope is designed to provide actionable insights for industry participants while maintaining focus on the most significant market drivers and trends.

Who are the key companies in the SiP technology market and what are their recent developments?

The SiP technology market features several key companies that are driving innovation and shaping industry trends through their technological advancements and strategic initiatives. Leading companies include ASE Group, Amkor Technology, ChipMOS TECHNOLOGIES INC., Fujitsu Ltd., GS Nanotech, JCET Group Co., Ltd., Qualcomm Technologies, Inc., Renesas Electronics Corporation, Samsung Electronics Co., Ltd., and Texas Instruments Incorporated. These companies have been actively pursuing various strategic developments to strengthen their market positions. Recent activities include investments in advanced packaging technologies, expansion of manufacturing capabilities, and strategic partnerships to enhance technological expertise. Companies are focusing on developing solutions for emerging applications such as 5G infrastructure, automotive electronics, and IoT devices. Many players are also investing in research and development to address technical challenges related to thermal management and signal integrity. The competitive landscape is characterized by continuous innovation, with companies regularly announcing new product launches, capacity expansions, and strategic collaborations to maintain their competitive advantage in the evolving market.